Debt Collection Software Market Overview - Definition, scope, and significance

Debt collection software represents a specialized category of financial technology solutions designed to automate and streamline the process of recovering outstanding debts on behalf of creditors, lenders, and collection agencies. This software encompasses a comprehensive suite of tools including automated communication systems, payment processing capabilities, compliance management features, and analytics platforms that work together to improve recovery rates while reducing operational costs. The scope of the debt collection software market extends across various industries including banking and financial services, telecommunications, healthcare, retail, and utilities, where unpaid accounts and delinquent payments represent significant financial challenges. The significance of this market has grown substantially as organizations seek to balance the need for effective debt recovery with increasingly complex regulatory requirements and the rising costs of manual collection processes. Modern debt collection software solutions leverage artificial intelligence, machine learning, and data analytics to create more personalized and effective collection strategies while ensuring compliance with consumer protection laws and industry regulations.

Debt Collection Software Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The debt collection software market is primarily driven by the increasing volume of outstanding consumer and commercial debt globally, coupled with the growing complexity of regulatory compliance requirements that necessitate sophisticated technological solutions. Organizations face mounting pressure to improve recovery rates while reducing operational costs, creating strong demand for automated systems that can handle large volumes of accounts efficiently. The shift toward digital-first customer engagement and the proliferation of multiple communication channels have created opportunities for software solutions that can manage omnichannel collection strategies. However, the market faces several restraints including the high initial implementation costs for enterprise-grade solutions, data security and privacy concerns, and the challenge of integrating new systems with legacy infrastructure. Key challenges include maintaining compliance with evolving regulations across different jurisdictions, managing customer experience during the collection process, and addressing the technical limitations of older systems. Opportunities exist in emerging markets where debt collection practices are modernizing, the development of AI-powered predictive analytics for improved recovery strategies, and the expansion of cloud-based solutions that offer greater accessibility and scalability for organizations of all sizes.

Debt Collection Software Market Growth Trends - Current and emerging trends shaping the market

The debt collection software market is experiencing several transformative trends that are reshaping how organizations approach debt recovery. One of the most significant trends is the increasing adoption of artificial intelligence and machine learning algorithms to predict payment behavior, optimize contact strategies, and personalize collection approaches based on individual debtor profiles. The market is also witnessing a strong shift toward cloud-based deployment models, offering greater flexibility, scalability, and cost-effectiveness compared to traditional on-premises solutions. Another emerging trend is the integration of advanced analytics and business intelligence tools that provide deeper insights into collection performance and enable data-driven decision-making. The industry is also seeing increased focus on omnichannel communication capabilities, allowing collectors to engage with debtors through their preferred channels including email, SMS, mobile apps, and social media platforms. Additionally, there is growing emphasis on compliance automation features that help organizations navigate complex regulatory landscapes across different regions. The market is also experiencing innovation in payment processing integration, enabling seamless digital payment options that improve recovery rates and customer satisfaction.

COVID-19 Impact on the Debt Collection Software Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the debt collection software market, creating both challenges and opportunities for industry participants. During the initial pandemic period, many organizations faced significant increases in delinquent accounts and payment defaults across multiple sectors, particularly in retail, hospitality, and consumer services. This surge in bad debt highlighted the critical need for efficient collection processes and accelerated the adoption of automated solutions. The pandemic also forced a rapid digital transformation in collection practices, as traditional face-to-face collection methods became impractical or impossible due to lockdowns and social distancing measures. This shift accelerated the adoption of digital communication channels and remote collection capabilities. However, the economic uncertainty also led to increased regulatory scrutiny and temporary restrictions on collection activities in many jurisdictions, requiring software solutions to quickly adapt to new compliance requirements. As the market recovers, there is evidence of sustained demand for advanced collection software as organizations recognize the long-term benefits of digital transformation in their collection operations. The pandemic has fundamentally changed how organizations approach debt collection, with many implementing more sophisticated, technology-driven strategies that are likely to persist in the post-pandemic landscape.

