Facade Market Overview - Definition, scope, and significance

The facade market encompasses the design, manufacturing, and installation of exterior building envelopes, including curtain walls, windows, doors, and cladding systems. This market serves the construction industry by providing critical building components that protect structures from environmental elements while enhancing aesthetic appeal and energy efficiency. Facades play a vital role in modern architecture, serving as the primary interface between interior spaces and the external environment. The market includes various materials such as glass, metal, ceramic, and wood, catering to residential, commercial, and industrial applications. As building codes become more stringent regarding energy performance and sustainability, the facade market has gained significant importance in meeting these evolving requirements.

Facade Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The facade market is driven by rapid urbanization, increasing construction activities, and growing demand for energy-efficient buildings. Stringent government regulations promoting sustainable construction and the rising adoption of smart building technologies are propelling market growth. However, the market faces restraints such as high initial costs, complex installation processes, and the need for specialized labor. Challenges include supply chain disruptions, fluctuating raw material prices, and the technical difficulties associated with retrofitting existing structures. Opportunities exist in the development of innovative materials, integration of renewable energy systems, and the expansion of green building certifications. The market is also benefiting from technological advancements in facade systems, including self-cleaning surfaces and dynamic glazing solutions.

Facade Market Growth Trends - Current and emerging trends shaping the market

The facade market is witnessing several notable growth trends, including the increasing adoption of sustainable and energy-efficient materials. There is a growing preference for smart facades that can adapt to environmental conditions, such as electrochromic glass that changes opacity based on sunlight intensity. The market is also seeing a rise in the use of lightweight composite materials that offer improved thermal performance and durability. Prefabrication and modular construction techniques are gaining traction, allowing for faster installation and reduced on-site waste. Additionally, there is an emerging trend toward biophilic design, incorporating natural elements into facade systems to enhance occupant well-being and connection to nature.

COVID-19 Impact on the Facade Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly impacted the facade market through supply chain disruptions, labor shortages, and project delays. Construction activities were halted in many regions, leading to a temporary decline in demand for facade systems. However, the market demonstrated resilience as the construction industry adapted to new safety protocols and implemented digital technologies for remote collaboration. The pandemic also accelerated the adoption of prefabrication and modular construction methods, which reduce on-site labor requirements. As economies recover, the facade market is experiencing a rebound driven by pent-up demand, government stimulus packages for infrastructure development, and the increasing focus on building health and wellness features.

Facade Market Competitive Landscape - Major competitors and market consolidation

The facade market features a competitive landscape with both established multinational corporations and regional players. Key companies such as Saint-Gobain S.A., Kingspan Group Plc, and Aluplex India Pvt Ltd dominate the market with their extensive product portfolios and global presence. The market is characterized by strategic partnerships, mergers, and acquisitions as companies seek to expand their geographical reach and technological capabilities. Competition is intensifying as firms invest in research and development to introduce innovative products that meet evolving sustainability and performance standards. The market also sees collaboration between facade manufacturers and architects to develop customized solutions for high-profile projects.

