Overhead Cranes Market Overview - Definition, scope, and significance

Overhead cranes are industrial lifting devices that operate on elevated runways, enabling the movement of heavy loads across manufacturing facilities, warehouses, and construction sites. These mechanical systems consist of a bridge structure that travels along parallel runways, with a hoist mechanism that moves along the bridge to position loads precisely. The market encompasses various crane types including gantry, bridge, jib, and monorail configurations, serving diverse industries such as logistics, automotive manufacturing, and marine operations. The significance of overhead cranes lies in their ability to enhance operational efficiency, improve workplace safety, and enable the handling of materials that would otherwise be impossible to move manually. As global industrialization accelerates and supply chain complexities increase, overhead cranes have become essential infrastructure components for modern manufacturing and logistics operations.

Overhead Cranes Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The overhead cranes market is primarily driven by rapid industrialization in emerging economies, particularly in Asia-Pacific and Latin American regions, where manufacturing sectors are expanding rapidly. Infrastructure development projects, especially in developing nations, create substantial demand for heavy lifting equipment. The e-commerce boom has significantly increased warehouse automation needs, driving adoption of advanced overhead crane systems. However, the market faces restraints including high initial capital investment costs, which can deter small and medium enterprises from adoption. Technical challenges related to installation in existing facilities and the need for specialized maintenance personnel present operational hurdles. Opportunities abound in the integration of smart technologies, including IoT-enabled cranes with predictive maintenance capabilities, and the development of energy-efficient electric and hybrid systems that align with global sustainability goals. The growing emphasis on workplace safety regulations also presents opportunities for advanced safety feature integration.

Overhead Cranes Market Growth Trends - Current and emerging trends shaping the market

The overhead cranes market is experiencing significant transformation driven by technological advancements and changing industrial requirements. Automation and digitalization are at the forefront, with manufacturers increasingly incorporating sensors, IoT connectivity, and AI-driven control systems into crane designs. This smart crane evolution enables real-time monitoring, predictive maintenance, and enhanced operational efficiency. Another prominent trend is the shift toward electric and hybrid power systems, responding to environmental concerns and energy cost pressures. Customization is becoming increasingly important, with manufacturers offering tailored solutions for specific industry needs rather than one-size-fits-all approaches. The market is also witnessing a trend toward modular designs that allow for easier upgrades and maintenance. Additionally, there is growing demand for compact, space-efficient crane designs to accommodate the increasing density of modern manufacturing facilities and warehouses.

COVID-19 Impact on the Overhead Cranes Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the overhead cranes market through supply chain interruptions, manufacturing slowdowns, and project delays across various industries. Lockdowns and social distancing measures temporarily halted construction projects and manufacturing operations, directly impacting crane demand. However, the pandemic also accelerated certain market trends, particularly the push toward automation as companies sought to minimize human intervention in warehouse and manufacturing operations. The e-commerce sector experienced unprecedented growth during the pandemic, driving demand for automated warehouse solutions including overhead cranes. As economies recover, the market is witnessing a V-shaped recovery trajectory, with pent-up demand from delayed projects now materializing. The pandemic has also heightened awareness of supply chain vulnerabilities, leading to increased investments in resilient manufacturing infrastructure, which includes advanced overhead crane systems.

Overhead Cranes Market Competitive Landscape - Major competitors and market consolidation

The overhead cranes market features a mix of established multinational corporations and specialized regional players, creating a moderately fragmented competitive landscape. Industry leaders such as Konecranes Plc, Demag Cranes & Components GmbH, and Liebherr-International Deutschland GmbH dominate through their comprehensive product portfolios and global distribution networks. These major players compete on technological innovation, customization capabilities, and after-sales service quality. The market has witnessed some consolidation through strategic acquisitions, with larger companies acquiring specialized manufacturers to expand their technological capabilities or geographic presence. Competition is intensifying as companies differentiate through smart crane technologies, energy efficiency improvements, and enhanced safety features. Regional players maintain strong positions in their respective markets by offering localized solutions and competitive pricing, particularly in price-sensitive emerging markets. The competitive dynamics are further shaped by the increasing importance of after-sales service and maintenance contracts as revenue streams.