Debt Collection Software Market Competitive Landscape - Major competitors and market consolidation

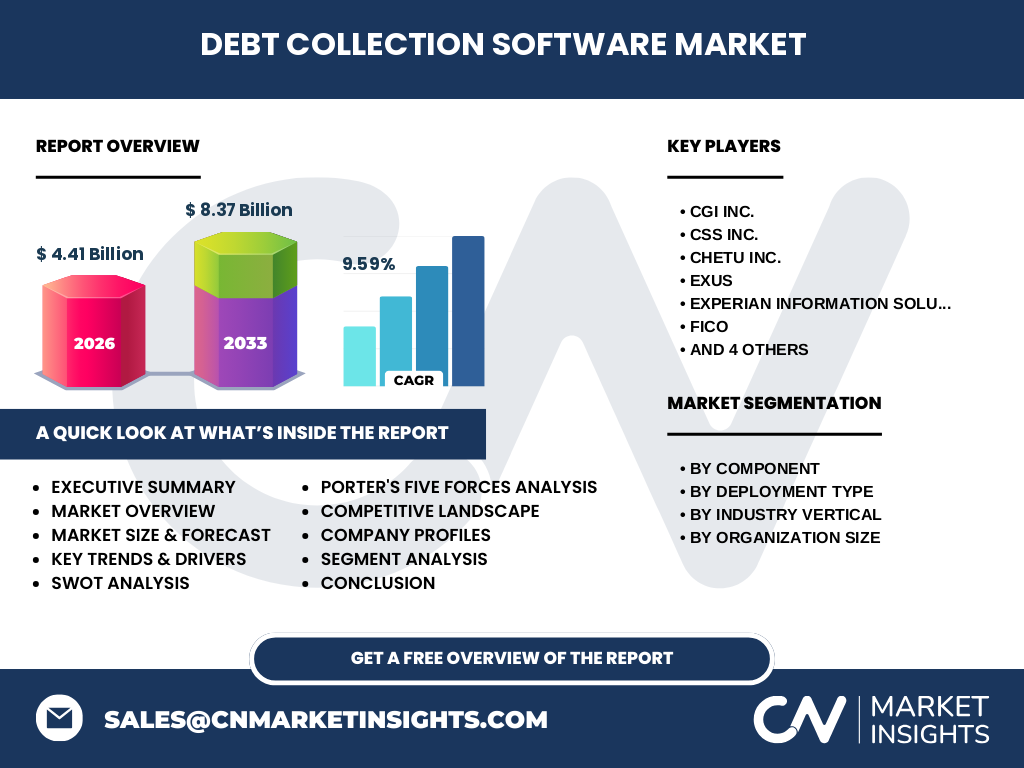

The debt collection software market features a diverse competitive landscape with a mix of established technology providers, specialized collection software vendors, and emerging fintech companies. Major players in the market include CGI Inc., CSS Inc., Chetu Inc., EXUS, Experian Information Solutions Inc., FICO, FIS, Loxon Solutions, Pegasystems Inc., and Quantrax Corporation Inc. These companies compete on various factors including product functionality, integration capabilities, compliance features, pricing models, and customer support services. The market is characterized by ongoing consolidation as larger technology companies acquire specialized collection software providers to expand their product portfolios and market reach. Competition is intensifying as new entrants bring innovative approaches leveraging artificial intelligence, machine learning, and cloud technologies to disrupt traditional collection methods. Companies are increasingly focusing on developing comprehensive platforms that offer end-to-end collection management rather than point solutions, as customers seek integrated systems that can handle the entire collection lifecycle. The competitive landscape is also influenced by regional dynamics, with some vendors having strong presence in specific geographic markets while others operate on a global scale. Strategic partnerships between software providers and payment processors, credit bureaus, and other financial service providers are becoming increasingly common as companies seek to offer more comprehensive solutions to their customers.

Executive Summary - High-level overview and key findings about Debt Collection Software Market

The debt collection software market is positioned for substantial growth over the forecast period, driven by the increasing need for efficient debt recovery solutions and the ongoing digital transformation of financial services. The market is projected to grow from $4.41 billion in 2026 to $8.37 billion by 2033, representing a robust compound annual growth rate of 9.59%. This growth is fueled by the rising volume of consumer and commercial debt, increasing regulatory complexity, and the need for organizations to improve collection efficiency while managing costs. The market is characterized by a diverse range of solutions catering to different industry verticals, deployment preferences, and organizational sizes. Cloud-based solutions are gaining significant traction due to their scalability and cost-effectiveness, while large enterprises continue to invest in comprehensive platforms that offer advanced analytics and integration capabilities. The competitive landscape is dynamic, with both established players and innovative newcomers competing to provide the most effective and compliant collection solutions. Key trends shaping the market include the adoption of artificial intelligence and machine learning technologies, the shift toward omnichannel communication strategies, and the increasing focus on compliance automation. As organizations continue to face challenges in managing delinquent accounts, the demand for sophisticated debt collection software solutions is expected to remain strong throughout the forecast period.

