Cellular IoT Market Overview - Definition, scope, and significance

The Cellular IoT (Internet of Things) market represents a transformative technology ecosystem that connects physical devices, vehicles, appliances, and other items through cellular networks, enabling them to exchange data and perform intelligent functions without human intervention. This market encompasses the deployment of cellular technologies specifically designed for IoT applications, including 2G, 3G, 4G LTE, LTE-M, NB-IoT, and 5G networks, which provide the connectivity backbone for billions of connected devices worldwide. The significance of this market lies in its ability to revolutionize industries by enabling real-time monitoring, predictive maintenance, automation, and data-driven decision-making across sectors such as healthcare, manufacturing, transportation, energy, and smart cities. As businesses increasingly seek to optimize operations, reduce costs, and enhance customer experiences, cellular IoT solutions offer unprecedented opportunities for innovation and efficiency gains.

Cellular IoT Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The cellular IoT market is propelled by several key drivers including the rapid proliferation of connected devices, increasing demand for real-time data analytics, and the growing adoption of Industry 4.0 principles across manufacturing sectors. The rollout of 5G networks presents significant opportunities for ultra-reliable low-latency communication, enabling new use cases in autonomous vehicles, remote surgery, and industrial automation. However, the market faces restraints such as high initial infrastructure costs, security and privacy concerns, and the complexity of managing large-scale IoT deployments. Challenges include ensuring interoperability between different cellular technologies, addressing power consumption issues for battery-operated devices, and navigating regulatory compliance across different regions. Despite these obstacles, opportunities abound in emerging markets, the development of edge computing solutions, and the integration of artificial intelligence with cellular IoT systems to create more intelligent and autonomous networks.

Cellular IoT Market Growth Trends - Current and emerging trends shaping the market

The cellular IoT market is experiencing several transformative growth trends that are reshaping the technological landscape. One prominent trend is the shift toward low-power wide-area (LPWA) technologies such as LTE-M and NB-IoT, which offer extended battery life and improved coverage for IoT devices. Another significant trend is the convergence of cellular IoT with cloud computing and edge processing, enabling faster data analysis and reduced latency. The market is also witnessing increased adoption of private 5G networks for industrial applications, providing dedicated connectivity with enhanced security and reliability. Additionally, the integration of artificial intelligence and machine learning algorithms with cellular IoT platforms is enabling predictive analytics and autonomous decision-making capabilities. The emergence of smart city initiatives worldwide is driving demand for cellular IoT solutions in areas such as intelligent transportation systems, environmental monitoring, and public safety applications.

COVID-19 Impact on the Cellular IoT Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the cellular IoT market, initially causing supply chain disruptions, project delays, and reduced capital expenditure across industries. However, the pandemic also accelerated digital transformation initiatives, leading to increased adoption of remote monitoring and automation solutions. Healthcare applications saw significant growth, with cellular IoT enabling remote patient monitoring, telemedicine, and contactless temperature screening. The manufacturing sector experienced a surge in demand for predictive maintenance and asset tracking solutions to minimize downtime and ensure operational continuity. As businesses adapted to new working models, the need for reliable connectivity and real-time data exchange became more critical than ever. The market is now on a recovery trajectory, with pent-up demand driving renewed investment in cellular IoT infrastructure and applications across various sectors.

Cellular IoT Market Competitive Landscape - Major competitors and market consolidation

