Aircraft Valve Market Overview - Definition, scope, and significance

Aircraft valves are critical components in aerospace systems that control the flow of fluids such as fuel, hydraulic fluid, and air conditioning refrigerants. These precision-engineered devices regulate pressure, direction, and rate of fluid movement across various aircraft systems. The Aircraft Valve Market encompasses the manufacturing, distribution, and maintenance of these essential components for commercial, military, and general aviation aircraft. This market is significant because valves ensure the safe and efficient operation of aircraft systems, directly impacting flight safety, fuel efficiency, and overall aircraft performance. As the global aviation industry continues to expand, the demand for reliable, lightweight, and high-performance aircraft valves grows proportionally, making this a vital segment within the broader aerospace supply chain.

Aircraft Valve Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the Aircraft Valve Market include increasing global air passenger traffic, rising demand for new commercial aircraft, and the growing military aviation sector. Technological advancements in valve design, such as the development of lightweight composite materials and smart valve systems, are also propelling market growth. However, the market faces restraints including high manufacturing costs, stringent regulatory requirements, and supply chain disruptions. Challenges include the need for continuous innovation to meet evolving aircraft performance standards and the complexity of integrating new valve technologies into existing aircraft systems. Opportunities exist in the aftermarket segment, driven by aging aircraft fleets requiring maintenance and replacement parts, as well as the potential for growth in emerging markets where aviation infrastructure is rapidly expanding.

Aircraft Valve Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the Aircraft Valve Market include the increasing adoption of lightweight materials such as titanium and advanced polymers to reduce aircraft weight and improve fuel efficiency. There is also a growing trend toward miniaturization and integration of multiple valve functions into single units to save space and reduce complexity. Emerging trends include the development of smart valves with integrated sensors for real-time monitoring and predictive maintenance, as well as the increasing use of additive manufacturing (3D printing) for rapid prototyping and production of complex valve geometries. Additionally, the market is witnessing a shift toward more environmentally friendly valve designs that reduce emissions and improve overall aircraft sustainability, aligning with the aviation industry's broader environmental goals.

COVID-19 Impact on the Aircraft Valve Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant negative impact on the Aircraft Valve Market, primarily due to the dramatic reduction in air travel and subsequent decrease in aircraft production and deliveries. Many aircraft manufacturers temporarily halted or reduced production, leading to decreased demand for aircraft valves. The aftermarket segment also suffered as grounded aircraft required less maintenance. However, the market is showing signs of recovery as air travel demand gradually returns to pre-pandemic levels. The recovery trajectory is supported by increasing passenger confidence, government stimulus packages for the aviation industry, and the resumption of aircraft production. Additionally, the pandemic has accelerated certain trends, such as the adoption of digital technologies for remote monitoring and maintenance of aircraft systems, which may benefit the valve market in the long term.

Aircraft Valve Market Competitive Landscape - Major competitors and market consolidation

