What is the Automotive Body-In-White Market Overview - Definition, scope, and significance?

The Automotive Body-In-White (BIW) market refers to the manufacturing and assembly of a vehicle's primary structural framework before the addition of doors, hoods, fenders, and other components. This crucial stage in automotive production involves welding or joining various sheet metal parts to create the skeletal structure of a vehicle. The BIW represents the foundation upon which all other vehicle components are mounted and plays a critical role in determining vehicle safety, performance, and overall quality. As the automotive industry continues to evolve with advancements in lightweight materials, electric vehicles, and autonomous driving technologies, the BIW market has become increasingly significant, serving as a key differentiator for manufacturers seeking to improve fuel efficiency, safety standards, and production efficiency.

What are the Automotive Body-In-White Market Drivers, Restraints, Challenges, and Opportunities?

The Automotive Body-In-White market is driven by several key factors, including the growing demand for lightweight vehicles to improve fuel efficiency and reduce emissions, stringent government regulations regarding vehicle safety and environmental standards, and the increasing adoption of electric vehicles requiring specialized structural designs. The rising focus on vehicle safety and crashworthiness also drives innovation in BIW design and materials. However, the market faces restraints such as high initial investment costs for advanced manufacturing equipment, complex supply chain management, and the challenge of balancing weight reduction with structural integrity. Additionally, the increasing complexity of vehicle designs and the need for customization pose significant challenges. Opportunities exist in the development of new materials like advanced high-strength steel and aluminum alloys, the integration of smart manufacturing technologies, and the growing demand for electric and autonomous vehicles requiring specialized BIW structures.

What are the Automotive Body-In-White Market Growth Trends?

The Automotive Body-In-White market is experiencing several significant growth trends that are reshaping the industry landscape. One prominent trend is the increasing adoption of lightweight materials such as aluminum, magnesium, and carbon fiber reinforced polymers (CFRP) to reduce vehicle weight and improve fuel efficiency. Another key trend is the integration of advanced manufacturing technologies, including robotics, automation, and Industry 4.0 solutions, to enhance production efficiency and quality control. The market is also witnessing a shift towards modular and flexible manufacturing systems that can accommodate diverse vehicle platforms and customization requirements. Additionally, there is a growing focus on sustainability and recyclability in BIW design, with manufacturers exploring eco-friendly materials and production processes. The rise of electric vehicles is driving demand for specialized BIW structures that can accommodate battery packs and provide enhanced safety features, while the increasing complexity of vehicle designs is pushing the boundaries of traditional BIW manufacturing techniques.

What is the COVID-19 Impact on the Automotive Body-In-White Market?

The COVID-19 pandemic had a significant impact on the Automotive Body-In-White market, causing widespread disruptions across the global automotive supply chain. During the initial phases of the pandemic, manufacturing facilities were forced to shut down or operate at reduced capacity, leading to production delays and supply shortages. The sudden drop in consumer demand for vehicles resulted in decreased orders for BIW components and assemblies, affecting manufacturers' revenue streams. However, as the automotive industry began to recover, the BIW market demonstrated resilience and adaptability. Manufacturers implemented stringent safety protocols, invested in automation to reduce human contact, and explored digital solutions for remote collaboration and design optimization. The pandemic also accelerated the adoption of electric vehicles and sustainable manufacturing practices, as governments and consumers prioritized environmental concerns. Looking ahead, the BIW market is expected to benefit from the industry's renewed focus on supply chain resilience, localization of production, and the integration of advanced technologies to enhance manufacturing flexibility and efficiency.

What is the Automotive Body-In-White Market Competitive Landscape?

The Automotive Body-In-White market features a competitive landscape characterized by a mix of established automotive suppliers, specialized BIW manufacturers, and emerging technology providers. Major players in the market include global automotive giants such as Magna International Inc., ThyssenKrupp AG, and Tata Steel Limited, alongside specialized BIW manufacturers like Gestamp Automocion S.A. and Kuka AG. The competitive environment is shaped by factors such as technological innovation, manufacturing capabilities, global presence, and the ability to provide integrated solutions across the automotive value chain. Companies are increasingly focusing on developing lightweight materials, advanced manufacturing processes, and smart factory solutions to gain a competitive edge. Strategic partnerships, mergers, and acquisitions are common strategies employed by market players to expand their product portfolios, enter new geographic markets, and strengthen their technological capabilities. The market also sees competition from regional players who offer cost-effective solutions and cater to local market demands, particularly in emerging economies.

