Viral Vector and Plasmid DNA Manufacturing Market Overview - Definition, scope, and significance

Viral Vector and Plasmid DNA Manufacturing refers to the specialized biomanufacturing processes used to produce viral vectors and plasmid DNA for gene therapy, cell therapy, and vaccine development applications. This market encompasses the production of critical biological materials that serve as delivery vehicles for genetic material in advanced therapeutics. The significance of this market lies in its foundational role in the rapidly expanding field of gene therapy, where viral vectors act as vehicles to deliver therapeutic genes into target cells, while plasmid DNA serves as the genetic template for vector production and as a direct therapeutic agent in DNA vaccines. As the biotechnology and pharmaceutical industries continue to advance personalized medicine and targeted therapies, the Viral Vector and Plasmid DNA Manufacturing market has become increasingly essential for enabling cutting-edge treatments for previously incurable diseases.

Viral Vector and Plasmid DNA Manufacturing Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the Viral Vector and Plasmid DNA Manufacturing market include the growing prevalence of genetic disorders and cancer, increasing investment in gene therapy research, and the expanding pipeline of cell and gene therapy products. The COVID-19 pandemic has further accelerated demand for viral vector-based vaccines and therapies, creating unprecedented growth opportunities. However, the market faces several restraints including complex manufacturing processes, stringent regulatory requirements, and high production costs. Key challenges include scalability issues, limited manufacturing capacity, and the need for specialized expertise and infrastructure. Despite these obstacles, significant opportunities exist in the form of technological advancements in manufacturing processes, increasing outsourcing of production to contract development and manufacturing organizations (CDMOs), and the emergence of new therapeutic applications for viral vectors and plasmid DNA beyond traditional gene therapy.

Viral Vector and Plasmid DNA Manufacturing Market Growth Trends - Current and emerging trends shaping the market

The Viral Vector and Plasmid DNA Manufacturing market is experiencing several transformative growth trends that are reshaping the industry landscape. One of the most significant trends is the shift toward allogeneic cell therapies and off-the-shelf products, which requires scalable manufacturing solutions and has increased demand for viral vector production capacity. Another emerging trend is the development of novel viral vector platforms, including engineered AAV capsids and lentiviral vectors with improved targeting capabilities and reduced immunogenicity. The market is also witnessing a trend toward modular and flexible manufacturing facilities that can accommodate multiple products and production scales. Additionally, there is growing interest in continuous manufacturing processes and automation to improve efficiency and reduce costs. The integration of digital technologies, including artificial intelligence and machine learning for process optimization, represents another key trend that is expected to transform viral vector and plasmid DNA manufacturing in the coming years.

COVID-19 Impact on the Viral Vector and Plasmid DNA Manufacturing Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has had a profound impact on the Viral Vector and Plasmid DNA Manufacturing market, creating both challenges and opportunities. On the positive side, the pandemic has significantly accelerated the development and manufacturing of viral vector-based vaccines, particularly mRNA vaccines that require plasmid DNA as a critical starting material. This has led to increased investment in manufacturing capacity and capabilities across the industry. However, the pandemic also disrupted supply chains, delayed clinical trials, and created workforce challenges that affected production schedules. The market demonstrated remarkable resilience during this period, with many companies adapting their operations to maintain critical supply chains for ongoing therapies. Looking ahead, the recovery trajectory suggests sustained growth as the lessons learned during the pandemic have highlighted the importance of flexible, scalable manufacturing capabilities and robust supply chain management in the viral vector and plasmid DNA manufacturing sector.

Viral Vector and Plasmid DNA Manufacturing Market Competitive Landscape - Major competitors and market consolidation

