Submarine Cable System Market Overview - Definition, scope, and significance

The submarine cable system market encompasses the design, manufacturing, installation, and maintenance of undersea telecommunications and power transmission cables that connect continents and islands across the world's oceans. These sophisticated networks form the backbone of global internet infrastructure, carrying over 95% of international data traffic, including voice calls, internet connectivity, and financial transactions. Beyond telecommunications, submarine cables also serve critical energy transmission needs, enabling the interconnection of power grids across vast distances. The market includes various cable types such as single-core and multi-core configurations, different capacity tiers ranging from less than 10 Tb/s to over 30 Tb/s, and comprehensive service offerings including installation, maintenance, and upgrade solutions. The significance of this market lies in its fundamental role in enabling global connectivity, supporting economic growth, and facilitating the digital transformation of societies worldwide.

Submarine Cable System Market Drivers, Restraints, Challenges, and Opportunities

The submarine cable system market is primarily driven by the exponential growth in global data traffic, increasing demand for high-speed internet connectivity, and the expansion of cloud computing services. The proliferation of 5G networks and the Internet of Things (IoT) further amplifies the need for robust undersea infrastructure. However, the market faces several restraints, including high installation and maintenance costs, geopolitical tensions affecting cable routes, and environmental concerns related to seabed disruption. Technical challenges such as cable damage from ship anchors, fishing activities, and natural disasters pose ongoing operational risks. Despite these challenges, significant opportunities exist in emerging markets, particularly in Africa and Southeast Asia, where digital infrastructure development is accelerating. The transition to renewable energy sources also creates new demand for power transmission submarine cables, while advancements in cable technology, such as higher capacity and improved durability, open doors for market expansion.

Submarine Cable System Market Growth Trends

The submarine cable system market is experiencing several transformative growth trends that are reshaping the industry landscape. One prominent trend is the increasing demand for higher capacity cables, with the industry moving toward systems capable of transmitting 20 Tb/s and beyond to accommodate growing data volumes. Another significant trend is the shift toward shorter cable routes connecting regional hubs, complementing traditional transoceanic cables. The market is also witnessing increased collaboration between content providers and cable operators, with tech giants like Google, Facebook, and Amazon investing directly in submarine cable infrastructure. Additionally, there is a growing emphasis on cable route diversification to enhance network resilience and reduce single points of failure. The integration of advanced monitoring systems and predictive maintenance technologies is becoming standard practice, improving operational efficiency and reducing downtime. Furthermore, the market is seeing increased interest in dynamic cable systems that can be repositioned as needed, offering greater flexibility in meeting changing connectivity demands.

COVID-19 Impact on the Submarine Cable System Market

The COVID-19 pandemic had a profound impact on the submarine cable system market, initially causing disruptions in manufacturing, installation, and maintenance activities due to lockdowns and travel restrictions. Supply chain interruptions led to delays in cable production and component deliveries, while social distancing measures complicated on-site installation and repair operations. However, the pandemic also accelerated demand for digital connectivity as remote work, online education, and digital entertainment became ubiquitous. This surge in internet usage highlighted the critical importance of submarine cable infrastructure, leading to increased investment in capacity expansion and network resilience. The recovery trajectory has been robust, with the market rebounding strongly as restrictions eased and the need for enhanced digital infrastructure became more apparent. The pandemic has fundamentally shifted perceptions about the essential nature of submarine cables, positioning them as critical infrastructure comparable to roads and energy networks, which is likely to influence future investment and policy decisions in the sector.

