Asset Integrity Management Market Overview - Definition, scope, and significance

Asset Integrity Management (AIM) refers to the systematic approach of ensuring that physical assets across various industries continue to perform their required functions effectively and efficiently while protecting health, safety, and the environment. The scope of AIM encompasses a comprehensive range of activities including inspection, maintenance, repair, and operational processes designed to preserve the integrity of assets throughout their lifecycle. This market is significant because it directly impacts operational reliability, safety compliance, and cost optimization for industries that rely on complex physical infrastructure. AIM has become increasingly critical as industries face aging infrastructure, stringent regulatory requirements, and the need to maximize asset performance while minimizing environmental impact and operational risks.

Asset Integrity Management Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the Asset Integrity Management market include increasing regulatory compliance requirements across industries, aging infrastructure in developed economies, and the growing focus on operational safety and environmental protection. The oil and gas industry's expansion, particularly in offshore operations, creates substantial demand for AIM services. However, the market faces restraints such as high implementation costs and the complexity of integrating AIM systems with existing infrastructure. Challenges include the shortage of skilled professionals, technological obsolescence, and the difficulty of managing assets in harsh environments. Opportunities exist in the digital transformation of AIM through IoT integration, predictive maintenance technologies, and the expansion of AIM services into emerging markets where industrial infrastructure is rapidly developing.

Asset Integrity Management Market Growth Trends - Current and emerging trends shaping the market

The Asset Integrity Management market is experiencing significant growth trends driven by digital transformation and technological advancement. The integration of artificial intelligence and machine learning into AIM systems is enabling predictive maintenance capabilities that reduce downtime and optimize asset performance. Cloud-based AIM solutions are gaining traction due to their scalability and accessibility, allowing real-time monitoring and data analysis across geographically dispersed assets. The adoption of digital twins technology is emerging as a powerful trend, providing virtual representations of physical assets for enhanced monitoring and decision-making. Additionally, there is a growing emphasis on sustainability and environmental compliance, driving demand for AIM services that can help organizations meet their environmental, social, and governance (ESG) objectives while maintaining operational efficiency.

COVID-19 Impact on the Asset Integrity Management Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the Asset Integrity Management market through supply chain interruptions, project delays, and reduced industrial activity across sectors. Many organizations postponed non-critical maintenance activities and inspections to conserve resources during the economic uncertainty. However, the pandemic also accelerated the adoption of digital AIM solutions as remote monitoring and virtual inspections became necessary due to travel restrictions and social distancing requirements. The recovery trajectory shows a strong rebound as industries prioritize asset reliability and safety to prevent costly failures and ensure business continuity. The pandemic has heightened awareness of the importance of robust AIM systems, particularly in critical infrastructure sectors, leading to increased investment in digital AIM technologies that enable remote operations and predictive maintenance capabilities.

Asset Integrity Management Market Competitive Landscape - Major competitors and market consolidation

