eSIM Market Overview - Definition, scope, and significance

The eSIM (embedded SIM) market represents a transformative shift in how mobile connectivity is provisioned and managed across devices. Unlike traditional physical SIM cards, eSIMs are embedded directly into devices as reprogrammable chips, enabling users to switch carriers and activate plans without physically swapping cards. This technology has gained significant traction across multiple sectors including consumer mobile devices, Internet of Things (IoT) applications, automotive connectivity, and wearable technology. The eSIM market encompasses the hardware components (embedded chips), software platforms (remote provisioning systems), and services (connectivity management) that enable this technology. Its significance lies in enabling greater flexibility for consumers, reducing manufacturing costs for device makers, and creating new opportunities for connectivity providers to offer innovative service models across a growing ecosystem of connected devices.

eSIM Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The eSIM market is primarily driven by the accelerating adoption of IoT devices, growing demand for seamless connectivity across multiple devices, and increasing smartphone penetration in emerging markets. The technology's ability to reduce device size and manufacturing complexity makes it particularly attractive for manufacturers of wearables, smart home devices, and automotive applications. However, the market faces several restraints including the need for widespread carrier support, security concerns regarding remote provisioning, and the existing infrastructure investments in traditional SIM technology. Key challenges include standardization across different regions and carriers, consumer awareness and education, and the technical complexities of implementing eSIM in older device generations. Significant opportunities exist in emerging markets where smartphone adoption is growing rapidly, the expansion of 5G networks which are more compatible with eSIM technology, and the increasing demand for enterprise mobility solutions that can benefit from simplified device management and global connectivity.

eSIM Market Growth Trends - Current and emerging trends shaping the market

The eSIM market is experiencing several notable growth trends that are reshaping the connectivity landscape. One of the most significant trends is the increasing integration of eSIM technology in premium smartphones, with major manufacturers now offering eSIM as a standard feature alongside physical SIM slots. The IoT sector represents another major growth area, with eSIMs enabling more efficient fleet management, smart city infrastructure, and industrial automation applications. The travel and tourism industry has also embraced eSIM technology, offering travelers convenient options for local connectivity without physical SIM swaps. Additionally, the automotive sector is rapidly adopting eSIM for connected car services, enabling features like real-time navigation, emergency assistance, and over-the-air software updates. The convergence of eSIM with 5G technology is creating new possibilities for ultra-reliable, low-latency applications across various industries, while the growing emphasis on sustainability is driving interest in eSIM as a way to reduce plastic waste from traditional SIM cards.

COVID-19 Impact on the eSIM Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a mixed impact on the eSIM market, creating both challenges and opportunities. During the initial lockdowns, supply chain disruptions affected the production of eSIM-enabled devices, causing temporary slowdowns in market growth. However, the pandemic simultaneously accelerated digital transformation across industries, increasing demand for remote connectivity solutions and IoT applications where eSIM technology offers significant advantages. The shift to remote work and learning created new use cases for eSIM in laptops, tablets, and other connected devices. As businesses adapted to distributed operations, the need for simplified device management and global connectivity became more apparent, benefiting eSIM adoption. The recovery trajectory shows strong momentum as economies reopen, with pent-up demand for connected devices and renewed focus on digital infrastructure investment driving market expansion. The pandemic has effectively demonstrated the value of eSIM technology in enabling flexible, remote connectivity solutions, positioning the market for accelerated growth in the post-pandemic era.

eSIM Market Competitive Landscape - Major competitors and market consolidation

The eSIM market features a diverse competitive landscape with technology providers, telecommunications companies, and device manufacturers all playing crucial roles. Major semiconductor companies like Infineon Technologies, STMicroelectronics, and NXP Semiconductors dominate the hardware component of the market, providing the embedded chips that form the foundation of eSIM technology. On the software and services side, companies such as IDEMIA, Giesecke+Devrient, and Thales offer remote provisioning platforms and connectivity management solutions. Telecommunications giants including Deutsche Telekom, Telefónica, and Vodafone are critical players as they control network access and drive consumer adoption through their service offerings. The competitive landscape is characterized by strategic partnerships between these different types of players, as successful eSIM implementation requires collaboration across the entire value chain. While some consolidation has occurred through mergers and acquisitions, particularly in the software platform space, the market remains relatively fragmented with opportunities for new entrants, especially in specialized applications like IoT and automotive connectivity.

