India Natural Gas and LNG Market Overview - Definition, scope, and significance

The India Natural Gas and LNG Market encompasses the production, distribution, and consumption of natural gas and liquefied natural gas within the Indian subcontinent. Natural gas serves as a cleaner alternative to traditional fossil fuels, playing a crucial role in India's energy transition strategy. The market includes upstream activities such as exploration and production, midstream operations like transportation and storage, and downstream services including distribution to end-users. The significance of this market lies in its potential to reduce India's carbon footprint while meeting the country's growing energy demands, supporting industrial growth, and enhancing energy security through diversified supply sources.

India Natural Gas and LNG Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

Key drivers propelling the India Natural Gas and LNG Market include government initiatives to increase the share of natural gas in the energy mix, growing environmental awareness, and the need for cleaner fuel alternatives. The expansion of city gas distribution networks and increasing industrial demand also contribute to market growth. However, the market faces restraints such as high infrastructure costs, price volatility, and competition from other energy sources. Challenges include the development of LNG import terminals, pipeline connectivity issues, and regulatory hurdles. Opportunities exist in expanding LNG import capacity, developing domestic gas fields, and leveraging technological advancements to improve efficiency and reduce costs across the value chain.

India Natural Gas and LNG Market Growth Trends - Current and emerging trends shaping the market

The India Natural Gas and LNG Market is witnessing several significant trends. There is a growing emphasis on increasing the share of natural gas in the primary energy mix, with the government targeting a 15% share by 2030. The expansion of city gas distribution networks to cover more geographical areas is another notable trend. Additionally, there is an increasing focus on LNG imports to meet domestic demand, with several new regasification terminals being planned or under construction. The market is also seeing a shift towards digitalization and the adoption of advanced technologies for efficient operations and supply chain management. Furthermore, there is a trend towards developing small-scale LNG solutions to cater to remote and industrial areas not connected by pipelines.

Emerging trends include the exploration of green hydrogen production using natural gas as a feedstock, the development of floating storage and regasification units (FSRUs) for flexible LNG imports, and the integration of renewable energy sources with natural gas infrastructure. The market is also witnessing increased interest in compressed natural gas (CNG) for transportation and piped natural gas (PNG) for domestic and commercial use. These trends are shaping the future of the India Natural Gas and LNG Market, driving innovation and creating new opportunities for growth and development.

COVID-19 Impact on the India Natural Gas and LNG Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the India Natural Gas and LNG Market, causing disruptions across the entire value chain. The initial lockdowns and subsequent restrictions led to a sharp decline in industrial activity and energy demand, resulting in reduced consumption of natural gas. LNG imports were particularly affected due to decreased demand and supply chain disruptions. The power sector, a major consumer of natural gas, experienced reduced electricity demand, further impacting gas consumption. City gas distribution networks also faced challenges due to reduced mobility and commercial activity.

However, the market has shown resilience and is on a recovery trajectory. As economic activities resumed, there was a gradual increase in natural gas demand, particularly in the industrial and power sectors. The government's continued focus on expanding the natural gas infrastructure and increasing its share in the energy mix has provided support for market recovery. The pandemic has also accelerated the adoption of digital technologies and remote monitoring systems in the industry. Looking ahead, the market is expected to witness sustained growth as India continues its economic recovery and focuses on cleaner energy sources to meet its climate commitments.

India Natural Gas and LNG Market Competitive Landscape - Major competitors and market consolidation

The India Natural Gas and LNG Market features a mix of public sector undertakings, private companies, and international players. Major competitors in the market include GAIL (India) Limited, Oil and Natural Gas Corporation (ONGC), Indian Oil Corporation Limited (IOCL), Bharat Petroleum Corporation Limited (BPCL), and Hindustan Petroleum Corporation Limited (HPCL). These companies are involved in various aspects of the natural gas value chain, from exploration and production to distribution and marketing.

In the LNG segment, key players include Petronet LNG Limited, which operates major LNG import terminals, and international companies like Royal Dutch Shell and Total S.A., which have a significant presence in the Indian market. The city gas distribution sector is dominated by companies such as Indraprastha Gas Limited, Mahanagar Gas Limited, and Gujarat Gas Limited. These companies are responsible for the distribution of natural gas to households, commercial establishments, and transport sectors in their respective regions.