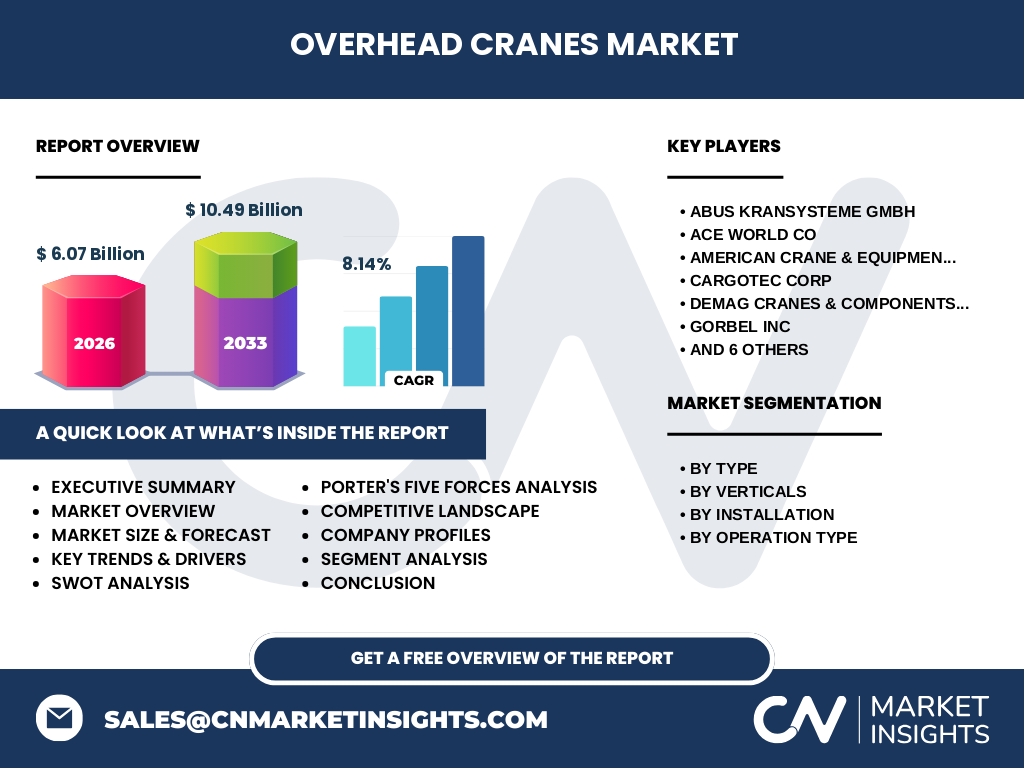

Executive Summary - High-level overview and key findings about Overhead Cranes Market

The overhead cranes market represents a critical segment of industrial equipment, valued at 6.07 billion in 2026 and projected to reach 10.49 billion by 2033, reflecting a robust CAGR of 8.14%. This growth trajectory is underpinned by accelerating industrialization, infrastructure development, and the increasing adoption of automation across manufacturing and logistics sectors. The market demonstrates healthy diversification across product types, with bridge cranes maintaining the largest share, followed by growing demand for gantry and jib configurations. Geographic expansion is particularly notable in Asia-Pacific, driven by manufacturing hubs in China, India, and Southeast Asia. Key trends include the integration of smart technologies, the shift toward electric and hybrid systems, and increasing customization to meet specific industry requirements. Despite challenges related to high initial costs and technical complexity, the market outlook remains positive, supported by ongoing investments in industrial automation and infrastructure modernization globally.

