Automotive Semiconductor Market Overview - Definition, scope, and significance

The Automotive Semiconductor Market encompasses the specialized integrated circuits, sensors, microcontrollers, and other electronic components designed specifically for automotive applications. These semiconductors are engineered to withstand harsh automotive environments including extreme temperatures, vibration, and electromagnetic interference while meeting stringent safety and reliability standards. The market covers components used across various vehicle systems including powertrain control, infotainment, advanced driver assistance systems (ADAS), body electronics, and safety systems. As vehicles become increasingly electrified and autonomous, automotive semiconductors have become the backbone of modern transportation technology, enabling critical functions from engine management to autonomous driving capabilities. The significance of this market lies in its fundamental role in vehicle functionality, safety, and the ongoing transformation of the automotive industry toward electric and autonomous vehicles.

Automotive Semiconductor Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the Automotive Semiconductor Market include the rapid electrification of vehicles, increasing demand for ADAS features, and the growing trend toward autonomous driving capabilities. Stringent emission regulations worldwide are pushing automakers to adopt more sophisticated powertrain control systems, while consumer demand for connected and intelligent vehicles continues to rise. The transition from internal combustion engines to electric vehicles creates substantial demand for power electronics and battery management systems. However, the market faces several restraints including supply chain disruptions, semiconductor shortages, and the high cost of advanced automotive-grade components. Technical challenges such as ensuring functional safety, cybersecurity, and long-term reliability in automotive applications present ongoing obstacles. Despite these challenges, significant opportunities exist in emerging technologies such as 5G connectivity, artificial intelligence for autonomous vehicles, and the development of semiconductors specifically designed for electric vehicle applications.

Automotive Semiconductor Market Growth Trends - Current and emerging trends shaping the market

The Automotive Semiconductor Market is experiencing transformative growth trends driven by technological evolution and changing consumer expectations. One of the most significant trends is the consolidation of electronic control units (ECUs) into centralized computing architectures, which requires more powerful and integrated semiconductor solutions. The shift toward electric vehicles is creating unprecedented demand for power semiconductors, battery management systems, and charging infrastructure components. Another emerging trend is the development of AI-specific chips for autonomous driving applications, enabling real-time processing of sensor data for vehicle perception and decision-making. The automotive industry's transition to 5G connectivity is driving demand for high-bandwidth communication semiconductors. Additionally, there is a growing trend toward software-defined vehicles, where functionality can be updated and enhanced through over-the-air updates, requiring more flexible and powerful semiconductor platforms. The market is also seeing increased adoption of advanced packaging technologies and heterogeneous integration to improve performance while reducing size and power consumption.

COVID-19 Impact on the Automotive Semiconductor Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the Automotive Semiconductor Market, initially causing severe disruptions in production and supply chains. Factory shutdowns across Asia, Europe, and North America led to significant production delays and inventory shortages. The pandemic exposed vulnerabilities in the just-in-time manufacturing model prevalent in the automotive industry, resulting in cascading effects throughout the supply chain. Interestingly, while automotive demand initially plummeted, the subsequent recovery was stronger than expected, creating a mismatch between semiconductor supply and automotive demand. This imbalance led to one of the most severe semiconductor shortages in automotive history, forcing automakers to prioritize production of higher-margin vehicles and delay launches of new models. The recovery trajectory shows gradual improvement as semiconductor manufacturers increase capacity and automakers diversify their supplier base. The crisis has accelerated strategic initiatives including vertical integration, regional supply chain development, and increased inventory buffers to enhance supply chain resilience.

Automotive Semiconductor Market Competitive Landscape - Major competitors and market consolidation

The Automotive Semiconductor Market features a highly competitive landscape dominated by both specialized automotive semiconductor companies and diversified technology giants. The market is characterized by intense competition in terms of technology innovation, reliability, and automotive-grade certifications. Key players are engaged in strategic partnerships with automakers to develop custom solutions and secure long-term supply agreements. The competitive environment is further intensified by the entry of new players from the consumer electronics and technology sectors seeking to capitalize on the automotive industry's transformation. Market consolidation is evident through mergers, acquisitions, and strategic alliances aimed at expanding technological capabilities and market reach. Companies are competing not only on component performance but also on comprehensive solutions that include software, development tools, and technical support. The competitive dynamics are shaped by the need for functional safety certification, cybersecurity capabilities, and the ability to support the complex requirements of electric and autonomous vehicles.