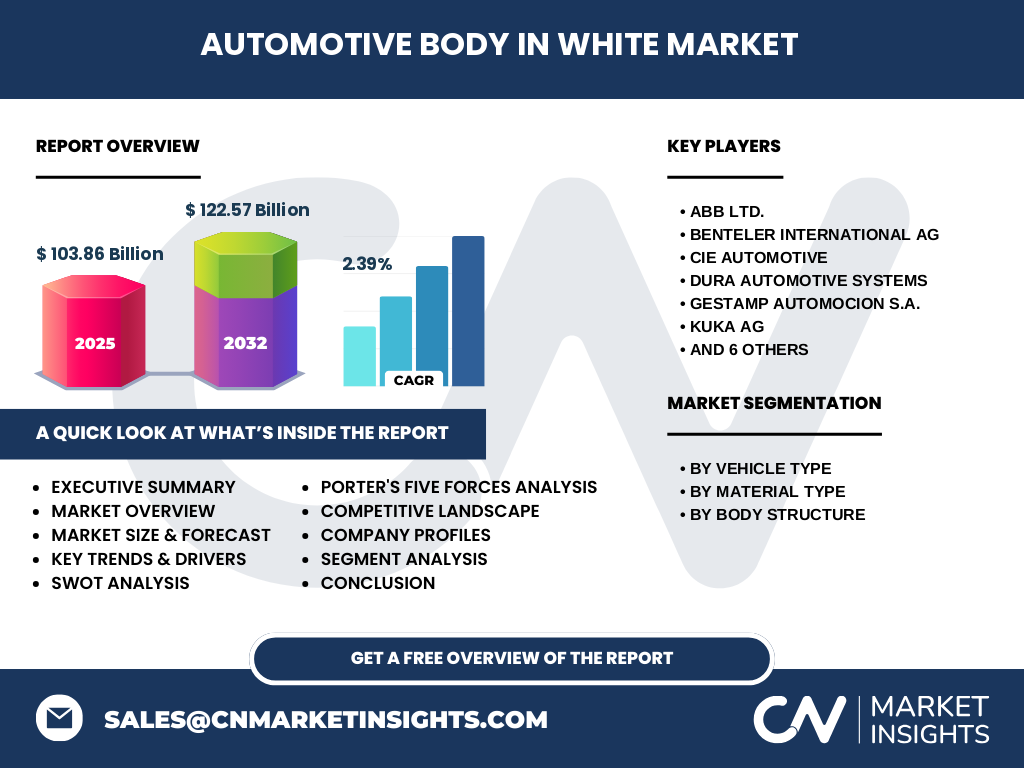

What is the Executive Summary of the Automotive Body-In-White Market?

The Automotive Body-In-White market is poised for steady growth, with the market size projected to increase from USD 103.86 billion in 2025 to USD 122.57 billion by 2032, representing a compound annual growth rate (CAGR) of 2.39%. This growth is driven by the increasing demand for lightweight vehicles, stringent safety regulations, and the rising adoption of electric vehicles. The market is segmented by vehicle type, material type, and body structure, with passenger cars and steel materials currently dominating the market share. However, the growing popularity of aluminum and advanced high-strength steel is expected to drive significant changes in material preferences. Geographically, the market is witnessing strong growth in Asia-Pacific, particularly in China and India, due to the expanding automotive manufacturing base and increasing vehicle production. Key players in the market are focusing on technological innovation, strategic partnerships, and capacity expansion to maintain their competitive edge and capitalize on emerging opportunities in the evolving automotive landscape.

What is the Automotive Body-In-White Market Forecast for 2025-2032?

The Automotive Body-In-White market is forecasted to experience steady growth over the period from 2025 to 2032, with the market size expected to increase from USD 103.86 billion in 2025 to USD 122.57 billion by 2032. This represents a compound annual growth rate (CAGR) of 2.39% over the forecast period. The growth trajectory is driven by several factors, including the increasing demand for lightweight vehicles to improve fuel efficiency and reduce emissions, the rising adoption of electric vehicles requiring specialized structural designs, and the implementation of stringent safety regulations worldwide. The market is also expected to benefit from technological advancements in manufacturing processes, such as the integration of robotics and automation, as well as the development of new materials like advanced high-strength steel and aluminum alloys. However, the growth rate may be influenced by factors such as raw material price fluctuations, geopolitical tensions affecting supply chains, and the pace of electric vehicle adoption across different regions.