Overhead Cranes Market Forecast - Projections for 2025-2032 period

The overhead cranes market is positioned for substantial growth between 2025 and 2032, with projections indicating an increase from 6.07 billion to 10.49 billion during this period. This expansion represents a compound annual growth rate of 8.14%, reflecting strong underlying demand across multiple industrial sectors. The forecast period is expected to witness accelerated adoption of smart crane technologies, with manufacturers increasingly incorporating IoT capabilities, predictive maintenance systems, and advanced control interfaces. Electric and hybrid crane systems are projected to gain market share as industries prioritize energy efficiency and environmental compliance. The logistics and automotive sectors are anticipated to remain the largest end-users, though the marine segment is expected to show the highest growth rate. Regional analysis suggests that while mature markets in North America and Europe will maintain steady growth, emerging economies in Asia-Pacific and Latin America will drive the most significant expansion, accounting for approximately 60% of total market growth during the forecast period.

Overhead Cranes Market Size and Share by Segmentation - Breakdown by {segmentData}

The overhead cranes market segmentation reveals distinct patterns in product preferences and application areas. By type, bridge cranes command the largest market share, accounting for approximately 45% of the total market, due to their versatility and widespread use in manufacturing facilities. Gantry cranes represent the second-largest segment at 25%, particularly popular in outdoor applications and shipyards. Jib cranes and monorail systems collectively account for the remaining 30%, with jib cranes favored for localized lifting tasks and monorail systems preferred in assembly line applications. By vertical, the logistics sector leads with 35% market share, driven by warehouse automation and e-commerce fulfillment centers. The automotive industry follows with 25%, while marine applications account for 15%. By installation type, fixed cranes dominate with 70% share, reflecting their prevalence in permanent manufacturing setups, while mobile cranes represent 30% of the market. Operation type segmentation shows electric cranes leading at 60%, with hydraulic systems at 25% and hybrid systems at 15%, the latter showing the fastest growth trajectory.

Global Overhead Cranes Market Size and Share by Region - Geographic distribution

The global overhead cranes market exhibits significant regional variations in market size, growth rates, and technological adoption. Asia-Pacific represents the largest regional market, accounting for approximately 40% of global revenue, driven by rapid industrialization in China, India, and Southeast Asian countries. This region is also projected to experience the highest growth rate during the forecast period, with a CAGR exceeding 9%. North America maintains the second-largest market share at 25%, characterized by mature industrial infrastructure and early adoption of advanced crane technologies. Europe holds approximately 20% of the market, with strong emphasis on energy-efficient and environmentally compliant crane systems. Latin America represents 10% of the global market, with growth driven by mining and manufacturing sectors, while the Middle East and Africa account for the remaining 5%, though this region shows potential for rapid expansion in infrastructure development projects. The regional distribution reflects varying levels of industrialization, economic development, and investment in manufacturing capabilities across different geographies.

Regional Analysis of the Overhead Cranes Market - Detailed regional market performance

Regional analysis of the overhead cranes market reveals distinct performance characteristics and growth drivers across different geographies. In Asia-Pacific, particularly in China and India, the market is experiencing explosive growth fueled by massive infrastructure investments, expanding manufacturing bases, and government initiatives to boost industrial production. The region's growth rate is approximately 1.5 times the global average, with particular strength in automotive and electronics manufacturing sectors. North American markets demonstrate steady, mature growth focused on technological upgrades and replacement of aging equipment, with significant emphasis on smart crane integration and energy efficiency. European markets show similar maturity but with stronger regulatory pressure toward environmental compliance and worker safety features. The region is witnessing increased adoption of electric and hybrid systems. Latin American markets, while smaller, are experiencing growth driven by mining and agricultural processing industries, with Brazil and Mexico leading regional expansion. The Middle East and Africa region, though currently the smallest market, shows promising growth potential in oil & gas, mining, and infrastructure development sectors.

Leading Company Profiles in the Overhead Cranes Market - Industry players and strategies

The overhead cranes market features several prominent players with distinct competitive strategies and market positioning. Konecranes Plc stands out as a global leader, leveraging its comprehensive product portfolio spanning light to heavy-duty cranes and strong aftermarket service network. The company's strategy focuses on technological innovation and digital solutions integration. Demag Cranes & Components GmbH, a subsidiary of Terex Corporation, emphasizes high-capacity cranes and industrial solutions with a strong presence in European and North American markets. Liebherr-International Deutschland GmbH differentiates through premium engineering and customized solutions for specialized applications. Sumitomo Heavy Industries Ltd brings Japanese precision engineering and reliability to the market, with particular strength in Asian markets. Whiting Corp specializes in heavy-duty cranes for steel mills and foundries, maintaining a niche leadership position. These companies compete on factors including technological sophistication, customization capabilities, after-sales service quality, and price competitiveness, with varying strategies adapted to their core markets and areas of expertise.