Submarine Cable System Market Competitive Landscape

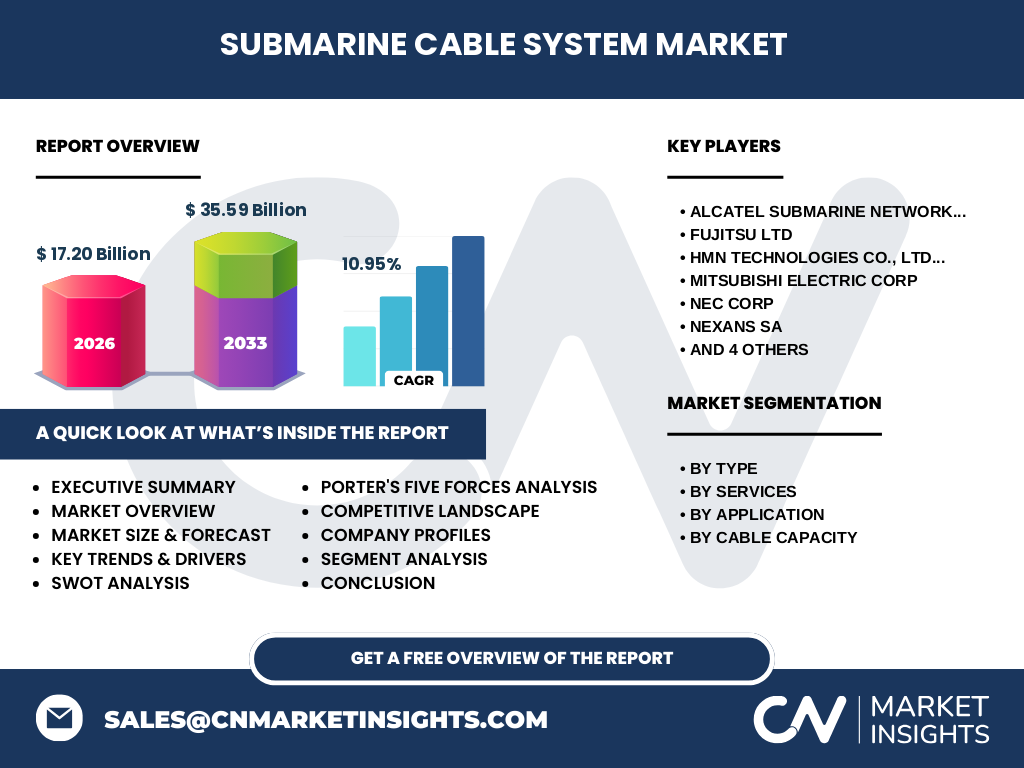

The submarine cable system market features a concentrated competitive landscape dominated by a handful of specialized manufacturers and system integrators. Key players include Alcatel Submarine Networks, Prysmian SpA, NEC Corp, and SubCom, LLC, which together control a significant portion of the market share. These companies compete on technological innovation, project execution capabilities, and comprehensive service offerings. The market has seen increasing consolidation, with larger players acquiring specialized firms to expand their technological capabilities and geographic reach. Competition is particularly intense in high-capacity cable systems, where technological differentiation can provide a competitive edge. The entry of content providers as direct investors has also altered the competitive dynamics, creating new partnership models and challenging traditional industry structures. Regional players are emerging in Asia-Pacific and the Middle East, adding another layer of competition, particularly in markets with growing digital infrastructure needs. The competitive landscape is characterized by long-term relationships with telecom operators, complex project bidding processes, and the need for substantial financial resources to undertake major cable projects.

Executive Summary

The submarine cable system market represents a critical component of global digital infrastructure, valued at approximately 17.20 Billion in 2026 and projected to reach 35.59 Billion by 2033, reflecting a robust CAGR of 10.95%. This growth is driven by escalating global data traffic, expanding cloud computing services, and increasing demand for high-speed connectivity across both developed and emerging markets. The market is segmented by cable type (single-core and multi-core), services (installation, maintenance, and upgrade), application (communication and energy & power), and capacity tiers ranging from less than 10 Tb/s to over 30 Tb/s. Key industry players including Alcatel Submarine Networks, Prysmian SpA, NEC Corp, and SubCom, LLC dominate the landscape, competing on technological innovation and comprehensive service offerings. The COVID-19 pandemic initially disrupted operations but ultimately underscored the essential nature of submarine cable infrastructure, accelerating investment in digital connectivity. Looking forward, the market faces challenges including high installation costs and geopolitical tensions, but opportunities abound in emerging markets, renewable energy integration, and technological advancements. The market's trajectory points toward continued expansion, driven by the fundamental need for reliable, high-capacity global connectivity.

Submarine Cable System Market Forecast

The submarine cable system market is poised for substantial growth between 2027 and 2032, with projections indicating the market will expand from its 2026 value of 17.20 Billion to reach 35.59 Billion by 2033. This represents a compound annual growth rate (CAGR) of 10.95%, reflecting strong underlying demand drivers and technological advancements. The forecast period will likely see continued expansion in high-capacity cable systems, particularly those exceeding 20 Tb/s, as data traffic volumes continue their exponential growth trajectory. Regional markets in Asia-Pacific, Africa, and Latin America are expected to demonstrate particularly strong growth rates as digital infrastructure development accelerates in these regions. The energy & power segment is also projected to gain momentum, driven by increasing renewable energy integration and cross-border power transmission projects. Service segments, particularly maintenance and upgrade services, are anticipated to grow as the installed base of submarine cables expands and the need for ongoing support increases. The forecast assumes continued technological innovation in cable design and materials, which will enable longer cable runs and higher capacities, further driving market expansion.