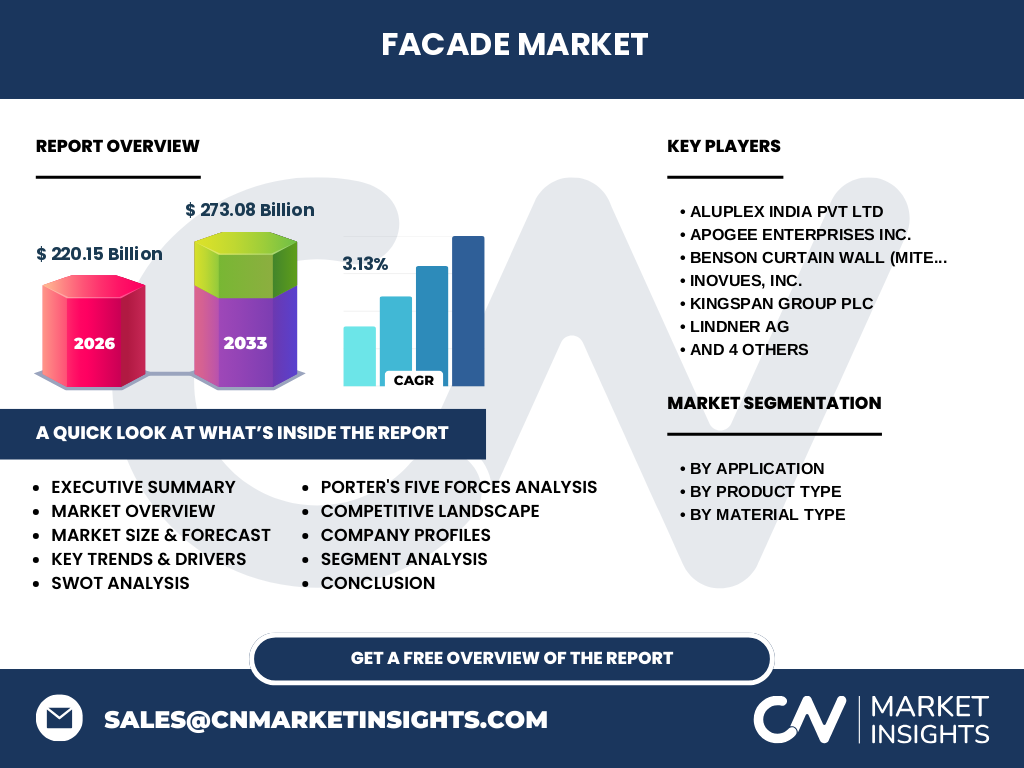

Executive Summary - High-level overview and key findings about Facade Market

The facade market is a dynamic sector within the construction industry, valued at approximately 220.15 billion in 2026 and projected to reach 273.08 billion by 2033, growing at a CAGR of 3.13%. The market is segmented by application (residential, commercial, and industrial), product type (windows, doors, and curtain walling), and material type (glass, metal, ceramic, and wood). Key drivers include urbanization, energy efficiency regulations, and technological advancements, while challenges encompass high costs and complex installation requirements. The competitive landscape is characterized by major players such as Saint-Gobain S.A. and Kingspan Group Plc, with regional variations in market dynamics. The COVID-19 pandemic initially disrupted the market but has since led to increased adoption of digital technologies and prefabrication methods.

Facade Market Forecast - Projections for 2025-2032 period

The facade market is projected to experience steady growth from 2025 to 2032, with a compound annual growth rate of 3.13%. Starting from a market size of 220.15 billion in 2026, the market is expected to reach 273.08 billion by 2033. This growth is driven by increasing construction activities, particularly in emerging economies, and the ongoing emphasis on energy-efficient building envelopes. The commercial sector is anticipated to remain the largest application segment, while curtain walling is expected to see the highest growth among product types due to its widespread use in high-rise buildings. Glass and metal materials will continue to dominate the market, with innovations in these materials further driving adoption.

Facade Market Size and Share by Segmentation - Breakdown by {segmentData}

The facade market is segmented by application, product type, and material type. By application, the commercial sector holds the largest market share, driven by the construction of office buildings, retail spaces, and hospitality facilities. The residential segment is also significant, particularly in regions with high housing demand. In terms of product type, curtain walling accounts for a substantial portion of the market due to its use in modern high-rise construction. Windows and doors represent the remaining share, with increasing demand for energy-efficient variants. By material type, glass dominates the market, followed by metal, ceramic, and wood. Glass facades are favored for their aesthetic appeal and ability to maximize natural light, while metal offers durability and design flexibility.

Global Facade Market Size and Share by Region - Geographic distribution

The global facade market exhibits varying dynamics across different regions. Asia-Pacific is the largest and fastest-growing market, driven by rapid urbanization and infrastructure development in countries like China and India. North America and Europe represent mature markets with a focus on retrofitting and energy-efficient upgrades to existing buildings. The Middle East and Africa region shows strong potential due to ongoing construction projects and a preference for high-end facade systems in commercial buildings. Latin America is experiencing steady growth, supported by economic development and increasing construction activities. Regional variations in building codes, climate conditions, and architectural preferences influence the demand for specific facade types and materials.

Regional Analysis of the Facade Market - Detailed regional market performance

The facade market demonstrates distinct regional characteristics and growth patterns. In Asia-Pacific, particularly in China and India, the market is booming due to massive urban development projects and the construction of smart cities. North America focuses on sustainable building practices and retrofitting existing structures with energy-efficient facades. Europe emphasizes strict energy performance standards and the use of innovative materials to meet green building certifications. The Middle East, especially the Gulf Cooperation Council (GCC) countries, invests heavily in iconic architectural projects featuring advanced facade systems. Latin America shows steady growth, with Brazil and Mexico leading the market. Each region's unique climatic conditions, building regulations, and economic factors influence the adoption of specific facade technologies and materials.

Leading Company Profiles in the Facade Market - Industry players and strategies

Key players in the facade market include Saint-Gobain S.A., Kingspan Group Plc, and Aluplex India Pvt Ltd, among others. These companies have established strong market positions through extensive product portfolios, global distribution networks, and continuous innovation. Saint-Gobain S.A. focuses on sustainable solutions and has a diverse range of facade products catering to various applications. Kingspan Group Plc emphasizes energy efficiency and has developed advanced insulation systems for facades. Aluplex India Pvt Ltd leverages its expertise in aluminum-based facade systems to serve the growing Asian market. These companies employ strategies such as strategic partnerships, mergers and acquisitions, and investment in research and development to maintain their competitive edge and expand their market presence.