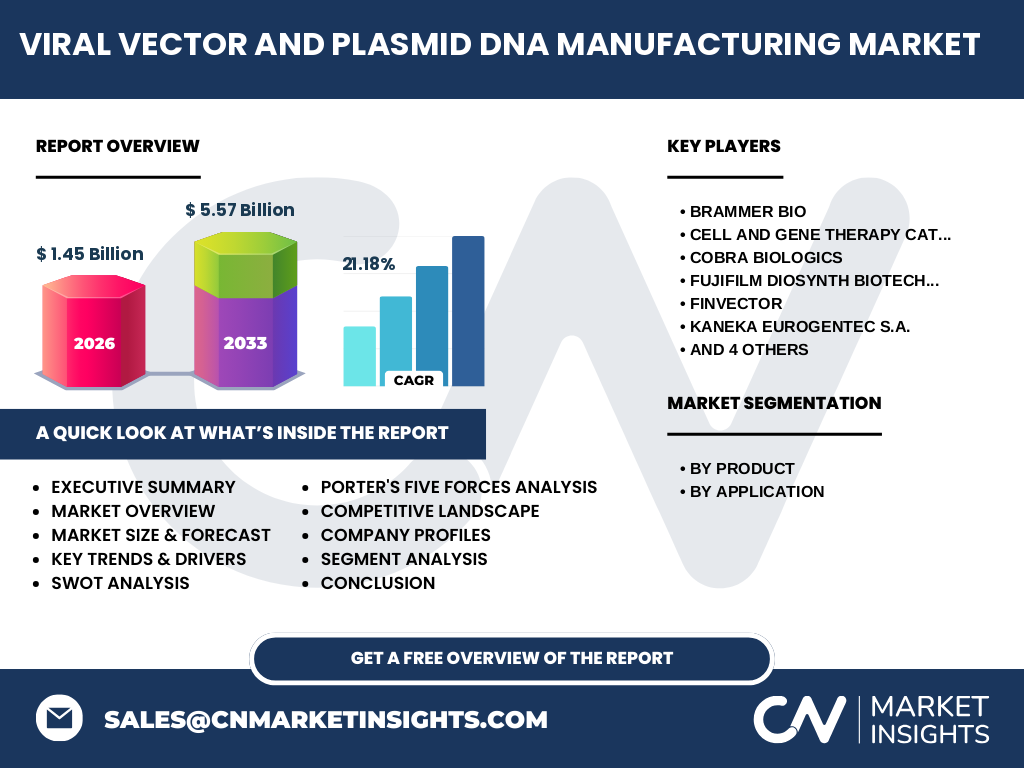

The Viral Vector and Plasmid DNA Manufacturing market features a competitive landscape characterized by a mix of specialized contract manufacturing organizations, large pharmaceutical companies with in-house capabilities, and innovative biotechnology firms. Key players in this market include Brammer Bio, Cell and Gene Therapy Catapult, Cobra Biologics, FUJIFILM Diosynth Biotechnologies, FinVector, Kaneka Eurogentec S.A., MassBiologics, Sanofi, Spark Therapeutics, and Uniqure. The competitive dynamics are shaped by ongoing market consolidation, with larger companies acquiring specialized CDMOs to expand their manufacturing capabilities and secure supply chains. This consolidation trend is driven by the increasing demand for viral vector and plasmid DNA manufacturing services and the need for companies to offer end-to-end solutions. Competition in the market is primarily based on manufacturing capacity, technical expertise, quality standards, and the ability to meet stringent regulatory requirements. Companies are also competing on their ability to offer innovative manufacturing solutions, including single-use technologies, continuous processing, and digital integration.

Executive Summary - High-level overview and key findings about Viral Vector and Plasmid DNA Manufacturing Market

The Viral Vector and Plasmid DNA Manufacturing market represents a critical segment of the biopharmaceutical industry, providing essential manufacturing services for advanced therapies. With a market size of $1.45 billion in 2026 and projected to reach $5.57 billion by 2033, the market is experiencing robust growth at a CAGR of 21.18%. This exceptional growth is driven by the expanding pipeline of gene therapies, increasing investment in cell and gene therapy research, and the growing demand for personalized medicine approaches. The market is segmented by product type into viral vectors and non-viral vectors, and by application into cancer, inherited disorders, and viral infections. Key findings indicate that the market is characterized by significant technological advancements, increasing outsourcing trends, and a competitive landscape featuring both specialized CDMOs and integrated pharmaceutical companies. The COVID-19 pandemic has further accelerated market growth by highlighting the importance of viral vector and plasmid DNA manufacturing capabilities for vaccine development and other therapeutic applications.