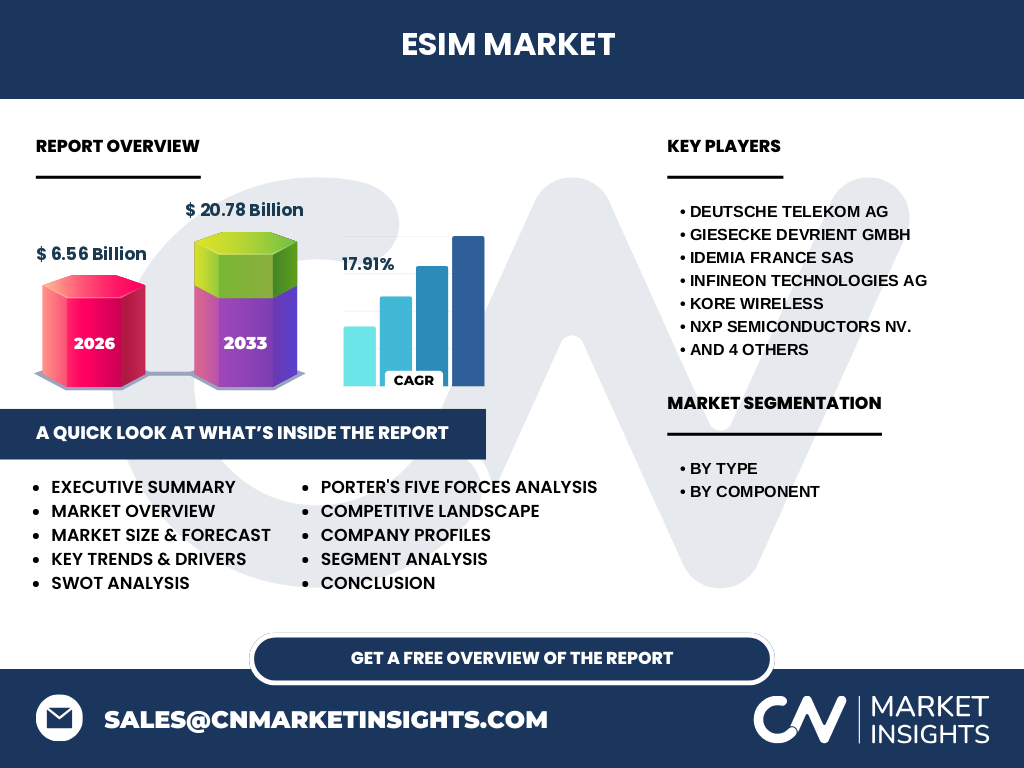

Executive Summary - High-level overview and key findings about eSIM Market

The eSIM market is positioned for substantial growth, with the market size projected to expand from $6.56 billion in 2026 to $20.78 billion by 2033, representing a robust CAGR of 17.91%. This growth is driven by increasing adoption across consumer devices, IoT applications, and enterprise solutions. The market segmentation reveals distinct opportunities across consumer eSIMs, IoT eSIMs, and travel eSIMs, with hardware, software, and services components creating a comprehensive ecosystem. Key findings indicate that while the technology has achieved significant penetration in premium smartphones and wearables, the greatest growth potential lies in emerging applications such as connected vehicles, smart city infrastructure, and industrial IoT. The competitive landscape shows strong participation from established technology companies and telecom operators, with strategic partnerships being essential for market success. Regional analysis suggests varying adoption rates globally, with developed markets leading in consumer applications while emerging markets show strong potential for IoT and enterprise solutions. Overall, the eSIM market represents a fundamental shift in how connectivity is delivered and managed, with the technology well-positioned to benefit from broader trends toward digitalization and device interconnectivity.

