Fourth Party Logistics Market Overview - Definition, scope, and significance

The Fourth Party Logistics (4PL) market represents a specialized segment of supply chain management where a single partner manages and controls the entire supply chain on behalf of the client. Unlike traditional third-party logistics providers, 4PL providers act as integrators, coordinating multiple logistics providers, technology, and resources to deliver comprehensive supply chain solutions. The market encompasses services such as strategic planning, network design, procurement, and end-to-end supply chain management. With a current market size of $82.43 billion in 2026 and projected growth to $134.44 billion by 2033, the 4PL market plays a crucial role in modern business operations, particularly for companies seeking to optimize their supply chains, reduce costs, and improve efficiency through external expertise.

Fourth Party Logistics Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The 4PL market is driven by increasing globalization, the need for supply chain optimization, and the growing complexity of logistics operations. Companies are increasingly outsourcing their supply chain management to focus on core competencies, while the rise of e-commerce and omnichannel retail has created demand for sophisticated logistics solutions. However, the market faces restraints such as high implementation costs, resistance to change from traditional logistics models, and the complexity of integrating multiple systems and partners. Challenges include maintaining service quality across diverse operations, ensuring data security, and managing cultural differences in global operations. Opportunities exist in emerging markets, the adoption of advanced technologies like AI and IoT, and the development of sustainable logistics solutions.

Fourth Party Logistics Market Growth Trends - Current and emerging trends shaping the market

The 4PL market is experiencing significant growth trends driven by digital transformation and evolving customer expectations. Key trends include the increasing adoption of cloud-based supply chain management systems, the integration of artificial intelligence and machine learning for predictive analytics, and the growing emphasis on sustainability in logistics operations. The market is also seeing a shift towards more specialized 4PL services, with providers focusing on specific industries or supply chain functions. The COVID-19 pandemic has accelerated trends such as nearshoring and the development of more resilient supply chains. Additionally, the rise of blockchain technology is creating new opportunities for transparency and traceability in 4PL operations.

COVID-19 Impact on the Fourth Party Logistics Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has had a profound impact on the 4PL market, initially causing significant disruptions to global supply chains. Lockdowns, border closures, and labor shortages led to delays and increased costs for many companies. However, the pandemic also highlighted the value of 4PL providers in managing complex supply chain challenges. As a result, many companies have increased their reliance on 4PL services to improve supply chain resilience and flexibility. The recovery trajectory shows a shift towards more localized and diversified supply chains, with increased investment in digital technologies and risk management strategies. The pandemic has also accelerated the adoption of e-commerce and last-mile delivery solutions, creating new opportunities for 4PL providers.

Fourth Party Logistics Market Competitive Landscape - Major competitors and market consolidation

