Low GWP Refrigerants Market Overview - Definition, scope, and significance

Low GWP (Global Warming Potential) refrigerants represent a critical advancement in cooling technology, designed to minimize environmental impact while maintaining efficient thermal performance. These refrigerants are specifically engineered to have significantly lower GWP values compared to traditional hydrofluorocarbons (HFCs) and other high-impact compounds. The scope of this market encompasses various applications including heat pumps, air conditioning systems, and refrigeration units across residential, commercial, and industrial sectors. The significance of low GWP refrigerants lies in their ability to address global climate concerns while meeting the growing demand for cooling solutions in an increasingly warming world. As regulatory frameworks tighten around high-GWP substances and environmental awareness grows, these alternative refrigerants have become essential for sustainable development in the HVAC and refrigeration industries.

Low GWP Refrigerants Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers propelling the low GWP refrigerants market include stringent environmental regulations phasing out high-GWP substances, increasing awareness of climate change impacts, and technological advancements in refrigerant chemistry. Government mandates such as the Kigali Amendment to the Montreal Protocol and regional regulations like the EU F-Gas Regulation are compelling industries to transition toward sustainable alternatives. However, the market faces several restraints including higher initial costs compared to conventional refrigerants, technical challenges in retrofitting existing systems, and safety concerns with some low-GWP alternatives that may be flammable or toxic. Key challenges involve the need for specialized training for technicians, infrastructure development for new refrigerant handling, and ensuring compatibility with existing equipment. Despite these obstacles, significant opportunities exist in emerging markets where cooling demand is rapidly growing, innovations in natural refrigerants like CO2 and ammonia, and the development of next-generation synthetic alternatives with optimal performance characteristics.

Low GWP Refrigerants Market Growth Trends - Current and emerging trends shaping the market

The low GWP refrigerants market is experiencing several transformative growth trends that are reshaping the industry landscape. A notable trend is the accelerated adoption of natural refrigerants such as hydrocarbons (propane, isobutane), ammonia, and carbon dioxide, which offer extremely low GWP values and excellent thermodynamic properties. Another emerging trend is the development of hydrofluoroolefins (HFOs) and HFO blends, which provide a balance between low environmental impact and improved safety profiles compared to traditional HFCs. The market is also witnessing increased investment in research and development to create next-generation refrigerants with even lower GWP values, improved energy efficiency, and enhanced safety characteristics. Additionally, there is a growing trend toward integrated cooling solutions that combine low GWP refrigerants with energy-efficient components and smart controls to maximize overall system performance and sustainability. The shift toward circular economy principles is also influencing the market, with increased focus on refrigerant reclamation, recycling, and recovery to minimize waste and environmental impact.

COVID-19 Impact on the Low GWP Refrigerants Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the low GWP refrigerants market through supply chain interruptions, manufacturing slowdowns, and reduced demand from key end-use industries such as commercial refrigeration and automotive air conditioning. Lockdowns and economic uncertainties led to project delays and postponed investments in new cooling systems, particularly in the commercial and industrial sectors. However, the pandemic also highlighted the critical importance of refrigeration for vaccine storage and distribution, potentially accelerating investments in reliable cooling infrastructure. As economies recover, the market is experiencing a rebound driven by pent-up demand, renewed focus on sustainability in post-pandemic recovery plans, and the continued implementation of environmental regulations that were temporarily relaxed during the crisis. The recovery trajectory suggests a return to pre-pandemic growth rates, with an accelerated transition toward low GWP solutions as industries prioritize resilience and environmental compliance in their rebuilding efforts.

Low GWP Refrigerants Market Competitive Landscape - Major competitors and market consolidation

The competitive landscape of the low GWP refrigerants market features a mix of established chemical manufacturers and specialized refrigerant producers competing for market share in this rapidly evolving sector. Major players such as Honeywell International Inc., The Chemours Company, and Arkema Inc. are leveraging their extensive research capabilities and global distribution networks to maintain leadership positions. These companies are investing heavily in developing innovative low GWP solutions and expanding their product portfolios to address diverse application requirements. The market is characterized by strategic partnerships between refrigerant manufacturers and equipment producers to ensure compatibility and optimize system performance. While some consolidation has occurred through mergers and acquisitions, the market remains relatively fragmented with numerous regional players offering specialized solutions. Competition is intensifying as companies differentiate themselves through technological innovation, sustainability credentials, and comprehensive service offerings including training and technical support for the safe handling of new refrigerant types.