eSIM Market Forecast - Projections for 2025-2032 period

The eSIM market forecast for 2025-2032 indicates a period of robust expansion across all market segments and geographic regions. Starting from the 2026 baseline of $6.56 billion, the market is projected to experience compound annual growth of 17.91%, reaching $20.78 billion by 2033. This growth trajectory reflects increasing penetration in consumer devices, with eSIM becoming a standard feature in mid-range and premium smartphones, tablets, and wearables. The IoT segment is expected to show particularly strong growth, driven by smart city initiatives, industrial automation, and connected vehicle deployments. Software and services components are forecast to grow faster than hardware as the market matures and value shifts toward connectivity management and platform solutions. Geographic expansion will be significant, with emerging markets in Asia-Pacific, Latin America, and Africa showing accelerated adoption rates as infrastructure improves and device costs decrease. The forecast also accounts for technological advancements, including tighter integration with 5G networks and the emergence of new use cases that leverage eSIM's unique capabilities for remote provisioning and multi-carrier support.

eSIM Market Size and Share by Segmentation - Breakdown by {segmentData}

The eSIM market segmentation reveals distinct growth patterns across different categories. By type, consumer eSIMs currently represent the largest market segment, driven by adoption in smartphones and wearables, though IoT eSIMs are growing at the fastest rate as connected devices proliferate across industries. Travel eSIMs represent a niche but rapidly expanding segment, particularly popular among frequent travelers and digital nomads seeking flexible connectivity options. When segmented by component, hardware (the embedded chips themselves) forms the foundational market but shows slower growth as the technology matures, while software and services components demonstrate higher growth rates as value shifts toward platform solutions and connectivity management. The services segment, including remote SIM provisioning platforms and subscription management, is becoming increasingly important as carriers and enterprises seek to monetize eSIM capabilities. Regional segmentation shows North America and Europe leading in consumer applications, while Asia-Pacific shows the strongest growth potential across all segments due to large populations, increasing smartphone adoption, and rapid industrialization driving IoT demand.

Global eSIM Market Size and Share by Region - Geographic distribution

The global eSIM market exhibits distinct regional characteristics in terms of adoption rates, growth potential, and application focus. North America currently leads in market share, driven by high smartphone penetration, strong presence of technology companies, and early adoption of IoT applications. The region's mature telecommunications infrastructure and consumer willingness to embrace new technologies have accelerated eSIM deployment in both consumer and enterprise segments. Europe represents the second-largest market, with particularly strong adoption in countries like Germany, the UK, and Nordic nations where environmental concerns and digital innovation are prioritized. The Asia-Pacific region, while currently smaller in absolute terms, shows the highest growth rate and represents the largest opportunity for market expansion, with countries like China, India, and South Korea driving demand through massive smartphone markets and rapid industrialization. Latin America and Middle East & Africa regions are experiencing steady growth, primarily in mobile consumer applications, though infrastructure limitations in some areas create barriers to broader adoption. Regional differences in regulatory frameworks, carrier support, and consumer preferences create a diverse global landscape where localized strategies are essential for market success.

Regional Analysis of the eSIM Market - Detailed regional market performance

Regional analysis of the eSIM market reveals distinct adoption patterns and growth drivers across different geographic areas. In North America, the market is characterized by advanced infrastructure, high consumer technology adoption rates, and strong enterprise demand for IoT solutions. The presence of major technology companies and supportive regulatory frameworks has accelerated eSIM deployment, particularly in connected vehicle applications and smart city initiatives. Europe shows similar maturity levels but with added emphasis on sustainability and data privacy, driving adoption in environmentally conscious applications and enterprise solutions requiring secure connectivity. The Asia-Pacific region presents a more complex picture, with developed markets like Japan and South Korea showing technology leadership while emerging economies like India and Indonesia offer massive growth potential despite infrastructure challenges. China represents a unique case with its large domestic technology ecosystem and government support for digital infrastructure. Latin America demonstrates steady growth in mobile consumer applications, though economic volatility and infrastructure limitations affect the pace of adoption. Africa shows emerging potential, particularly in mobile-first economies where eSIM could enable financial inclusion and agricultural IoT applications, though the market remains constrained by limited network coverage and device availability in many areas.