Debt Collection Software Market Forecast - Projections for 2025-2032 period

The debt collection software market is projected to experience significant growth throughout the 2025-2032 forecast period, with the market size expected to expand from $4.41 billion in 2026 to $8.37 billion by 2033, representing a compound annual growth rate of 9.59%. This robust growth trajectory is driven by several factors including the increasing volume of outstanding debt globally, the continued digital transformation of financial services, and the growing complexity of regulatory compliance requirements. The forecast period will likely see accelerated adoption of cloud-based solutions as organizations seek more flexible and cost-effective alternatives to traditional on-premises systems. The integration of artificial intelligence and machine learning capabilities into collection software is expected to become more prevalent, driving improvements in recovery rates and operational efficiency. Industry vertical segmentation will continue to evolve, with particular growth expected in sectors such as healthcare, retail, and telecommunications where debt management challenges are particularly acute. The market will also likely see increased demand for solutions that can handle the growing complexity of consumer debt portfolios and provide more sophisticated analytics and reporting capabilities. Regional growth patterns will vary, with developed markets continuing to invest in advanced solutions while emerging markets present significant opportunities for expansion as debt collection practices modernize.

Debt Collection Software Market Size and Share by Segmentation - Breakdown by {segmentData}

The debt collection software market can be segmented across multiple dimensions, each offering distinct growth opportunities and market dynamics. By component, the market is divided into software and services, with software solutions representing the larger share due to the increasing demand for comprehensive collection platforms. The software segment is further characterized by the growing preference for cloud-based solutions over on-premises deployments, driven by their scalability and lower total cost of ownership. In terms of deployment type, cloud-based solutions are experiencing faster growth rates compared to traditional on-premises systems, reflecting the broader trend toward digital transformation in financial services. By industry vertical, the banking, financial services, and insurance (BFSI) sector currently dominates the market, accounting for the largest share due to the high volume of consumer and commercial debt managed by financial institutions. However, the IT & telecom sector is showing strong growth potential as telecommunications companies face increasing challenges with unpaid bills and service disconnects. The retail sector also represents a significant market segment, particularly as e-commerce continues to grow and create new debt management challenges. By organization size, large enterprises currently hold the majority market share due to their greater resources for investment in sophisticated collection solutions, but the small and medium enterprise (SME) segment is expected to show the fastest growth as cloud-based solutions make advanced collection capabilities more accessible to smaller organizations.

Global Debt Collection Software Market Size and Share by Region - Geographic distribution

The global debt collection software market exhibits distinct regional characteristics and growth patterns across different geographic areas. North America currently represents the largest regional market, driven by the high volume of consumer debt, sophisticated financial services infrastructure, and early adoption of advanced collection technologies. The United States, in particular, has a well-established market for debt collection software, with numerous vendors offering specialized solutions and a regulatory environment that, while complex, provides clear guidelines for collection practices. Europe represents the second-largest regional market, characterized by diverse regulatory environments across different countries and a growing emphasis on consumer protection in debt collection practices. The Asia-Pacific region is expected to show the fastest growth during the forecast period, driven by rapid economic development, increasing consumer lending, and the modernization of debt collection practices in emerging economies such as China and India. Latin America presents significant growth opportunities due to the large informal economy and increasing formalization of debt collection practices, while the Middle East and Africa region is experiencing gradual growth as financial services infrastructure develops and regulatory frameworks evolve. Regional variations in debt collection regulations, economic conditions, and technological adoption rates create unique market dynamics in each geographic area, requiring vendors to adapt their solutions to local requirements and preferences.

