3D Metrology Market Overview - Definition, scope, and significance

3D metrology refers to the science of measurement in three dimensions, encompassing technologies and processes used to measure the physical geometrical characteristics of objects. This market includes hardware such as coordinate measuring machines (CMMs), optical digitizers, and laser scanners, as well as software solutions for data analysis and processing. The significance of 3D metrology lies in its critical role across industries where precision and quality control are paramount. From automotive manufacturing to aerospace engineering, 3D metrology ensures that components meet exact specifications, reducing defects and improving overall product quality. The market's importance has grown substantially with the increasing complexity of products and the demand for higher precision in manufacturing processes.

3D Metrology Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The 3D metrology market is driven by several key factors, including the increasing adoption of automation in manufacturing, the growing demand for quality control and inspection across industries, and the rise of Industry 4.0 initiatives. The automotive and aerospace sectors, in particular, are major drivers due to their need for precise measurements in complex component manufacturing. However, the market faces challenges such as the high cost of advanced metrology equipment and the need for skilled operators. Additionally, the integration of metrology systems with existing manufacturing processes can be complex and time-consuming. Opportunities in the market include the development of portable and handheld metrology devices, the integration of artificial intelligence and machine learning in metrology software, and the expansion of 3D metrology applications in emerging industries such as medical devices and renewable energy.

3D Metrology Market Growth Trends - Current and emerging trends shaping the market

The 3D metrology market is experiencing several notable growth trends. One significant trend is the increasing adoption of non-contact measurement technologies, such as optical and laser-based systems, which offer faster and more versatile measurement capabilities compared to traditional contact methods. Another emerging trend is the integration of Internet of Things (IoT) technologies with metrology systems, enabling real-time data collection and analysis. The market is also seeing a shift towards cloud-based metrology software solutions, which offer improved accessibility and collaboration capabilities. Additionally, there is a growing trend towards the use of augmented reality (AR) and virtual reality (VR) in metrology applications, particularly for training and visualization purposes. The increasing demand for in-line and in-process metrology solutions is also shaping the market, as manufacturers seek to improve efficiency and reduce production time.

COVID-19 Impact on the 3D Metrology Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the 3D metrology market, as it did on many industrial sectors. During the initial phases of the pandemic, many manufacturing facilities were forced to shut down or operate at reduced capacity, leading to a temporary decline in demand for metrology equipment and services. However, the pandemic also highlighted the importance of quality control and precision manufacturing, particularly in the production of medical devices and personal protective equipment. As industries adapted to new safety protocols and implemented social distancing measures, there was an increased demand for automated and non-contact metrology solutions. The market is now on a recovery trajectory, with many industries resuming operations and investing in advanced metrology technologies to improve efficiency and ensure product quality in a post-pandemic world.

3D Metrology Market Competitive Landscape - Major competitors and market consolidation