The market is witnessing increasing consolidation as companies seek to strengthen their positions and expand their geographical presence. This is evident in the growing number of mergers, acquisitions, and joint ventures among both domestic and international players. The competitive landscape is also characterized by investments in infrastructure development, technological advancements, and strategic partnerships to enhance market share and improve operational efficiency.

Executive Summary - High-level overview and key findings about India Natural Gas and LNG Market

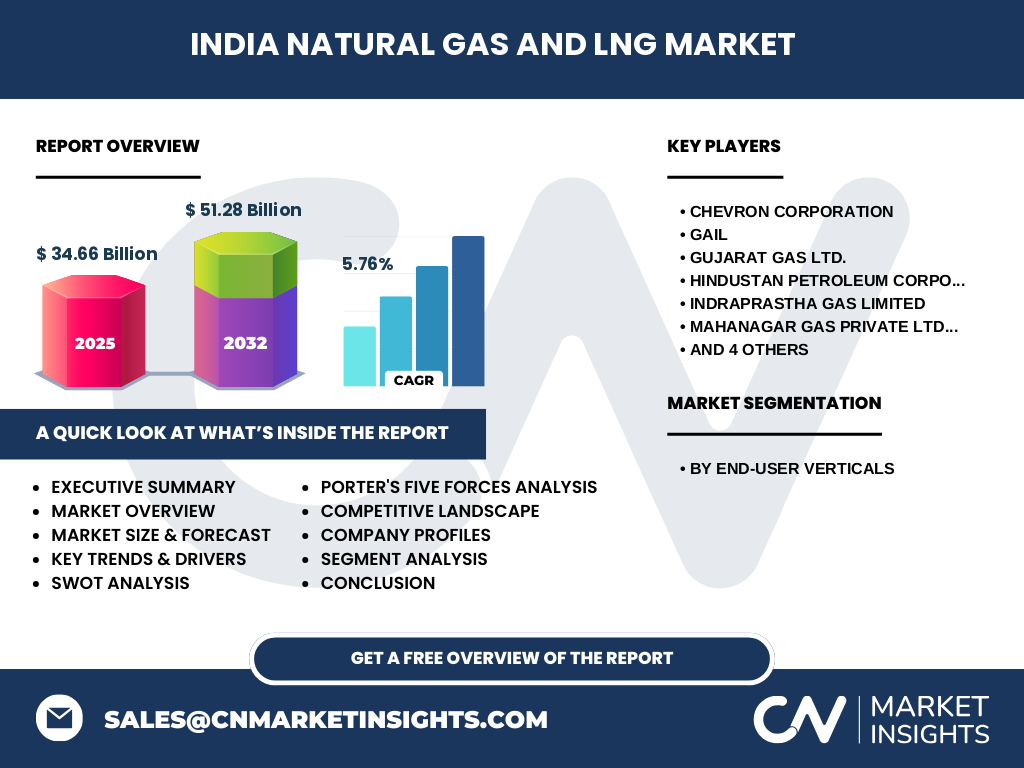

The India Natural Gas and LNG Market is poised for significant growth, driven by increasing energy demand, government initiatives for cleaner fuel adoption, and expanding infrastructure. The market, valued at 34.66 Billion in 2025, is projected to reach 51.28 Billion by 2032, growing at a CAGR of 5.76%. This growth is underpinned by the government's target to increase the share of natural gas in the primary energy mix to 15% by 2030, up from the current 6.2%.

Key findings indicate that the market is segmented by end-user verticals, including Power, Fertilizer, City Gas Distribution, and Industrial sectors. The City Gas Distribution segment is expected to witness substantial growth due to the expansion of piped natural gas networks across the country. The Industrial sector remains a significant consumer, driven by the need for cleaner fuel alternatives and cost-effective energy solutions.