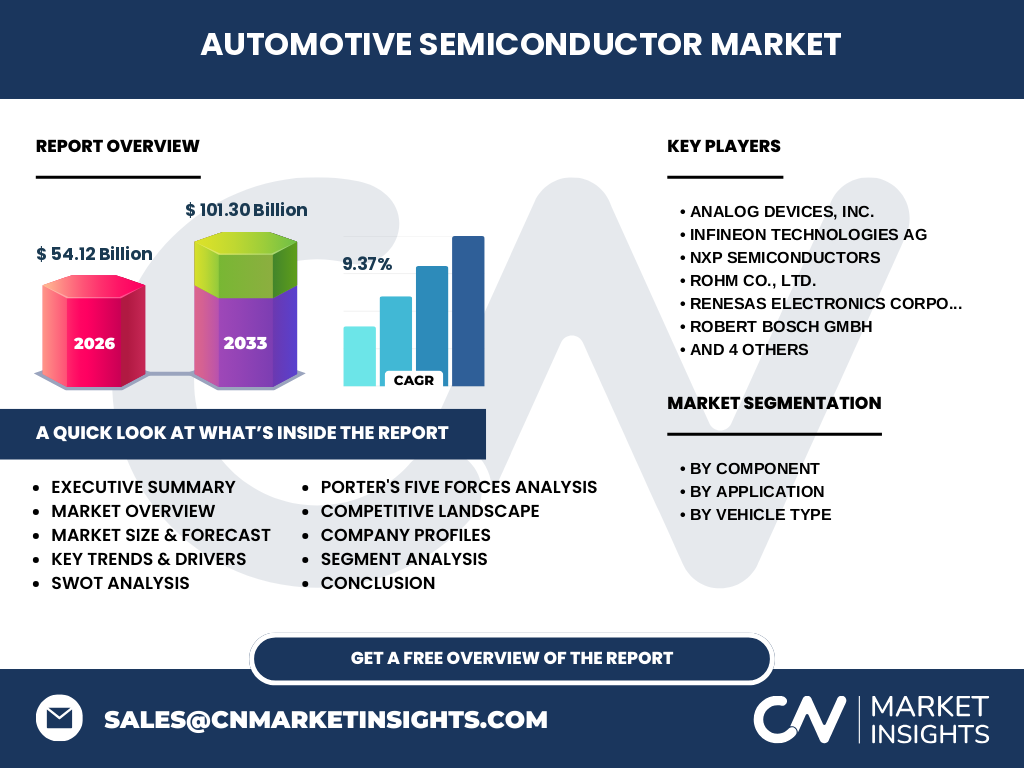

Executive Summary - High-level overview and key findings about Automotive Semiconductor Market

The Automotive Semiconductor Market is positioned for substantial growth, with market size projected to increase from 54.12 Billion in 2026 to 101.30 Billion by 2033, representing a robust CAGR of 9.37%. This growth is driven by the automotive industry's fundamental transformation toward electrification, connectivity, and autonomy. The market is characterized by increasing semiconductor content per vehicle, with electric vehicles requiring significantly more semiconductor content than traditional internal combustion engine vehicles. Key findings indicate that the shift toward software-defined vehicles and centralized computing architectures is creating demand for more powerful and integrated semiconductor solutions. The market is witnessing a convergence of automotive and technology industries, with traditional semiconductor companies facing competition from new entrants with expertise in AI, connectivity, and cloud computing. Strategic imperatives for market participants include developing solutions for electric vehicles, enhancing functional safety capabilities, and building resilient supply chains. The market presents significant opportunities for companies that can deliver innovative, reliable, and cost-effective semiconductor solutions that address the evolving needs of the automotive industry.

Automotive Semiconductor Market Forecast - Projections for 2025-2032 period

The Automotive Semiconductor Market is forecast to experience substantial growth throughout the 2025-2032 period, with the market expanding from 54.12 Billion to 101.30 Billion. This represents a compound annual growth rate of 9.37%, reflecting the accelerating adoption of electric vehicles, increasing semiconductor content per vehicle, and the proliferation of advanced automotive features. The forecast period will likely see continued strong demand for power semiconductors, microcontrollers, and sensors as the automotive industry undergoes its most significant transformation in decades. Key growth drivers during this period include the increasing penetration of electric vehicles across all vehicle segments, the advancement of autonomous driving technologies, and the continued evolution of connected vehicle platforms. The market is expected to benefit from ongoing technological innovations in semiconductor manufacturing processes, packaging technologies, and integration capabilities. Regional variations in growth rates are anticipated, with emerging markets showing particularly strong expansion as automotive production and adoption of advanced vehicle technologies accelerate in these regions.