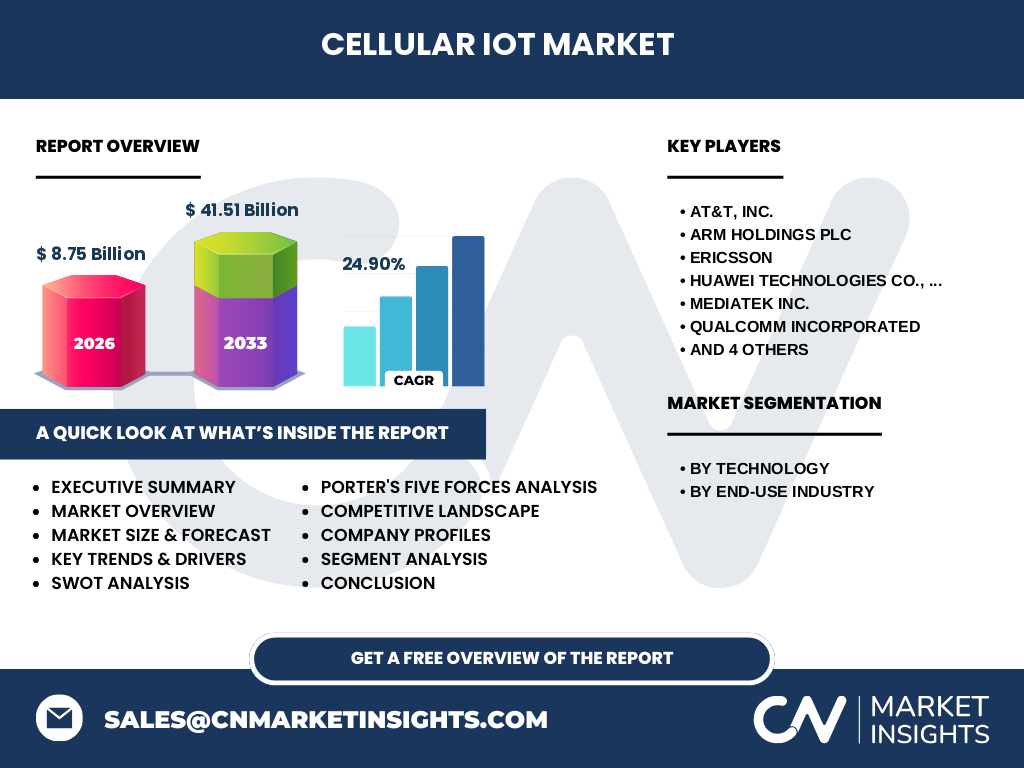

The cellular IoT market features a competitive landscape characterized by a mix of established telecommunications giants, semiconductor manufacturers, and specialized IoT solution providers. Major players such as AT&T, Ericsson, and Huawei Technologies Co., Ltd. leverage their extensive network infrastructure and global presence to offer comprehensive cellular IoT solutions. Semiconductor companies like Qualcomm Incorporated and Mediatek Inc. focus on developing advanced chipsets and modules that enable efficient IoT connectivity. The market is witnessing increased consolidation through strategic partnerships, mergers, and acquisitions as companies seek to expand their technological capabilities and market reach. For instance, Sierra Wireless, Inc. and Sequans Communications SA specialize in providing IoT-specific hardware and software solutions, while Thales Group offers security-focused IoT applications. This competitive environment is driving innovation and pushing companies to differentiate through value-added services, vertical-specific solutions, and enhanced security features.

Executive Summary - High-level overview and key findings about Cellular IoT Market

The cellular IoT market is poised for exponential growth, with the market size projected to expand from 8.75 billion in 2026 to 41.51 billion by 2033, representing a remarkable compound annual growth rate of 24.90%. This growth is fueled by the increasing adoption of connected devices across industries, the rollout of advanced cellular technologies, and the growing demand for real-time data analytics and automation. The market is segmented by technology, with 5G emerging as a key enabler for next-generation IoT applications, and by end-use industry, with industrial applications leading the adoption curve. The competitive landscape is characterized by a diverse ecosystem of players ranging from telecommunications providers to semiconductor manufacturers, each contributing to the market's innovation and expansion. As the market continues to evolve, key trends such as the adoption of LPWA technologies, the integration of AI and edge computing, and the development of smart city initiatives are expected to shape the future of cellular IoT.

Cellular IoT Market Forecast - Projections for 2025-2032 period

The cellular IoT market is projected to experience robust growth throughout the 2025-2032 period, with the market size expected to increase from 8.75 billion in 2026 to 41.51 billion by 2033. This represents a compound annual growth rate of 24.90%, indicating strong momentum and sustained demand for cellular IoT solutions. The forecast period is expected to be characterized by the widespread deployment of 5G networks, which will unlock new use cases and applications for IoT devices. The industrial sector is anticipated to remain the largest end-use segment, driven by the ongoing digital transformation of manufacturing processes and the adoption of Industry 4.0 principles. The infrastructure & construction, automotive & transportation, and energy & utilities sectors are also expected to show significant growth, as cellular IoT solutions enable more efficient operations and enhanced service delivery. Geographically, while North America and Europe are expected to maintain their leadership positions, the Asia-Pacific region is projected to exhibit the highest growth rate, driven by rapid industrialization and smart city initiatives in countries such as China, India, and Japan.