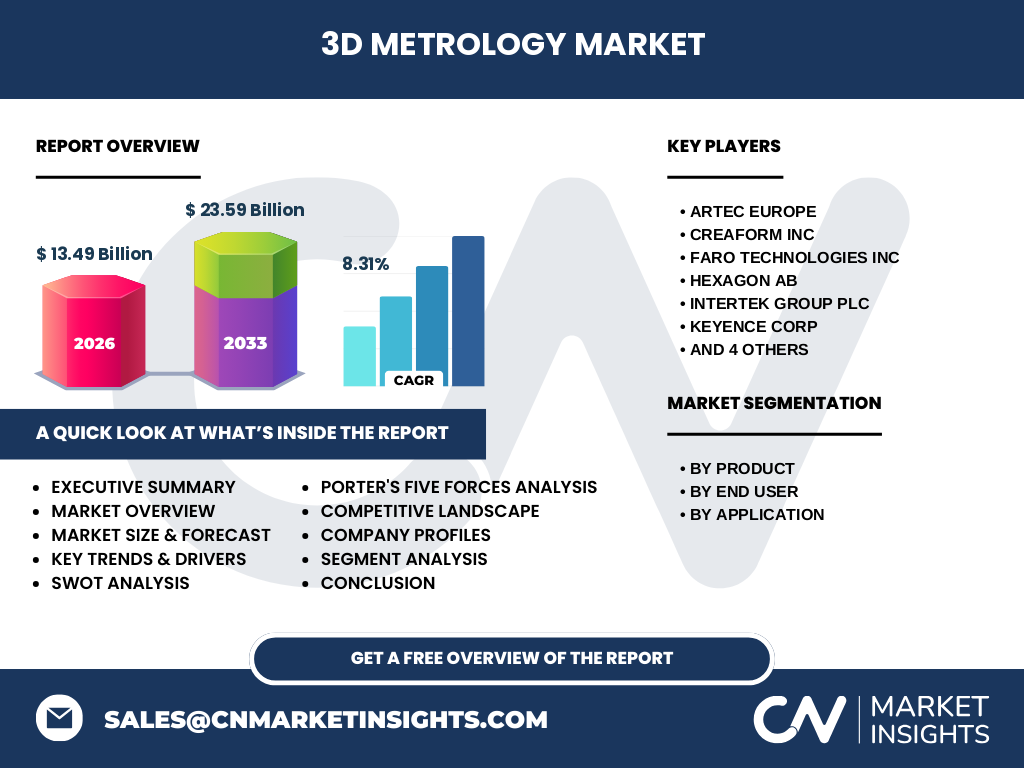

The 3D metrology market is characterized by the presence of several key players, including Artec Europe, Creaform Inc, FARO Technologies Inc, Hexagon AB, Intertek Group Plc, KEYENCE CORP, Mitutoyo Corporation, Nikon Metrology NV, Shining3D, and ZEISS. These companies compete on various factors such as product innovation, technological advancements, and global reach. The market has seen some consolidation in recent years, with larger companies acquiring smaller, specialized metrology firms to expand their product portfolios and market presence. For instance, Hexagon AB has made several strategic acquisitions to strengthen its position in the metrology market. Competition in the market is intense, with companies focusing on developing advanced technologies, improving user interfaces, and offering comprehensive software solutions to gain a competitive edge.

Executive Summary - High-level overview and key findings about 3D Metrology Market

The 3D metrology market is poised for significant growth, driven by increasing demand for precision manufacturing across various industries. With a projected compound annual growth rate (CAGR) of 8.31%, the market is expected to reach a value of 23.59 billion by 2033, up from 13.49 billion in 2026. This growth is fueled by advancements in metrology technologies, the rising adoption of automation in manufacturing, and the increasing complexity of products requiring precise measurements. The market is segmented by product type, end-user industry, and application, with hardware, automotive, and quality control and inspection being the dominant segments. Key players in the market are focusing on innovation and strategic partnerships to maintain their competitive edge. Despite challenges such as high equipment costs and the need for skilled operators, the market presents numerous opportunities for growth, particularly in emerging applications and regions.

3D Metrology Market Forecast - Projections for 2025-2032 period

The 3D metrology market is projected to experience robust growth between 2025 and 2032, with a compound annual growth rate (CAGR) of 8.31%. Starting from a market size of 13.49 billion in 2026, the market is expected to reach 23.59 billion by 2033. This growth is driven by increasing adoption of 3D metrology solutions across various industries, technological advancements in metrology equipment, and the rising demand for quality control and inspection. The forecast period is likely to see continued innovation in metrology technologies, with a focus on improving accuracy, speed, and ease of use. The integration of artificial intelligence and machine learning in metrology software is expected to be a significant trend during this period. Additionally, the market is likely to witness increased adoption of portable and handheld metrology devices, catering to the growing demand for flexible and on-site measurement solutions.

3D Metrology Market Size and Share by Segmentation - Breakdown by {segmentData}

The 3D metrology market is segmented by product type, end-user industry, and application. By product type, the market is divided into hardware, services, and software. Hardware currently dominates the market, driven by the high demand for advanced measurement equipment such as coordinate measuring machines and optical digitizers. However, the software segment is expected to witness significant growth due to the increasing need for sophisticated data analysis and processing tools. In terms of end-user industries, the automotive sector holds a substantial share of the market, followed by electronics, aerospace and defense, and medical industries. The quality control and inspection application segment accounts for the largest share of the market, reflecting the critical importance of precision measurement in manufacturing processes. Other applications such as reverse engineering and virtual simulation are also gaining traction, particularly in industries focused on product development and prototyping.

Global 3D Metrology Market Size and Share by Region - Geographic distribution

The global 3D metrology market exhibits varying growth patterns across different regions. North America currently holds a significant share of the market, driven by the presence of major metrology companies, advanced manufacturing industries, and high adoption of Industry 4.0 technologies. Europe follows closely, with countries like Germany, France, and the UK being key contributors due to their strong automotive and aerospace sectors. The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, fueled by rapid industrialization, increasing investments in manufacturing, and the growing adoption of advanced metrology solutions in countries like China, Japan, and South Korea. The region's expanding electronics and automotive industries are particularly driving demand for 3D metrology equipment. Latin America and the Middle East & Africa regions are also showing promising growth, albeit at a slower pace, as industries in these regions increasingly recognize the importance of quality control and precision manufacturing.

