Microdisplay Market Overview - Definition, scope, and significance

Microdisplays are compact, high-resolution display technologies that are typically less than 25 millimeters in diagonal measurement. These miniaturized visual output devices serve as the core imaging components in a wide range of applications where space constraints and high image quality are paramount. The technology encompasses various display types including Liquid Crystal Display (LCD), Liquid Crystal on Silicon (LCoS), Digital Light Processing (DLP), and Organic Light Emitting Diode (OLED) variants. Microdisplays have become increasingly significant in modern technology ecosystems, enabling augmented reality (AR) headsets, head-mounted displays (HMDs), near-to-eye (NTE) devices, and projection systems. Their importance stems from their ability to deliver high-quality visual experiences in compact form factors, making them essential components in military equipment, medical devices, consumer electronics, and automotive applications. The market's growth is driven by the increasing demand for immersive technologies and the continuous miniaturization of electronic devices.

Microdisplay Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The microdisplay market is propelled by several key drivers, including the rapid adoption of augmented and virtual reality technologies across consumer and industrial applications. The growing demand for head-mounted displays in gaming, training simulations, and remote collaboration has created substantial market opportunities. Additionally, advancements in display resolution and power efficiency have expanded the potential applications for microdisplays. However, the market faces significant restraints, including high manufacturing costs and complex production processes that limit scalability. Technical challenges such as heat dissipation, color accuracy, and power consumption continue to pose obstacles for manufacturers. Despite these challenges, opportunities abound in emerging applications such as automotive heads-up displays, medical visualization systems, and military night vision equipment. The increasing integration of microdisplays in smart glasses and wearable devices presents another avenue for market expansion, particularly as consumer acceptance of these technologies grows.

Microdisplay Market Growth Trends - Current and emerging trends shaping the market

The microdisplay market is experiencing several transformative trends that are reshaping its landscape. One prominent trend is the shift toward higher resolution displays, with manufacturers increasingly focusing on 4K and even 8K microdisplays to meet the demands of immersive applications. Another significant trend is the growing adoption of OLED technology due to its superior contrast ratios, faster response times, and wider viewing angles compared to traditional LCD microdisplays. The integration of artificial intelligence and machine learning capabilities into microdisplay systems is also gaining traction, enabling features such as adaptive brightness and enhanced image processing. Additionally, the market is witnessing a trend toward the development of transparent and flexible microdisplays, opening up new possibilities for augmented reality applications. The increasing focus on energy efficiency and the development of low-power microdisplay solutions for extended battery life in portable devices represent another crucial trend shaping the market's future.

COVID-19 Impact on the Microdisplay Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a multifaceted impact on the microdisplay market, initially causing disruptions in manufacturing and supply chain operations due to lockdowns and restrictions. The temporary closure of production facilities and the shortage of critical components led to delays in product launches and reduced market growth in 2020. However, the pandemic also accelerated certain market trends, particularly in the adoption of virtual and augmented reality technologies for remote work, education, and entertainment. The increased demand for personal electronic devices and home entertainment systems provided some offset to the initial negative impacts. As the world recovers from the pandemic, the microdisplay market is experiencing a robust rebound, driven by pent-up demand and accelerated digital transformation initiatives. The recovery trajectory shows strong growth potential, particularly in applications related to remote collaboration, virtual training, and immersive entertainment experiences.

Microdisplay Market Competitive Landscape - Major competitors and market consolidation

The microdisplay market features a competitive landscape characterized by both established technology giants and specialized display manufacturers. Key players such as Sony Semiconductor Solutions Corporation, LG Electronics, and AUO Corporation leverage their extensive resources and technological expertise to maintain significant market positions. Meanwhile, specialized companies like KOPIN Corporation, Himax Technologies, and eMagin focus on niche applications and innovative technologies to differentiate themselves. The market has witnessed some consolidation through strategic partnerships and acquisitions, as companies seek to expand their technological capabilities and market reach. Competition is primarily based on factors such as display resolution, power efficiency, size, and cost. Companies are also competing on their ability to provide integrated solutions and customization options for specific applications. The entry of new players and the continuous innovation in display technologies are intensifying the competitive dynamics in the market.