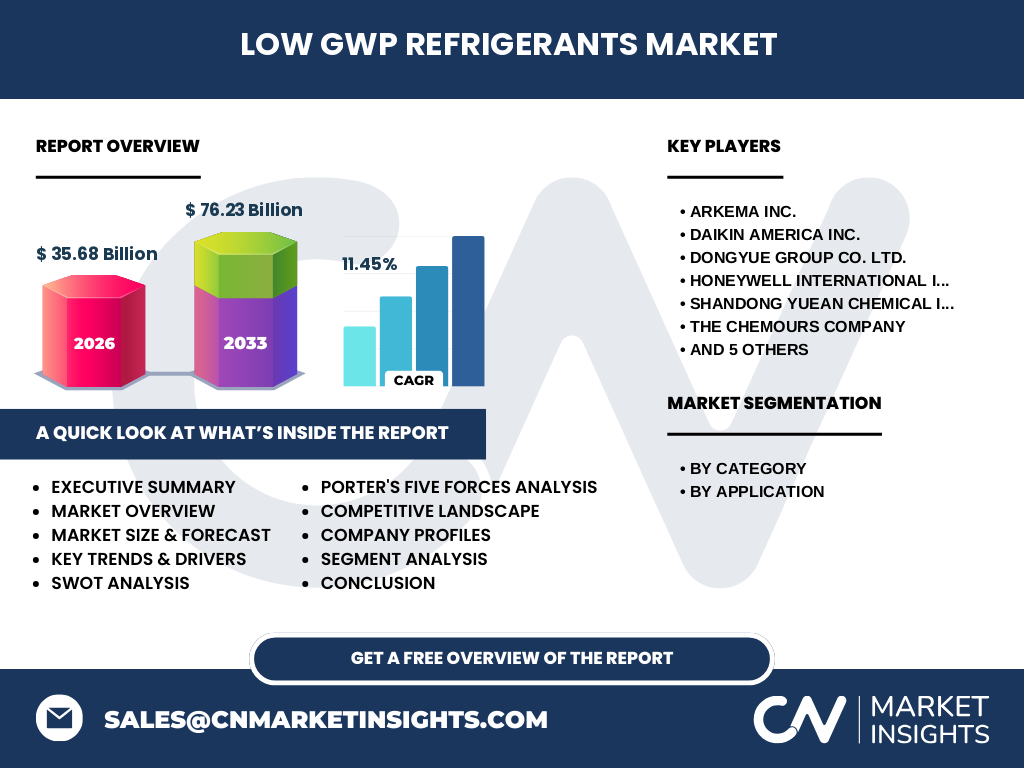

Executive Summary - High-level overview and key findings about Low GWP Refrigerants Market

The low GWP refrigerants market represents a dynamic and rapidly growing sector driven by urgent environmental imperatives and supportive regulatory frameworks. With a market size of 35.68 billion in 2026 and projected to reach 76.23 billion by 2033, the industry is experiencing robust growth at a CAGR of 11.45%. This expansion reflects the accelerating transition away from high-GWP refrigerants toward sustainable alternatives across all major application segments including heat pumps, air conditioning, and refrigeration. The market is characterized by technological innovation, with natural refrigerants and advanced synthetic alternatives gaining traction alongside traditional options. While challenges exist in terms of cost, safety, and implementation, the overall trajectory points toward sustained growth as environmental regulations tighten and end-users increasingly prioritize sustainability. The competitive landscape features both global chemical giants and specialized players, with success increasingly dependent on innovation capabilities, regulatory compliance, and comprehensive service offerings.

Low GWP Refrigerants Market Forecast - Projections for 2025-2032 period

The low GWP refrigerants market is poised for substantial growth between 2025 and 2032, with the industry expected to expand from its 2026 valuation of 35.68 billion to reach 76.23 billion by 2033. This represents a compound annual growth rate of 11.45%, reflecting the accelerating momentum behind sustainable cooling solutions. The forecast period will likely see continued strong demand across all application segments, with heat pumps emerging as a particularly dynamic area due to their role in energy-efficient heating and cooling. Air conditioning systems are expected to maintain their dominant position in the market, driven by increasing global temperatures and rising living standards in developing regions. The refrigeration segment will benefit from growing cold chain infrastructure and food safety requirements. Geographically, while developed regions will continue to lead in adoption rates, emerging markets in Asia, Africa, and Latin America will represent significant growth opportunities as they upgrade aging infrastructure and implement new cooling systems with low GWP refrigerants as the standard.

