Specialty Hospitals Market Overview - Definition, scope, and significance

Specialty hospitals are healthcare facilities that focus on providing specialized medical care for specific patient populations, medical conditions, or treatment modalities. Unlike general hospitals that offer a broad range of medical services, specialty hospitals concentrate their expertise, resources, and infrastructure on particular areas of medicine such as oncology, orthopedics, cardiology, neurology, pediatrics, or rehabilitation. These facilities are designed to deliver highly specialized care with dedicated equipment, specialized medical staff, and treatment protocols tailored to their specific focus area. The significance of specialty hospitals lies in their ability to provide concentrated expertise, potentially better outcomes for specific conditions, and more efficient resource utilization compared to general hospitals. They serve as centers of excellence for particular medical conditions and often become referral destinations for complex cases requiring specialized knowledge and advanced treatment approaches.

Specialty Hospitals Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The specialty hospitals market is driven by several key factors including the rising prevalence of chronic diseases, an aging global population requiring specialized care, technological advancements in medical treatments, and increasing patient preference for specialized care facilities. The growing demand for personalized medicine and targeted therapies has also contributed to the expansion of specialty hospitals. However, the market faces restraints such as high operational costs, regulatory challenges, and the need for significant capital investment in specialized equipment and trained personnel. Challenges include maintaining consistent quality standards across different specialties, managing complex reimbursement systems, and addressing workforce shortages in specialized medical fields. Opportunities exist in expanding into emerging markets, developing innovative treatment approaches, leveraging digital health technologies, and forming strategic partnerships between specialty hospitals and research institutions to advance medical knowledge and treatment options.

Specialty Hospitals Market Growth Trends - Current and emerging trends shaping the market

The specialty hospitals market is experiencing several notable growth trends, including the increasing adoption of minimally invasive surgical techniques, the integration of artificial intelligence and machine learning in diagnostic and treatment planning, and the expansion of telemedicine services within specialty care settings. There is a growing trend toward patient-centric care models that emphasize personalized treatment plans and improved patient experiences. The market is also witnessing the emergence of hybrid specialty hospitals that combine multiple related specialties under one roof to provide comprehensive care for complex conditions. Another significant trend is the focus on value-based care models that prioritize patient outcomes and cost-effectiveness. Additionally, there is increasing emphasis on preventive care and early intervention within specialty hospitals, particularly in areas such as oncology and cardiology, where early detection can significantly improve treatment outcomes.

COVID-19 Impact on the Specialty Hospitals Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the specialty hospitals market, initially causing significant disruptions in elective procedures and non-emergency specialized care. Many specialty hospitals faced operational challenges due to resource reallocation to support COVID-19 response efforts, including the repurposing of intensive care units and specialized equipment. However, the pandemic also accelerated certain trends within the specialty hospitals market, such as the adoption of telemedicine and remote monitoring technologies, which became essential for maintaining patient care during lockdowns and social distancing measures. The recovery trajectory has shown resilience, with specialty hospitals adapting to new safety protocols and implementing enhanced infection control measures. There has been a renewed focus on building healthcare system resilience, with specialty hospitals investing in surge capacity and flexible care models to better respond to future health crises while maintaining their core specialized services.

Specialty Hospitals Market Competitive Landscape - Major competitors and market consolidation

The specialty hospitals market features a competitive landscape characterized by a mix of large healthcare systems, independent specialty facilities, and academic medical centers. Major competitors include established healthcare providers such as Cleveland Clinic, Johns Hopkins Medicine, and NYU Langone Hospitals, which operate multiple specialty hospitals and centers of excellence. The market has seen increasing consolidation through mergers and acquisitions, with larger healthcare systems acquiring independent specialty hospitals to expand their service offerings and geographic reach. Competition is driven by factors such as clinical expertise, technological capabilities, patient outcomes, and brand reputation. The market also includes specialized for-profit operators like HCA Healthcare and Universal Health Services, as well as non-profit organizations focused on specific medical conditions. Competition is intensifying as hospitals strive to differentiate themselves through innovative treatments, patient experience enhancements, and strategic partnerships with research institutions and technology companies.