Regional Analysis of the 3D Metrology Market - Detailed regional market performance

The 3D metrology market's performance varies significantly across different regions. In North America, the market is characterized by high adoption rates of advanced metrology technologies, driven by the presence of major manufacturing industries and a strong focus on quality control. The region's aerospace and defense sector, in particular, is a significant contributor to market growth. Europe, with its robust automotive and aerospace industries, particularly in countries like Germany and France, represents another key market for 3D metrology. The region is also witnessing increased adoption of Industry 4.0 technologies, driving demand for advanced metrology solutions. In the Asia-Pacific region, rapid industrialization and the growing presence of electronics and automotive manufacturing hubs are fueling market growth. Countries like China, Japan, and South Korea are investing heavily in advanced manufacturing technologies, including 3D metrology. The region is also seeing increased adoption of portable and handheld metrology devices, catering to the needs of small and medium-sized enterprises.

Leading Company Profiles in the 3D Metrology Market - Industry players and strategies

The 3D metrology market is dominated by several key players, each with its unique strengths and strategies. Hexagon AB, for instance, has established itself as a leader through a combination of innovative product development and strategic acquisitions. The company's focus on integrating software and hardware solutions has positioned it strongly in the market. FARO Technologies Inc is known for its portable metrology solutions, catering to industries that require on-site measurements. Mitutoyo Corporation, with its long-standing reputation in precision measurement, continues to innovate in both contact and non-contact metrology technologies. ZEISS, leveraging its expertise in optics, has developed advanced optical metrology solutions that are widely used in the semiconductor and electronics industries. These companies, along with others like Artec Europe, Creaform Inc, and Shining3D, are continuously investing in research and development to introduce new products and improve existing technologies, aiming to maintain their competitive edge in the market.

Porter's Five Forces Analysis of the 3D Metrology Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the 3D metrology market. The threat of new entrants is moderate, as the market requires significant capital investment and technical expertise to develop advanced metrology solutions. However, the presence of open-source software and the increasing availability of 3D printing technologies may lower entry barriers for some niche players. The bargaining power of buyers is relatively high, given the availability of multiple suppliers and the increasing commoditization of some metrology equipment. Suppliers' bargaining power is moderate, with key components and technologies being sourced from a limited number of specialized suppliers. The threat of substitutes is low, as 3D metrology technologies offer unique capabilities that are difficult to replicate with alternative methods. Competitive rivalry in the market is intense, with major players competing on factors such as product innovation, pricing, and after-sales services. The market is also witnessing increased collaboration between metrology companies and end-user industries to develop customized solutions.

SWOT Analysis of the 3D Metrology Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the 3D metrology market reveals several key factors influencing its growth and development. Strengths of the market include the increasing demand for precision manufacturing across industries, the continuous technological advancements in metrology equipment, and the growing adoption of Industry 4.0 technologies. The market also benefits from the critical role that metrology plays in quality control and assurance processes. However, weaknesses such as the high cost of advanced metrology equipment and the need for skilled operators to use complex systems pose challenges to market growth. Opportunities in the market are abundant, including the expansion of metrology applications into new industries, the development of portable and user-friendly metrology solutions, and the integration of artificial intelligence and machine learning in metrology software. Threats to the market include economic uncertainties that may affect manufacturing investments, the potential for technological disruptions that could render existing solutions obsolete, and increasing competition from both established players and new entrants.

3D Metrology Market Value Chain Analysis - Industry structure and value flow

The 3D metrology market value chain encompasses several key stages, from raw material suppliers to end-users. At the beginning of the chain, suppliers of specialized components such as sensors, lasers, and precision mechanical parts provide the building blocks for metrology equipment. These components are then used by metrology equipment manufacturers to produce hardware solutions like coordinate measuring machines, optical scanners, and portable metrology devices. Software developers create the data analysis and processing tools that complement the hardware, often working in collaboration with equipment manufacturers. Distributors and system integrators play a crucial role in bringing these solutions to end-users, providing installation, training, and after-sales support. The end-users, primarily from industries such as automotive, aerospace, electronics, and medical devices, utilize these metrology solutions for quality control, inspection, and product development. Value is added at each stage of the chain, with continuous innovation and improvement driving the overall growth of the market.