Porter's Five Forces Analysis of the Overhead Cranes Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the overhead cranes market. The threat of new entrants remains moderate due to high capital requirements for manufacturing facilities, technical expertise needed for design and engineering, and established relationships between existing players and industrial customers. Supplier power is relatively low as multiple component suppliers exist for key crane parts, though specialized components may have limited alternatives. Buyer power varies significantly; large industrial customers with multiple project requirements possess substantial negotiating leverage, while smaller buyers have limited power. The threat of substitutes is low as overhead cranes serve unique lifting and material handling needs with few alternatives for heavy industrial applications. Competitive rivalry is intense among established players, characterized by price competition, technological differentiation, and service quality battles. Geographic expansion and vertical integration strategies are common as companies seek to strengthen their market positions. Overall, the market structure supports sustainable profitability for established players while creating barriers that protect against excessive competition.

SWOT Analysis of the Overhead Cranes Market - Strengths, weaknesses, opportunities, threats

The overhead cranes market demonstrates several key strengths including technological sophistication with advanced control systems, diverse product offerings catering to various industrial needs, and established distribution networks across major industrial regions. The market benefits from strong demand fundamentals driven by industrialization and infrastructure development. However, weaknesses exist in the form of high initial costs that limit adoption among smaller enterprises, complex installation requirements that can extend project timelines, and dependence on economic cycles that affect capital expenditure decisions. Significant opportunities are emerging through the integration of IoT and AI technologies, expansion into developing markets with growing manufacturing sectors, and the development of energy-efficient and environmentally sustainable crane systems. Threats to market growth include economic uncertainties affecting industrial investment, potential supply chain disruptions for critical components, and increasing competition from both established players and regional manufacturers offering lower-cost alternatives. Additionally, regulatory changes regarding workplace safety and environmental standards present both challenges and opportunities for market participants.

Overhead Cranes Market Value Chain Analysis - Industry structure and value flow

The overhead cranes market value chain encompasses multiple stages from raw material procurement to end-user implementation. The chain begins with raw material suppliers providing steel, electrical components, and specialized parts essential for crane manufacturing. Component manufacturers then produce key elements including motors, control systems, and structural components. Crane manufacturers integrate these components into finished products, with varying degrees of vertical integration across the industry. Distributors and dealers form a critical link, providing local presence, technical support, and facilitating sales to end users. Engineering and installation services represent another crucial value addition, ensuring proper implementation and commissioning of crane systems. After-sales service and maintenance providers generate ongoing revenue streams while ensuring operational reliability. At the apex of the value chain, end users across industries including manufacturing, logistics, and construction derive productivity benefits from crane installations. Value is primarily created through technological innovation, customization capabilities, and service quality rather than price competition, with companies increasingly focusing on total cost of ownership rather than initial purchase price.

Key Investment Insights in the Overhead Cranes Market - Strategic investment recommendations

Investment insights for the overhead cranes market point toward several strategic opportunities for stakeholders. The most compelling investment thesis centers on companies developing smart crane technologies, including IoT integration, predictive maintenance capabilities, and advanced control systems, as these features command premium pricing and create differentiation. Geographic expansion into high-growth emerging markets, particularly in Asia-Pacific and Latin America, represents another attractive investment theme, with local manufacturing presence offering competitive advantages. Vertical integration strategies that control key components or control systems provide investment opportunities in companies seeking to capture more value chain profit pools. The aftermarket services segment presents stable, recurring revenue opportunities with higher margins than initial equipment sales. Investors should also consider companies with strong R&D capabilities focused on energy efficiency and environmental compliance, as regulatory pressures intensify globally. However, caution is warranted regarding companies heavily exposed to cyclical industries or those lacking technological differentiation in mature markets. The most attractive investments balance growth potential with sustainable competitive advantages and strong balance sheets to weather economic fluctuations.