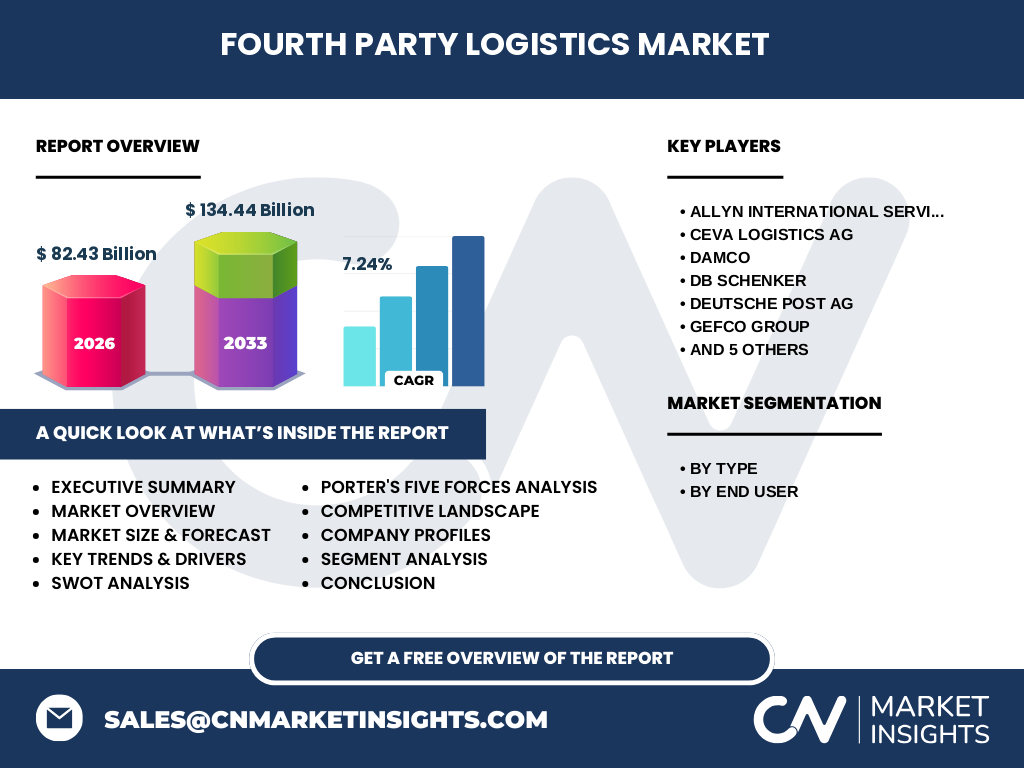

The 4PL market features a competitive landscape with several major players and a mix of large multinational corporations and specialized providers. Key competitors include Allyn International Services, CEVA Logistics AG, DAMCO, DB Schenker, Deutsche Post AG, GEFCO Group, GEODIS, Logistics Plus Inc., United Parcel Service, and XPO Logistics. The market is characterized by ongoing consolidation, with larger companies acquiring specialized providers to expand their service offerings and geographic reach. Competition is intense in terms of service quality, technological capabilities, and pricing. Many providers are differentiating themselves through industry-specific expertise or innovative solutions. The market also sees competition from traditional 3PL providers expanding into 4PL services and technology companies entering the logistics space.

Executive Summary - High-level overview and key findings about Fourth Party Logistics Market

The Fourth Party Logistics market is experiencing robust growth, with the market size expected to increase from $82.43 billion in 2026 to $134.44 billion by 2033, representing a CAGR of 7.24%. This growth is driven by increasing demand for integrated supply chain solutions, technological advancements, and the need for greater supply chain resilience. The market is characterized by diverse service models, including Synergy Plus Operating Model, Solution Integrator Model, and Industry Innovator Model, catering to various end-user industries such as aerospace, automotive, consumer electronics, and healthcare. Key findings indicate a strong trend towards digitalization and sustainability in 4PL operations, with significant opportunities in emerging markets and specialized industry segments. The competitive landscape remains dynamic, with major players focusing on technological innovation and strategic partnerships to maintain their market position.

Fourth Party Logistics Market Forecast - Projections for 2025-2032 period

The 4PL market is projected to experience steady growth from 2025 to 2032, with the market size expected to reach $134.44 billion by 2033, growing at a CAGR of 7.24%. This forecast is based on several factors, including the continued expansion of global trade, increasing adoption of advanced technologies in supply chain management, and the growing complexity of logistics operations. The forecast period is likely to see increased investment in digital infrastructure, with a particular focus on AI, IoT, and blockchain technologies. The market is also expected to benefit from the ongoing trend of supply chain localization and the increasing importance of sustainability in logistics operations. However, potential challenges such as economic uncertainties and geopolitical tensions may impact the growth trajectory.

Fourth Party Logistics Market Size and Share by Segmentation - Breakdown by {segmentData}

The 4PL market can be segmented by type and end-user industry. By type, the market includes Synergy Plus Operating Model, Solution Integrator Model, and Industry Innovator Model. The Solution Integrator Model currently holds the largest market share, driven by its comprehensive approach to supply chain management. By end-user, the market serves industries such as Aerospace & Defense, Automotive, Consumer Electronics, Food & Beverages, Industrial, Healthcare, and Retail. The Automotive and Consumer Electronics sectors currently dominate the market, accounting for the largest share of 4PL services. However, the Healthcare and Food & Beverages sectors are expected to see the highest growth rates due to increasing demand for specialized logistics solutions in these industries.