The competitive landscape is characterized by the presence of major public sector undertakings, private companies, and international players. Key companies such as GAIL, ONGC, and Petronet LNG are focusing on expanding their infrastructure and market presence through strategic investments and partnerships. The market is also witnessing technological advancements, particularly in LNG regasification and distribution, to improve efficiency and reduce costs.

Despite challenges such as high infrastructure costs and regulatory hurdles, the market presents numerous opportunities for growth. These include the development of new LNG import terminals, expansion of city gas distribution networks, and the integration of renewable energy sources with natural gas infrastructure. The COVID-19 pandemic has accelerated the adoption of digital technologies, which is expected to further enhance operational efficiency and market resilience.

India Natural Gas and LNG Market Forecast - Projections for 2025-2032 period

The India Natural Gas and LNG Market is expected to experience steady growth over the forecast period of 2025-2032. Starting from a market size of 34.66 Billion in 2025, the market is projected to reach 51.28 Billion by 2032, reflecting a compound annual growth rate (CAGR) of 5.76%. This growth trajectory is underpinned by several factors, including increasing energy demand, government initiatives to promote cleaner fuels, and expanding infrastructure for natural gas distribution and LNG imports.

The forecast period is likely to witness significant developments in the market, particularly in the expansion of city gas distribution networks and the addition of new LNG import terminals. The power sector is expected to remain a major consumer of natural gas, driven by the need for cleaner and more efficient energy sources. The industrial sector is also projected to contribute to market growth, as industries increasingly adopt natural gas for its cost-effectiveness and lower emissions compared to other fossil fuels.

In terms of LNG imports, the market is expected to see a substantial increase in regasification capacity, with several new terminals planned or under construction. This expansion will enhance India's ability to meet its growing natural gas demand through imports. The fertilizer sector, which is a significant consumer of natural gas, is also likely to contribute to market growth, supported by government policies aimed at increasing domestic fertilizer production.

While the market faces challenges such as price volatility and infrastructure development costs, the overall outlook remains positive. The government's continued focus on increasing the share of natural gas in the energy mix, coupled with technological advancements and strategic investments by key players, is expected to drive sustained growth in the India Natural Gas and LNG Market over the forecast period.

India Natural Gas and LNG Market Size and Share by Segmentation - Breakdown by {segmentData}

The India Natural Gas and LNG Market is segmented by end-user verticals, providing insights into the distribution of market size and share across different sectors. The primary segments include Power, Fertilizer, City Gas Distribution, and Industrial sectors.

The Power sector is a significant consumer of natural gas in India, utilizing it for electricity generation. This segment is expected to maintain a substantial share of the market, driven by the need for cleaner and more efficient energy sources to meet the country's growing electricity demand. The Fertilizer sector also represents a considerable portion of the market, as natural gas is a key feedstock for the production of urea and other fertilizers. Government policies aimed at increasing domestic fertilizer production are likely to support the growth of this segment.

The City Gas Distribution (CGD) segment is witnessing rapid expansion, with the government's initiative to increase the coverage of piped natural gas networks across the country. This segment includes the distribution of natural gas to households, commercial establishments, and the transport sector. The CGD segment is expected to show significant growth during the forecast period, driven by increasing urbanization and the shift towards cleaner fuel alternatives.

The Industrial sector, which includes manufacturing, petrochemicals, and other industries, is another major consumer of natural gas. This segment is likely to maintain a substantial share of the market, as industries increasingly adopt natural gas for its cost-effectiveness and lower emissions compared to other fossil fuels. The growth of this segment is supported by the overall industrial development in the country and the push towards cleaner energy sources.

While specific market share percentages are not provided, the segmentation by end-user verticals offers a comprehensive view of how the India Natural Gas and LNG Market is distributed across different sectors. This breakdown helps in understanding the relative importance of each segment and their contribution to the overall market growth and dynamics.

Global India Natural Gas and LNG Market Size and Share by Region - Geographic distribution

The India Natural Gas and LNG Market exhibits a diverse geographic distribution, with significant variations in consumption and infrastructure development across different regions of the country. While specific regional market share data is not provided, it is possible to outline the general geographic distribution based on known consumption patterns and infrastructure development.