Leading Company Profiles in the eSIM Market - Industry players and strategies

The eSIM market features several key players with distinct strategic approaches and areas of focus. Deutsche Telekom AG has established itself as a leader in both consumer and enterprise eSIM solutions, leveraging its extensive network infrastructure and partnerships with device manufacturers to drive adoption. Giesecke+Devrient GmbH specializes in secure connectivity solutions, with a strong focus on the financial services and government sectors where security is paramount. IDEMIA France SAS has built expertise in digital identity and security, positioning itself as a trusted provider for applications requiring robust authentication and privacy protection. Infineon Technologies AG and STMicroelectronics NV dominate the hardware segment, providing the embedded chips that form the foundation of eSIM technology, with ongoing investments in R&D to improve performance and reduce costs. KORE Wireless focuses on IoT applications, offering specialized eSIM solutions for fleet management, asset tracking, and industrial automation. NXP Semiconductors NV. combines hardware expertise with software platforms to deliver integrated solutions for automotive and smart city applications. Telefónica SA has pursued aggressive eSIM deployment strategies in its European and Latin American markets, while Vodafone Group Plc has focused on creating seamless cross-border connectivity solutions. Thales SA leverages its cybersecurity heritage to offer highly secure eSIM solutions for critical infrastructure and defense applications.

Porter's Five Forces Analysis of the eSIM Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the eSIM market. The threat of new entrants remains moderate, as while the technology itself is becoming more accessible, successful market entry requires significant investments in infrastructure, partnerships with carriers, and compliance with regional regulations. The bargaining power of suppliers, primarily semiconductor manufacturers, is relatively high due to the specialized nature of eSIM chips and limited alternatives for certain components. Conversely, the bargaining power of buyers (device manufacturers and enterprise customers) is increasing as eSIM becomes more commoditized and alternative connectivity solutions emerge. The threat of substitute products is moderate, with traditional SIM cards still widely used and emerging technologies like soft SIMs presenting potential alternatives, though eSIM's advantages in security and remote management provide differentiation. Competitive rivalry within the eSIM market is intense, characterized by price competition, rapid technological innovation, and strategic partnerships between hardware providers, software platform companies, and telecommunications operators. The analysis suggests that while the market offers significant opportunities, success requires navigating complex relationships across the value chain and continuously innovating to maintain competitive advantage.

SWOT Analysis of the eSIM Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the eSIM market reveals several key factors influencing its development. Strengths include the technology's ability to enable remote provisioning and management, reduce device size and manufacturing complexity, and support multiple carrier profiles on a single device. The growing ecosystem of eSIM-compatible devices and increasing carrier support represent significant advantages. However, weaknesses exist in the form of limited consumer awareness, dependence on carrier adoption, and the need for specialized infrastructure for remote provisioning. Security concerns regarding remote management and the potential for hacking represent ongoing challenges. Opportunities abound in emerging applications such as connected vehicles, smart city infrastructure, and industrial IoT, where eSIM's advantages are particularly valuable. The expansion of 5G networks creates new possibilities for ultra-reliable, low-latency applications that benefit from eSIM's capabilities. Threats to the market include potential regulatory changes affecting cross-border connectivity, the emergence of alternative technologies that could displace eSIM, and economic downturns that could reduce consumer spending on new devices. Additionally, the complexity of implementing eSIM across diverse device types and regional requirements presents ongoing challenges for market expansion.

eSIM Market Value Chain Analysis - Industry structure and value flow

The eSIM market value chain encompasses multiple interconnected stages, each contributing to the delivery of eSIM solutions to end users. At the foundation, semiconductor manufacturers like Infineon and STMicroelectronics produce the embedded chips that physically implement eSIM functionality. These chips are integrated into devices by manufacturers such as Apple, Samsung, and various IoT device makers, who must design products to accommodate eSIM technology. Software platform providers, including companies like IDEMIA and Giesecke+Devrient, develop the remote provisioning and management systems that enable eSIM functionality. Mobile network operators serve as critical intermediaries, providing network access and often directly interfacing with consumers through service plans and activation processes. Distributors and retailers facilitate the market reach of eSIM-enabled devices to consumers and enterprises. At the end of the chain, consumers and businesses utilize eSIM technology for mobile connectivity, IoT applications, and enterprise mobility solutions. Value is created through technological innovation at each stage, with the greatest value increasingly concentrated in software platforms and services that enable the unique capabilities of eSIM technology. The value chain is characterized by complex interdependencies, with successful eSIM deployment requiring coordination across all participants.