What is the Automotive Body-In-White Market Size and Share by Segmentation?

The Automotive Body-In-White market is segmented based on vehicle type, material type, and body structure, each contributing to the overall market dynamics. By vehicle type, the market is divided into passenger cars and commercial vehicles, with passenger cars currently holding a larger market share due to their higher production volumes and diverse model offerings. The material type segment includes aluminum, steel, magnesium, and carbon fiber reinforced polymer (CFRP), with steel dominating the market share due to its cost-effectiveness and widespread availability. However, aluminum is gaining traction, particularly in premium and electric vehicle segments, due to its lightweight properties. The body structure segment is categorized into frame-mounted structure and monocoque structure, with monocoque structures being more prevalent in passenger cars for their superior safety and weight reduction benefits. The market share distribution among these segments is influenced by factors such as vehicle type preferences, material cost and availability, and regional manufacturing trends.

What is the Global Automotive Body-In-White Market Size and Share by Region?

The global Automotive Body-In-White market exhibits varying growth patterns and market shares across different regions, reflecting the diverse automotive manufacturing landscapes and consumer preferences worldwide. Asia-Pacific currently holds the largest market share, driven by the presence of major automotive manufacturing hubs in countries like China, Japan, and South Korea. The region's dominance is attributed to its large population, increasing disposable incomes, and the growing demand for vehicles, particularly in emerging economies. North America and Europe follow as significant markets, characterized by advanced automotive technologies, stringent safety regulations, and a strong focus on electric vehicle adoption. These regions are witnessing increased investments in lightweight materials and advanced manufacturing processes to meet evolving industry standards. Latin America and the Middle East & Africa represent emerging markets with growing automotive sectors, offering potential opportunities for market expansion. The regional market shares are influenced by factors such as vehicle production volumes, government policies, technological advancements, and the presence of key automotive manufacturers and suppliers.

What is the Regional Analysis of the Automotive Body-In-White Market?

The Automotive Body-In-White market exhibits distinct characteristics and growth patterns across different regions, reflecting the unique automotive manufacturing landscapes and market dynamics. In Asia-Pacific, particularly in China, Japan, and South Korea, the market is driven by the presence of major automotive manufacturing hubs, large-scale vehicle production, and increasing investments in electric vehicle technologies. The region benefits from a skilled workforce, established supply chains, and government initiatives promoting domestic manufacturing. North America, led by the United States and Canada, focuses on technological innovation, with a strong emphasis on lightweight materials and advanced manufacturing processes. The region's market is characterized by the presence of major automotive OEMs and a well-developed supplier network. Europe, with countries like Germany, France, and the UK at the forefront, emphasizes sustainability and electric vehicle adoption, driving demand for specialized BIW structures. The region is known for its stringent safety regulations and high-quality manufacturing standards. Latin America and the Middle East & Africa, while smaller markets, are experiencing growth due to increasing vehicle production and investments in automotive manufacturing capabilities.

Who are the Leading Company Profiles in the Automotive Body-In-White Market?

The Automotive Body-In-White market features several prominent players who have established themselves as leaders through their technological expertise, global presence, and comprehensive product offerings. ABB Ltd. is recognized for its advanced robotics and automation solutions, which are crucial for efficient BIW manufacturing processes. Benteler International AG specializes in lightweight vehicle structures and innovative material solutions, catering to the growing demand for fuel-efficient vehicles. CIE Automotive focuses on providing integrated BIW solutions, leveraging its expertise in metal forming and assembly technologies. Dura Automotive Systems is known for its advanced manufacturing capabilities and focus on electric vehicle structures. Gestamp Automocion S.A. stands out for its global presence and expertise in metal forming technologies. Kuka AG offers comprehensive automation solutions for BIW manufacturing, including robotics and software systems. Magna International Inc. is a major player with a wide range of BIW products and services, supported by its global manufacturing footprint. Martinrea International Inc. specializes in metal forming and lightweighting solutions. Norsk Hydro ASA is a key supplier of aluminum products for the automotive industry. TECOSIM Group provides engineering and simulation services for BIW design and optimization. Tata Steel Limited offers advanced high-strength steel solutions for BIW applications. ThyssenKrupp AG is known for its innovative material technologies and manufacturing expertise in the automotive sector.