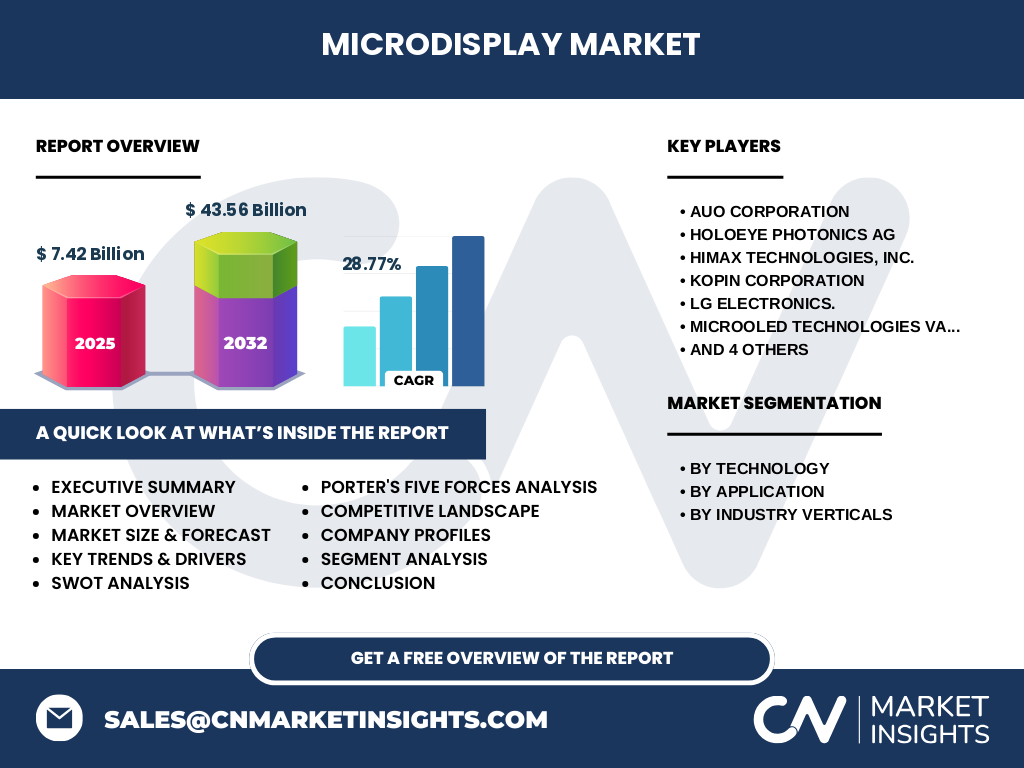

Executive Summary - High-level overview and key findings about Microdisplay Market

The microdisplay market is positioned for substantial growth, with projections indicating an expansion from USD 7.42 billion in 2025 to USD 43.56 billion by 2032, representing a remarkable CAGR of 28.77%. This growth is driven by the increasing adoption of augmented and virtual reality technologies, advancements in display resolution, and the expanding applications across various industry verticals. The market is characterized by technological diversity, with LCD, LCoS, DLP, and OLED technologies competing for market share. Key applications include near-to-eye devices, projection systems, and specialized industrial equipment. The market's future is shaped by trends toward higher resolution displays, energy efficiency, and integration with emerging technologies. While challenges exist in terms of manufacturing costs and technical limitations, the overall market outlook remains highly positive, with significant opportunities in automotive, healthcare, military, and consumer electronics sectors.

Microdisplay Market Forecast - Projections for 2025-2032 period

The microdisplay market is projected to experience exceptional growth over the forecast period from 2025 to 2032, with the market size expected to increase from USD 7.42 billion to USD 43.56 billion. This represents a compound annual growth rate (CAGR) of 28.77%, indicating robust expansion across all market segments. The forecast period is expected to be characterized by rapid technological advancements, particularly in resolution capabilities and power efficiency. The near-to-eye application segment is anticipated to show the highest growth rate, driven by the increasing adoption of AR and VR devices. The military and defense sector is also expected to contribute significantly to market growth, with continued investments in advanced visualization systems. The consumer electronics segment, particularly in smart glasses and wearable devices, is projected to experience substantial expansion as these technologies become more mainstream. The automotive sector's increasing integration of heads-up displays and augmented reality windshields is another key factor driving market growth during this period.

Microdisplay Market Size and Share by Segmentation - Breakdown by {segmentData}

The microdisplay market segmentation reveals distinct patterns in technology adoption and application preferences. By technology, the market is divided into LCD, LCoS, DLP, and OLED segments. LCD microdisplays currently hold a significant market share due to their established manufacturing processes and cost-effectiveness, but OLED technology is gaining traction rapidly due to its superior image quality and power efficiency. In terms of applications, the near-to-eye segment dominates the market, driven by the proliferation of AR and VR headsets, while projection applications maintain a steady share in commercial and industrial settings. The industry verticals segmentation shows that consumer electronics represents the largest share, followed by military and defense applications. Healthcare applications are experiencing the fastest growth rate, driven by the increasing adoption of medical visualization systems and surgical displays. The automotive sector is also showing significant growth potential, particularly in advanced driver assistance systems and heads-up displays.