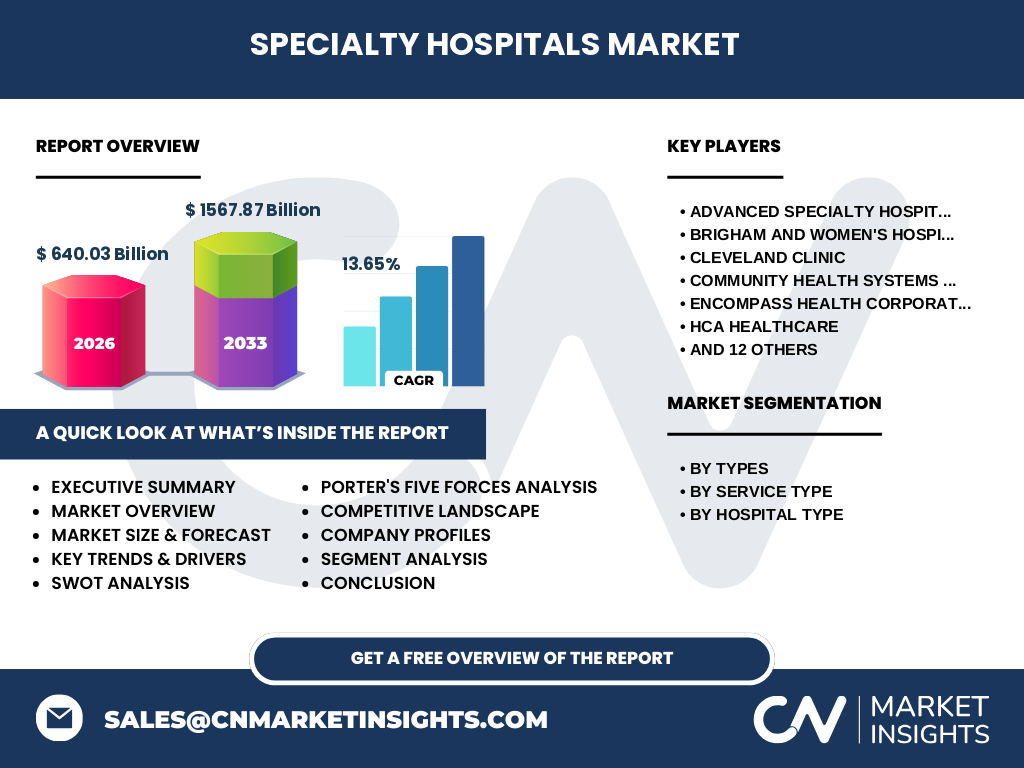

Executive Summary - High-level overview and key findings about Specialty Hospitals Market

The specialty hospitals market represents a significant and growing segment of the healthcare industry, characterized by facilities that provide focused, high-quality care for specific medical conditions or patient populations. With a market size of 640.03 Billion in 2026 and projected to reach 1567.87 Billion by 2033, the market demonstrates robust growth with a CAGR of 13.65%. The market encompasses various specialties including pediatric, obstetrics-gynecology, ENT, oncology, rehabilitation, orthopedic, neurology, cardiology, and IVF hospitals, serving both outpatient and inpatient needs across public and private hospital settings. Key players in the market include renowned institutions such as Cleveland Clinic, Johns Hopkins Medicine, and NYU Langone Hospitals, alongside specialized operators like HCA Healthcare and Universal Health Services. The market is driven by factors such as increasing chronic disease prevalence, technological advancements, and patient demand for specialized care, while facing challenges related to costs, regulation, and workforce shortages. The COVID-19 pandemic has accelerated digital transformation and highlighted the importance of healthcare system resilience, shaping the future trajectory of specialty hospitals.