Regional Analysis of the Debt Collection Software Market - Detailed regional market performance

Regional analysis of the debt collection software market reveals significant variations in market maturity, growth rates, and adoption patterns across different geographic areas. In North America, the market is characterized by high technology adoption rates, sophisticated regulatory frameworks, and a mature ecosystem of software providers. The United States leads the region with a well-developed market for both enterprise and mid-market collection solutions, while Canada shows steady growth driven by the increasing complexity of debt collection regulations and the need for compliance management tools. Europe presents a diverse landscape with significant variations between Western and Eastern European markets. Western European countries such as the United Kingdom, Germany, and France have well-established markets for collection software, driven by strict consumer protection regulations and the need for compliance with GDPR requirements. Eastern European markets are experiencing faster growth as debt collection practices modernize and regulatory frameworks develop. The Asia-Pacific region shows the most dynamic growth patterns, with developed markets such as Australia and Singapore leading in technology adoption while emerging economies such as China, India, and Southeast Asian countries present significant growth opportunities as their financial services sectors expand. The region's growth is driven by increasing consumer lending, mobile payment adoption, and the need for more efficient collection processes. Latin America and the Middle East & Africa regions, while currently smaller markets, are showing promising growth as economic development progresses and regulatory frameworks for debt collection become more established.

Leading Company Profiles in the Debt Collection Software Market - Industry players and strategies

The debt collection software market features several prominent players, each with distinct strategic approaches and areas of specialization. CGI Inc. is a global IT consulting and systems integration company that offers comprehensive debt collection solutions as part of its financial services portfolio, focusing on large enterprise clients and complex integration requirements. CSS Inc. specializes in collection management software with a strong emphasis on compliance features and regulatory reporting capabilities, serving both financial institutions and collection agencies. Chetu Inc. provides custom software development services for debt collection applications, offering tailored solutions that address specific client requirements across various industry verticals. EXUS offers specialized debt collection and management software with a focus on the European market, providing solutions that address the region's complex regulatory requirements. Experian Information Solutions Inc. leverages its extensive data assets and analytics capabilities to provide collection software that integrates credit information and predictive analytics for improved recovery strategies. FICO brings its expertise in analytics and decision management to the debt collection market, offering solutions that use advanced algorithms to optimize collection strategies. FIS provides comprehensive financial technology solutions including debt collection software as part of its broader portfolio of banking and payments technology. Loxon Solutions focuses on providing collection software for the telecommunications and utility sectors, addressing the specific challenges of these industries. Pegasystems Inc. offers a unified platform that includes debt collection capabilities, leveraging its expertise in business process management and customer relationship management. Quantrax Corporation Inc. specializes in providing collection software for the ARM (accounts receivable management) industry, offering solutions that cater to collection agencies and third-party debt buyers.

Porter's Five Forces Analysis of the Debt Collection Software Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the debt collection software market. The threat of new entrants is moderate, as the market requires significant technical expertise, regulatory knowledge, and established relationships with financial institutions, creating barriers to entry. However, the growing demand for innovative solutions and the shift toward cloud-based platforms have lowered some barriers, allowing new players with innovative approaches to enter the market. The bargaining power of buyers is increasing as organizations become more sophisticated in their technology procurement and seek solutions that offer greater flexibility, integration capabilities, and value for money. Large enterprise customers, in particular, have significant negotiating power due to their volume requirements and ability to influence product development. The bargaining power of suppliers is relatively low, as there are numerous software component providers and technology partners available to support collection software development. However, suppliers of specialized compliance and regulatory data may have moderate bargaining power due to the critical nature of their services. The threat of substitute products or services is moderate, as organizations could theoretically develop in-house solutions or rely on manual processes, but the complexity of modern collection requirements and regulatory compliance makes comprehensive software solutions increasingly necessary. Competitive rivalry in the market is intense, with numerous established players and new entrants competing on factors such as functionality, compliance features, pricing, and customer support. The market is also characterized by ongoing consolidation as larger companies acquire specialized providers to expand their capabilities and market reach.

SWOT Analysis of the Debt Collection Software Market - Strengths, weaknesses, opportunities, threats

A comprehensive SWOT analysis of the debt collection software market reveals several key factors influencing its development and growth potential. Strengths of the market include the increasing sophistication of technology solutions that offer improved recovery rates and operational efficiency, the growing demand for compliance management tools in an increasingly regulated environment, and the expanding range of features and capabilities that address diverse industry needs. The market also benefits from strong growth drivers including the rising volume of consumer and commercial debt, the ongoing digital transformation of financial services, and the increasing recognition of the importance of effective debt management. However, the market also faces certain weaknesses, including the high implementation costs and complexity of enterprise-grade solutions, the challenges of integrating new systems with legacy infrastructure, and the potential for negative customer experiences if collection practices are not properly managed. Data security and privacy concerns represent ongoing challenges, particularly as solutions handle sensitive financial information. Opportunities in the market are significant and include the growing adoption of artificial intelligence and machine learning technologies, the expansion of cloud-based solutions that offer greater accessibility and scalability, and the potential for growth in emerging markets where debt collection practices are modernizing. The increasing focus on customer experience in collection processes also presents opportunities for innovative solutions that balance recovery effectiveness with consumer protection. Threats to the market include evolving regulatory requirements that may increase compliance costs, economic downturns that could lead to increased default rates and collection challenges, and the potential for new technologies or approaches to disrupt traditional collection models.