Porter's Five Forces Analysis of the Facade Market - Competitive forces assessment

The facade market's competitive landscape is shaped by Porter's Five Forces. The threat of new entrants is moderate due to high capital requirements and the need for technical expertise. Bargaining power of suppliers is significant, particularly for specialized materials like high-performance glass and advanced composites. The bargaining power of buyers is increasing as they demand more customized solutions and energy-efficient products. The threat of substitutes is relatively low, as facades are essential building components with few alternatives. Competitive rivalry is intense, with numerous players competing on price, quality, and innovation. The market is also influenced by the bargaining power of contractors and architects who specify facade systems for construction projects.

SWOT Analysis of the Facade Market - Strengths, weaknesses, opportunities, threats

The facade market's strengths include its essential role in modern construction, the availability of diverse materials and technologies, and the growing emphasis on energy efficiency. Weaknesses encompass high initial costs, complex installation processes, and vulnerability to economic downturns affecting the construction industry. Opportunities exist in the development of smart facade systems, expansion into emerging markets, and the increasing demand for sustainable building solutions. Threats include intense competition, potential supply chain disruptions, and the risk of technological obsolescence as new materials and systems emerge. The market must also navigate challenges related to changing building codes and regulations across different regions.

Facade Market Value Chain Analysis - Industry structure and value flow

The facade market's value chain consists of several key stages, starting with raw material suppliers who provide glass, metals, ceramics, and wood. These materials are then processed by manufacturers who create facade components such as curtain walls, windows, and doors. Distributors and wholesalers play a crucial role in supplying these products to contractors and construction companies. Architects and engineers specify facade systems for projects, while contractors handle the installation. End-users, including building owners and developers, ultimately benefit from the facade systems' performance and aesthetics. The value chain is characterized by close collaboration between stakeholders to ensure product quality, compliance with regulations, and successful project delivery.

Key Investment Insights in the Facade Market - Strategic investment recommendations

Strategic investment opportunities in the facade market include focusing on energy-efficient and sustainable facade systems, which are increasingly in demand due to stricter building codes and environmental awareness. Investors should consider companies developing smart facade technologies that can adapt to environmental conditions and integrate with building management systems. There is also potential in expanding into emerging markets, particularly in Asia-Pacific and the Middle East, where rapid urbanization is driving construction growth. Investments in research and development to create innovative materials with improved thermal performance and durability are likely to yield returns. Additionally, companies offering comprehensive facade solutions, including design, manufacturing, and installation services, present attractive investment prospects.

Facade Market Conclusion - Summary and key takeaways

The facade market is a critical component of the construction industry, valued at 220.15 billion in 2026 and projected to grow to 273.08 billion by 2033 at a CAGR of 3.13%. The market is driven by urbanization, energy efficiency regulations, and technological advancements, while facing challenges such as high costs and complex installation processes. Key trends include the adoption of smart facade systems, sustainable materials, and prefabrication techniques. The competitive landscape is characterized by major players like Saint-Gobain S.A. and Kingspan Group Plc, with regional variations in market dynamics. Despite the initial impact of COVID-19, the market is recovering and adapting to new construction practices. Strategic investments in energy-efficient and smart facade technologies present significant opportunities for growth.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology that combines primary and secondary research. Primary research involved interviews with industry experts, facade manufacturers, and construction professionals to gather insights on market trends, challenges, and opportunities. Secondary research included analysis of company annual reports, industry publications, and government databases to validate market size and growth projections. The research team employed both top-down and bottom-up approaches to estimate market size and share by application, product type, and material type. Data triangulation was used to ensure accuracy and reliability of the findings. The forecast period of 2025-2032 was determined based on historical data analysis and expert opinions on future market developments.

Research Scope - Coverage and limitations

This research covers the global facade market, focusing on key regions including North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America. The study examines market dynamics by application (residential, commercial, and industrial), product type (windows, doors, and curtain walling), and material type (glass, metal, ceramic, and wood). The research scope includes market size, growth trends, competitive landscape, and key player strategies. However, it is important to note that the research does not cover every single market participant or regional variation in detail. The study also does not account for potential future technological disruptions that could significantly alter market dynamics. Additionally, the research is based on available data and may not capture every local market nuance or emerging trend in real-time.

Key Companies and Recent Developments in the Facade Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Leading companies in the facade market, such as Saint-Gobain S.A., Kingspan Group Plc, and Aluplex India Pvt Ltd, have been actively pursuing strategic developments to strengthen their market positions. Saint-Gobain S.A. has announced investments in smart glass technologies and sustainable facade solutions, aligning with global energy efficiency trends. Kingspan Group Plc has launched new high-performance insulation systems for facades, enhancing thermal efficiency in buildings. Aluplex India Pvt Ltd has expanded its manufacturing capabilities to meet growing demand in the Asian market. Additionally, companies like Benson Curtain Wall and Inovues, Inc. have introduced innovative curtain walling systems with improved installation efficiency. Strategic partnerships between facade manufacturers and technology providers are becoming increasingly common, focusing on integrating smart building technologies into facade systems. These developments reflect the industry's commitment to innovation, sustainability, and meeting evolving market demands.