Cellular IoT Market Size and Share by Segmentation - Breakdown by {segmentData}

The cellular IoT market is segmented by technology and end-use industry, each contributing uniquely to the overall market size and share. In terms of technology, 4G currently dominates the market due to its widespread availability and mature ecosystem, but LTE-M and NB-IoT are rapidly gaining traction for their low-power, wide-area capabilities. The 5G segment, while currently smaller, is expected to show the highest growth rate as networks expand and new use cases emerge. By end-use industry, the industrial sector holds the largest market share, driven by applications in manufacturing, logistics, and asset tracking. The automotive & transportation industry is another significant segment, leveraging cellular IoT for connected vehicles, fleet management, and smart transportation systems. Healthcare, energy & utilities, and retail are also key segments, each utilizing cellular IoT for specific applications such as remote patient monitoring, smart grid management, and inventory tracking. The consumer electronics segment, while smaller, is growing rapidly with the proliferation of smart home devices and wearables.

Global Cellular IoT Market Size and Share by Region - Geographic distribution

The global cellular IoT market exhibits varying growth patterns and adoption rates across different regions, influenced by factors such as technological infrastructure, regulatory environment, and industry focus. North America currently leads the market, driven by advanced telecommunications infrastructure, high technology adoption rates, and a strong presence of key industry players. The region's focus on smart city initiatives and industrial automation further contributes to its market dominance. Europe follows closely, with countries like Germany, the UK, and France investing heavily in Industry 4.0 and IoT applications. The Asia-Pacific region is expected to show the highest growth rate during the forecast period, fueled by rapid industrialization, expanding telecommunications networks, and government initiatives in countries such as China, Japan, and South Korea. China, in particular, is emerging as a major player in the cellular IoT market, with significant investments in 5G infrastructure and smart manufacturing. Latin America and the Middle East & Africa regions, while currently smaller markets, are expected to see steady growth as telecommunications infrastructure improves and industries increasingly adopt IoT solutions.

Regional Analysis of the Cellular IoT Market - Detailed regional market performance

A detailed regional analysis of the cellular IoT market reveals distinct characteristics and growth drivers in each geographic area. In North America, the market is characterized by early adoption of advanced technologies, strong venture capital funding for IoT startups, and a focus on smart city initiatives. The region's emphasis on industrial automation and connected vehicles is driving significant demand for cellular IoT solutions. Europe's market is shaped by stringent data privacy regulations, which influence the development of secure IoT applications, and a strong automotive industry that is pioneering connected car technologies. The Asia-Pacific region presents a diverse landscape, with China leading in 5G deployment and smart manufacturing, Japan focusing on robotics and automation, and India emerging as a hub for IoT innovation in agriculture and smart cities. Latin America is seeing growing adoption in smart metering and fleet management applications, while the Middle East & Africa region is investing in IoT for oil & gas monitoring and smart city projects in countries like the UAE and Saudi Arabia.

Leading Company Profiles in the Cellular IoT Market - Industry players and strategies

The cellular IoT market features several leading companies, each with distinct strategies and areas of expertise. AT&T, Inc. leverages its extensive network infrastructure to offer comprehensive IoT solutions, focusing on vertical-specific applications and partnerships with device manufacturers. Arm Holdings Plc specializes in designing energy-efficient processors and connectivity solutions for IoT devices, enabling longer battery life and improved performance. Ericsson is at the forefront of 5G technology development, providing network infrastructure and IoT platforms that support massive device connectivity. Huawei Technologies Co., Ltd. offers end-to-end IoT solutions, from chipsets to cloud platforms, with a strong focus on 5G and smart city applications. Qualcomm Incorporated develops advanced modems and processors for IoT devices, emphasizing low power consumption and high performance. Mediatek Inc. targets the mass market with cost-effective IoT solutions, while Sequans Communications SA specializes in LTE chips for IoT applications. Sierra Wireless, Inc. provides hardware and software solutions for IoT connectivity, and ZTE Corporation offers a range of IoT products and services, particularly in the Asia-Pacific region.