Global Fourth Party Logistics Market Size and Share by Region - Geographic distribution

While specific regional data is not provided, the global 4PL market is expected to show varying growth rates across different regions. North America and Europe currently represent the largest markets for 4PL services, driven by the presence of major multinational corporations and advanced logistics infrastructure. The Asia-Pacific region is expected to see the highest growth rate, fueled by rapid industrialization, increasing e-commerce adoption, and the expansion of manufacturing activities in countries like China and India. Latin America and the Middle East & Africa regions are also expected to contribute to market growth, albeit at a slower pace, due to improving economic conditions and increasing adoption of modern supply chain practices.

Regional Analysis of the Fourth Party Logistics Market - Detailed regional market performance

The 4PL market exhibits diverse characteristics across different regions. In North America, the market is mature and highly competitive, with a strong focus on technological innovation and sustainability. Europe shows similar maturity but with a greater emphasis on regulatory compliance and green logistics. The Asia-Pacific region is experiencing rapid growth, driven by expanding manufacturing sectors and increasing adoption of e-commerce. China and India are key growth markets in this region, with local providers emerging alongside global players. Latin America is seeing steady growth, particularly in countries like Brazil and Mexico, driven by improving economic conditions and increasing foreign investment. The Middle East & Africa region, while currently smaller, shows potential for growth due to increasing infrastructure development and economic diversification efforts in countries like the UAE and South Africa.

Leading Company Profiles in the Fourth Party Logistics Market - Industry players and strategies

The 4PL market is dominated by several key players, each with distinct strategies and strengths. Allyn International Services focuses on providing customized logistics solutions with a strong emphasis on technology integration. CEVA Logistics AG leverages its global network and industry expertise to offer comprehensive supply chain solutions. DAMCO, a subsidiary of Maersk, combines shipping expertise with advanced logistics capabilities. DB Schenker emphasizes its strong European presence and diverse service portfolio. Deutsche Post AG (DHL) utilizes its extensive global network and brand recognition. GEFCO Group specializes in automotive logistics, while GEODIS offers a wide range of supply chain solutions across multiple industries. Logistics Plus Inc. focuses on providing innovative and cost-effective solutions. United Parcel Service (UPS) leverages its strong brand and technological capabilities. XPO Logistics is known for its asset-light model and focus on technology-driven solutions.

Porter's Five Forces Analysis of the Fourth Party Logistics Market - Competitive forces assessment

The 4PL market is characterized by intense competition, with high rivalry among existing players driving innovation and service quality. The threat of new entrants is moderate, as the market requires significant capital investment and established relationships to compete effectively. The bargaining power of buyers is increasing as companies become more knowledgeable about supply chain management and seek customized solutions. The bargaining power of suppliers is relatively low, as 4PL providers often have multiple options for logistics partners and technology providers. The threat of substitutes is moderate, with companies having the option to insource their logistics operations or work with multiple specialized providers instead of a single 4PL partner. Overall, the market dynamics favor established players with strong technological capabilities and comprehensive service offerings.

SWOT Analysis of the Fourth Party Logistics Market - Strengths, weaknesses, opportunities, threats

The 4PL market's strengths include its ability to provide comprehensive supply chain solutions, advanced technological capabilities, and expertise in managing complex logistics operations. However, weaknesses such as high implementation costs and potential resistance to change from traditional logistics models can hinder market growth. Opportunities in the market include the increasing adoption of digital technologies, the growing demand for sustainable logistics solutions, and the potential for expansion in emerging markets. Threats to the market include economic uncertainties, geopolitical tensions affecting global trade, and the potential for technological disruptions that could change the logistics landscape. The market's ability to adapt to changing customer needs and technological advancements will be crucial in addressing these threats and capitalizing on opportunities.