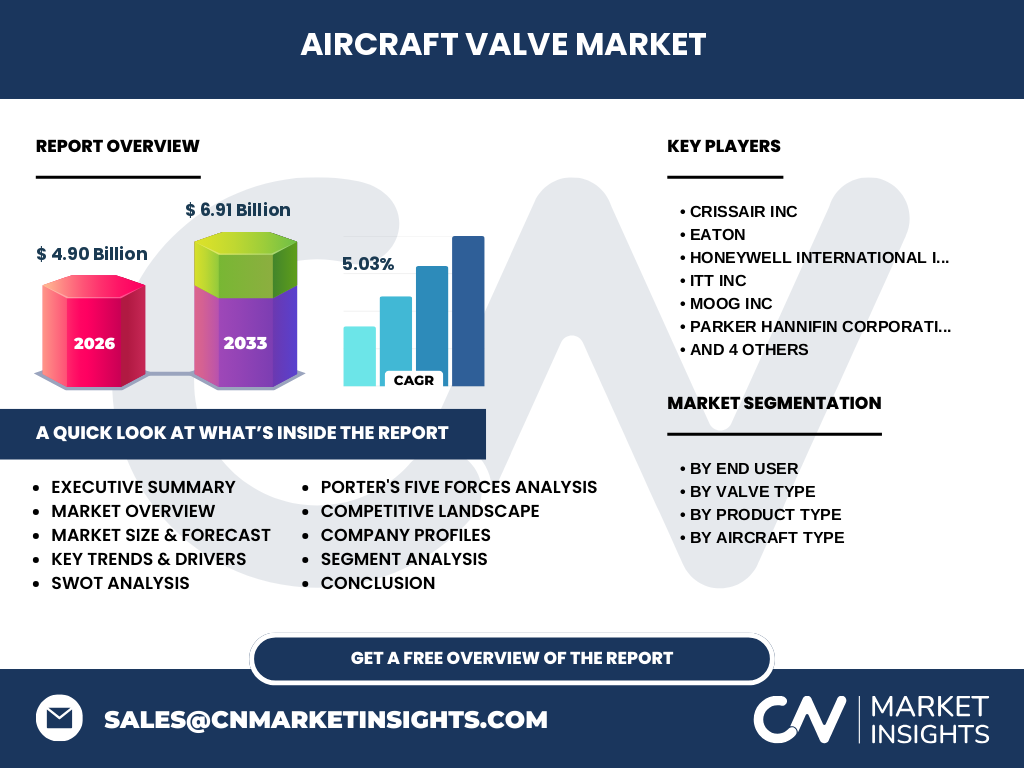

The Aircraft Valve Market is characterized by a moderately consolidated competitive landscape, with several key players dominating the market. Major competitors include Crissair Inc, Eaton, Honeywell International Inc, ITT Inc, Moog Inc, Parker Hannifin Corporation, Raytheon Technologies Corp, Safran Group, Triumph Group Inc, and Woodward Inc. These companies compete based on factors such as product quality, technological innovation, price, and customer relationships. The market has seen some consolidation through mergers and acquisitions, with larger companies acquiring smaller specialized firms to expand their product portfolios and technological capabilities. Competition is intense in terms of developing valves that meet increasingly stringent performance and environmental standards while also addressing the demand for cost reduction from aircraft manufacturers and operators.

Executive Summary - High-level overview and key findings about Aircraft Valve Market

The Aircraft Valve Market is a critical component of the aerospace industry, valued at 4.90 Billion in 2026 and projected to grow to 6.91 Billion by 2033, representing a CAGR of 5.03%. The market is driven by increasing global air traffic, technological advancements in valve design, and the growing demand for new aircraft. Key segments include fuel system valves, hydraulic system valves, air conditioning system valves, and lubrication systems valves, with applications across fixed-wing and rotary-wing aircraft. The market serves both Original Equipment Manufacturers (OEMs) and Maintenance, Repair, and Overhaul (MRO) providers. While facing challenges such as high manufacturing costs and regulatory hurdles, the market presents significant opportunities in emerging markets and the aftermarket segment. The competitive landscape is dominated by established aerospace companies that are continuously innovating to meet evolving industry demands.

Aircraft Valve Market Forecast - Projections for 2025-2032 period

The Aircraft Valve Market is expected to experience steady growth from 2025 to 2032, with projections indicating an increase from 4.90 Billion in 2026 to 6.91 Billion by 2033. This represents a compound annual growth rate (CAGR) of 5.03% over the forecast period. The growth is anticipated to be driven by several factors, including the recovery of the global aviation industry post-COVID-19, increasing demand for new commercial and military aircraft, and the ongoing replacement of aging aircraft fleets. The aftermarket segment is expected to see particularly strong growth as airlines seek to extend the life of existing aircraft. Technological advancements, such as the development of smart valves and the use of advanced materials, are also expected to contribute to market growth. Regional markets in Asia-Pacific and the Middle East are projected to experience above-average growth rates due to expanding aviation infrastructure and increasing air travel demand.

Aircraft Valve Market Size and Share by Segmentation - Breakdown by {segmentData}

The Aircraft Valve Market is segmented by end user, valve type, product type, and aircraft type. By end user, the market is divided into OEMs and MRO providers, with OEMs typically accounting for a larger share due to the demand for new aircraft production. In terms of valve type, the market includes pilot valves, poppet valves, and flapper-nozzle valves, with pilot valves often being the most prevalent due to their widespread use in aircraft systems. By product type, the market is segmented into fuel system valves, hydraulic system valves, air conditioning system valves, and lubrication systems valves. Fuel system valves generally represent the largest segment due to the critical nature of fuel management in aircraft operations. By aircraft type, the market is divided into fixed-wing and rotary-wing aircraft, with fixed-wing aircraft typically accounting for a larger share due to the higher volume of commercial aircraft production compared to helicopters.

Global Aircraft Valve Market Size and Share by Region - Geographic distribution

While specific regional market share data is not provided, the global Aircraft Valve Market is expected to be distributed across key regions including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America and Europe are likely to hold significant market shares due to the presence of major aircraft manufacturers and established aerospace industries. The Asia-Pacific region is anticipated to experience the highest growth rate, driven by increasing aircraft orders from airlines in countries like China and India, as well as the expansion of local aircraft manufacturing capabilities. The Middle East is also expected to see substantial growth due to investments in aviation infrastructure and the presence of major airline hubs. Latin America and Africa may have smaller market shares but are expected to show steady growth as air travel demand increases in these regions.

