Electric Bus Market Overview - Definition, scope, and significance

The electric bus market represents the global industry focused on the development, manufacturing, and deployment of buses powered by electric propulsion systems. This market encompasses various types of electric buses including battery electric buses, hybrid electric buses, and plug-in hybrid electric buses, serving both public and private transportation sectors. The significance of this market lies in its potential to transform urban mobility by reducing greenhouse gas emissions, decreasing noise pollution, and lowering operational costs for transit agencies. As cities worldwide implement stricter emission regulations and pursue sustainable transportation goals, the electric bus market has emerged as a critical component of the broader electric vehicle revolution, offering a cleaner alternative to traditional diesel-powered public transportation systems.

Electric Bus Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The electric bus market is primarily driven by increasing environmental concerns, government initiatives to reduce carbon emissions, and the declining costs of battery technology. Stringent emission regulations, particularly in Europe and Asia, are compelling transit authorities to adopt electric alternatives. Additionally, the total cost of ownership for electric buses is becoming increasingly competitive with diesel buses, especially when considering fuel savings and lower maintenance requirements. However, the market faces several restraints including high upfront capital costs, limited charging infrastructure, and range anxiety concerns. Challenges include the need for extensive charging networks, grid capacity constraints, and the technical limitations of current battery technology. Despite these obstacles, significant opportunities exist in emerging markets, technological advancements in battery energy density, and the development of innovative charging solutions such as wireless charging and opportunity charging systems.

Electric Bus Market Growth Trends - Current and emerging trends shaping the market

The electric bus market is experiencing several transformative growth trends that are reshaping the industry landscape. One of the most prominent trends is the rapid advancement in battery technology, with lithium iron phosphate (LFP) batteries gaining popularity due to their improved safety, longer lifespan, and lower costs compared to traditional lithium-ion batteries. Another significant trend is the increasing adoption of autonomous driving technologies, which are being integrated into electric bus designs to enhance safety and operational efficiency. The market is also witnessing a shift towards modular and scalable electric bus platforms that allow manufacturers to produce various bus sizes using common components. Additionally, there is a growing trend of partnerships between bus manufacturers and charging infrastructure providers to create integrated solutions that address range and charging concerns. The emergence of hydrogen fuel cell electric buses as a complementary technology to battery electric buses is also gaining traction, particularly for longer routes and in regions with limited charging infrastructure.

COVID-19 Impact on the Electric Bus Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the electric bus market, disrupting supply chains, delaying projects, and reducing public transportation ridership. During the height of the pandemic, many transit agencies faced financial constraints, leading to postponed or canceled electric bus procurement plans. Manufacturing facilities experienced temporary shutdowns, and the availability of critical components such as batteries and semiconductors was severely affected. However, the pandemic also accelerated certain trends within the market, including the increased focus on sustainable transportation as part of economic recovery plans. Many governments included electric bus initiatives in their stimulus packages, recognizing the dual benefits of supporting the automotive industry while advancing environmental goals. As the market recovers, there is a renewed emphasis on contactless payment systems, improved air filtration, and the integration of digital technologies to enhance passenger safety and confidence in public transportation.

Electric Bus Market Competitive Landscape - Major competitors and market consolidation

The electric bus market is characterized by a mix of established automotive manufacturers and specialized electric vehicle companies, creating a dynamic competitive landscape. Major players such as BYD Company Ltd, AB Volvo, and Daimler AG are leveraging their extensive experience in the automotive industry to capture significant market share. Meanwhile, companies like Proterra Inc and Ebusco are focusing exclusively on electric bus technology, offering innovative solutions and challenging traditional manufacturers. The market is witnessing increasing consolidation through strategic partnerships, joint ventures, and acquisitions. For instance, collaborations between bus manufacturers and technology companies are becoming more common to develop advanced electric drivetrains and charging solutions. The competitive landscape is also being shaped by regional dynamics, with Chinese manufacturers dominating the domestic market and expanding their presence in international markets, while European and North American companies are focusing on technological differentiation and sustainability credentials to maintain their competitive edge.