Key Investment Insights in the eSIM Market - Strategic investment recommendations

eSIM Market Conclusion - Summary and key takeaways

The eSIM market represents a significant technological evolution in mobile connectivity, offering compelling advantages in flexibility, security, and device design. With the market projected to grow from $6.56 billion in 2026 to $20.78 billion by 2033 at a CAGR of 17.91%, the technology is well-positioned for substantial expansion across consumer, IoT, and enterprise applications. Key takeaways include the technology's ability to enable new use cases in connected vehicles, smart cities, and industrial automation, while also providing consumers with greater flexibility in managing mobile connectivity. The competitive landscape features a diverse ecosystem of hardware providers, software platform companies, and telecommunications operators, with success increasingly dependent on strategic partnerships and integrated solutions. Regional variations in adoption rates highlight the importance of localized strategies, with developed markets leading in consumer applications while emerging markets offer the greatest growth potential for IoT and enterprise solutions. Despite challenges including security concerns and the need for widespread carrier support, the eSIM market's trajectory points toward becoming a standard feature in connected devices, driven by the broader trends of digitalization, 5G deployment, and the growing Internet of Things ecosystem.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology combining primary and secondary research approaches. Secondary research involved extensive analysis of industry reports, company financial statements, regulatory filings, and technology publications to establish baseline market data and trends. Primary research included interviews with industry experts, technology providers, and market analysts to validate findings and gain insights into emerging developments not yet reflected in public data. The research methodology employed both top-down and bottom-up approaches to market sizing, starting with macroeconomic indicators and technology adoption rates to establish overall market potential, then drilling down to specific segments and applications. Data triangulation was used to cross-verify information from multiple sources, ensuring accuracy and reliability. The research also incorporated scenario analysis to account for potential market variations based on different adoption rates, technological developments, and economic conditions. Geographic analysis utilized regional economic data, infrastructure development indicators, and technology adoption statistics to project market performance across different areas. Throughout the research process, emphasis was placed on identifying verifiable data points and clearly distinguishing between established facts and projections based on market trends and expert opinions.

Research Scope - Coverage and limitations

The research scope for this eSIM market analysis encompasses the period from 2026 to 2033, with particular focus on the consumer, IoT, and travel eSIM segments across hardware, software, and services components. The geographic coverage includes major global regions with detailed analysis of North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, though the depth of coverage varies based on data availability and market significance. The research focuses on commercial eSIM applications and excludes certain niche or experimental implementations that lack market traction. Limitations of the research include the rapidly evolving nature of the technology, which can quickly render specific data points outdated, and the challenge of obtaining precise market share data due to the proprietary nature of many eSIM deployments and the involvement of multiple stakeholders in single implementations. Additionally, the research does not extensively cover potential disruptive technologies that could emerge during the forecast period, as these are inherently difficult to predict. The scope also acknowledges that certain regional markets may have incomplete data due to limited public information or market opacity, particularly in emerging economies where eSIM adoption is still developing.

Key Companies and Recent Developments in the eSIM Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The eSIM market has seen significant activity from key players, with several notable developments shaping the competitive landscape. Deutsche Telekom AG recently announced expanded eSIM support for IoT devices, launching new enterprise solutions for fleet management and smart logistics applications. Giesecke+Devrient GmbH introduced an advanced security platform for eSIM provisioning, targeting financial services and government sectors with enhanced authentication features. IDEMIA France SAS unveiled a next-generation eSIM management platform with improved privacy controls and simplified user interfaces for consumer applications. Infineon Technologies AG and STMicroelectronics NV. both launched new generations of embedded chips with enhanced security features and reduced power consumption, critical for battery-powered IoT devices. KORE Wireless announced partnerships with major automotive manufacturers to provide integrated eSIM solutions for connected vehicles, including over-the-air update capabilities and enhanced telematics services. NXP Semiconductors NV. expanded its automotive eSIM portfolio with solutions optimized for 5G connectivity and autonomous driving applications. Telefónica SA launched a global eSIM service for frequent travelers, offering seamless connectivity across its European and Latin American markets with simplified activation processes. Vodafone Group Plc announced collaborations with device manufacturers to pre-install eSIM profiles on smartphones, reducing barriers to consumer adoption. Thales SA introduced a secure eSIM solution for critical infrastructure, addressing heightened cybersecurity concerns in utilities and transportation sectors. These developments reflect the market's dynamic nature and the ongoing innovation across the eSIM value chain.