Specialty Hospitals Market Forecast - Projections for 2025-2032 period

The specialty hospitals market is projected to experience significant growth during the 2025-2032 period, with the market size expected to increase from 640.03 Billion in 2026 to 1567.87 Billion by 2033, representing a compound annual growth rate (CAGR) of 13.65%. This robust growth forecast is driven by several factors, including the increasing prevalence of chronic diseases requiring specialized care, technological advancements in medical treatments, and the growing demand for personalized healthcare services. The forecast period is likely to see continued expansion across all specialty segments, with oncology, cardiology, and orthopedic hospitals potentially showing the strongest growth due to the aging population and rising incidence of related conditions. The outpatient segment is expected to grow faster than inpatient services, reflecting the trend toward less invasive treatments and shorter hospital stays. Geographic expansion into emerging markets and the development of new specialty areas are also expected to contribute to market growth during this period.

Specialty Hospitals Market Size and Share by Segmentation - Breakdown by {segmentData}

The specialty hospitals market can be segmented by types, service type, and hospital type. By types, the market includes pediatric hospitals, obstetrics-gynecology hospitals, ENT hospitals, oncology hospitals, rehabilitation hospitals, orthopedic hospitals, neurology hospitals, cardiology hospitals, and IVF hospitals. Each specialty segment serves a specific patient population or medical condition, with oncology and cardiology hospitals likely representing significant market shares due to the high prevalence of cancer and cardiovascular diseases globally. By service type, the market is divided into outpatient and inpatient services, with outpatient services gaining increasing importance due to advancements in minimally invasive procedures and the trend toward shorter hospital stays. By hospital type, the market comprises public hospitals and private hospitals, with private specialty hospitals often leading in terms of technological adoption and service quality, while public hospitals play a crucial role in providing accessible specialized care to broader populations.

Global Specialty Hospitals Market Size and Share by Region - Geographic distribution

The global specialty hospitals market exhibits varying growth patterns and market shares across different regions. North America, particularly the United States, represents a significant portion of the global market due to its advanced healthcare infrastructure, high healthcare expenditure, and the presence of major specialty hospital operators. Europe follows as another substantial market, with countries like Germany, France, and the United Kingdom showing strong growth in specialty healthcare services. The Asia-Pacific region is expected to demonstrate the highest growth rate during the forecast period, driven by increasing healthcare investments, rising middle-class populations, and growing awareness of specialized medical treatments. Emerging markets in Latin America and the Middle East & Africa are also showing promising growth, albeit from a smaller base, as these regions invest in improving their healthcare infrastructure and expanding access to specialized medical services. The regional distribution of the market is influenced by factors such as healthcare policies, economic development, disease prevalence, and cultural attitudes toward specialized care.

Regional Analysis of the Specialty Hospitals Market - Detailed regional market performance

Regional analysis of the specialty hospitals market reveals distinct characteristics and growth patterns across different geographic areas. In North America, the market is mature and highly competitive, with a strong focus on technological innovation and patient experience. The region benefits from advanced healthcare infrastructure, favorable reimbursement policies, and a high concentration of leading specialty hospitals and research institutions. Europe's specialty hospitals market is characterized by a mix of public and private providers, with varying healthcare systems across countries influencing market dynamics. The region emphasizes quality of care and patient outcomes, with significant investments in specialized medical technologies. The Asia-Pacific region presents a rapidly growing market, driven by increasing healthcare expenditure, expanding medical tourism, and government initiatives to improve healthcare access. Countries like China, India, and Singapore are emerging as key markets for specialty hospitals, with growing demand for advanced medical treatments and specialized care facilities. Latin America and the Middle East & Africa regions are experiencing gradual market development, with increasing investments in healthcare infrastructure and growing awareness of specialized medical services.

Leading Company Profiles in the Specialty Hospitals Market - Industry players and strategies

The specialty hospitals market features several leading companies that have established themselves as key players through their expertise, technological capabilities, and strategic approaches. Cleveland Clinic stands out as a world-renowned specialty hospital system, particularly in cardiology and neurology, known for its integrated care model and research excellence. Johns Hopkins Medicine is another prominent player, recognized for its comprehensive specialty services and pioneering medical research. NYU Langone Hospitals has gained prominence through its focus on specialized care across multiple disciplines and its commitment to medical education and innovation. HCA Healthcare, as one of the largest for-profit hospital operators, has a significant presence in the specialty hospitals market through its network of specialized facilities. Other notable players include Brigham and Women's Hospital, known for its expertise in complex medical conditions, and Memorial Sloan Kettering Cancer Center, a world leader in oncology care. These companies employ strategies such as technological innovation, strategic partnerships, and expansion into new specialty areas to maintain their competitive edge and market leadership.