The western region of India, particularly Gujarat, is a major hub for natural gas consumption and infrastructure. Gujarat hosts several LNG import terminals and has an extensive pipeline network, making it a key region for natural gas distribution. The state's industrial base, including petrochemicals and fertilizers, contributes significantly to natural gas consumption in this region.

The northern region, especially around the National Capital Region (NCR), has seen substantial growth in city gas distribution networks. Delhi and its surrounding areas have witnessed significant expansion in piped natural gas connections for households and CNG stations for vehicles. This region is expected to maintain a strong presence in the market due to ongoing urbanization and government initiatives to promote cleaner fuels.

The western coast, including Maharashtra and Gujarat, is crucial for LNG imports, with major terminals located in Dahej and Hazira. These regions play a vital role in meeting the country's LNG demand and are likely to continue their importance in the market.

The eastern region, particularly around the Krishna-Godavari basin, is significant for domestic natural gas production. States like Andhra Pradesh and Telangana are key consumers of natural gas, especially in the power and industrial sectors.

The southern region, including Tamil Nadu and Karnataka, has been expanding its natural gas infrastructure, particularly in city gas distribution and power generation. The region's growing industrial base and increasing focus on cleaner energy sources are expected to drive natural gas consumption.

While specific market share data for each region is not provided, this geographic distribution highlights the diverse nature of the India Natural Gas and LNG Market and the varying levels of development and consumption across different parts of the country.

Regional Analysis of the India Natural Gas and LNG Market - Detailed regional market performance

The India Natural Gas and LNG Market exhibits distinct regional characteristics and performance across different parts of the country. While specific quantitative data for each region is not provided, a detailed analysis based on known infrastructure and consumption patterns can be outlined.

Western India, particularly Gujarat, stands out as a leader in natural gas consumption and infrastructure. The region hosts major LNG import terminals, including the Dahej terminal operated by Petronet LNG, which is one of the largest in the country. Gujarat's extensive pipeline network and industrial base, including petrochemicals and fertilizers, contribute significantly to the region's strong performance in the natural gas market. The state's proactive policies in promoting natural gas usage have further bolstered its position.

The National Capital Region (NCR) in Northern India has shown remarkable growth in city gas distribution. Delhi, in particular, has witnessed a rapid expansion of piped natural gas connections for households and a growing network of CNG stations for vehicles. This growth is driven by government initiatives to promote cleaner fuels and reduce air pollution in the capital city. The region's performance is characterized by increasing consumer adoption and expanding infrastructure.

The Western Coast, including Maharashtra, plays a crucial role in LNG imports and distribution. The region's strategic location and existing port infrastructure have facilitated the development of LNG terminals, such as the one in Hazira. Maharashtra's industrial and commercial centers, particularly around Mumbai, contribute to significant natural gas consumption, supporting the region's strong market performance.

The Eastern region, centered around the Krishna-Godavari basin, is vital for domestic natural gas production. States like Andhra Pradesh and Telangana have developed substantial natural gas infrastructure, particularly in power generation and industrial applications. The region's performance is characterized by a balance between production and consumption, with a focus on utilizing domestic resources.

Southern India, including Tamil Nadu and Karnataka, has been expanding its natural gas infrastructure, particularly in city gas distribution and power generation. The region's growing industrial base and increasing focus on cleaner energy sources are driving natural gas consumption. The performance in this region is marked by gradual but steady growth in natural gas adoption across various sectors.

While specific market share data for each region is not provided, this analysis highlights the diverse nature of the India Natural Gas and LNG Market and the varying levels of development and consumption across different parts of the country. Each region's performance is influenced by factors such as existing infrastructure, industrial base, government policies, and consumer adoption of natural gas.

Leading Company Profiles in the India Natural Gas and LNG Market - Industry players and strategies

The India Natural Gas and LNG Market is characterized by the presence of several key players, each with distinct strategies and market positions. While specific details about each company's market share or recent developments are not provided, an overview of the leading companies and their general strategies can be outlined.

GAIL (India) Limited, a Maharatna PSU, is one of the largest players in the natural gas sector. The company's strategy focuses on expanding its pipeline network, increasing LNG import capacity, and diversifying into city gas distribution. GAIL's integrated business model, covering exploration, production, transmission, and marketing, positions it as a key player in the value chain.