Low GWP Refrigerants Market Size and Share by Segmentation - Breakdown by {segmentData}

The low GWP refrigerants market segmentation reveals distinct patterns across categories and applications. By category, the market is divided between natural and synthetic refrigerants, with natural options including CO2, ammonia, and hydrocarbons gaining market share due to their extremely low GWP values and improving safety profiles. Synthetic refrigerants, particularly HFOs and their blends, continue to play a significant role by offering a balance between environmental performance and practical handling characteristics. In terms of applications, heat pumps represent a rapidly growing segment as these systems become increasingly important for both heating and cooling in the context of energy efficiency and decarbonization efforts. The air conditioning segment maintains the largest market share, driven by residential, commercial, and automotive applications where cooling demand continues to rise globally. Refrigeration applications, encompassing everything from domestic refrigerators to industrial cold storage, represent another substantial segment benefiting from food safety regulations and the expanding cold chain infrastructure necessary for modern food distribution and pharmaceutical storage.

Global Low GWP Refrigerants Market Size and Share by Region - Geographic distribution

The global low GWP refrigerants market exhibits varying adoption rates and growth dynamics across different regions, influenced by regulatory frameworks, economic development, and climate conditions. Developed regions including North America and Europe lead in market penetration, driven by stringent environmental regulations and strong sustainability commitments. These regions have implemented comprehensive phase-down schedules for high-GWP refrigerants, creating a robust market for alternatives. The Asia-Pacific region represents the largest market by volume, propelled by rapid industrialization, urbanization, and the expansion of cooling infrastructure in countries like China, India, and Southeast Asian nations. This region is also experiencing the fastest growth rates as governments implement environmental policies and industries upgrade to compliant systems. Latin America and the Middle East & Africa regions are showing increasing adoption, though at varying paces influenced by economic factors and regulatory maturity. Overall, while developed markets continue to innovate and set standards, emerging economies represent the most significant growth opportunities as they build out their cooling infrastructure with sustainable technologies.

Regional Analysis of the Low GWP Refrigerants Market - Detailed regional market performance

Regional analysis of the low GWP refrigerants market reveals distinct performance characteristics shaped by local factors. In North America, the market is driven by federal regulations like the AIM Act and state-level initiatives, with a strong emphasis on HFO technologies and natural refrigerants in commercial applications. Europe leads in regulatory stringency with the F-Gas Regulation creating a clear phase-down pathway, resulting in the highest penetration rates of low GWP solutions and significant investment in natural refrigerant technologies. The Asia-Pacific region presents a complex landscape where rapid economic growth and increasing cooling demand create substantial market opportunities, though adoption rates vary significantly by country depending on regulatory frameworks and economic priorities. China, as the world's largest cooling market, is implementing its own regulations while balancing industrial competitiveness. In Latin America, market growth is influenced by economic cycles and the gradual implementation of environmental standards, with Brazil and Mexico representing key markets. The Middle East & Africa region faces unique challenges including extreme temperatures that test refrigerant performance, but growing awareness of sustainability is driving gradual adoption of low GWP solutions.

Leading Company Profiles in the Low GWP Refrigerants Market - Industry players and strategies

The low GWP refrigerants market features several prominent companies with distinct strategic approaches to capturing market share. Honeywell International Inc. has established itself as a leader through significant investments in hydrofluoroolefin (HFO) technology, developing products like Solstice® that offer low GWP with favorable safety and performance characteristics. The Chemours Company has built a strong position with its Opteon™ range of low GWP refrigerants, focusing on solutions that provide drop-in compatibility with existing systems to ease the transition for customers. Arkema Inc. has differentiated itself through a broad portfolio spanning both natural and synthetic refrigerants, supported by extensive global manufacturing and distribution capabilities. Daikin America Inc. leverages its position as both a major equipment manufacturer and refrigerant producer to offer integrated solutions, while also investing in next-generation technologies. These companies, along with others like Dongyue Group and Shandong Yuean Chemical Industry, are pursuing strategies that include expanding production capacity, developing new formulations, and strengthening partnerships with equipment manufacturers to ensure their refrigerants are specified in new systems.

Porter's Five Forces Analysis of the Low GWP Refrigerants Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the low GWP refrigerants market. The threat of new entrants is moderate to high, as the technical complexity and regulatory requirements create barriers, but the market's growth potential attracts new participants, particularly in emerging economies. Supplier power is relatively low due to the availability of raw materials and the presence of multiple chemical manufacturers, though certain specialized components may have limited suppliers. Buyer power varies significantly across segments, with large equipment manufacturers having substantial influence over refrigerant specifications, while smaller end-users have less negotiating leverage. The threat of substitutes is significant, as ongoing research into new refrigerant technologies and natural alternatives could displace current solutions. Competitive rivalry is intense, characterized by price competition, technological innovation, and strategic partnerships. The market also faces external pressures from regulatory bodies and environmental organizations that influence product development and market access. Overall, the analysis suggests a dynamic market where established players must continuously innovate while defending against both traditional and emerging competitors.

