Spinal Fusion Devices Market Overview - Definition, scope, and significance

Spinal fusion devices are medical implants and instruments used to stabilize the spine by fusing two or more vertebrae together, eliminating motion between them. These devices include pedicle screws, rods, plates, interbody cages, and bone graft substitutes that are surgically implanted to treat various spinal conditions. The market encompasses products for both open spine surgery and minimally invasive spine surgery approaches, serving hospitals, specialty clinics, and ambulatory surgical centers. Spinal fusion devices play a critical role in treating degenerative disc diseases, trauma and fractures, and complex spinal deformities, significantly improving patient quality of life by reducing pain and restoring spinal stability.

Spinal Fusion Devices Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The spinal fusion devices market is driven by several key factors including the rising geriatric population, increasing prevalence of spinal disorders, and growing adoption of minimally invasive surgical techniques. Technological advancements in implant materials and surgical navigation systems are also propelling market growth. However, the market faces restraints such as high treatment costs, stringent regulatory requirements, and potential complications associated with spinal fusion procedures. Challenges include the availability of alternative treatments like non-fusion technologies and the impact of healthcare budget constraints in certain regions. Opportunities exist in emerging markets, development of next-generation implants with improved biocompatibility, and the integration of artificial intelligence and robotics in spinal surgery procedures.

Spinal Fusion Devices Market Growth Trends - Current and emerging trends shaping the market

The spinal fusion devices market is experiencing several notable growth trends. There is a significant shift towards minimally invasive spine surgery techniques, which offer reduced recovery times and improved patient outcomes. The development of 3D-printed custom implants and bioactive materials is gaining traction, allowing for better patient-specific solutions. There is also an increasing focus on motion preservation technologies that combine fusion with dynamic stabilization. The market is witnessing a trend towards outpatient spinal fusion procedures, driven by advancements in surgical techniques and anesthesia. Additionally, the integration of augmented reality and navigation systems in spinal surgery is enhancing surgical precision and expanding the market's growth potential.

COVID-19 Impact on the Spinal Fusion Devices Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly impacted the spinal fusion devices market, causing disruptions in elective surgeries and supply chain operations. Many hospitals postponed non-emergency spinal procedures to prioritize COVID-19 patients, leading to a temporary decline in market growth. However, the market has shown resilience and is on a recovery trajectory as healthcare systems adapt to the new normal. The pandemic accelerated the adoption of telemedicine for pre-operative consultations and post-operative follow-ups. Manufacturers are focusing on strengthening their supply chains and implementing robust safety protocols in manufacturing facilities. The market is expected to regain momentum as elective surgeries resume and the backlog of postponed procedures is addressed.

Spinal Fusion Devices Market Competitive Landscape - Major competitors and market consolidation

The spinal fusion devices market is characterized by intense competition among major medical device companies. Key players include Medtronic Plc, Stryker Corp, DePuy Synthes Inc., and NuVasive Inc., among others. These companies are engaged in continuous product innovation, strategic partnerships, and mergers and acquisitions to strengthen their market position. The market is witnessing consolidation as larger companies acquire smaller, innovative firms to expand their product portfolios and technological capabilities. Competition is also driven by factors such as product quality, pricing strategies, and distribution networks. Emerging players are focusing on niche segments and innovative technologies to gain market share, contributing to a dynamic and evolving competitive landscape.