Porter's Five Forces Analysis of the Specialty Hospitals Market - Competitive forces assessment

Porter's Five Forces analysis provides insights into the competitive dynamics of the specialty hospitals market. The threat of new entrants is moderate to high due to the significant capital requirements, regulatory hurdles, and the need for specialized expertise and reputation in the healthcare industry. However, emerging technologies and changing healthcare policies may create opportunities for new players. The bargaining power of buyers (patients) is increasing due to greater healthcare awareness, access to information, and the availability of alternative treatment options. The bargaining power of suppliers, including medical equipment manufacturers and pharmaceutical companies, is moderate, as specialty hospitals often require highly specialized and sometimes unique supplies. The threat of substitute products or services is present, with alternative treatment options such as outpatient clinics and telemedicine services potentially competing with traditional specialty hospital services. Competitive rivalry in the market is intense, driven by factors such as clinical outcomes, technological capabilities, patient experience, and brand reputation. The market is characterized by both large healthcare systems and specialized independent facilities competing for market share and patient volumes.

SWOT Analysis of the Specialty Hospitals Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the specialty hospitals market reveals several key factors influencing its development. Strengths of the market include the high level of specialized expertise available, advanced technological capabilities, and the potential for better patient outcomes in specific medical conditions. Specialty hospitals often have dedicated resources and staff focused on particular areas of medicine, allowing for more efficient and effective treatment. However, weaknesses include high operational costs, potential over-specialization that may limit flexibility in service offerings, and the challenge of maintaining expertise across multiple specialties for larger hospital systems. Opportunities in the market include the growing demand for specialized care due to aging populations and increasing chronic disease prevalence, technological advancements enabling new treatment options, and the potential for expansion into emerging markets. Threats to the market include regulatory challenges, reimbursement pressures, competition from general hospitals expanding their specialty services, and the potential for disruptive innovations in healthcare delivery models that could challenge traditional specialty hospital structures.

Specialty Hospitals Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the specialty hospitals market reveals a complex ecosystem of interconnected activities and stakeholders. The primary activities in the value chain include inbound logistics, involving the procurement of specialized medical equipment, supplies, and pharmaceuticals; operations, encompassing patient care delivery, diagnostic services, and treatment procedures; outbound logistics, which involves patient discharge planning and follow-up care coordination; marketing and sales, including patient acquisition and referral management; and service, covering post-treatment care and patient support. Support activities include procurement of specialized medical technologies, human resource management to attract and retain specialized medical professionals, technological development for advanced treatment options, and infrastructure development to support specialized care delivery. The value chain also involves key partnerships with research institutions, medical device manufacturers, pharmaceutical companies, and insurance providers. Effective management of this value chain is crucial for specialty hospitals to deliver high-quality, efficient, and cost-effective specialized care while maintaining their competitive advantage in the market.

Key Investment Insights in the Specialty Hospitals Market - Strategic investment recommendations

Investment insights in the specialty hospitals market suggest several strategic opportunities for stakeholders. Investors should consider focusing on high-growth specialty areas such as oncology, cardiology, and neurology, which are expected to see increasing demand due to aging populations and rising disease prevalence. Investments in technological infrastructure, including advanced diagnostic equipment, telemedicine capabilities, and data analytics systems, are likely to yield significant returns as these technologies become increasingly integral to specialized care delivery. Strategic partnerships and collaborations between specialty hospitals, research institutions, and technology companies present opportunities for innovation and market expansion. There is also potential for investment in emerging markets, particularly in the Asia-Pacific region, where growing healthcare expenditure and improving infrastructure are driving demand for specialized medical services. Additionally, investments in workforce development and training programs to address shortages of specialized medical professionals could provide long-term competitive advantages. Investors should also consider the potential of value-based care models and outcomes-based reimbursement systems, which are likely to shape the future of specialty healthcare delivery.