Automotive Semiconductor Market Size and Share by Segmentation - Breakdown by {segmentData}

The Automotive Semiconductor Market segmentation reveals distinct patterns in component demand, application requirements, and vehicle type preferences. By component, the market encompasses optical components, sensors & actuators, memory, microcontrollers, analog ICs, and logic and discrete power devices, each serving critical functions in modern vehicles. The application segmentation includes advanced driver assistance systems, body electronics, infotainment, powertrain, and safety systems, with ADAS and powertrain applications showing particularly strong growth due to electrification and autonomy trends. Vehicle type segmentation covers passenger vehicles, light commercial vehicles (LCV), and heavy commercial vehicles (HCV), with passenger vehicles currently dominating the market but commercial vehicles showing increasing adoption of advanced semiconductor technologies. The market share distribution varies significantly across these segments, with power devices and microcontrollers commanding substantial portions due to their fundamental role in vehicle operation, while specialized components such as optical sensors for autonomous driving represent emerging high-growth segments.

Global Automotive Semiconductor Market Size and Share by Region - Geographic distribution

The global Automotive Semiconductor Market exhibits distinct regional characteristics and growth patterns across major geographic areas. Asia-Pacific represents the largest regional market, driven by the concentration of automotive manufacturing in countries such as China, Japan, South Korea, and increasingly India. This region benefits from strong domestic demand, government support for electric vehicles, and the presence of major automotive and semiconductor manufacturers. Europe follows as a significant market, characterized by stringent emission regulations, strong adoption of electric vehicles, and the presence of premium automotive brands that drive demand for advanced semiconductor technologies. North America shows robust growth potential, supported by technological innovation, strong consumer demand for connected and autonomous vehicles, and increasing electric vehicle adoption. Other regions, including Latin America and the Middle East & Africa, represent emerging markets with growing automotive production and increasing adoption of advanced vehicle technologies. Regional market dynamics are influenced by factors such as government policies, infrastructure development, consumer preferences, and the presence of automotive manufacturing hubs.

Regional Analysis of the Automotive Semiconductor Market - Detailed regional market performance

Regional analysis of the Automotive Semiconductor Market reveals significant variations in market maturity, growth rates, and technology adoption across different geographic areas. Asia-Pacific dominates the regional landscape, accounting for the largest market share due to its comprehensive automotive manufacturing ecosystem, strong domestic demand, and aggressive electric vehicle policies, particularly in China. The region benefits from established semiconductor manufacturing capabilities and increasing vertical integration by automotive companies. Europe represents a mature market characterized by rapid electric vehicle adoption, stringent emission standards, and strong demand for advanced driver assistance systems. The region's focus on sustainability and technological leadership drives continuous innovation in automotive semiconductors. North America shows distinctive characteristics including strong demand for premium vehicles, advanced technological infrastructure, and increasing investments in autonomous driving technologies. The region benefits from the presence of major technology companies and a robust startup ecosystem focused on automotive innovation. Emerging regions demonstrate varying levels of market development, with some showing rapid growth potential as automotive production and technology adoption increase.

Leading Company Profiles in the Automotive Semiconductor Market - Industry players and strategies

The Automotive Semiconductor Market features several leading companies that have established strong positions through technological expertise, strategic partnerships, and comprehensive product portfolios. Analog Devices, Inc. has built a reputation for precision analog and mixed-signal solutions critical for automotive applications. Infineon Technologies AG specializes in power semiconductors and microcontrollers, with a strong focus on energy efficiency and automotive applications. NXP Semiconductors has developed comprehensive automotive solutions including processors for infotainment and domain control applications. ROHM CO., LTD. offers a diverse portfolio of automotive-grade semiconductors with particular strength in power devices and analog ICs. Renesas Electronics Corporation provides a wide range of automotive microcontrollers and system-on-chip solutions. Robert Bosch GmbH, while primarily known as an automotive supplier, has developed significant semiconductor capabilities through its in-house manufacturing. STMicroelectronics offers a broad portfolio of automotive semiconductors including power management and MEMS sensors. Semiconductor Components Industries, LLC focuses on discrete and analog semiconductors for automotive applications. TOSHIBA CORPORATION provides power semiconductors and memory solutions for automotive use. Texas Instruments Incorporated offers a comprehensive range of automotive-grade analog and embedded processing solutions.