Oil and Natural Gas Corporation (ONGC), another major public sector undertaking, primarily focuses on exploration and production. ONGC's strategy involves increasing domestic gas production to reduce import dependence and exploring opportunities in deepwater and unconventional gas resources. The company's strong upstream capabilities make it a crucial player in ensuring India's natural gas supply.

Petronet LNG Limited is a leader in the LNG import and regasification segment. The company's strategy revolves around expanding its LNG terminal capacity, both through brownfield expansions and greenfield projects. Petronet LNG's focus on long-term LNG sourcing agreements and its plans to venture into LNG bunkering and small-scale LNG distribution highlight its growth-oriented approach.

Gujarat Gas Ltd., the largest city gas distribution company in India, has a strategy centered on expanding its geographical presence and customer base. The company focuses on increasing PNG connections for households and commercial establishments, as well as growing its CNG business for vehicles. Gujarat Gas's strong regional presence and customer-centric approach have been key to its success.

Indraprastha Gas Limited (IGL) dominates the city gas distribution market in the National Capital Region. IGL's strategy involves continuous expansion of its pipeline network, increasing CNG stations, and promoting PNG connections. The company's focus on the Delhi market, coupled with its efforts to improve operational efficiency, has solidified its position as a market leader in the region.

Hindustan Petroleum Corporation Ltd. (HPCL) and Indian Oil Corporation Ltd. (IOCL), both public sector oil marketing companies, have been expanding their presence in the natural gas sector. Their strategies include entering city gas distribution, setting up LNG facilities, and integrating natural gas into their existing fuel retail networks. These companies leverage their extensive retail presence and customer base to grow in the natural gas market.

Royal Dutch Shell PLC and Total S.A., international oil majors, have been increasing their investments in India's natural gas sector. Their strategies involve participating in LNG terminal projects, city gas distribution, and downstream marketing. These companies bring global expertise and technology to the Indian market, contributing to its development and growth.

While specific details about each company's market share or recent developments are not provided, these leading players collectively shape the India Natural Gas and LNG Market through their diverse strategies and significant investments in infrastructure and technology.

Porter's Five Forces Analysis of the India Natural Gas and LNG Market - Competitive forces assessment

Porter's Five Forces analysis provides a framework for understanding the competitive dynamics of the India Natural Gas and LNG Market. This analysis examines five key forces that shape the industry's competitive landscape and profitability potential.

1. Threat of New Entrants: The threat of new entrants in the India Natural Gas and LNG Market is moderate to high. While the market offers significant growth potential, barriers to entry are substantial. These barriers include the need for large capital investments in infrastructure such as pipelines, LNG terminals, and storage facilities. Additionally, regulatory approvals and government policies play a crucial role in market entry. However, the growing demand for natural gas and government initiatives to increase private sector participation are attracting new players, particularly in the city gas distribution segment.

2. Bargaining Power of Suppliers: The bargaining power of suppliers in the India Natural Gas and LNG Market is relatively high, especially for LNG imports. India relies heavily on imported LNG to meet its natural gas demand, making it dependent on global suppliers. This dependence gives suppliers significant leverage in pricing and contract negotiations. However, the presence of multiple LNG exporting countries and the development of long-term supply agreements have somewhat mitigated this power. For domestic gas production, the bargaining power of suppliers (primarily ONGC and Reliance Industries) is moderate, as they compete with imported LNG.

3. Bargaining Power of Buyers: The bargaining power of buyers in the India Natural Gas and LNG Market varies across segments. Large industrial consumers and power plants, being significant volume consumers, have moderate bargaining power. They can negotiate prices and switch between natural gas and alternative fuels based on economics. However, retail consumers in the city gas distribution segment, such as households and small commercial establishments, have low bargaining power due to the lack of alternatives and the essential nature of the product.