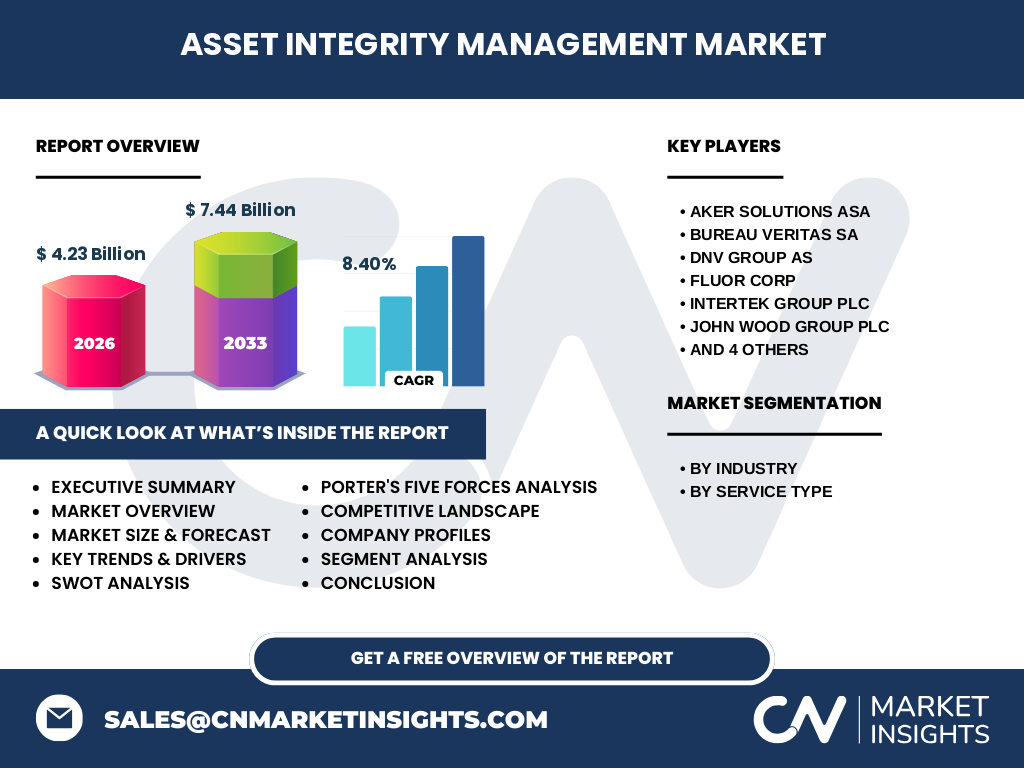

The Asset Integrity Management market features a moderately consolidated competitive landscape with several key players dominating the industry. Major competitors include Aker Solutions ASA, Bureau Veritas SA, DNV Group AS, Fluor Corp, Intertek Group Plc, John Wood Group Plc, Oceaneering International Inc, ROSEN Group, SGS SA, and TechnipFMC plc. These companies compete based on their technical expertise, global presence, service portfolio breadth, and technological capabilities. Market consolidation is occurring through strategic mergers, acquisitions, and partnerships as companies seek to expand their service offerings and geographic reach. The competitive landscape is characterized by a mix of large multinational corporations with comprehensive AIM capabilities and specialized niche players focusing on specific industries or service types. Competition is intensifying as digital transformation creates opportunities for both established players and new entrants to differentiate their offerings.

Executive Summary - High-level overview and key findings about Asset Integrity Management Market

The Asset Integrity Management market is positioned for substantial growth, with market size projected to increase from $4.23 billion in 2026 to $7.44 billion by 2033, representing a robust CAGR of 8.40%. This growth is driven by increasing industrial activity, aging infrastructure, and the critical need for safety and compliance across multiple sectors. The market is segmented by industry, with oil & gas, power, marine, mining, and aerospace being the primary sectors, and by service type, including non-destructive testing inspection, corrosion management, pipeline integrity management, structural integrity management, and risk-based inspection. Key players are investing heavily in digital technologies and expanding their service portfolios to capture growing market opportunities. The market presents significant potential for companies that can offer integrated, technology-driven AIM solutions that address the evolving needs of asset-intensive industries.

Asset Integrity Management Market Forecast - Projections for 2025-2032 period

The Asset Integrity Management market is projected to experience substantial growth during the 2025-2032 period, with the market size expected to reach $7.44 billion by 2033 from $4.23 billion in 2026. This represents a compound annual growth rate of 8.40% over the forecast period. The growth trajectory is supported by increasing industrial investments, particularly in emerging economies, and the ongoing digital transformation of AIM services. The forecast indicates particularly strong growth in services related to predictive maintenance and digital monitoring solutions, as industries seek to optimize asset performance and reduce operational costs. Geographic expansion in Asia-Pacific and the Middle East regions is expected to contribute significantly to market growth, driven by industrialization and infrastructure development in these regions.

Asset Integrity Management Market Size and Share by Segmentation - Breakdown by {segmentData}

The Asset Integrity Management market is segmented by industry and service type, with each segment showing distinct growth patterns. By industry, the oil & gas sector currently represents the largest market share due to the critical nature of asset integrity in this high-risk industry and the extensive infrastructure involved. The power sector follows closely, driven by the need to maintain aging power generation and transmission assets. By service type, non-destructive testing inspection services account for a significant portion of the market due to their widespread application across all industries. Corrosion management services are experiencing rapid growth, particularly in industries dealing with harsh environments. Pipeline integrity management is a specialized but essential segment, especially for the oil & gas industry, while structural integrity management and risk-based inspection services are gaining traction as industries adopt more sophisticated AIM approaches.

Global Asset Integrity Management Market Size and Share by Region - Geographic distribution

The global Asset Integrity Management market exhibits varying growth patterns across different geographic regions. North America and Europe currently dominate the market due to their mature industrial infrastructure and stringent regulatory frameworks requiring comprehensive AIM services. These regions have a high concentration of aging assets that require ongoing integrity management, driving consistent demand for AIM services. The Asia-Pacific region is emerging as the fastest-growing market, fueled by rapid industrialization, infrastructure development, and increasing awareness of asset integrity importance in countries like China, India, and Southeast Asian nations. The Middle East and Africa region, particularly the Gulf Cooperation Council countries, represents significant growth potential due to extensive oil & gas operations and ongoing infrastructure projects. Latin America shows moderate growth, primarily driven by the oil & gas and mining sectors in countries like Brazil and Chile.