Porter's Five Forces Analysis of the Automotive Semiconductor Market - Competitive forces assessment

Porter's Five Forces analysis of the Automotive Semiconductor Market reveals a complex competitive landscape shaped by multiple strategic forces. The threat of new entrants is moderate but increasing, as technology companies from adjacent industries bring new capabilities and business models to the automotive sector. However, high barriers to entry exist due to the need for automotive-grade certification, significant R&D investments, and established relationships with automakers. The bargaining power of buyers (automakers) is substantial, as they represent concentrated demand and can influence pricing and technical specifications. Conversely, the bargaining power of suppliers (semiconductor manufacturers) varies, with some specialized suppliers holding strong positions while others face competitive pressure. The threat of substitute products is relatively low in the short term but could increase as new technologies emerge and alternative approaches to vehicle functionality are developed. Competitive rivalry within the market is intense, characterized by technological innovation, price competition, and the struggle for market share in rapidly evolving application areas such as electric vehicles and autonomous driving systems.

SWOT Analysis of the Automotive Semiconductor Market - Strengths, weaknesses, opportunities, threats

A comprehensive SWOT analysis of the Automotive Semiconductor Market reveals significant insights into the industry's strategic position. Strengths include the market's fundamental importance to vehicle functionality, the increasing semiconductor content per vehicle, and the growing demand for advanced automotive features. The industry benefits from strong technological capabilities, established automotive-grade certification processes, and long-term relationships with major automotive manufacturers. Weaknesses include vulnerability to supply chain disruptions, the high cost of automotive-grade development and certification, and the long product lifecycles that can slow innovation. Opportunities abound in emerging technologies such as electric vehicles, autonomous driving, and connected vehicles, as well as in expanding markets in developing regions and the potential for new business models through software-defined vehicles. Threats include intense competition from both established players and new entrants, rapid technological changes that can render existing solutions obsolete, and geopolitical factors affecting supply chains and trade relationships. The market also faces challenges from economic cycles affecting automotive production and potential regulatory changes impacting technology development.

Automotive Semiconductor Market Value Chain Analysis - Industry structure and value flow

The Automotive Semiconductor Market value chain encompasses a complex network of activities from raw material suppliers through to end customers, with multiple layers of value creation and distribution. The chain begins with suppliers of raw materials and manufacturing equipment, followed by semiconductor foundries and fabrication facilities that produce the basic semiconductor components. Design houses and intellectual property providers create the architectural and functional designs that enable advanced features. Automotive semiconductor companies then integrate these components into specialized solutions meeting the rigorous requirements of the automotive industry. Tier-1 suppliers incorporate these semiconductors into more comprehensive electronic control units and systems, which are then integrated by automakers into complete vehicles. Throughout this chain, value is added through technological innovation, quality assurance, reliability testing, and the development of software and development tools. The value chain is characterized by long development cycles, significant capital investments, and the need for close collaboration between participants to ensure compatibility and functionality across the entire automotive system.

Key Investment Insights in the Automotive Semiconductor Market - Strategic investment recommendations

Strategic investment insights for the Automotive Semiconductor Market highlight several key areas for potential growth and value creation. Investors should consider the strong growth trajectory of electric vehicle-related semiconductors, including power devices, battery management systems, and on-board charging solutions, as the automotive industry undergoes its most significant transformation in decades. Advanced driver assistance systems and autonomous driving technologies represent another compelling investment opportunity, driven by increasing consumer demand for safety features and regulatory support for vehicle automation. The shift toward software-defined vehicles creates investment potential in more powerful and flexible computing platforms, as well as in the development of over-the-air update capabilities. Regional investment strategies should consider the varying growth rates and technology adoption patterns across different geographic markets, with particular attention to Asia-Pacific's dominant position and rapid growth. Strategic partnerships and vertical integration initiatives by major automotive companies present both opportunities and risks that investors should carefully evaluate. The market's vulnerability to supply chain disruptions also suggests investment potential in companies developing more resilient supply chain models and regional manufacturing capabilities.