Regional Analysis of the Aircraft Valve Market - Detailed regional market performance

The Aircraft Valve Market performance varies significantly across different regions. North America, particularly the United States, is expected to maintain a strong market position due to the presence of major aircraft manufacturers like Boeing and a robust aerospace supply chain. Europe, with companies like Airbus and a concentration of tier-1 suppliers, is also likely to be a significant market. The Asia-Pacific region is projected to be the fastest-growing market, driven by increasing aircraft orders from airlines in China, India, and Southeast Asian countries, as well as the development of local aerospace industries in these nations. Countries like Japan and South Korea, with their advanced manufacturing capabilities, are also contributing to regional market growth. The Middle East, while a smaller market in absolute terms, is expected to see above-average growth due to investments in aviation infrastructure and the presence of major airline hubs in countries like the UAE and Qatar. Latin America and Africa, while currently smaller markets, are expected to show steady growth as air travel demand increases in these regions.

Leading Company Profiles in the Aircraft Valve Market - Industry players and strategies

The Aircraft Valve Market is dominated by several key players, each with their own strategies and market positioning. Crissair Inc is known for its high-performance valves and actuators, focusing on innovation and quality. Eaton, a diversified industrial manufacturer, leverages its broad portfolio to offer comprehensive valve solutions for various aircraft systems. Honeywell International Inc, with its extensive aerospace experience, provides advanced valve technologies integrated with its other aircraft systems. ITT Inc specializes in critical components for harsh environments, including aircraft valves designed for extreme conditions. Moog Inc is recognized for its precision control components, including high-performance valves for both commercial and military aircraft. Parker Hannifin Corporation offers a wide range of aerospace valves, emphasizing reliability and efficiency. Raytheon Technologies Corp, through its Collins Aerospace division, provides integrated valve systems as part of larger aircraft subsystems. Safran Group, a major aerospace supplier, focuses on lightweight and fuel-efficient valve designs. Triumph Group Inc specializes in complex assemblies, including integrated valve systems. Woodward Inc, known for its control solutions, offers advanced valve technologies for both aircraft and industrial applications.

Porter's Five Forces Analysis of the Aircraft Valve Market - Competitive forces assessment

Porter's Five Forces analysis of the Aircraft Valve Market reveals the following competitive dynamics: The threat of new entrants is relatively low due to high capital requirements, stringent regulatory standards, and the need for established relationships with aircraft manufacturers. The bargaining power of buyers (aircraft manufacturers and airlines) is moderate to high, as they often have multiple suppliers to choose from and can exert pressure on prices and quality. The bargaining power of suppliers is moderate, with suppliers of specialized materials and components having some leverage, but the presence of multiple suppliers balancing this power. The threat of substitute products is low, as aircraft valves have highly specialized functions with few alternatives. Competitive rivalry is intense, with established players competing on technology, quality, price, and customer relationships. The market is characterized by ongoing innovation and the need to meet increasingly stringent performance and environmental standards, which drives continuous improvement and differentiation among competitors.

SWOT Analysis of the Aircraft Valve Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Aircraft Valve Market reveals the following: Strengths include the critical nature of valves in aircraft systems, ensuring consistent demand; established relationships with major aircraft manufacturers; and ongoing technological advancements in valve design and materials. Weaknesses include high manufacturing costs, vulnerability to economic downturns in the aviation industry, and the complexity of meeting diverse regulatory requirements across different regions. Opportunities exist in the growing aftermarket segment, expansion into emerging markets, and the development of smart valves with integrated monitoring capabilities. Threats include intense competition leading to pricing pressures, potential supply chain disruptions, and the risk of technological obsolescence as new aircraft designs may require different valve specifications. Additionally, the market faces threats from global economic uncertainties and potential changes in aviation regulations that could impact demand for certain types of valves.

Aircraft Valve Market Value Chain Analysis - Industry structure and value flow

The Aircraft Valve Market value chain consists of several key stages: Raw material suppliers provide specialized metals, alloys, and polymers used in valve manufacturing. Component manufacturers produce individual parts and sub-assemblies for valves. Valve manufacturers design, engineer, and assemble the final products, often incorporating advanced technologies such as smart sensors and control systems. Distributors and suppliers then deliver these valves to aircraft manufacturers (OEMs) or maintenance providers (MROs). Aircraft manufacturers integrate the valves into their systems during the production process, while MRO providers install and maintain valves in existing aircraft. The value flow is characterized by high levels of quality control and certification at each stage, reflecting the critical nature of these components in aircraft safety. The value chain also includes extensive research and development efforts, particularly in areas such as materials science and miniaturization, to meet evolving industry demands for lighter, more efficient, and more reliable valve systems.