Viral Vector and Plasmid DNA Manufacturing Market Forecast - Projections for 2025-2032 period

The Viral Vector and Plasmid DNA Manufacturing market is projected to experience substantial growth during the 2025-2032 period, with the market size expected to increase from $1.45 billion in 2026 to $5.57 billion by 2033. This represents a compound annual growth rate of 21.18%, indicating strong and sustained market expansion over the forecast period. The growth trajectory is supported by several factors including the continued advancement of gene therapy technologies, increasing regulatory approvals for cell and gene therapy products, and growing investment in manufacturing infrastructure. The forecast period is expected to see significant capacity expansions, with many companies investing in new facilities and upgrading existing capabilities to meet rising demand. Additionally, technological innovations in manufacturing processes, including the adoption of single-use technologies and continuous manufacturing, are expected to drive efficiency improvements and cost reductions, further supporting market growth during this period.

Viral Vector and Plasmid DNA Manufacturing Market Size and Share by Segmentation - Breakdown by {segmentData}

The Viral Vector and Plasmid DNA Manufacturing market can be segmented by product type and application, with each segment contributing differently to the overall market size and share. By product, the market is divided into viral vectors and non-viral vectors, with viral vectors currently dominating due to their widespread use in gene therapy applications. Within viral vectors, adeno-associated viruses (AAV) represent the largest sub-segment, followed by lentiviral and retroviral vectors. By application, the market is segmented into cancer, inherited disorders, and viral infections. The cancer segment currently holds the largest market share, driven by the growing adoption of CAR-T cell therapies and other cell-based cancer treatments that require viral vector manufacturing. The inherited disorders segment is expected to experience the fastest growth during the forecast period, supported by the increasing number of gene therapies targeting rare genetic diseases. The viral infections segment, while currently smaller, has seen significant growth due to the COVID-19 pandemic and the development of viral vector-based vaccines.

Global Viral Vector and Plasmid DNA Manufacturing Market Size and Share by Region - Geographic distribution

The global Viral Vector and Plasmid DNA Manufacturing market exhibits distinct regional patterns in terms of market size and share, with North America currently representing the largest regional market. This dominance is attributed to the presence of major biotechnology hubs, significant research and development activities, and favorable regulatory frameworks in the United States and Canada. Europe represents the second-largest regional market, with countries like Germany, the UK, and Switzerland hosting numerous biotechnology companies and research institutions. The Asia-Pacific region is emerging as the fastest-growing market, driven by increasing investments in biotechnology infrastructure, growing research activities, and the expansion of contract manufacturing services. Countries such as China, Japan, and South Korea are particularly noteworthy for their rapid market growth. Latin America and the Middle East & Africa represent smaller but growing regional markets, with increasing adoption of advanced therapies and growing investments in healthcare infrastructure contributing to market expansion in these regions.

Regional Analysis of the Viral Vector and Plasmid DNA Manufacturing Market - Detailed regional market performance

Regional analysis of the Viral Vector and Plasmid DNA Manufacturing market reveals distinct performance characteristics across different geographic areas. In North America, the market is characterized by advanced manufacturing capabilities, strong research infrastructure, and significant investment from both private and public sectors. The region benefits from a well-established biotechnology ecosystem and favorable regulatory environment that supports innovation in gene therapy. Europe demonstrates strong market performance with a focus on collaborative research initiatives, particularly within the European Union framework. The region is notable for its emphasis on standardization and quality control in manufacturing processes. The Asia-Pacific region shows the most dynamic growth, with countries like China rapidly expanding their manufacturing capabilities and attracting international partnerships. This region is characterized by increasing government support for biotechnology development and growing domestic demand for advanced therapies. Emerging markets in Latin America and the Middle East & Africa are showing promising growth, though they face challenges related to infrastructure development and regulatory harmonization.