What is the Porter's Five Forces Analysis of the Automotive Body-In-White Market?

The Porter's Five Forces analysis of the Automotive Body-In-White market reveals a competitive landscape shaped by several key factors. The threat of new entrants is moderate, as the market requires significant capital investment, advanced technological capabilities, and established relationships with automotive OEMs. However, the growing demand for electric vehicles and new manufacturing technologies may lower barriers to entry for innovative startups. The bargaining power of buyers, primarily automotive OEMs, is high due to their large purchase volumes and ability to switch suppliers. This pressure forces BIW manufacturers to continuously improve quality, reduce costs, and offer innovative solutions. The bargaining power of suppliers is moderate, with key raw material suppliers having some influence due to the specialized nature of materials used in BIW manufacturing. The threat of substitute products is low, as BIW structures are essential components of vehicle manufacturing with limited alternatives. Competitive rivalry in the market is intense, with numerous global and regional players competing on factors such as technology, quality, price, and customer service. The market is characterized by ongoing consolidation through mergers and acquisitions as companies seek to expand their capabilities and market share.

What is the SWOT Analysis of the Automotive Body-In-White Market?

The SWOT analysis of the Automotive Body-In-White market reveals a complex landscape of strengths, weaknesses, opportunities, and threats. Strengths of the market include the essential nature of BIW structures in vehicle manufacturing, the presence of established global players with advanced technological capabilities, and the increasing demand for lightweight and fuel-efficient vehicles. The market also benefits from ongoing innovations in materials and manufacturing processes, as well as the growing adoption of electric vehicles requiring specialized BIW designs. However, weaknesses exist in the form of high initial investment costs for advanced manufacturing equipment, complex supply chain management, and the challenge of balancing weight reduction with structural integrity. Opportunities in the market include the development of new materials like advanced high-strength steel and aluminum alloys, the integration of smart manufacturing technologies, and the expansion of electric and autonomous vehicle production. Threats to the market include raw material price fluctuations, geopolitical tensions affecting global supply chains, and the potential for disruptive technologies that could alter traditional BIW manufacturing processes.

What is the Automotive Body-In-White Market Value Chain Analysis?

The Automotive Body-In-White market value chain encompasses a series of interconnected activities that transform raw materials into finished vehicle structures. The chain begins with raw material suppliers who provide essential inputs such as steel, aluminum, and other metals used in BIW manufacturing. These materials are then processed by component manufacturers who produce individual parts through processes like stamping, forming, and welding. The next stage involves BIW system integrators who assemble these components into complete body structures using advanced manufacturing techniques such as robotics and automation. Original Equipment Manufacturers (OEMs) then incorporate these BIW structures into their vehicle assembly processes. Throughout the value chain, various support activities play crucial roles, including research and development for new materials and manufacturing technologies, quality control and testing, logistics and supply chain management, and after-sales services. The value chain is characterized by a high degree of specialization, with companies focusing on specific stages of the process to optimize efficiency and quality. Collaboration and integration among value chain partners are essential for ensuring seamless production and meeting the evolving demands of the automotive industry.

What are the Key Investment Insights in the Automotive Body-In-White Market?

The Automotive Body-In-White market presents several key investment insights for stakeholders looking to capitalize on emerging opportunities. One significant area of investment is in advanced manufacturing technologies, including robotics, automation, and Industry 4.0 solutions, which can enhance production efficiency, quality control, and flexibility. The development and adoption of lightweight materials such as advanced high-strength steel, aluminum alloys, and carbon fiber reinforced polymers (CFRP) represent another promising investment avenue, driven by the increasing demand for fuel-efficient and electric vehicles. Investments in research and development for new material technologies and manufacturing processes are crucial for maintaining a competitive edge in the market. The growing electric vehicle segment offers opportunities for specialized BIW structures that can accommodate battery packs and provide enhanced safety features. Additionally, investments in sustainable manufacturing practices and recyclable materials align with the industry's focus on environmental responsibility and can provide long-term competitive advantages. Strategic partnerships and collaborations along the value chain can also offer investment opportunities, enabling companies to leverage complementary strengths and expand their market presence.

What is the Automotive Body-In-White Market Conclusion?