Submarine Cable System Market Size and Share by Segmentation

The submarine cable system market exhibits distinct patterns across its various segmentation categories. By type, both single-core and multi-core cables maintain significant market presence, with multi-core configurations gaining traction for high-capacity applications due to their superior performance characteristics. In terms of services, installation services currently represent the largest segment, driven by ongoing new cable deployments, while maintenance and upgrade services are experiencing the fastest growth as the installed base expands. The application segmentation reveals that communication services dominate the market, accounting for the majority of installations, though the energy & power segment is gaining momentum with increasing renewable energy projects and cross-border power transmission initiatives. Capacity segmentation shows a clear trend toward higher bandwidth solutions, with cables in the 20-30 Tb/s and above 30 Tb/s categories experiencing the most rapid growth, while the less than 10 Tb/s segment is gradually declining as operators upgrade to higher capacity systems. This segmentation analysis highlights the market's evolution toward higher capacity, more complex systems that serve both telecommunications and energy transmission needs.

Global Submarine Cable System Market Size and Share by Region

The global submarine cable system market demonstrates significant regional variations in terms of market size and growth dynamics. The Asia-Pacific region currently represents the largest market share, driven by the presence of major technology hubs, high population density, and aggressive digital infrastructure development in countries like China, Japan, and Singapore. North America maintains a strong market position, supported by substantial content provider investments and the need for transoceanic connectivity to Europe and Asia. Europe represents another significant regional market, characterized by extensive submarine cable networks connecting the continent to both Americas and Africa, with particular emphasis on redundancy and resilience. The Middle East and Africa region, while currently smaller in market size, is experiencing the fastest growth rate as countries invest in digital infrastructure to support economic diversification and regional connectivity. Latin America shows moderate market growth, with increasing investments in submarine cables to improve international connectivity and support the region's digital transformation. These regional variations reflect differences in economic development, digital maturity, and strategic priorities regarding connectivity infrastructure.

Regional Analysis of the Submarine Cable System Market

The submarine cable system market exhibits distinct regional characteristics that influence market dynamics and growth trajectories. In the Asia-Pacific region, market growth is propelled by rapid digitalization, expanding data center infrastructure, and strategic initiatives to enhance regional connectivity. Countries like Singapore have positioned themselves as major cable hubs, while China's Belt and Road Initiative includes significant submarine cable investments. North America's market is characterized by strong content provider involvement, with companies like Google, Facebook, and Amazon directly investing in cable systems to support their global operations. The region also benefits from stable regulatory environments and advanced technological capabilities. Europe's market is distinguished by its focus on network resilience and redundancy, with multiple cable routes connecting the continent to ensure uninterrupted connectivity. The region also leads in cross-border energy transmission projects using submarine power cables. The Middle East and Africa region is experiencing transformative growth, with countries investing in submarine cables to bridge the digital divide and support economic development. Latin America's market is evolving, with increasing attention to improving international connectivity and supporting the region's growing digital economy, though challenges remain in terms of infrastructure development and investment.

Leading Company Profiles in the Submarine Cable System Market

The submarine cable system market is dominated by several key players, each with distinct strengths and strategic approaches. Alcatel Submarine Networks, a subsidiary of Nokia, is recognized as a global leader, offering comprehensive end-to-end solutions from design to installation and maintenance. The company has been involved in numerous high-profile projects and continues to innovate in high-capacity cable technology. Prysmian SpA, an Italian company, is another major player with a strong presence in both telecommunications and power transmission submarine cables. The company leverages its extensive manufacturing capabilities and global reach to serve diverse market needs. NEC Corp from Japan brings advanced technological expertise and has been involved in several cutting-edge projects, particularly in the Asia-Pacific region. SubCom, LLC, formerly TE SubCom, is known for its specialized capabilities in complex cable installations and has a strong track record in transoceanic projects. Other notable players include Fujitsu Ltd, HMN Technologies Co., Ltd., Mitsubishi Electric Corp, Nexans SA, Sumitomo Electric Industries Ltd, and Vodafone Group Plc, each contributing to the market with their unique technological capabilities, regional strengths, and service offerings. These companies compete on technological innovation, project execution capabilities, and comprehensive service portfolios to maintain their market positions.