Key Investment Insights in the Aircraft Valve Market - Strategic investment recommendations

Key investment insights for the Aircraft Valve Market suggest focusing on companies that are leaders in technological innovation, particularly those developing smart valves with integrated monitoring capabilities and those utilizing advanced materials to reduce weight and improve efficiency. Investments in firms with strong aftermarket services and MRO capabilities may also be attractive, given the growing demand for maintenance of aging aircraft fleets. The market for valves in emerging aircraft segments, such as electric and hybrid-electric aircraft, presents significant growth potential and could be an area for strategic investment. Additionally, companies with a strong presence in high-growth regions like Asia-Pacific may offer better growth prospects. Investors should also consider the financial health and R&D capabilities of valve manufacturers, as the ability to innovate and adapt to changing industry standards is crucial in this market. However, potential investors should be aware of the cyclical nature of the aviation industry and the impact this can have on valve manufacturers' performance.

Aircraft Valve Market Conclusion - Summary and key takeaways

The Aircraft Valve Market is a vital segment of the aerospace industry, characterized by steady growth, technological innovation, and critical importance to aircraft safety and performance. With a projected CAGR of 5.03% from 2026 to 2033, the market is poised for continued expansion, driven by increasing global air travel, technological advancements, and the growing demand for new aircraft. The market is segmented by end user, valve type, product type, and aircraft type, with fuel system valves and fixed-wing aircraft representing significant portions of the market. Key players include established aerospace companies that compete on technology, quality, and customer relationships. While facing challenges such as high manufacturing costs and regulatory hurdles, the market presents significant opportunities in emerging markets, the aftermarket segment, and the development of smart valve technologies. Investors and industry participants should focus on innovation, quality, and strategic partnerships to succeed in this competitive and evolving market.

Research Methodology - How this research was conducted

The research for this Aircraft Valve Market report was conducted using a comprehensive methodology that combined primary and secondary research sources. Primary research involved interviews with industry experts, including executives from valve manufacturing companies, aircraft manufacturers, and aviation consultants. These interviews provided insights into market trends, competitive dynamics, and future outlook. Secondary research included analysis of industry reports, company financial statements, trade publications, and regulatory documents. Market size and growth projections were derived from a combination of historical data analysis, industry trend assessment, and expert forecasts. The segmentation analysis was based on company reports, industry classifications, and market observations. Regional analysis incorporated economic indicators, aviation industry data, and regional market reports. The competitive landscape was developed through company profiling, market share analysis, and assessment of recent developments and strategic initiatives. All data was cross-validated to ensure accuracy and reliability of the findings presented in this report.

Research Scope - Coverage and limitations

The research scope for this Aircraft Valve Market report encompasses the global market for aircraft valves, including analysis of market size, growth trends, segmentation, regional distribution, competitive landscape, and future projections. The report covers the period from 2026 to 2033, with a base year of 2026. The scope includes various types of aircraft valves used in commercial, military, and general aviation aircraft, segmented by end user (OEMs and MRO), valve type (pilot valves, poppet valves, flapper-nozzle valves), product type (fuel system valves, hydraulic system valves, air conditioning system valves, lubrication systems valves), and aircraft type (fixed-wing and rotary-wing). The report provides insights into key market drivers, restraints, opportunities, and challenges. However, it is important to note that the scope does not include detailed financial data for individual companies beyond what is publicly available, nor does it provide granular market share data for all segments and regions. The report also does not cover every minor player in the market, focusing instead on major industry participants and trends.

Key Companies and Recent Developments in the Aircraft Valve Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Aircraft Valve Market is dominated by several key companies, each with their own recent developments and strategic initiatives. Crissair Inc has been focusing on expanding its product line to include more lightweight and high-performance valves, particularly for military applications. Eaton has announced partnerships with several aircraft manufacturers to develop integrated valve systems that improve fuel efficiency. Honeywell International Inc recently launched a new series of smart valves with advanced diagnostic capabilities, aimed at reducing maintenance costs for airlines. ITT Inc has expanded its manufacturing capabilities in Asia to better serve the growing regional market. Moog Inc has introduced a new line of miniature valves designed for space-constrained aircraft systems. Parker Hannifin Corporation has acquired a smaller valve manufacturer to strengthen its position in the commercial aviation segment. Raytheon Technologies Corp, through its Collins Aerospace division, has unveiled a next-generation valve system that integrates with aircraft health monitoring systems. Safran Group has announced a strategic partnership with a leading aircraft manufacturer to develop fuel-efficient valve technologies. Triumph Group Inc has expanded its aftermarket services to include predictive maintenance solutions for aircraft valves. Woodward Inc has launched a new range of digital valves designed for electric and hybrid-electric aircraft, positioning itself for future market trends.