Regional Analysis of the Asset Integrity Management Market - Detailed regional market performance

Regional analysis reveals distinct market dynamics across different geographic areas. In North America, the market is characterized by high technology adoption rates and strict regulatory compliance requirements, with the United States leading due to its extensive oil & gas infrastructure and power generation assets. Europe shows strong growth driven by environmental regulations and the need to maintain aging industrial infrastructure, with countries like Norway and the UK being particularly active in offshore oil & gas AIM services. The Asia-Pacific region presents a dynamic growth environment, with China and India investing heavily in industrial infrastructure and power generation, creating substantial demand for AIM services. The Middle East focuses primarily on oil & gas AIM services, with countries like Saudi Arabia and the UAE investing in both traditional and renewable energy infrastructure. Latin America's market is closely tied to the performance of its natural resource sectors, particularly oil & gas in Brazil and mining in Chile and Peru.

Leading Company Profiles in the Asset Integrity Management Market - Industry players and strategies

The Asset Integrity Management market features several prominent companies with distinct strategic approaches. Aker Solutions ASA focuses on providing integrated AIM solutions for the oil & gas industry, leveraging its engineering expertise and global presence. Bureau Veritas SA offers comprehensive inspection and certification services across multiple industries, emphasizing quality and compliance. DNV Group AS specializes in technical assurance and risk management, particularly in the maritime and energy sectors. Fluor Corp provides engineering, procurement, and construction services with integrated AIM capabilities. Intertek Group Plc offers testing, inspection, and certification services across diverse industries. John Wood Group Plc delivers integrated energy services with strong AIM capabilities. Oceaneering International Inc specializes in offshore oil & gas AIM services. ROSEN Group focuses on pipeline integrity management solutions. SGS SA provides inspection, verification, testing, and certification services globally. TechnipFMC plc offers technology solutions for the energy industry with integrated AIM services. These companies are increasingly investing in digital technologies and expanding their service portfolios to maintain competitive advantage.

Porter's Five Forces Analysis of the Asset Integrity Management Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics of the Asset Integrity Management market. The threat of new entrants is moderate due to the high capital requirements, technical expertise needed, and established relationships between existing players and major industrial clients. Bargaining power of suppliers is relatively low as AIM services primarily rely on human expertise and standardized equipment. The bargaining power of buyers is moderate to high, particularly for large industrial clients who can negotiate pricing and service terms, though the specialized nature of AIM services limits buyer leverage. The threat of substitute products or services is low as AIM represents a specialized field with few alternatives for ensuring asset integrity. Competitive rivalry is intense among established players, characterized by price competition, service differentiation, and technological innovation. The market shows signs of consolidation as larger players acquire specialized firms to expand capabilities and geographic reach.

SWOT Analysis of the Asset Integrity Management Market - Strengths, weaknesses, opportunities, threats

Strengths of the Asset Integrity Management market include the critical nature of AIM services across industries, the growing adoption of digital technologies, and the increasing regulatory emphasis on safety and environmental compliance. Weaknesses encompass the high costs associated with implementing comprehensive AIM systems, the shortage of skilled professionals, and the complexity of integrating new technologies with legacy systems. Opportunities exist in the expansion of digital AIM solutions, the growing demand for predictive maintenance capabilities, and the increasing focus on sustainability and environmental compliance. Threats include economic downturns that may reduce industrial investment, potential regulatory changes that could impact service requirements, and the rapid pace of technological change that may render existing solutions obsolete. The market also faces competition from in-house AIM capabilities developed by large industrial organizations and the potential for commoditization of certain AIM services.

Asset Integrity Management Market Value Chain Analysis - Industry structure and value flow

The Asset Integrity Management market value chain encompasses several key stages, beginning with raw data collection through sensors, inspections, and monitoring systems. This data flows to analysis and processing stages where specialized software and human expertise transform raw information into actionable insights. Service providers then deliver these insights through various AIM services including inspection, maintenance planning, and risk assessment. The value chain extends to implementation, where maintenance and repair activities are executed based on AIM recommendations. Technology providers supply the tools and platforms that enable modern AIM capabilities, while consulting firms offer strategic guidance on AIM program development and optimization. The final stage involves continuous monitoring and improvement, creating a cyclical process that enhances asset performance over time. This value chain is characterized by significant integration between technology providers, service companies, and end-user industries, with digital transformation creating new opportunities for value creation throughout the chain.