Automotive Semiconductor Market Conclusion - Summary and key takeaways

The Automotive Semiconductor Market stands at a pivotal juncture, characterized by robust growth projections, technological transformation, and significant market opportunities. With the market size expected to nearly double from 54.12 Billion to 101.30 Billion by 2033 at a CAGR of 9.37%, the industry is benefiting from the automotive sector's fundamental shift toward electrification, connectivity, and autonomy. Key takeaways include the increasing semiconductor content per vehicle, the growing importance of specialized automotive-grade components, and the convergence of automotive and technology industries. The market is characterized by strong competition among established players and new entrants, with success dependent on technological innovation, reliability, and the ability to meet evolving automotive requirements. Strategic imperatives for market participants include developing solutions for electric vehicles, enhancing functional safety capabilities, and building resilient supply chains. The market presents significant opportunities for companies that can deliver innovative, reliable, and cost-effective semiconductor solutions that address the evolving needs of the automotive industry while navigating the challenges of supply chain complexity and rapid technological change.

Research Methodology - How this research was conducted

The research methodology employed for this Automotive Semiconductor Market analysis combines multiple approaches to ensure comprehensive and accurate market insights. Primary research forms a crucial component, involving interviews with industry experts, semiconductor manufacturers, automotive OEMs, and supply chain participants to gather firsthand information about market trends, challenges, and opportunities. Secondary research encompasses extensive review of industry reports, company financial statements, technical publications, and market databases to validate findings and provide historical context. The analysis incorporates both top-down and bottom-up approaches to market sizing, starting with broad industry estimates and refining them through detailed examination of component categories, applications, and vehicle types. Data triangulation techniques are employed to cross-verify information from multiple sources, ensuring reliability and accuracy. The methodology also includes careful consideration of macroeconomic factors, regulatory environments, and technological trends that influence market dynamics. Geographic analysis is conducted through regional data collection and assessment of local market conditions, automotive production volumes, and technology adoption rates.

Research Scope - Coverage and limitations

The research scope for this Automotive Semiconductor Market analysis encompasses the comprehensive examination of semiconductor components specifically designed for automotive applications across all major vehicle categories and geographic regions. The scope includes detailed analysis of component types, applications, vehicle categories, and market dynamics from 2025 through 2033, with particular focus on the projected growth from 54.12 Billion to 101.30 Billion. Coverage extends to key market players, competitive landscape, technological trends, and regional market variations. However, the research has certain limitations inherent to market analysis. These include potential variations in data availability across different regions, the challenge of obtaining precise market share information due to the proprietary nature of many companies' data, and the difficulty of accurately forecasting long-term market dynamics in a rapidly evolving technological landscape. Additionally, the analysis is constrained by the availability of public information regarding certain niche applications and emerging technologies. The scope also does not extend to detailed technical specifications of individual components or proprietary information held by specific companies.

Key Companies and Recent Developments in the Automotive Semiconductor Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Automotive Semiconductor Market features several key companies that have recently announced significant developments shaping the industry landscape. Analog Devices, Inc. has introduced advanced sensor technologies for electric vehicle battery management systems and enhanced its portfolio of automotive-grade precision components. Infineon Technologies AG has announced new silicon carbide power semiconductors designed specifically for electric vehicle applications, offering improved efficiency and thermal performance. NXP Semiconductors has launched next-generation automotive processors with enhanced security features and AI capabilities for autonomous driving applications. ROHM CO., LTD. has developed new power management ICs optimized for electric vehicle charging systems and introduced automotive-grade LED drivers for advanced lighting applications. Renesas Electronics Corporation has announced strategic partnerships with major automakers to develop custom semiconductor solutions for next-generation electric vehicles. Robert Bosch GmbH has expanded its semiconductor manufacturing capabilities with new production facilities focused on automotive applications. STMicroelectronics has launched innovative MEMS sensors for advanced driver assistance systems and introduced new power semiconductors for electric vehicle powertrains. Semiconductor Components Industries, LLC has announced the development of enhanced discrete power devices for automotive applications. TOSHIBA CORPORATION has introduced new automotive-grade memory solutions and power semiconductors for electric vehicle applications. Texas Instruments Incorporated has launched advanced analog and embedded processing solutions specifically designed for electric vehicle and autonomous driving applications. These developments reflect the industry's focus on addressing the growing demands of electric vehicles, autonomous driving, and connected vehicle technologies.