Debt Collection Software Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the debt collection software market reveals a complex ecosystem of interconnected activities and participants that contribute to the creation and delivery of collection solutions. At the foundation of the value chain are software developers and technology providers who create the core collection platforms and applications, investing in research and development to incorporate advanced features such as artificial intelligence, machine learning, and predictive analytics. These developers work closely with data providers and credit bureaus who supply the critical information needed for effective collection strategies, including consumer credit data, payment history, and contact information. System integrators and implementation partners play a crucial role in customizing solutions for specific client needs, ensuring proper integration with existing systems, and providing training and support services. Cloud service providers form another essential layer of the value chain, offering the infrastructure and platform services that enable scalable, accessible collection solutions. Financial institutions, collection agencies, and other end-users represent the primary customers who purchase and implement these solutions to manage their debt recovery operations. Throughout the value chain, regulatory compliance specialists and legal advisors provide essential guidance to ensure that collection practices and software solutions adhere to applicable laws and regulations across different jurisdictions. Payment processors and financial technology partners contribute by enabling seamless payment processing capabilities within collection software, improving recovery rates and customer experience. The value chain is characterized by increasing collaboration and integration among participants as the market moves toward more comprehensive, end-to-end collection solutions that address the full spectrum of debt recovery needs.

Key Investment Insights in the Debt Collection Software Market - Strategic investment recommendations

The debt collection software market presents several compelling investment opportunities for both strategic and financial investors. Key investment insights suggest focusing on companies that are developing innovative solutions leveraging artificial intelligence and machine learning technologies, as these capabilities are increasingly becoming essential differentiators in the market. Investors should consider opportunities in cloud-based collection platforms, which offer significant advantages in terms of scalability, accessibility, and cost-effectiveness compared to traditional on-premises solutions. The growing emphasis on compliance automation presents another attractive investment area, as organizations seek solutions that can navigate complex regulatory requirements across different jurisdictions. Strategic investors, particularly those in the financial services and technology sectors, may find value in acquiring specialized collection software providers to expand their product portfolios and enter new market segments. The small and medium enterprise (SME) segment represents an underserved market with significant growth potential, as cloud-based solutions make advanced collection capabilities more accessible to smaller organizations. Investors should also consider the geographic expansion opportunities in emerging markets where debt collection practices are modernizing and regulatory frameworks are developing. Companies that offer comprehensive, integrated solutions that address the full collection lifecycle, from early-stage delinquency management to legal collections, are likely to be attractive investment targets. Additionally, investments in companies that prioritize customer experience and ethical collection practices may offer long-term advantages as the industry faces increasing scrutiny and the need to balance recovery effectiveness with consumer protection.

Debt Collection Software Market Conclusion - Summary and key takeaways

The debt collection software market is experiencing robust growth and transformation, driven by the increasing need for efficient debt recovery solutions in an increasingly complex regulatory and economic environment. With the market projected to grow from $4.41 billion in 2026 to $8.37 billion by 2033 at a CAGR of 9.59%, the opportunities for vendors, investors, and end-users are substantial. The market is characterized by technological innovation, with artificial intelligence, machine learning, and cloud computing reshaping how organizations approach debt collection. Key trends include the shift toward omnichannel communication strategies, the growing importance of compliance automation, and the increasing focus on customer experience in collection processes. The competitive landscape is dynamic, featuring a mix of established technology providers, specialized collection software vendors, and innovative newcomers, with ongoing consolidation as companies seek to expand their capabilities and market reach. Regional variations in market maturity, regulatory requirements, and growth rates create diverse opportunities across different geographic areas. As organizations continue to face challenges in managing delinquent accounts and navigating complex regulatory environments, the demand for sophisticated debt collection software solutions is expected to remain strong. Success in this market will require vendors to balance technological innovation with regulatory compliance, customer experience considerations, and the ability to address diverse industry needs across different market segments and geographic regions.