4. Threat of Substitute Products: The threat of substitutes in the India Natural Gas and LNG Market is moderate to high. Natural gas faces competition from alternative energy sources such as coal, oil, renewable energy, and nuclear power. In the power sector, renewable energy sources like solar and wind are increasingly becoming cost-competitive. In industrial applications, coal remains a significant competitor. However, natural gas's advantages in terms of lower emissions and efficiency help maintain its competitiveness in many applications.

5. Intensity of Competitive Rivalry: The intensity of competitive rivalry in the India Natural Gas and LNG Market is high. The market is characterized by the presence of both public sector undertakings and private players competing across the value chain. In the city gas distribution segment, there is intense competition for geographical exclusivity and market share. The LNG import segment also sees competition among terminal operators and marketers. This high rivalry is driving investments in infrastructure, technological advancements, and customer acquisition strategies.

Overall, Porter's Five Forces analysis reveals a dynamic and competitive market environment in India's natural gas and LNG sector. While the market offers significant growth opportunities, companies must navigate challenges related to supplier power, competitive intensity, and the threat of substitutes. Success in this market requires strategic investments, efficient operations, and the ability to adapt to changing market conditions and regulatory environments.

SWOT Analysis of the India Natural Gas and LNG Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the India Natural Gas and LNG Market provides insights into the internal strengths and weaknesses, as well as external opportunities and threats facing the industry.

Strengths:

1. Growing Energy Demand: India's rapidly expanding economy and population drive increasing energy demand, creating a strong market for natural gas.

2. Government Support: Proactive government policies and initiatives to increase the share of natural gas in the energy mix provide a favorable regulatory environment.

3. Expanding Infrastructure: Significant investments in pipeline networks, LNG terminals, and city gas distribution systems are enhancing the market's infrastructure.

4. Diverse Supply Sources: India's ability to source LNG from multiple global suppliers provides flexibility and energy security.

5. Environmental Benefits: Natural gas is considered a cleaner fuel compared to coal and oil, aligning with India's climate commitments and pollution reduction goals.

Weaknesses:

1. High Infrastructure Costs: The development of natural gas infrastructure requires substantial capital investments, which can be a barrier to rapid expansion.

2. Price Volatility: Natural gas prices, especially for LNG imports, can be volatile, affecting market stability and consumer affordability.

3. Domestic Production Limitations: India's domestic natural gas production is insufficient to meet growing demand, leading to high import dependence.

4. Complex Regulatory Environment: Multiple regulatory bodies and complex approval processes can slow down project implementation and market growth.

5. Competition from Alternatives: Natural gas faces competition from renewable energy sources and other fossil fuels in various applications.

Opportunities:

1. City Gas Distribution Expansion: The government's target to increase CGD coverage across the country presents significant growth opportunities.

2. LNG Import Capacity Growth: Plans to add new LNG import terminals can enhance India's ability to meet growing demand.

3. Industrial Sector Growth: Increasing industrialization and the need for cleaner fuel alternatives offer opportunities in the industrial segment.

4. Technological Advancements: Innovations in LNG regasification, distribution, and small-scale LNG can open new market segments.

5. Integration with Renewable Energy: Natural gas can complement renewable energy sources, providing opportunities for integrated energy solutions.

Threats:

1. Global Price Fluctuations: Volatility in global natural gas and LNG prices can impact India's import bill and market stability.

2. Geopolitical Risks: International tensions and trade disputes can affect LNG supply chains and pricing.

3. Policy Changes: Shifts in government policies or regulations could impact market growth and investment decisions.

4. Environmental Concerns: While cleaner than other fossil fuels, natural gas is still a source of greenhouse gas emissions, facing increasing scrutiny.

5. Infrastructure Security: The extensive pipeline network and LNG facilities require robust security measures against potential threats.

This SWOT analysis highlights the complex dynamics of the India Natural Gas and LNG Market, showcasing its potential for growth while also identifying the challenges that need to be addressed for sustainable development.

India Natural Gas and LNG Market Value Chain Analysis - Industry structure and value flow

The India Natural Gas and LNG Market value chain encompasses the entire process from gas exploration and production to its final consumption by end-users. This analysis outlines the key stages of the value chain and the participants involved in each stage.