Porter's Five Forces Analysis of the Cellular IoT Market - Competitive forces assessment

Porter's Five Forces analysis of the cellular IoT market reveals a dynamic competitive landscape. The threat of new entrants is moderate, as the market requires significant capital investment in technology development and network infrastructure, but the growing demand for IoT solutions is attracting new players. The bargaining power of suppliers, primarily semiconductor manufacturers and network equipment providers, is relatively high due to the specialized nature of IoT components and the limited number of suppliers capable of meeting the industry's technical requirements. Buyers, including enterprises and government agencies, have moderate bargaining power, as they can choose from a range of solutions but are often locked into specific ecosystems once deployed. The threat of substitutes is low, as cellular IoT offers unique advantages in terms of coverage, reliability, and security compared to alternative connectivity technologies. Competitive rivalry is intense, with major players competing on technology innovation, pricing, and vertical-specific solutions. The market is also influenced by the threat of new regulations and standards, which can impact the development and deployment of cellular IoT solutions.

SWOT Analysis of the Cellular IoT Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the cellular IoT market reveals several key factors influencing its growth and development. The market's strengths include the widespread availability of cellular networks, the ability to provide reliable and secure connectivity over long distances, and the continuous advancement of cellular technologies such as 5G. However, weaknesses such as high power consumption in some applications, the complexity of managing large-scale IoT deployments, and the need for specialized expertise in IoT development pose challenges to market growth. Opportunities abound in emerging markets, the development of new use cases enabled by 5G, and the integration of AI and edge computing with cellular IoT solutions. Threats to the market include cybersecurity risks, regulatory challenges related to data privacy and cross-border data flows, and the potential for market saturation in some application areas. Additionally, the market faces the challenge of ensuring interoperability between different cellular technologies and addressing the skills gap in IoT development and management.

Cellular IoT Market Value Chain Analysis - Industry structure and value flow

The cellular IoT market value chain consists of several interconnected stages, each contributing to the development and deployment of IoT solutions. At the foundation are semiconductor manufacturers and component suppliers, who provide the essential building blocks such as processors, modems, and sensors. Network equipment providers and telecommunications companies form the next layer, offering the infrastructure and connectivity services that enable IoT devices to communicate. IoT platform providers offer the software and services needed to manage, analyze, and secure IoT data and devices. System integrators and solution providers combine these elements to create end-to-end IoT solutions tailored to specific industries and applications. At the top of the value chain are the end-users, including enterprises, government agencies, and consumers, who deploy and utilize IoT solutions to achieve their business or personal objectives. The value chain is characterized by complex relationships and partnerships, with companies often operating at multiple levels to provide comprehensive solutions. The flow of value is driven by the increasing demand for data-driven insights and automation across industries, with each layer of the value chain adding functionality and value to the overall IoT solution.

Key Investment Insights in the Cellular IoT Market - Strategic investment recommendations

The cellular IoT market presents several compelling investment opportunities for stakeholders looking to capitalize on the growing demand for connected solutions. Strategic investments in 5G infrastructure and LPWA technologies such as LTE-M and NB-IoT are likely to yield significant returns as these technologies enable new use cases and expand the addressable market for cellular IoT. Investors should also consider opportunities in IoT security solutions, as the increasing number of connected devices creates a growing need for robust cybersecurity measures. The development of edge computing and AI-powered analytics for IoT data represents another promising area for investment, enabling faster decision-making and more intelligent IoT applications. Vertical-specific solutions in industries such as healthcare, automotive, and smart cities offer targeted investment opportunities with high growth potential. Additionally, investments in companies developing energy-efficient IoT devices and solutions for extending battery life could address one of the key challenges in the market. Strategic partnerships and acquisitions to build comprehensive IoT ecosystems and expand geographic presence are also recommended for companies looking to strengthen their market position.