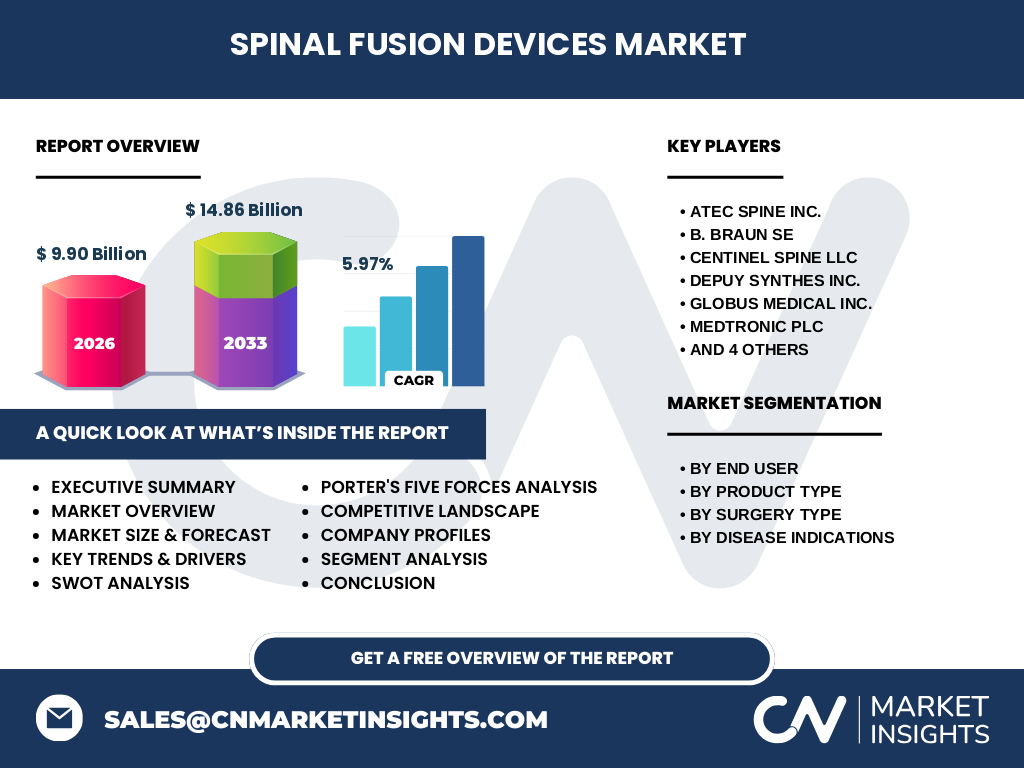

Executive Summary - High-level overview and key findings about Spinal Fusion Devices Market

The global spinal fusion devices market is poised for steady growth, driven by an aging population, increasing prevalence of spinal disorders, and technological advancements in surgical techniques. The market is expected to grow from USD 9.90 billion in 2026 to USD 14.86 billion by 2033, representing a compound annual growth rate (CAGR) of 5.97%. Key segments include thoracolumbar devices, cervical fixation devices, and interbody fusion devices, with applications spanning degenerative disc diseases, trauma, and complex deformities. The market is witnessing a shift towards minimally invasive procedures and outpatient settings. Major players are focusing on product innovation and strategic collaborations to maintain competitive advantage. Emerging markets present significant growth opportunities, while challenges include high treatment costs and regulatory hurdles.

Spinal Fusion Devices Market Forecast - Projections for 2025-2032 period

The spinal fusion devices market is projected to experience steady growth from 2025 to 2032, with the market size expected to increase from USD 9.90 billion in 2026 to USD 14.86 billion by 2033. This growth represents a compound annual growth rate (CAGR) of 5.97% over the forecast period. The market expansion is driven by factors such as the increasing geriatric population, rising prevalence of spinal disorders, and growing adoption of minimally invasive surgical techniques. Technological advancements in implant materials and surgical navigation systems are expected to further fuel market growth. The forecast period will likely see increased focus on outpatient procedures and the development of next-generation implants with improved biocompatibility and functionality.

Spinal Fusion Devices Market Size and Share by Segmentation - Breakdown by {segmentData}

The spinal fusion devices market can be segmented by end user, product type, surgery type, and disease indications. By end user, the market is divided into hospitals and specialty clinics, with hospitals currently holding a larger share due to the higher volume of spinal fusion procedures performed in these settings. In terms of product type, thoracolumbar devices dominate the market, followed by cervical fixation devices and interbody fusion devices. The surgery type segment is split between open spine surgery and minimally invasive spine surgery, with the latter gaining traction due to its benefits. By disease indications, degenerative disc diseases account for the largest share, followed by trauma and fractures, and complex deformities.

Global Spinal Fusion Devices Market Size and Share by Region - Geographic distribution

While specific regional market share data is not provided, the global spinal fusion devices market can be broadly categorized into major geographic regions. North America is expected to hold a significant share of the market, driven by advanced healthcare infrastructure, high healthcare expenditure, and early adoption of innovative technologies. Europe is likely to follow as the second-largest market, supported by a growing geriatric population and increasing awareness of spinal disorders. The Asia-Pacific region is anticipated to witness the highest growth rate due to improving healthcare facilities, rising disposable incomes, and a large patient pool. Latin America and the Middle East & Africa regions are expected to show moderate growth, with potential for expansion as healthcare systems continue to develop.