Porter's Five Forces Analysis of the Submarine Cable System Market

Applying Porter's Five Forces framework to the submarine cable system market reveals a complex competitive environment. The threat of new entrants is relatively low due to the substantial capital requirements, specialized technical expertise needed, and strong relationships that incumbent players have established with customers. The bargaining power of buyers, primarily telecom operators and content providers, is moderate to high, as they often have multiple options for cable providers and can influence pricing and technical specifications. Supplier power is relatively low for standard components but can be significant for specialized equipment and materials, where few alternatives exist. The threat of substitutes is minimal, as submarine cables remain the most efficient and cost-effective means of transmitting large volumes of data across oceans, with alternatives like satellite communications unable to match their capacity and latency characteristics. Competitive rivalry within the industry is intense, with a few major players competing on technological innovation, project execution capabilities, and comprehensive service offerings. The market also experiences pressure from content providers who are increasingly investing directly in submarine cable infrastructure, potentially bypassing traditional telecom operators.

SWOT Analysis of the Submarine Cable System Market

A SWOT analysis of the submarine cable system market reveals several key factors influencing its trajectory. Strengths of the market include the critical nature of submarine cables for global connectivity, continuous technological advancements enabling higher capacities and longer distances, and the presence of established players with proven track records in complex installations. The market also benefits from strong demand drivers, including exponential data traffic growth and increasing cloud computing adoption. However, weaknesses exist, such as the high costs associated with cable installation and maintenance, vulnerability to physical damage from various sources, and the complex regulatory environments that can delay projects. Opportunities abound in emerging markets where digital infrastructure is still developing, the growing renewable energy sector requiring power transmission cables, and potential advancements in materials science that could reduce costs or improve performance. Threats to the market include geopolitical tensions that can affect cable routes, environmental concerns regarding seabed disruption, and the potential for alternative technologies to emerge, though currently none can match submarine cables' capacity and efficiency. Additionally, the market faces risks from natural disasters and climate change impacts on ocean conditions, which could affect cable reliability.

Submarine Cable System Market Value Chain Analysis

The submarine cable system market value chain encompasses a complex network of activities and participants, each contributing to the delivery of end-to-end solutions. The chain begins with raw material suppliers providing specialized materials such as high-strength fibers, copper, and optical fibers essential for cable construction. These materials flow to manufacturers who produce the actual submarine cable systems, incorporating advanced technologies for signal transmission and power delivery. System integrators then design complete solutions, combining cables with necessary equipment like repeaters and branching units. Installation contractors execute the complex process of deploying cables across ocean floors, requiring specialized ships and equipment. Service providers offer ongoing maintenance, repair, and upgrade services throughout the cable's operational life. At the demand end, telecom operators and content providers drive requirements for new cable systems based on their connectivity needs. Supporting these core activities are research institutions advancing cable technology, regulatory bodies overseeing installations, and consulting firms providing expertise on route planning and environmental assessments. This value chain is characterized by long lead times, high capital requirements, and the need for specialized expertise at each stage, creating significant barriers to entry and reinforcing the market's concentrated structure.

Key Investment Insights in the Submarine Cable System Market

The submarine cable system market presents compelling investment opportunities driven by several key factors. The market's projected growth, with a CAGR of 10.95% leading to a value of 35.59 Billion by 2033, indicates strong potential returns for investors. Strategic investment areas include high-capacity cable systems exceeding 20 Tb/s, which are increasingly in demand to support growing data traffic. Emerging markets in Africa, Southeast Asia, and Latin America offer attractive opportunities as these regions accelerate their digital infrastructure development. The energy & power segment represents a growing investment frontier, particularly for projects involving renewable energy integration and cross-border power transmission. Investors should also consider the service segment, including maintenance and upgrade services, which provides recurring revenue streams as the installed base of submarine cables expands. Technological innovation remains a key investment theme, with advancements in materials science, signal processing, and monitoring systems offering potential competitive advantages. However, investors must also consider risks including geopolitical tensions affecting cable routes, environmental regulations, and the substantial capital requirements for major projects. Strategic partnerships between content providers and cable operators represent another investment trend, potentially offering more stable returns through diversified ownership structures.