Key Investment Insights in the 3D Metrology Market - Strategic investment recommendations

The 3D metrology market presents several attractive investment opportunities for both established players and new entrants. One key area for investment is the development of advanced software solutions that leverage artificial intelligence and machine learning to improve data analysis and decision-making processes. As the volume of metrology data continues to grow, there is an increasing need for intelligent software that can provide actionable insights in real-time. Another promising area is the development of portable and handheld metrology devices, which offer flexibility and ease of use for on-site measurements. Investments in the integration of metrology systems with other manufacturing technologies, such as robotics and IoT, could also yield significant returns as industries move towards more connected and automated production environments. Additionally, there is potential for growth in emerging markets, particularly in the Asia-Pacific region, where rapid industrialization is driving demand for advanced manufacturing technologies. Strategic partnerships and collaborations between metrology companies and end-user industries could also provide valuable investment opportunities, allowing for the development of customized solutions that address specific industry needs.

3D Metrology Market Conclusion - Summary and key takeaways

The 3D metrology market is experiencing significant growth, driven by increasing demand for precision manufacturing across various industries and continuous technological advancements. With a projected compound annual growth rate (CAGR) of 8.31%, the market is expected to reach 23.59 billion by 2033, up from 13.49 billion in 2026. Key trends shaping the market include the adoption of non-contact measurement technologies, the integration of IoT and AI in metrology systems, and the growing demand for portable and handheld devices. While the market faces challenges such as high equipment costs and the need for skilled operators, it presents numerous opportunities for growth, particularly in emerging applications and regions. The competitive landscape is characterized by the presence of several major players, each focusing on innovation and strategic partnerships to maintain their market position. As industries continue to prioritize quality control and precision manufacturing, the 3D metrology market is poised for continued expansion and technological advancement in the coming years.

Research Methodology - How this research was conducted

This research on the 3D metrology market was conducted using a comprehensive methodology that combines both primary and secondary research. Primary research involved interviews with industry experts, including metrology equipment manufacturers, software developers, and end-users from various industries. These interviews provided valuable insights into market trends, technological advancements, and future growth prospects. Secondary research involved an extensive review of industry reports, company annual reports, press releases, and relevant publications. Data from government sources, industry associations, and market research databases were also analyzed to validate findings and provide a broader context for the market analysis. The research methodology also included a detailed analysis of the competitive landscape, market segmentation, and regional dynamics. To ensure accuracy and reliability, the findings were cross-validated using multiple data sources and expert opinions.

Research Scope - Coverage and limitations

The scope of this research on the 3D metrology market encompasses a comprehensive analysis of the market's current state and future prospects. The research covers key market segments, including product types (hardware, services, and software), end-user industries (automotive, electronics, aerospace and defense, medical, energy and power, and heavy machinery), and applications (quality control and inspection, reverse engineering, and virtual simulation). The study also includes a detailed regional analysis, examining market dynamics across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The research timeframe extends from 2025 to 2032, providing both historical context and future projections. However, it's important to note that the research has certain limitations. The availability and reliability of data, particularly in emerging markets, may affect the accuracy of some projections. Additionally, rapid technological changes in the metrology industry could potentially impact market dynamics in ways that are difficult to predict. Despite these limitations, the research provides a robust and comprehensive overview of the 3D metrology market, offering valuable insights for industry stakeholders and potential investors.

Key Companies and Recent Developments in the 3D Metrology Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The 3D metrology market is characterized by the presence of several key players who are continuously innovating and expanding their market presence. Hexagon AB, one of the market leaders, has recently announced the launch of its new Metrology Software Suite, which integrates various metrology applications into a single platform, enhancing productivity and ease of use. FARO Technologies Inc has introduced its latest generation of portable CMMs, offering improved accuracy and speed for on-site measurements. Mitutoyo Corporation has expanded its product line with the introduction of advanced optical measurement systems, catering to the growing demand for non-contact metrology solutions. ZEISS has announced a strategic partnership with a leading automotive manufacturer to develop customized metrology solutions for electric vehicle production. Shining3D has launched a new series of 3D scanners with enhanced portability and user-friendly interfaces, targeting small and medium-sized enterprises. These developments reflect the industry's focus on innovation, user experience, and addressing specific industry needs. Additionally, many companies are investing in research and development to integrate artificial intelligence and machine learning capabilities into their metrology solutions, aiming to provide more intelligent and automated measurement processes.