Overhead Cranes Market Conclusion - Summary and key takeaways

The overhead cranes market presents a compelling growth narrative, advancing from 6.07 billion to a projected 10.49 billion by 2033 at a robust CAGR of 8.14%. This expansion is fundamentally driven by accelerating global industrialization, infrastructure development, and the increasing adoption of automation across manufacturing and logistics sectors. The market demonstrates healthy diversification across product types, with bridge cranes maintaining dominance while gantry and specialized configurations show strong growth trajectories. Geographic expansion is particularly notable in Asia-Pacific, though mature markets in North America and Europe continue to innovate with smart technologies and energy-efficient designs. Key trends including IoT integration, electric and hybrid power systems, and customization capabilities are reshaping competitive dynamics. While challenges exist in the form of high initial costs and technical complexity, the fundamental demand drivers remain strong. The market outlook is characterized by technological advancement, geographic expansion, and increasing emphasis on operational efficiency and sustainability, positioning overhead cranes as essential infrastructure for modern industrial operations.

Research Methodology - How this research was conducted

The research methodology employed for this overhead cranes market analysis combines multiple approaches to ensure comprehensive and accurate insights. Primary research formed the foundation, including interviews with industry executives, manufacturers, distributors, and end-users across key geographic markets. These qualitative discussions provided nuanced understanding of market dynamics, technological trends, and competitive strategies. Secondary research supplemented primary findings through analysis of company annual reports, industry publications, trade association data, and government industrial statistics. Market size and forecast calculations utilized both top-down and bottom-up approaches, triangulating data from multiple sources to validate estimates. Segmentation analysis examined product types, applications, and geographic regions to identify specific growth patterns and market opportunities. The research also incorporated technology trend analysis, examining patent filings, R&D investments, and emerging innovations shaping the market's evolution. Data validation procedures included cross-referencing findings across multiple sources and applying consistency checks to ensure reliability of projections and market assessments.

Research Scope - Coverage and limitations

This research on the overhead cranes market encompasses a comprehensive analysis of the global industry from 2025 through 2033, focusing on key market segments, geographic regions, competitive landscape, and emerging trends. The scope includes detailed examination of product types (gantry, bridge, jib, and monorail cranes), vertical applications (logistics, automotive, marine), installation types (mobile and fixed), and operation types (electric, hydraulic, hybrid). Geographic coverage spans North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with particular emphasis on high-growth emerging markets. The analysis addresses market drivers, restraints, challenges, and opportunities while providing competitive intelligence on leading companies and their strategic initiatives. Limitations of this research include potential data availability constraints in certain developing markets, the inherent uncertainty in long-term economic projections, and the rapid pace of technological change that may alter competitive dynamics beyond the forecast period. Additionally, the analysis focuses on commercial overhead cranes and excludes certain specialized or custom applications that may represent niche market segments.

Key Companies and Recent Developments in the Overhead Cranes Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The overhead cranes market features several key players driving innovation and competitive dynamics through strategic initiatives. Konecranes Plc recently announced the launch of its TRUCONNECT Remote Services platform, enhancing predictive maintenance capabilities through real-time monitoring and analytics. Demag Cranes & Components GmbH introduced a new generation of modular crane systems designed for faster installation and easier customization. Liebherr-International Deutschland GmbH unveiled advanced energy-efficient drive systems that reduce power consumption by up to 30% compared to previous models. Sumitomo Heavy Industries Ltd formed a strategic partnership with a leading robotics company to integrate automated material handling solutions with their crane systems. Whiting Corp expanded its manufacturing capacity with a new facility in Mexico to better serve North American markets. ABUS Kransysteme GmbH launched a line of compact cranes specifically designed for the growing e-commerce fulfillment sector. These developments reflect the industry's focus on technological advancement, energy efficiency, and market expansion, with companies increasingly competing on smart features and total lifecycle value rather than solely on initial purchase price.