Leading Company Profiles in the Viral Vector and Plasmid DNA Manufacturing Market - Industry players and strategies

The Viral Vector and Plasmid DNA Manufacturing market features several leading companies that have established strong positions through various strategic approaches. Brammer Bio has positioned itself as a specialized CDMO with comprehensive viral vector manufacturing capabilities, focusing on end-to-end solutions for gene therapy developers. Cell and Gene Therapy Catapult serves as a unique organization bridging the gap between academia and industry, providing technical expertise and manufacturing capabilities to support the development of cell and gene therapies. Cobra Biologics has established itself as a global CDMO with extensive experience in biologics and viral vector manufacturing, offering scalable solutions across multiple platforms. FUJIFILM Diosynth Biotechnologies leverages its parent company's resources to provide integrated manufacturing solutions with a focus on quality and reliability. Kaneka Eurogentec S.A. specializes in plasmid DNA manufacturing and has expanded its capabilities to include viral vector production. These companies, along with others like MassBiologics, Sanofi, Spark Therapeutics, and Uniqure, are pursuing strategies that include capacity expansion, technological innovation, and strategic partnerships to strengthen their market positions.

Porter's Five Forces Analysis of the Viral Vector and Plasmid DNA Manufacturing Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the Viral Vector and Plasmid DNA Manufacturing market. The threat of new entrants is moderate due to the high capital requirements, complex regulatory environment, and need for specialized expertise, though increasing market opportunities are attracting new players. The bargaining power of buyers is relatively high given the specialized nature of these services and the limited number of qualified manufacturers, allowing customers to negotiate on price and terms. The bargaining power of suppliers is moderate, with suppliers of raw materials and specialized equipment having some influence, though established manufacturers often have long-term supplier relationships. The threat of substitutes is low as viral vectors and plasmid DNA have unique properties essential for gene therapy applications, with few viable alternatives. Competitive rivalry is intense, characterized by ongoing capacity expansions, technological innovations, and strategic acquisitions as companies compete for market share in this growing industry.

SWOT Analysis of the Viral Vector and Plasmid DNA Manufacturing Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Viral Vector and Plasmid DNA Manufacturing market reveals several key factors shaping the industry landscape. Strengths of the market include the growing demand for advanced therapies, technological advancements in manufacturing processes, and the increasing number of gene therapy approvals. Weaknesses include the complexity of manufacturing processes, high production costs, and scalability challenges that limit capacity expansion. Opportunities in the market are abundant, including the development of novel viral vector platforms, expansion into new therapeutic areas, and the increasing adoption of automation and digital technologies in manufacturing. Threats to the market include stringent regulatory requirements that can delay product approvals, potential supply chain disruptions, and the risk of manufacturing failures that could impact product quality and patient safety. Additionally, the market faces competitive pressures from both established players and new entrants seeking to capitalize on the growing demand for viral vector and plasmid DNA manufacturing services.

Viral Vector and Plasmid DNA Manufacturing Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the Viral Vector and Plasmid DNA Manufacturing market reveals a complex ecosystem involving multiple stakeholders and processes. The value chain begins with research and development activities, where innovative therapies are designed and initial manufacturing processes are developed. This is followed by the supply of raw materials and components, including cell lines, media, and specialized equipment necessary for production. The core manufacturing activities involve upstream processes such as cell culture and vector production, downstream processes including purification and formulation, and quality control testing to ensure product safety and efficacy. Contract manufacturing organizations play a crucial role in the value chain by providing specialized manufacturing services to therapy developers. The value chain also includes regulatory affairs and compliance activities, which are essential for obtaining necessary approvals. Finally, the distribution and delivery of manufactured products to clinical and commercial customers completes the value chain, with logistics and cold chain management being critical components for maintaining product integrity.

Key Investment Insights in the Viral Vector and Plasmid DNA Manufacturing Market - Strategic investment recommendations

Key investment insights in the Viral Vector and Plasmid DNA Manufacturing market suggest several strategic opportunities for investors and companies looking to enter or expand in this sector. Investment in manufacturing capacity expansion is particularly attractive given the projected market growth and increasing demand for viral vector and plasmid DNA production services. Companies should consider investing in flexible manufacturing platforms that can accommodate multiple product types and scales, as this versatility is increasingly valued by customers. Technological investments in automation, continuous manufacturing processes, and digital integration represent another key opportunity, as these innovations can significantly improve efficiency and reduce costs. Strategic partnerships and acquisitions are recommended for companies seeking to rapidly expand their capabilities or enter new geographic markets. Additionally, investments in talent development and specialized expertise are crucial given the complex nature of viral vector and plasmid DNA manufacturing. Finally, investors should consider the growing importance of sustainability in manufacturing operations, with investments in energy-efficient processes and waste reduction strategies becoming increasingly important.