The Automotive Body-In-White market is a critical and dynamic segment of the automotive industry, playing a pivotal role in vehicle safety, performance, and manufacturing efficiency. As the market continues to evolve, driven by trends such as lightweighting, electric vehicle adoption, and advanced manufacturing technologies, companies operating in this space must remain agile and innovative to maintain their competitive edge. The market's steady growth, projected to reach USD 122.57 billion by 2032 with a CAGR of 2.39%, reflects the ongoing importance of BIW structures in vehicle manufacturing. Key players are focusing on technological advancements, strategic partnerships, and capacity expansion to capitalize on emerging opportunities and address challenges such as raw material price fluctuations and complex supply chain management. The increasing emphasis on sustainability and recyclability in BIW design presents both challenges and opportunities for manufacturers. As the automotive industry continues to transform, the BIW market will remain at the forefront of innovation, playing a crucial role in shaping the future of vehicle design and manufacturing.

What is the Research Methodology for this Automotive Body-In-White Market Report?

The research methodology for this Automotive Body-In-White market report involved a comprehensive and systematic approach to gather, analyze, and interpret data from multiple sources. The process began with extensive secondary research, including the review of industry reports, company annual reports, press releases, and relevant publications from automotive associations and regulatory bodies. This was complemented by primary research, which involved interviews with industry experts, key opinion leaders, and executives from leading companies in the BIW market. The research team also conducted surveys and gathered data from automotive manufacturers and suppliers to gain insights into market trends, challenges, and opportunities. Data triangulation was employed to cross-verify information from multiple sources, ensuring the accuracy and reliability of the findings. The market size and forecast were determined using a combination of top-down and bottom-up approaches, considering factors such as vehicle production volumes, material usage trends, and regional market dynamics. The research methodology also incorporated Porter's Five Forces analysis and SWOT analysis to provide a comprehensive understanding of the market's competitive landscape and strategic positioning.

What is the Research Scope of this Automotive Body-In-White Market Report?

The research scope of this Automotive Body-In-White market report encompasses a comprehensive analysis of the global market, covering key aspects such as market size, growth trends, competitive landscape, and regional dynamics. The report focuses on the period from 2025 to 2032, providing historical data for 2025 and forecast projections for the subsequent years. The scope includes a detailed segmentation of the market by vehicle type (passenger cars and commercial vehicles), material type (aluminum, steel, magnesium, and carbon fiber reinforced polymer), and body structure (frame-mounted structure and monocoque structure). The research covers major geographic regions, including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, providing insights into regional market performance and growth opportunities. The report also examines key industry trends, drivers, restraints, and challenges affecting the market, as well as the impact of COVID-19 on the industry. Additionally, the research scope includes an analysis of leading company profiles, recent developments, and strategic initiatives in the market, offering a holistic view of the competitive landscape and future market prospects.

Who are the Key Companies and Recent Developments in the Automotive Body-In-White Market?

The Automotive Body-In-White market features several key companies that are driving innovation and shaping the industry landscape. ABB Ltd. has recently announced advancements in its robotics and automation solutions, focusing on enhancing flexibility and efficiency in BIW manufacturing processes. Benteler International AG has introduced new lightweight vehicle structures using advanced high-strength steel and aluminum alloys, catering to the growing demand for fuel-efficient vehicles. CIE Automotive has expanded its global presence through strategic acquisitions and partnerships, strengthening its position in the BIW market. Dura Automotive Systems has launched innovative electric vehicle structures, leveraging its expertise in lightweighting and advanced manufacturing technologies. Gestamp Automocion S.A. has invested in new production facilities and technologies to increase its capacity and meet the rising demand for BIW components. Kuka AG has unveiled next-generation robotics and software solutions for BIW assembly, incorporating artificial intelligence and machine learning capabilities. Magna International Inc. has announced collaborations with automotive OEMs to develop integrated BIW solutions for electric and autonomous vehicles. Martinrea International Inc. has focused on expanding its product portfolio with new aluminum and advanced high-strength steel offerings. Norsk Hydro ASA has invested in sustainable aluminum production technologies to meet the automotive industry's growing demand for eco-friendly materials. TECOSIM Group has introduced advanced simulation and engineering services for optimizing BIW design and performance. Tata Steel Limited has launched new high-strength steel grades specifically designed for BIW applications, offering improved crashworthiness and weight reduction. ThyssenKrupp AG has announced strategic partnerships to develop innovative material solutions and manufacturing processes for the evolving automotive industry.