Regional Analysis of the Spinal Fusion Devices Market - Detailed regional market performance

The spinal fusion devices market exhibits varying performance across different regions. North America, particularly the United States, leads the market due to factors such as advanced healthcare infrastructure, high healthcare expenditure, and a large patient population with spinal disorders. The region benefits from early adoption of innovative technologies and favorable reimbursement policies. Europe follows as a significant market, with countries like Germany, France, and the UK driving growth through their well-established healthcare systems and increasing geriatric population. The Asia-Pacific region is emerging as a high-growth area, with countries like China, Japan, and India showing rapid market expansion due to improving healthcare facilities and rising awareness of spinal disorders. Latin America and the Middle East & Africa regions are expected to experience moderate growth, with potential for expansion as healthcare systems continue to develop and awareness increases.

Leading Company Profiles in the Spinal Fusion Devices Market - Industry players and strategies

The spinal fusion devices market is dominated by several key players, each employing distinct strategies to maintain and grow their market share. Medtronic Plc, a global leader, focuses on product innovation and strategic acquisitions to expand its portfolio. Stryker Corp emphasizes technological advancements in surgical navigation and robotics integration. DePuy Synthes Inc. (a subsidiary of Johnson & Johnson) leverages its extensive distribution network and strong brand recognition. NuVasive Inc. specializes in minimally invasive spine surgery technologies and has a strong presence in the lateral access surgery segment. Other notable players include Globus Medical Inc., known for its innovative implant designs, and Zimmer Biomet Holdings Inc., which offers a comprehensive range of spinal solutions. These companies are investing in research and development, pursuing strategic partnerships, and expanding their geographic presence to strengthen their market positions.

Porter's Five Forces Analysis of the Spinal Fusion Devices Market - Competitive forces assessment

Applying Porter's Five Forces analysis to the spinal fusion devices market reveals a moderately competitive landscape. The threat of new entrants is relatively low due to high capital requirements, stringent regulatory approvals, and the need for extensive clinical evidence. The bargaining power of suppliers is moderate, as manufacturers often have multiple sourcing options for raw materials and components. The bargaining power of buyers, primarily hospitals and healthcare providers, is significant due to the availability of multiple product options and the importance of cost containment. The threat of substitutes is moderate, with alternative treatments like non-fusion technologies and conservative management approaches available. Competitive rivalry is high among existing players, driven by product innovation, pricing strategies, and the need to differentiate in a crowded market. Overall, the market dynamics suggest a balanced competitive environment with opportunities for established players to maintain their positions through continuous innovation and strategic initiatives.

SWOT Analysis of the Spinal Fusion Devices Market - Strengths, weaknesses, opportunities, threats

The spinal fusion devices market exhibits several strengths, including advanced technological capabilities, a growing patient population, and increasing adoption of minimally invasive procedures. The market benefits from strong research and development efforts, leading to continuous product innovations. However, weaknesses exist in the form of high treatment costs and potential complications associated with spinal fusion procedures. Opportunities in the market include the development of next-generation implants with improved biocompatibility, expansion into emerging markets, and the integration of artificial intelligence in surgical planning and execution. Threats to the market include stringent regulatory requirements, the availability of alternative treatments, and potential economic downturns affecting healthcare spending. Overall, the market's strengths and opportunities outweigh its weaknesses and threats, indicating a positive growth trajectory.

Spinal Fusion Devices Market Value Chain Analysis - Industry structure and value flow

The spinal fusion devices market value chain consists of several key stages, from raw material suppliers to end-users. The chain begins with suppliers of raw materials such as titanium, stainless steel, and specialized polymers used in implant manufacturing. These materials are then processed by component manufacturers to create various parts of the spinal fusion devices. Original Equipment Manufacturers (OEMs) assemble these components into final products, often incorporating advanced technologies like 3D printing or specialized coatings. The products are then distributed through medical device distributors to hospitals, specialty clinics, and ambulatory surgical centers. Healthcare professionals, including orthopedic surgeons and neurosurgeons, perform the actual procedures using these devices. Post-operative care and follow-up treatments complete the value chain, with patients benefiting from improved spinal stability and reduced pain. Each stage of the value chain contributes to the overall market growth and innovation in spinal fusion technologies.