Fourth Party Logistics Market Value Chain Analysis - Industry structure and value flow

The 4PL value chain consists of several key components that work together to deliver comprehensive supply chain solutions. At the core is the 4PL provider, which acts as the central coordinator and integrator of various logistics services. This includes strategic planning and network design, procurement of logistics services, technology integration, and performance management. The value chain also involves relationships with various stakeholders, including suppliers, carriers, warehouse operators, and technology providers. The flow of value in the 4PL market is characterized by the integration of physical logistics services with information technology, creating a seamless supply chain solution for clients. This integration allows for improved visibility, efficiency, and cost-effectiveness throughout the supply chain.

Key Investment Insights in the Fourth Party Logistics Market - Strategic investment recommendations

Investment opportunities in the 4PL market are driven by several key trends and developments. The increasing adoption of digital technologies, particularly AI, IoT, and blockchain, presents significant investment potential. Companies that can effectively integrate these technologies into their service offerings are likely to see strong growth. Another area of investment opportunity is in sustainable logistics solutions, as companies face increasing pressure to reduce their environmental impact. Emerging markets, particularly in Asia-Pacific and Latin America, offer potential for expansion and market share growth. Additionally, investments in specialized industry solutions, such as healthcare logistics or e-commerce fulfillment, could yield high returns given the growing complexity of these supply chains. Strategic partnerships and acquisitions to expand service offerings and geographic reach are also recommended investment strategies.

Fourth Party Logistics Market Conclusion - Summary and key takeaways

The Fourth Party Logistics market is poised for significant growth, with the market size expected to increase from $82.43 billion in 2026 to $134.44 billion by 2033, representing a CAGR of 7.24%. This growth is driven by increasing demand for integrated supply chain solutions, technological advancements, and the need for greater supply chain resilience. The market is characterized by diverse service models and end-user industries, with strong competition among key players. While challenges exist, such as high implementation costs and potential resistance to change, the market offers numerous opportunities for growth and innovation. The future of the 4PL market will likely be shaped by continued digital transformation, increasing focus on sustainability, and the ability to adapt to changing global trade dynamics.

Research Methodology - How this research was conducted

This market research report was compiled using a comprehensive methodology that combines both primary and secondary research. Primary research involved interviews with industry experts, 4PL providers, and end-users to gather firsthand insights into market trends, challenges, and opportunities. Secondary research included analysis of industry reports, company financial statements, and market data from reputable sources. The research team employed various analytical tools and models to interpret the data and project market trends. The report's findings are based on a combination of quantitative data analysis and qualitative expert insights, ensuring a balanced and comprehensive view of the Fourth Party Logistics market.

Research Scope - Coverage and limitations

This research report covers the global Fourth Party Logistics market, focusing on key market segments, regional trends, and major industry players. The scope includes an analysis of market drivers, restraints, and opportunities, as well as a detailed examination of market size, share, and growth projections. The report also covers competitive landscape analysis, including Porter's Five Forces and SWOT analysis. However, it's important to note that the research has limitations, including the availability of specific regional data and the potential for rapid technological changes to impact market dynamics. The report provides a comprehensive overview based on available data and expert analysis, but readers should consider these limitations when interpreting the findings.

Key Companies and Recent Developments in the Fourth Party Logistics Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The 4PL market features several key players, each with recent developments shaping the industry landscape. Allyn International Services has focused on expanding its technology offerings, launching new supply chain visibility tools. CEVA Logistics AG announced a strategic partnership with a major e-commerce platform to enhance last-mile delivery capabilities. DAMCO has invested in sustainable logistics solutions, introducing eco-friendly packaging options for clients. DB Schenker unveiled a new AI-powered predictive analytics platform for supply chain optimization. Deutsche Post AG (DHL) launched a global initiative to achieve carbon-neutral logistics operations by 2050. GEFCO Group announced the expansion of its automotive logistics network in Asia. GEODIS introduced a new industry-specific solution for healthcare logistics. Logistics Plus Inc. partnered with a leading IoT provider to enhance real-time tracking capabilities. United Parcel Service (UPS) launched a new blockchain-based platform for supply chain transparency. XPO Logistics announced the acquisition of a last-mile delivery specialist to strengthen its e-commerce capabilities.