Specialty Hospitals Market Conclusion - Summary and key takeaways

The specialty hospitals market represents a dynamic and growing segment of the healthcare industry, characterized by its focus on providing high-quality, specialized care for specific medical conditions and patient populations. With a market size of 640.03 Billion in 2026 and projected to reach 1567.87 Billion by 2033, growing at a CAGR of 13.65%, the market demonstrates significant potential for expansion and innovation. Key drivers of growth include the increasing prevalence of chronic diseases, technological advancements in medical treatments, and growing patient demand for specialized care. The market encompasses various specialties, including oncology, cardiology, orthopedics, and neurology, among others, serving both outpatient and inpatient needs across public and private hospital settings. Leading players such as Cleveland Clinic, Johns Hopkins Medicine, and NYU Langone Hospitals continue to shape the market through their expertise and innovative approaches to specialized care delivery. As the market evolves, factors such as digital transformation, value-based care models, and expansion into emerging markets are likely to play crucial roles in shaping its future trajectory.

Research Methodology - How this research was conducted

The research methodology for this specialty hospitals market analysis involved a comprehensive approach combining both primary and secondary research techniques. Primary research included interviews with industry experts, healthcare professionals, and key opinion leaders in the specialty hospitals sector to gather insights on market trends, challenges, and opportunities. Secondary research involved extensive analysis of industry reports, academic publications, government healthcare statistics, and company financial statements to validate and supplement primary findings. Market size and growth projections were derived using a combination of top-down and bottom-up approaches, considering factors such as disease prevalence, healthcare expenditure, and technological adoption rates. Data triangulation methods were employed to ensure the accuracy and reliability of the findings. The research also incorporated Porter's Five Forces analysis and SWOT analysis to provide a comprehensive understanding of the market dynamics and competitive landscape. Regional analysis was conducted by examining country-specific healthcare policies, economic indicators, and demographic trends to assess market potential across different geographic areas.

Research Scope - Coverage and limitations

The research scope for this specialty hospitals market analysis encompasses a comprehensive examination of the global market, covering key segments including hospital types (pediatric, obstetrics-gynecology, ENT, oncology, rehabilitation, orthopedic, neurology, cardiology, and IVF), service types (outpatient and inpatient), and hospital ownership types (public and private). The analysis includes major geographic regions such as North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The research covers the period from 2025 to 2032, with historical data and future projections provided for key market indicators. However, it is important to note some limitations of the research. The analysis is primarily focused on quantitative market data and may not capture all qualitative aspects of specialty hospital operations and patient experiences. Additionally, while efforts were made to include data from various regions, some emerging markets may have limited available information, potentially affecting the accuracy of regional projections. The research also does not delve into specific regulatory environments for each country, which can significantly impact market dynamics in different regions.

Key Companies and Recent Developments in the Specialty Hospitals Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The specialty hospitals market features several key companies that have made significant recent developments and strategic moves. Cleveland Clinic has continued to expand its global reach through partnerships and the establishment of new specialty centers, focusing on advancing cardiovascular and neurological care. Johns Hopkins Medicine has announced new initiatives in precision medicine and AI-driven diagnostics, aiming to enhance its specialty care offerings. NYU Langone Hospitals has recently launched innovative programs in cancer treatment and rehabilitation services, leveraging cutting-edge technologies and research collaborations. HCA Healthcare has made strategic acquisitions to strengthen its portfolio of specialty hospitals, particularly in high-demand areas such as oncology and orthopedics. Memorial Sloan Kettering Cancer Center has announced advancements in immunotherapy treatments and expanded its precision oncology programs. Brigham and Women's Hospital has introduced new specialized units for complex medical conditions, incorporating the latest in minimally invasive surgical techniques. These companies, along with other major players like Stanford Health Care and Indiana University Health, continue to drive innovation in the specialty hospitals market through strategic partnerships, technological advancements, and expanded service offerings, shaping the future of specialized healthcare delivery.