Submarine Cable System Market Conclusion

The submarine cable system market stands at a critical juncture, characterized by robust growth projections, technological advancements, and evolving market dynamics. With the market valued at 17.20 Billion in 2026 and expected to reach 35.59 Billion by 2033 at a CAGR of 10.95%, the industry demonstrates strong fundamentals driven by the insatiable global demand for data connectivity. The market's segmentation reveals a trend toward higher capacity systems, comprehensive service offerings, and applications spanning both telecommunications and energy transmission. While challenges exist, including high installation costs, geopolitical risks, and environmental concerns, the market's essential role in global connectivity provides a solid foundation for continued expansion. The COVID-19 pandemic has further underscored the critical nature of submarine cable infrastructure, likely accelerating investment and policy support. As the industry moves forward, success will depend on technological innovation, strategic partnerships, and the ability to navigate complex regulatory and environmental landscapes. The submarine cable system market remains a vital enabler of the digital economy, with its growth trajectory closely aligned with the broader trends of digitalization, cloud computing, and renewable energy integration.

Research Methodology

The research methodology employed for this submarine cable system market analysis combines multiple approaches to ensure comprehensive and accurate insights. Primary research formed a significant component, involving interviews with industry experts, manufacturers, service providers, and end-users to gather firsthand information on market trends, challenges, and opportunities. Secondary research complemented these efforts, drawing from a wide range of sources including industry reports, company financial statements, regulatory filings, trade publications, and academic journals. Market size and forecast calculations were derived using both top-down and bottom-up approaches, cross-validated with data triangulation to ensure accuracy. The analysis considered historical market data, current trends, and future projections, incorporating macroeconomic factors and industry-specific variables. Segmentation analysis was conducted based on type, service, application, and capacity, with regional breakdowns providing geographic context. The research also incorporated competitive analysis, examining market shares, strategies, and recent developments of key players. Throughout the process, data quality and consistency were prioritized, with findings reviewed by industry experts to validate conclusions and ensure the reliability of the market assessment.

Research Scope

The research scope for this submarine cable system market analysis encompasses a comprehensive examination of the global market from 2025 to 2032, with historical data and current market sizing provided for context. The study covers all major market segments including cable types (single-core and multi-core), services (installation, maintenance, and upgrade), applications (communication and energy & power), and capacity tiers (less than 10 Tb/s, 10-20 Tb/s, 20-30 Tb/s, and more than 30 Tb/s). Geographic coverage includes major regions such as North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America, with analysis of regional market dynamics, growth drivers, and challenges. The research focuses on key industry players, their market strategies, and competitive positioning, while also examining emerging trends and technological developments. The scope includes an assessment of market drivers, restraints, opportunities, and challenges, along with detailed analyses using frameworks such as Porter's Five Forces and SWOT. Investment insights and value chain analysis are provided to offer strategic perspectives. The research acknowledges limitations in data availability for certain niche segments and emerging markets, and notes that market dynamics may evolve with technological advancements and regulatory changes not fully captured in the forecast period.

Key Companies and Recent Developments in the Submarine Cable System Market

The submarine cable system market features several key companies that have recently announced significant developments, partnerships, and strategic initiatives. Alcatel Submarine Networks has been involved in multiple high-profile projects, including the deployment of advanced high-capacity cables with innovative repeater technologies. The company has also announced partnerships with content providers to develop next-generation cable systems. Prysmian SpA has expanded its manufacturing capabilities and announced several new cable installations, particularly focusing on renewable energy interconnections and regional connectivity projects. NEC Corp has unveiled advancements in optical transmission technology, enabling higher capacity cables over longer distances, and has secured contracts for major transoceanic projects. SubCom, LLC has announced the successful completion of several complex installations and introduced new monitoring systems for enhanced cable management. Fujitsu Ltd has partnered with regional operators to develop cable systems tailored to specific market needs, while Mitsubishi Electric Corp has announced innovations in cable materials that improve durability and performance. Nexans SA has expanded its presence in the energy & power segment with new submarine power cable projects. Sumitomo Electric Industries Ltd has introduced advanced branching unit technologies, and Vodafone Group Plc has announced investments in new cable systems to support its expanding network infrastructure. These developments reflect the industry's focus on technological innovation, strategic partnerships, and expanding into new market segments to maintain competitive advantages.