Global Microdisplay Market Size and Share by Region - Geographic distribution

The global microdisplay market exhibits varied regional dynamics, with Asia-Pacific currently dominating the market share due to the presence of major display manufacturers and strong consumer electronics demand. Countries like Japan, South Korea, and Taiwan are key contributors to the region's market leadership, hosting several major microdisplay manufacturers and benefiting from established supply chains. North America represents the second-largest market, driven by high adoption rates of AR/VR technologies and significant investments in military and defense applications. Europe shows steady growth, particularly in automotive and industrial applications, with countries like Germany and France leading the adoption of advanced display technologies. The Middle East and Africa region, while currently smaller in market share, is showing promising growth potential, particularly in military and defense applications. Latin America is also emerging as a potential growth market, driven by increasing consumer electronics adoption and infrastructure development.

Regional Analysis of the Microdisplay Market - Detailed regional market performance

Regional analysis of the microdisplay market reveals distinct growth patterns and market dynamics across different geographic areas. In Asia-Pacific, the market is characterized by rapid technological advancement and high manufacturing capacity, with countries like China, Japan, and South Korea leading in both production and consumption. The region benefits from strong government support for technology development and a robust ecosystem of suppliers and manufacturers. North America shows strong performance in high-end applications, particularly in military, aerospace, and medical sectors, driven by significant R&D investments and early adoption of emerging technologies. Europe demonstrates steady growth, with a focus on automotive applications and industrial uses, supported by strict quality standards and environmental regulations. The Middle East region shows increasing demand in military and defense applications, while Latin America presents emerging opportunities in consumer electronics and automotive sectors. Each region's performance is influenced by factors such as technological infrastructure, economic conditions, and industry-specific demands.

Leading Company Profiles in the Microdisplay Market - Industry players and strategies

The microdisplay market features several prominent players, each with distinct strategic approaches and technological focus areas. Sony Semiconductor Solutions Corporation stands out for its advanced OLED microdisplay technology and strong presence in professional and industrial applications. LG Electronics leverages its expertise in display technology to develop innovative microdisplay solutions, particularly in the OLED segment. KOPIN Corporation specializes in high-resolution microdisplays for defense and aerospace applications, maintaining a strong position in the military sector. Himax Technologies focuses on LCOS technology and has established partnerships with major AR/VR headset manufacturers. eMagin is known for its OLED microdisplays and has a strong presence in military and medical applications. AUO Corporation brings extensive experience in LCD technology to the microdisplay market. These companies employ various strategies including technological innovation, strategic partnerships, and market expansion to maintain their competitive positions. Their approaches range from focusing on specific applications to developing comprehensive solutions across multiple industries.

Porter's Five Forces Analysis of the Microdisplay Market - Competitive forces assessment

Porter's Five Forces analysis of the microdisplay market reveals a complex competitive landscape shaped by several key factors. The threat of new entrants is moderate, as the market requires significant capital investment and technical expertise, creating barriers to entry. However, the growing demand and potential profitability continue to attract new players. The bargaining power of suppliers is relatively high due to the specialized nature of components and materials required for microdisplay manufacturing. Conversely, the bargaining power of buyers varies by segment, with large OEMs having significant influence while smaller customers have limited negotiating power. The threat of substitute products is moderate, as alternative display technologies and projection methods exist, but microdisplays offer unique advantages in specific applications. Competitive rivalry is intense, with numerous players competing on technological innovation, price, and application-specific solutions. The market also experiences pressure from rapid technological changes, requiring continuous innovation and investment in R&D to maintain competitive positions.

SWOT Analysis of the Microdisplay Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the microdisplay market reveals several key factors influencing its development. Strengths include the technology's versatility across multiple applications, continuous technological advancements, and growing market demand driven by AR/VR adoption. The market benefits from established manufacturing capabilities and strong intellectual property portfolios among key players. However, weaknesses exist in the form of high production costs, technical challenges in miniaturization, and dependency on specific raw materials. Opportunities abound in emerging applications such as automotive HUDs, medical visualization, and industrial AR systems. The increasing demand for wearable devices and smart glasses presents another significant opportunity for market expansion. Threats include intense competition, rapid technological changes that could render existing solutions obsolete, and potential supply chain disruptions. Additionally, the market faces challenges from economic uncertainties and regulatory changes that could impact production and adoption rates.

Microdisplay Market Value Chain Analysis - Industry structure and value flow

The microdisplay market value chain encompasses multiple stages, from raw material suppliers to end-users, with each stage adding distinct value to the final product. The chain begins with suppliers of specialized materials such as semiconductors, substrates, and optical components. These materials are then processed by microdisplay manufacturers who integrate various technologies to produce the final display units. Component manufacturers play a crucial role in developing supporting elements such as driver circuits and optical modules. System integrators combine microdisplays with other components to create complete solutions for specific applications. Original Equipment Manufacturers (OEMs) incorporate these solutions into their products, while distributors and retailers facilitate market access. The value chain is characterized by high levels of specialization and technological expertise, with significant value added at the manufacturing and integration stages. The chain also involves substantial R&D investments and quality control measures to ensure product performance and reliability.