1. Exploration and Production (E&P):

The value chain begins with the exploration and production of natural gas. In India, this segment is dominated by public sector undertakings like ONGC and Oil India Limited, along with private players like Reliance Industries. This stage involves geological surveys, drilling, and extraction of natural gas from onshore and offshore fields. The E&P segment is crucial for ensuring domestic supply, although India still relies heavily on imports to meet its demand.

2. Processing and Treatment:

Once extracted, natural gas undergoes processing to remove impurities and separate valuable byproducts like propane and butane. This stage is essential for ensuring the quality and safety of the gas before it enters the transportation network. Processing plants are typically located near production sites or import terminals.

3. Transportation:

Transportation is a critical link in the value chain, involving the movement of natural gas from production or import sites to consumption centers. This segment includes:

- Pipelines: Both cross-country and regional pipelines transport natural gas across long distances. GAIL operates a significant portion of India's pipeline network.

- LNG Shipping: For imported LNG, specialized vessels transport the liquefied gas from exporting countries to Indian terminals.

- LNG Trucks: For last-mile connectivity and remote areas, LNG is sometimes transported by road tankers.

4. Storage:

Storage facilities play a vital role in balancing supply and demand, especially for seasonal variations. This includes underground storage facilities and above-ground LNG storage tanks at import terminals and satellite stations.

5. Regasification (for LNG):

At LNG import terminals, the liquefied gas is converted back into its gaseous state through regasification. This process involves heating the LNG using sea water or other heating methods. Major regasification terminals in India include Dahej, Hazira, and Kochi.

6. Distribution:

The distribution segment involves delivering natural gas to end-users. This includes:

- City Gas Distribution (CGD): Companies like Indraprastha Gas Limited and Gujarat Gas distribute natural gas to households, commercial establishments, and transport sectors within cities.

- Industrial Supply: Direct supply to large industrial consumers through pipelines or LNG supply.

- Power Plants: Supply to gas-based power generation facilities.

7. Marketing and Retail:

The final stage involves marketing natural gas to end-users and managing customer relationships. This includes setting prices, billing, and customer service. For LNG, this may also involve regasification at the customer's site for industrial consumers.

8. Support Services:

Throughout the value chain, various support services are essential, including:

- Engineering and Construction: For infrastructure development.

- Technology and IT: For efficient operations and management of the gas network.

- Regulatory Compliance: Ensuring adherence to safety and environmental standards.

- Financial Services: For project financing and risk management.

The India Natural Gas and LNG Market value chain is characterized by significant investments in infrastructure, complex logistics, and the need for technological expertise. The integration of these various stages is crucial for ensuring a reliable and efficient supply of natural gas to meet India's growing energy needs.

Key Investment Insights in the India Natural Gas and LNG Market - Strategic investment recommendations

The India Natural Gas and LNG Market presents numerous investment opportunities, driven by the country's growing energy demand, government initiatives, and the shift towards cleaner fuels. This analysis provides key investment insights and strategic recommendations for potential investors in the market.

1. LNG Import Infrastructure:

Investment in LNG import terminals and associated infrastructure is a key opportunity. With India's increasing reliance on imported natural gas, there is a need for additional regasification capacity. Investors should consider opportunities in developing new LNG terminals, particularly on the eastern coast, to diversify import sources and reduce regional imbalances. Additionally, investments in FSRUs (Floating Storage and Regasification Units) can provide flexible and cost-effective solutions for LNG imports.

2. Pipeline Network Expansion:

Investments in natural gas pipeline infrastructure are crucial for creating a national gas grid and improving last-mile connectivity. Opportunities exist in developing cross-country pipelines to connect gas sources with consumption centers, as well as regional pipelines to feed into city gas distribution networks. Investors should focus on projects that enhance connectivity between LNG terminals, domestic gas fields, and major demand centers.

3. City Gas Distribution (CGD):

The government's initiative to expand CGD coverage across the country presents significant investment opportunities. Investors should consider entering new geographical areas as they are awarded by the regulatory authorities. Focus areas include developing pipeline networks, setting up CNG stations, and establishing LNG facilities for industries. Investments in digital technologies for efficient network management and customer service can provide a competitive edge in this segment.