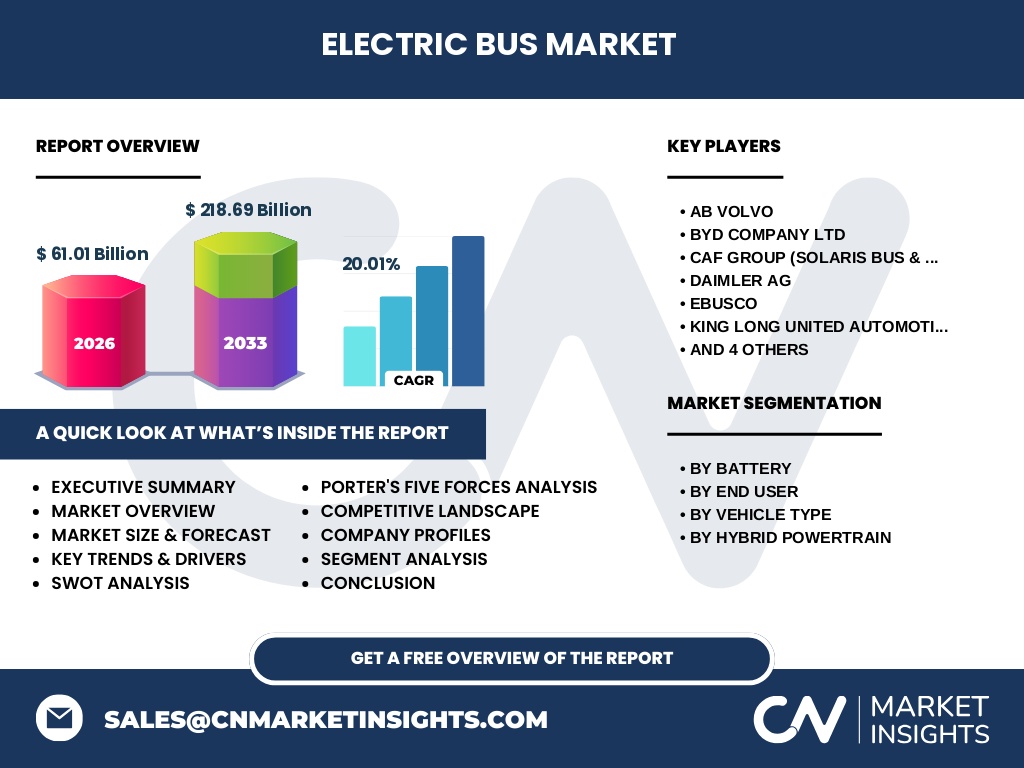

Executive Summary - High-level overview and key findings about Electric Bus Market

The electric bus market is at a pivotal juncture, with the industry poised for exponential growth driven by environmental regulations, technological advancements, and shifting consumer preferences. The market is expected to grow from a size of 61.01 Billion in 2026 to 218.69 Billion by 2033, representing a robust CAGR of 20.01%. This growth is underpinned by the increasing adoption of electric buses across various segments, including public transportation, private fleet operations, and specialized applications such as airport shuttles and university campuses. The market is characterized by a diverse range of battery technologies, with lithium iron phosphate and lithium nickel manganese cobalt oxide batteries leading the way. The end-user segment is dominated by public transportation authorities, but private sector adoption is accelerating. Vehicle types range from battery electric buses to hybrid and plug-in hybrid variants, with hybrid powertrains offering flexibility in different operational scenarios. As the market continues to evolve, key players are focusing on innovation, strategic partnerships, and geographic expansion to capitalize on emerging opportunities and address the challenges of electrification.

Electric Bus Market Forecast - Projections for 2025-2032 period

The electric bus market is projected to experience substantial growth during the 2025-2032 period, with the market size expected to increase from 61.01 Billion to 218.69 Billion. This represents a compound annual growth rate (CAGR) of 20.01%, indicating a rapidly expanding market with significant investment opportunities. The forecast period will likely see continued technological advancements in battery technology, leading to improved energy density, faster charging times, and reduced costs. The adoption of electric buses is expected to accelerate across all segments, with public transportation authorities leading the charge, followed by private fleet operators and specialized applications. Geographic expansion will be a key driver of growth, with emerging markets in Asia, Latin America, and Africa presenting substantial opportunities for market penetration. The forecast also suggests that government incentives, emission regulations, and the development of charging infrastructure will play crucial roles in shaping market dynamics. As the industry matures, we can expect to see increased competition, product innovation, and strategic collaborations among key players to capture market share and drive technological advancements.