Viral Vector and Plasmid DNA Manufacturing Market Conclusion - Summary and key takeaways

The Viral Vector and Plasmid DNA Manufacturing market represents a dynamic and rapidly growing segment of the biopharmaceutical industry, with a projected market size increase from $1.45 billion in 2026 to $5.57 billion by 2033, representing a CAGR of 21.18%. The market is driven by the expanding gene therapy pipeline, increasing investment in cell and gene therapy research, and the growing demand for personalized medicine approaches. Key takeaways from this analysis include the importance of manufacturing capacity expansion to meet rising demand, the critical role of technological innovation in improving efficiency and reducing costs, and the competitive dynamics characterized by both specialized CDMOs and integrated pharmaceutical companies. The COVID-19 pandemic has accelerated market growth by highlighting the importance of viral vector and plasmid DNA manufacturing capabilities for vaccine development and other therapeutic applications. As the market continues to evolve, companies that can offer flexible, scalable, and high-quality manufacturing solutions while navigating complex regulatory requirements will be best positioned for success in this promising industry.

Research Methodology - How this research was conducted

The research methodology employed for this Viral Vector and Plasmid DNA Manufacturing market analysis combines multiple approaches to ensure comprehensive and accurate insights. Primary research involved interviews with industry experts, including executives from manufacturing companies, regulatory affairs specialists, and biotechnology researchers, to gather firsthand perspectives on market dynamics and trends. Secondary research encompassed a thorough review of industry reports, scientific publications, company financial statements, and regulatory filings to validate findings and provide quantitative context. Market size and growth projections were developed using a combination of bottom-up and top-down approaches, analyzing data from individual market segments and extrapolating to the total market. The research also incorporated competitive analysis frameworks to assess the positioning of key players and identify emerging trends. Data triangulation was employed to cross-verify information from multiple sources, ensuring the reliability of the findings presented in this report.

Research Scope - Coverage and limitations

The research scope for this Viral Vector and Plasmid DNA Manufacturing market analysis encompasses a comprehensive examination of the global market, including market size, growth projections, competitive landscape, and key trends from 2025 to 2033. The analysis covers major geographic regions, including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with a focus on the most significant markets in each region. The research examines market segmentation by product type (viral vectors and non-viral vectors) and application (cancer, inherited disorders, and viral infections), providing detailed insights into each segment's performance and growth prospects. While the research aims to provide a thorough analysis of the market, it is important to note certain limitations, including the availability of public data for some smaller market segments and the potential for rapid technological changes that could impact market dynamics. Additionally, the analysis focuses on commercial aspects of the market and may not capture all nuances of academic or research-focused manufacturing activities.

Key Companies and Recent Developments in the Viral Vector and Plasmid DNA Manufacturing Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Viral Vector and Plasmid DNA Manufacturing market features several key companies that have recently announced significant developments shaping the industry landscape. Brammer Bio, now part of Thermo Fisher Scientific, has expanded its manufacturing capacity with new facilities in Florida and Massachusetts to meet growing demand for viral vector production. Cell and Gene Therapy Catapult has launched several initiatives to support the UK's cell and gene therapy industry, including the opening of new manufacturing facilities and the development of industry standards. Cobra Biologics has announced capacity expansions and new service offerings to support the growing gene therapy market. FUJIFILM Diosynth Biotechnologies has invested in new manufacturing capabilities and entered into strategic partnerships to enhance its viral vector production capacity. Kaneka Eurogentec S.A. has expanded its plasmid DNA manufacturing capabilities and entered into supply agreements with leading gene therapy developers. Sanofi has strengthened its position in the market through acquisitions and investments in manufacturing infrastructure. Spark Therapeutics, now part of Roche, continues to advance its gene therapy pipeline while maintaining manufacturing capabilities. Uniqure has expanded its manufacturing capacity to support the commercial launch of its gene therapies. These companies, along with other market participants, are actively pursuing strategies including capacity expansion, technological innovation, and strategic partnerships to strengthen their market positions and meet the growing demand for viral vector and plasmid DNA manufacturing services.