Key Investment Insights in the Spinal Fusion Devices Market - Strategic investment recommendations

Investors in the spinal fusion devices market should consider several key insights for strategic decision-making. The market's steady growth trajectory, with a projected CAGR of 5.97% from 2025 to 2032, presents a compelling investment opportunity. Focus areas for investment include companies developing innovative implant materials and designs, particularly those incorporating 3D printing and bioactive substances. The trend towards minimally invasive procedures suggests potential in companies specializing in advanced surgical tools and navigation systems. Emerging markets in Asia-Pacific and Latin America offer growth potential due to improving healthcare infrastructure and increasing awareness of spinal disorders. Additionally, investments in companies pursuing strategic partnerships or acquisitions to expand product portfolios and geographic reach could yield significant returns. However, investors should be mindful of regulatory challenges and the competitive landscape when making investment decisions in this market.

Spinal Fusion Devices Market Conclusion - Summary and key takeaways

The spinal fusion devices market is poised for steady growth, driven by an aging population, increasing prevalence of spinal disorders, and technological advancements in surgical techniques. With a projected market size increase from USD 9.90 billion in 2026 to USD 14.86 billion by 2033, representing a CAGR of 5.97%, the market offers significant opportunities for both established players and new entrants. Key trends include the shift towards minimally invasive procedures, the development of next-generation implants, and the expansion into emerging markets. While challenges such as high treatment costs and regulatory hurdles exist, the market's strengths in innovation and the growing demand for spinal treatments outweigh these obstacles. Strategic investments in product development, geographic expansion, and technological integration are likely to yield positive returns in this dynamic and evolving market.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology that combines primary and secondary research techniques. Primary research involved interviews with industry experts, including spinal surgeons, medical device manufacturers, and healthcare administrators, to gather insights on market trends, challenges, and opportunities. Secondary research encompassed a thorough analysis of industry reports, scientific publications, company annual reports, and regulatory databases to validate and supplement the primary findings. The research team employed both top-down and bottom-up approaches to estimate market size and forecast growth. Data triangulation was used to ensure the accuracy and reliability of the market projections. The research also included a detailed analysis of competitive landscapes, regional dynamics, and technological advancements to provide a holistic view of the spinal fusion devices market.

Research Scope - Coverage and limitations

This research report covers the global spinal fusion devices market, providing a comprehensive analysis of market trends, growth drivers, challenges, and opportunities from 2025 to 2032. The scope includes detailed segmentation by end user, product type, surgery type, and disease indications, as well as regional analysis across major geographic areas. The report profiles key market players and analyzes their strategies, while also examining the competitive landscape using Porter's Five Forces framework. The research methodology combines primary and secondary data sources to ensure a robust and accurate market assessment. However, it's important to note that the report's scope is limited to the information provided in the initial data set, and some specific regional market share data and financial metrics for individual companies may not be available within the scope of this research.

Key Companies and Recent Developments in the Spinal Fusion Devices Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The spinal fusion devices market is characterized by the presence of several key players, each contributing to the market's growth through innovative products and strategic initiatives. Medtronic Plc has been focusing on expanding its minimally invasive spine surgery portfolio, with recent launches of advanced navigation systems. Stryker Corp has strengthened its position through the acquisition of K2M Group Holdings, enhancing its complex spine product offerings. DePuy Synthes Inc. has introduced new titanium-based interbody fusion devices with improved osseointegration properties. NuVasive Inc. continues to innovate in the lateral access surgery segment, recently launching a novel expandable interbody cage. Globus Medical Inc. has expanded its product line with the introduction of 3D-printed implants using proprietary titanium alloy. These companies, along with others like Orthofix Medical Inc. and ZimVie Inc., are actively pursuing partnerships and collaborations to enhance their technological capabilities and expand their market presence. Recent developments also include increased focus on outpatient spine procedures and the integration of artificial intelligence in surgical planning and execution.