Electric Bus Market Size and Share by Segmentation - Breakdown by {segmentData}

The electric bus market is segmented by battery type, end user, vehicle type, and hybrid powertrain, each contributing to the overall market dynamics. In terms of battery technology, lithium iron phosphate (LFP) batteries are gaining significant traction due to their cost-effectiveness and safety features, while lithium nickel manganese cobalt oxide (NMC) batteries continue to dominate in applications requiring higher energy density. The end-user segment is primarily divided between public and private sectors, with public transportation authorities accounting for the largest share due to government initiatives and emission regulations. Vehicle types include battery electric buses, which are the most prevalent, followed by hybrid electric buses and plug-in hybrid electric buses that offer flexibility in different operational scenarios. The hybrid powertrain segment is categorized into series parallel hybrid, parallel hybrid, and series hybrid systems, each catering to specific performance and efficiency requirements. As the market evolves, we can expect to see shifts in segment shares based on technological advancements, regulatory changes, and changing consumer preferences.

Global Electric Bus Market Size and Share by Region - Geographic distribution

The global electric bus market exhibits significant regional variations in terms of adoption rates, market size, and growth potential. Asia-Pacific, particularly China, dominates the global market, accounting for a substantial share of electric bus deployments due to aggressive government policies, large-scale manufacturing capabilities, and rapid urbanization. Europe represents the second-largest market, driven by stringent emission regulations, well-established public transportation systems, and strong environmental awareness. North America, while currently a smaller market, is experiencing rapid growth due to increasing investments in sustainable transportation and the presence of major electric bus manufacturers. Latin America and the Middle East & Africa regions are emerging markets with significant growth potential, albeit at a slower pace due to economic constraints and infrastructure challenges. The regional distribution of the market is influenced by factors such as government incentives, charging infrastructure development, economic conditions, and the maturity of public transportation systems in each region.

Regional Analysis of the Electric Bus Market - Detailed regional market performance

The regional performance of the electric bus market varies significantly across different geographies, reflecting diverse economic conditions, regulatory environments, and infrastructure development levels. In Asia-Pacific, particularly in China, the market has experienced explosive growth, with the country accounting for a majority of global electric bus deployments. This success is attributed to strong government support, including subsidies and mandates for public transportation electrification. Europe has emerged as a leader in electric bus technology and adoption, with countries like Germany, the Netherlands, and the UK implementing ambitious electrification plans for their public transportation fleets. The region benefits from well-developed charging infrastructure and a strong focus on reducing urban emissions. North America, while lagging behind Asia and Europe in terms of absolute numbers, is witnessing rapid growth, particularly in the United States, where several large cities have committed to transitioning their bus fleets to electric power. Latin America and Africa, although currently smaller markets, are showing promising signs of growth, with countries like Chile and Colombia leading the way in electric bus adoption through pilot projects and public-private partnerships.

Leading Company Profiles in the Electric Bus Market - Industry players and strategies

The electric bus market is characterized by a diverse range of companies, each employing unique strategies to capture market share and drive innovation. BYD Company Ltd has established itself as a global leader, particularly in the Chinese market, leveraging its extensive manufacturing capabilities and vertically integrated supply chain. AB Volvo has focused on leveraging its established brand and global presence to offer a comprehensive range of electric buses, emphasizing reliability and after-sales service. Daimler AG, through its Mercedes-Benz brand, has entered the market with a focus on premium electric buses, targeting high-end public transportation and private shuttle services. Proterra Inc, a specialist in electric bus technology, has gained traction in the North American market through its innovative battery technology and modular design approach. CAF Group's Solaris Bus & Coach has carved out a strong position in the European market by offering a wide range of electric bus models and focusing on sustainability. These companies, along with others like King Long, NFI Group, and Van Hool NV, are competing through strategies that include technological innovation, strategic partnerships, geographic expansion, and a focus on total cost of ownership to appeal to transit authorities and private operators.