Research Methodology - How this research was conducted

The research methodology employed for this debt collection software market analysis combines multiple approaches to ensure comprehensive and accurate insights. The study utilizes both primary and secondary research methods to gather and validate market data. Primary research includes interviews with industry experts, software vendors, end-users, and other stakeholders in the debt collection ecosystem. These interviews provide valuable qualitative insights into market trends, challenges, and opportunities, as well as validation of quantitative data. Secondary research encompasses a thorough review of industry reports, company financial statements, regulatory filings, trade publications, and market databases. This approach allows for the collection of historical data and the identification of long-term trends in the market. The research also incorporates data triangulation techniques, where information from multiple sources is cross-validated to ensure accuracy and reliability. Market size and forecast calculations are based on a combination of top-down and bottom-up approaches, considering factors such as the number of potential customers, average spending on collection software, and regional economic conditions. The segmentation analysis is derived from a detailed examination of market characteristics, customer needs, and vendor offerings across different dimensions including component, deployment type, industry vertical, and organization size. The competitive landscape analysis is based on a comprehensive evaluation of vendor capabilities, market positioning, and strategic initiatives. Throughout the research process, particular attention is paid to maintaining objectivity and avoiding bias, with data sources carefully selected for their credibility and relevance to the debt collection software market.

Research Scope - Coverage and limitations

The research scope for this debt collection software market analysis encompasses a comprehensive examination of the global market, including market size, growth projections, segmentation analysis, competitive landscape, and regional dynamics. The study covers the period from 2025 to 2032, with specific focus on the forecast period and historical context to provide meaningful trend analysis. The research includes detailed segmentation by component (software and services), deployment type (on-premises and cloud), industry vertical (IT & telecom, BFSI, retail, manufacturing), and organization size (large enterprises and SMEs). Regional coverage includes North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with analysis of key countries and market dynamics within each region. The competitive landscape analysis profiles major market players including CGI Inc., CSS Inc., Chetu Inc., EXUS, Experian Information Solutions Inc., FICO, FIS, Loxon Solutions, Pegasystems Inc., and Quantrax Corporation Inc., examining their strategies, product offerings, and market positioning. The research also explores key trends, drivers, restraints, opportunities, and challenges shaping the market. Limitations of the research include the availability and reliability of data in certain regions, particularly in emerging markets where collection software adoption is still developing. The study also acknowledges the challenges of accurately forecasting market growth in a dynamic environment influenced by factors such as regulatory changes, economic conditions, and technological disruption. Additionally, the research focuses specifically on software solutions for debt collection and does not extensively cover related areas such as credit risk management or broader financial technology solutions, unless directly relevant to the collection software market.

Key Companies and Recent Developments in the Debt Collection Software Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The debt collection software market features several key companies that are driving innovation and shaping the industry through strategic developments and new product offerings. CGI Inc. has recently expanded its financial services portfolio with enhanced collection management solutions that incorporate advanced analytics and artificial intelligence capabilities, targeting large enterprise clients with complex integration requirements. CSS Inc. announced a major platform upgrade focused on improving compliance automation features and omnichannel communication capabilities, addressing the growing regulatory complexity in debt collection practices. Chetu Inc. has been actively developing custom collection software solutions for emerging markets, with recent projects focusing on mobile-first collection platforms for regions with high smartphone penetration but limited traditional banking infrastructure. EXUS has strengthened its position in the European market through strategic partnerships with local financial institutions, launching region-specific solutions that address the unique regulatory requirements of different European countries. Experian Information Solutions Inc. has integrated its extensive data assets with advanced collection software capabilities, introducing predictive analytics tools that help organizations optimize their collection strategies based on comprehensive consumer credit information. FICO has expanded its decision management platform to include enhanced debt collection modules, leveraging its expertise in analytics to provide more sophisticated recovery strategies and risk assessment capabilities. FIS has made significant investments in cloud-based collection solutions, launching new products that offer greater scalability and integration with its broader financial technology ecosystem. Loxon Solutions has focused on the telecommunications and utility sectors, recently announcing partnerships with major service providers to implement specialized collection solutions that address industry-specific challenges. Pegasystems Inc. has enhanced its unified platform with advanced collection capabilities, incorporating robotic process automation and intelligent automation features to improve operational efficiency. Quantrax Corporation Inc. has strengthened its position in the ARM industry through continuous product innovation, recently launching new features focused on improving agent productivity and compliance management for collection agencies.