Key Investment Insights in the Asset Integrity Management Market - Strategic investment recommendations

Strategic investment in the Asset Integrity Management market should focus on several key areas to maximize returns. Digital transformation represents the most significant investment opportunity, with companies that develop or adopt AI-powered predictive maintenance solutions, IoT integration capabilities, and cloud-based AIM platforms positioned for strong growth. Investment in specialized service areas such as corrosion management and pipeline integrity management offers opportunities in high-growth niches with strong barriers to entry. Geographic expansion into emerging markets, particularly in Asia-Pacific and the Middle East, presents substantial growth potential as these regions industrialize and develop their infrastructure. Companies should also consider investing in talent development and training programs to address the skilled professional shortage in the AIM sector. Strategic partnerships and acquisitions can provide accelerated access to new technologies, service capabilities, and geographic markets. Finally, investments in sustainability-focused AIM solutions that help clients meet environmental compliance requirements represent a growing opportunity as ESG considerations become increasingly important across industries.

Asset Integrity Management Market Conclusion - Summary and key takeaways

The Asset Integrity Management market is experiencing robust growth, driven by increasing industrial activity, aging infrastructure, and the critical need for safety and compliance across multiple sectors. With a projected market size increase from $4.23 billion in 2026 to $7.44 billion by 2033 at a CAGR of 8.40%, the market presents significant opportunities for companies that can offer integrated, technology-driven AIM solutions. The market is characterized by strong competition among major players who are investing in digital transformation and expanding their service portfolios. Key growth drivers include the oil & gas industry's expansion, particularly in offshore operations, and the increasing adoption of digital technologies such as AI, IoT, and predictive maintenance. Challenges remain in the form of high implementation costs and the shortage of skilled professionals. Companies that can successfully navigate these challenges while capitalizing on emerging opportunities in digital AIM solutions and geographic expansion are well-positioned for success in this growing market.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology combining primary and secondary research approaches. Primary research involved interviews with industry experts, service providers, and end-users to gather firsthand insights into market dynamics, challenges, and opportunities. Secondary research included analysis of industry reports, company financial statements, regulatory documents, and market databases to validate findings and establish market size and growth projections. The research methodology employed both top-down and bottom-up approaches to estimate market size, with segmentation analysis providing detailed insights into specific market segments. Data triangulation was used to ensure accuracy and reliability of the findings. The research also incorporated analysis of recent developments, partnerships, and strategic initiatives by key market players to provide a comprehensive view of the competitive landscape and market trends.

Research Scope - Coverage and limitations

This research covers the global Asset Integrity Management market from 2025 to 2033, with a particular focus on key market segments including industry verticals (oil & gas, power, marine, mining, aerospace) and service types (non-destructive testing inspection, corrosion management, pipeline integrity management, structural integrity management, risk-based inspection). The geographic scope encompasses major markets in North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America. The research provides detailed analysis of market size, growth trends, competitive landscape, and key players. Limitations of the research include the availability of public data for certain regions and market segments, potential variations in market definitions across different sources, and the inherent uncertainty in long-term market projections. The research focuses on commercial AIM services and does not extensively cover in-house AIM capabilities developed by large industrial organizations.

Key Companies and Recent Developments in the Asset Integrity Management Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Asset Integrity Management market features several key companies that are shaping the industry through innovation and strategic initiatives. Aker Solutions ASA has been focusing on digital transformation of AIM services, launching new software platforms for predictive maintenance and asset monitoring. Bureau Veritas SA recently announced expanded services in renewable energy asset integrity management, reflecting the industry's shift toward sustainable energy sources. DNV Group AS has strengthened its position through partnerships with technology companies to enhance its digital AIM capabilities, particularly in the maritime sector. Fluor Corp has been investing in advanced inspection technologies and expanding its AIM service portfolio through strategic acquisitions. Intertek Group Plc has launched new corrosion management solutions incorporating AI and machine learning for enhanced predictive capabilities. John Wood Group Plc has formed partnerships with technology providers to offer integrated digital AIM solutions for the energy sector. Oceaneering International Inc has expanded its offshore AIM services with new remotely operated vehicle (ROV) inspection capabilities. ROSEN Group has introduced advanced pipeline inspection technologies using electromagnetic acoustic transducers. SGS SA has expanded its global presence through strategic acquisitions in emerging markets. TechnipFMC plc has launched integrated AIM solutions combining hardware and software for enhanced asset monitoring and maintenance planning. These developments reflect the industry's focus on digital transformation, geographic expansion, and service diversification to meet evolving client needs.