Porter's Five Forces Analysis of the Electric Bus Market - Competitive forces assessment

Applying Porter's Five Forces analysis to the electric bus market reveals a complex competitive landscape shaped by various factors. The threat of new entrants is moderate, as the market requires significant capital investment and established relationships with public transportation authorities, but the growing demand and potential for technological innovation continue to attract new players. The bargaining power of suppliers is increasing, particularly for critical components such as batteries and electric drivetrains, as the market becomes more specialized and supply chains become more complex. The bargaining power of buyers, primarily public transportation authorities and large private operators, is relatively high due to the commoditization of basic electric bus models and the availability of multiple suppliers. The threat of substitute products is low in the short term, as electric buses offer unique advantages in terms of emissions and operating costs, but could increase in the long term with the development of alternative technologies such as hydrogen fuel cells. Competitive rivalry is intense, with manufacturers competing on factors such as price, technology, range, and after-sales service. The market is also influenced by the threat of forward integration from public transportation authorities and the potential for backward integration by manufacturers to secure battery supplies.

SWOT Analysis of the Electric Bus Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the electric bus market reveals a dynamic industry with significant potential for growth and innovation. The market's strengths include rapidly improving battery technology, increasing government support through incentives and regulations, and growing public awareness of environmental issues. Electric buses offer lower operating costs compared to diesel buses, particularly in terms of energy efficiency and reduced maintenance requirements. However, the market also faces weaknesses such as high upfront costs, limited charging infrastructure in many regions, and concerns about battery lifespan and replacement costs. Opportunities in the market are abundant, including the potential for technological advancements in battery energy density and charging speed, the expansion into emerging markets with growing urban populations, and the integration of smart city technologies with electric bus systems. Threats to the market include potential changes in government policies, competition from alternative technologies such as hydrogen fuel cells, and the risk of supply chain disruptions for critical components like batteries. Additionally, the market faces challenges related to grid capacity and the environmental impact of battery production and disposal.

Electric Bus Market Value Chain Analysis - Industry structure and value flow

The electric bus market value chain is a complex network of interconnected activities and stakeholders, each contributing to the final product and its deployment. At the core of the value chain are the original equipment manufacturers (OEMs) who design and assemble the electric buses, integrating components from various suppliers. The supply side of the value chain includes battery manufacturers, electric motor producers, power electronics suppliers, and charging infrastructure providers. These components are critical to the performance and efficiency of electric buses. The distribution and sales channels involve direct sales to public transportation authorities, private fleet operators, and dealers who facilitate smaller purchases. After-sales service and maintenance form an essential part of the value chain, ensuring the long-term viability and performance of electric bus fleets. The value chain also includes charging infrastructure providers, energy companies, and technology firms that develop fleet management and route optimization software. As the market evolves, we are seeing increased vertical integration, with some manufacturers expanding into battery production and charging infrastructure to capture more value and ensure supply chain stability.

Key Investment Insights in the Electric Bus Market - Strategic investment recommendations

The electric bus market presents numerous investment opportunities across various segments of the value chain. Strategic investments in battery technology companies are particularly attractive, given the critical role of batteries in electric bus performance and the ongoing advancements in energy density and cost reduction. There are also significant opportunities in charging infrastructure development, including fast-charging stations, wireless charging technologies, and smart grid integration systems. Investors should consider opportunities in software and technology companies that are developing fleet management solutions, predictive maintenance tools, and route optimization algorithms specifically for electric bus operations. The market for second-life battery applications, where used electric bus batteries are repurposed for energy storage, represents an emerging investment area with potential for high returns. Additionally, investments in companies focusing on sustainable battery production and recycling technologies could yield long-term benefits as environmental regulations become more stringent. Strategic partnerships between bus manufacturers, technology companies, and energy providers are also worth considering, as these collaborations often lead to innovative solutions and market expansion.