Cellular IoT Market Conclusion - Summary and key takeaways

The cellular IoT market is on a trajectory of rapid growth and transformation, driven by the increasing demand for connected devices, the rollout of advanced cellular technologies, and the growing adoption of IoT solutions across industries. With a projected compound annual growth rate of 24.90%, the market is expected to expand significantly from 8.75 billion in 2026 to 41.51 billion by 2033. The market is characterized by a diverse ecosystem of players, ranging from telecommunications giants to specialized IoT solution providers, each contributing to the innovation and expansion of the market. Key trends such as the adoption of LPWA technologies, the integration of AI and edge computing, and the development of smart city initiatives are shaping the future of cellular IoT. While the market faces challenges such as security concerns and the complexity of large-scale deployments, the opportunities for growth and innovation are substantial. As industries continue to embrace digital transformation, cellular IoT solutions are poised to play a crucial role in enabling more efficient, intelligent, and connected operations across the globe.

Research Methodology - How this research was conducted

The research for this cellular IoT market report was conducted using a comprehensive methodology that combines both primary and secondary research techniques. Primary research involved interviews with industry experts, including executives from leading cellular IoT companies, technology developers, and end-users across various sectors. These interviews provided valuable insights into market trends, challenges, and future outlook. Secondary research encompassed a thorough analysis of industry reports, company financial statements, press releases, and relevant publications from reputable sources such as industry associations, government agencies, and academic institutions. Market size and growth projections were derived using a combination of top-down and bottom-up approaches, considering factors such as technology adoption rates, industry growth trends, and regional economic indicators. The research also incorporated data triangulation to validate findings and ensure accuracy. The report's scope was defined to cover key market segments, including technology types and end-use industries, as well as major geographic regions. Limitations of the research include the rapidly evolving nature of the cellular IoT market and the potential for unforeseen technological or regulatory changes that could impact future growth projections.

Research Scope - Coverage and limitations

The research scope for this cellular IoT market report encompasses a comprehensive analysis of the market's current state and future projections, covering key segments such as technology types (2G & 3G, 4G, LTE-M, NB-IoT, and 5G) and end-use industries (industrial, infrastructure & construction, retail, consumer electronics, automotive & transportation, energy & utilities, and healthcare). The report provides a global perspective, analyzing market performance across major regions including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The research timeframe extends from historical data to projections through 2033, with a particular focus on the 2025-2032 period. The scope includes an analysis of market drivers, restraints, challenges, and opportunities, as well as a competitive landscape assessment of key players in the industry. However, the research has certain limitations, including the potential for rapid technological changes that could alter market dynamics, the impact of regulatory changes on market growth, and the difficulty in obtaining precise data for certain emerging applications and regions. Additionally, the scope does not extend to non-cellular IoT technologies such as Wi-Fi or Bluetooth-based solutions, focusing specifically on cellular connectivity.

Key Companies and Recent Developments in the Cellular IoT Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The cellular IoT market is characterized by the presence of several key companies, each driving innovation and shaping the industry through strategic developments and partnerships. AT&T, Inc. has been focusing on expanding its IoT platform capabilities and has recently announced partnerships with leading device manufacturers to enhance its IoT ecosystem. The company has also been investing in 5G infrastructure to support next-generation IoT applications. Arm Holdings Plc has introduced new energy-efficient processor designs specifically tailored for IoT devices, aiming to extend battery life and improve performance. Ericsson has been at the forefront of 5G technology development, with recent announcements of advanced network slicing capabilities for IoT applications and partnerships with cloud providers to enhance edge computing solutions. Huawei Technologies Co., Ltd. continues to expand its IoT product portfolio, with recent launches of integrated 5G and IoT chipsets designed for smart city applications. Qualcomm Incorporated has introduced new 5G modem-RF systems optimized for IoT devices, enabling faster data rates and lower latency. Mediatek Inc. has announced the development of cost-effective IoT solutions targeting emerging markets, while Sequans Communications SA has launched new LTE chips with enhanced power management features for battery-operated IoT devices. Sierra Wireless, Inc. has been focusing on providing comprehensive IoT connectivity solutions, with recent partnerships to expand its global network coverage. Thales Group has introduced advanced IoT security solutions, addressing the growing concern for data protection in connected devices. ZTE Corporation has been investing in 5G and IoT integration, with recent announcements of smart manufacturing solutions leveraging cellular IoT technology.