Key Investment Insights in the Microdisplay Market - Strategic investment recommendations

Investment insights for the microdisplay market indicate several strategic opportunities for stakeholders. The market's strong projected growth, with a CAGR of 28.77% from 2025 to 2032, suggests significant potential for returns on investment. Key areas for investment include OLED technology development, given its superior performance characteristics and growing market share. Investments in manufacturing capacity expansion, particularly in Asia-Pacific, could capitalize on the region's dominant market position and growing demand. Strategic partnerships and collaborations between technology providers and application developers present opportunities for market expansion and innovation. Additionally, investments in emerging applications such as automotive HUDs and medical visualization systems could yield substantial returns as these sectors continue to grow. The market also presents opportunities for vertical integration, particularly for companies looking to control more of the value chain and improve profit margins. However, investors should be mindful of the technical challenges and competitive pressures in the market.

Microdisplay Market Conclusion - Summary and key takeaways

The microdisplay market presents a compelling growth story, with projections indicating substantial expansion from USD 7.42 billion in 2025 to USD 43.56 billion by 2032. This growth is driven by technological advancements, increasing adoption of AR/VR technologies, and expanding applications across various industry verticals. The market's future is shaped by trends toward higher resolution displays, energy efficiency, and integration with emerging technologies. While challenges exist in terms of manufacturing costs and technical limitations, the overall market outlook remains highly positive. Key opportunities lie in automotive applications, medical visualization, and military systems, while the consumer electronics sector continues to drive significant demand. The competitive landscape is characterized by both established players and innovative newcomers, creating a dynamic environment for technological advancement and market growth. Success in this market will require continuous innovation, strategic partnerships, and a focus on addressing specific application needs.

Research Methodology - How this research was conducted

The research methodology for this microdisplay market analysis employed a comprehensive approach combining both primary and secondary research methods. Primary research involved interviews with industry experts, manufacturers, and end-users to gather firsthand insights into market dynamics, technological developments, and application trends. Secondary research included extensive review of industry publications, company reports, technical journals, and market databases to validate and supplement primary findings. The analysis incorporated data triangulation techniques to ensure accuracy and reliability of market estimates and forecasts. Market size calculations were based on both top-down and bottom-up approaches, considering various factors such as technology adoption rates, application growth, and regional market dynamics. The research also included competitive analysis, value chain assessment, and Porter's Five Forces analysis to provide a comprehensive understanding of the market landscape. Regular updates and validation of data were conducted throughout the research process to maintain the accuracy and relevance of the findings.

Research Scope - Coverage and limitations

The research scope for this microdisplay market analysis encompasses the period from 2025 to 2032, focusing on key market segments, technologies, applications, and geographic regions. The study covers major microdisplay technologies including LCD, LCoS, DLP, and OLED, with detailed analysis of their respective market shares and growth trajectories. Applications analyzed include near-to-eye devices, projection systems, and various industry-specific uses across military, healthcare, consumer electronics, and automotive sectors. The geographic scope includes major global regions, with particular attention to Asia-Pacific, North America, and Europe. The research also examines key market players, competitive dynamics, and emerging trends shaping the industry. Limitations of the study include the rapidly evolving nature of the technology, which may lead to unforeseen developments affecting market projections. Additionally, the analysis may not capture all regional nuances and emerging applications that could impact market growth. The study focuses primarily on commercial aspects and may not fully address all technical specifications and limitations of microdisplay technologies.

Key Companies and Recent Developments in the Microdisplay Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The microdisplay market features several key companies making significant strides through recent developments and strategic initiatives. Sony Semiconductor Solutions Corporation has been focusing on advancing its OLED microdisplay technology, with recent announcements regarding higher resolution displays for professional applications. LG Electronics continues to expand its OLED microdisplay portfolio, particularly targeting the AR/VR market with improved brightness and power efficiency. KOPIN Corporation has strengthened its position in the defense sector through new product launches and partnerships, while Himax Technologies has announced collaborations with major AR headset manufacturers to integrate its LCOS technology. eMagin has been developing next-generation OLED microdisplays with enhanced resolution and lower power consumption. MICROOLED Technologies VAT has introduced new high-brightness displays for outdoor applications. These companies are actively pursuing strategic partnerships, technological innovations, and market expansions to maintain their competitive positions. Recent developments also include investments in manufacturing capacity, research and development initiatives, and efforts to address specific application requirements across various industry verticals.