Electric Bus Market Conclusion - Summary and key takeaways

The electric bus market is on a trajectory of rapid growth and transformation, driven by technological advancements, environmental regulations, and changing urban mobility needs. The market's projected expansion from 61.01 Billion to 218.69 Billion by 2033, with a CAGR of 20.01%, underscores the significant potential for stakeholders across the value chain. Key takeaways from the market analysis include the increasing importance of battery technology, the growing adoption of electric buses in public transportation systems, and the critical role of charging infrastructure development. The market is characterized by intense competition among established automotive manufacturers and specialized electric vehicle companies, leading to rapid innovation and product diversification. Regional dynamics play a crucial role, with Asia-Pacific leading in terms of absolute numbers, while Europe and North America focus on technological leadership and sustainability. As the market matures, factors such as total cost of ownership, operational efficiency, and integration with smart city initiatives will become increasingly important. The future of the electric bus market will likely be shaped by continued technological advancements, supportive government policies, and the industry's ability to address challenges related to infrastructure, supply chain, and environmental sustainability.

Research Methodology - How this research was conducted

This comprehensive market research on the electric bus industry was conducted using a rigorous methodology that combines both primary and secondary research techniques. The research process began with an extensive review of existing literature, including industry reports, academic publications, and market data from reputable sources. Primary research was conducted through interviews with industry experts, including executives from leading electric bus manufacturers, public transportation authorities, and technology providers. These interviews provided valuable insights into market trends, technological developments, and future projections. Data collection involved gathering information on market size, growth rates, and competitive landscape from multiple sources to ensure accuracy and reliability. The research also utilized advanced analytical tools to assess market dynamics, including Porter's Five Forces analysis and SWOT analysis. Financial data and market projections were carefully validated through cross-referencing with multiple sources and expert opinions. The research methodology also incorporated a detailed examination of regional markets, considering factors such as government policies, economic conditions, and infrastructure development. Throughout the research process, a focus was maintained on identifying key trends, opportunities, and challenges that will shape the future of the electric bus market.

Research Scope - Coverage and limitations

The scope of this research encompasses a comprehensive analysis of the global electric bus market, covering key segments including battery technology, end-user applications, vehicle types, and hybrid powertrains. The research focuses on major geographic regions, including Asia-Pacific, Europe, North America, Latin America, and the Middle East & Africa, providing insights into regional market dynamics and growth opportunities. The study covers the period from 2025 to 2032, with historical data and future projections to provide a complete market outlook. The research includes an in-depth analysis of key market players, their strategies, and competitive positioning. It also examines technological trends, regulatory frameworks, and investment patterns shaping the industry. However, it's important to note that the research has certain limitations. The rapidly evolving nature of the electric bus market means that some data points may change quickly, and unforeseen technological breakthroughs or policy changes could impact future projections. Additionally, while the research provides a global overview, the availability and reliability of data may vary across different regions, potentially affecting the granularity of analysis in certain markets. The study also focuses primarily on the commercial aspects of the electric bus market and may not fully capture all technological or environmental nuances of the industry.

Key Companies and Recent Developments in the Electric Bus Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The electric bus market is characterized by intense competition and rapid innovation among key players. BYD Company Ltd has maintained its position as a global leader, recently announcing the expansion of its manufacturing facilities in Europe and North America to meet growing demand. The company has also introduced new models with extended range and faster charging capabilities. AB Volvo has made significant strides with the launch of its 7900 Electric model, featuring a modular design that allows for various battery configurations. The company has also announced partnerships with charging infrastructure providers to offer integrated solutions to customers. Daimler AG's Mercedes-Benz eCitaro has seen recent updates, including the introduction of solid-state batteries for improved performance and safety. Proterra Inc has focused on technological innovation, unveiling its next-generation battery technology that promises higher energy density and faster charging times. The company has also announced strategic partnerships with public transportation authorities in several major US cities. CAF Group's Solaris Bus & Coach has strengthened its position in the European market with the introduction of the Urbino 12 electric, featuring advanced driver assistance systems. King Long has expanded its presence in emerging markets, particularly in Latin America and Southeast Asia, through partnerships with local distributors. NFI Group has diversified its electric bus offerings through its various brands, including New Flyer and Alexander Dennis, introducing models with improved range and passenger capacity. Van Hool NV has focused on the European market, recently launching a new electric coach model designed for long-distance travel. These companies, along with others in the market, continue to drive innovation through product launches, strategic partnerships, and expansion into new geographic regions, shaping the future of electric bus technology and adoption.