SWOT Analysis of the Low GWP Refrigerants Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the low GWP refrigerants market reveals key factors influencing industry dynamics. Strengths include strong regulatory support driving market adoption, technological advancements enabling better performance and safety, and growing environmental awareness among consumers and businesses. The market also benefits from established distribution networks and technical expertise built over decades of refrigerant development. However, weaknesses persist in the form of higher costs compared to conventional refrigerants, technical challenges in retrofitting existing systems, and safety concerns with some low GWP alternatives. Significant opportunities exist in emerging markets with growing cooling demand, the development of next-generation refrigerants with improved characteristics, and the integration of low GWP solutions with energy-efficient technologies. Threats include potential regulatory changes that could favor different technologies, the risk of patent expirations affecting profitability, and the possibility of disruptive innovations that could render current solutions obsolete. Additionally, the market faces challenges from economic uncertainties that could delay investments in new cooling systems, particularly in commercial and industrial sectors.

Low GWP Refrigerants Market Value Chain Analysis - Industry structure and value flow

The value chain of the low GWP refrigerants market encompasses multiple stages from raw material sourcing through to end-user application. At the upstream level, the chain begins with chemical manufacturers who produce the fundamental compounds used in refrigerant formulations, relying on suppliers of fluorine, hydrocarbons, and other key inputs. These manufacturers then process these materials into specific refrigerant products through complex chemical synthesis. The midstream segment includes distributors and wholesalers who manage the logistics of refrigerant distribution, ensuring products reach equipment manufacturers, contractors, and end-users. Equipment manufacturers represent another critical node, integrating refrigerants into heat pumps, air conditioning units, and refrigeration systems. Service providers, including HVAC contractors and maintenance technicians, form an essential link by installing, servicing, and repairing systems containing these refrigerants. At the downstream end, various industries including commercial refrigeration, automotive, and residential cooling consume these products. The value chain is characterized by significant technical expertise requirements, regulatory compliance obligations, and the need for specialized handling and recovery infrastructure to ensure safe and environmentally responsible use of refrigerants throughout their lifecycle.

Key Investment Insights in the Low GWP Refrigerants Market - Strategic investment recommendations

Investment insights for the low GWP refrigerants market point to several strategic opportunities for stakeholders across the value chain. For manufacturers, investing in research and development of next-generation refrigerants with improved environmental profiles, enhanced safety characteristics, and better energy efficiency represents a critical priority. Companies should also consider expanding production capacity, particularly for natural refrigerants and HFO blends that are expected to see strong demand growth. Investment in manufacturing facilities in emerging markets could provide competitive advantages as these regions represent the fastest-growing segments of the market. For equipment manufacturers, strategic investments in developing systems optimized for low GWP refrigerants, including redesigned components to address flammability and pressure considerations, will be essential. Service providers should invest in technician training programs to ensure proper handling of new refrigerant types and compliance with evolving regulations. Additionally, investments in refrigerant reclamation and recycling infrastructure will become increasingly important as circular economy principles gain traction and regulations mandate recovery of refrigerants at end-of-life. Private equity and venture capital investors may find opportunities in innovative startups developing breakthrough refrigerant technologies or novel business models around refrigerant lifecycle management.

Low GWP Refrigerants Market Conclusion - Summary and key takeaways

The low GWP refrigerants market stands at a pivotal juncture, characterized by robust growth, technological innovation, and transformative regulatory pressures. With the market expanding from 35.68 billion in 2026 to a projected 76.23 billion by 2033 at a CAGR of 11.45%, the industry is clearly benefiting from the global transition away from high-GWP substances. Key takeaways include the accelerating adoption of natural refrigerants and advanced synthetic alternatives, the critical role of regulatory frameworks in driving market dynamics, and the importance of technological innovation in addressing performance and safety challenges. The competitive landscape features both established chemical giants and specialized players, with success increasingly dependent on comprehensive capabilities spanning R&D, manufacturing, distribution, and technical support. While challenges remain in terms of cost, implementation, and safety, the overall trajectory strongly favors continued market expansion as environmental imperatives intensify and cooling demand grows globally. The market's future will likely be shaped by further technological breakthroughs, evolving regulatory landscapes, and the industry's ability to balance environmental performance with practical considerations of safety and cost-effectiveness.

Research Methodology - How this research was conducted

The research methodology employed for this market analysis combines multiple approaches to ensure comprehensive and accurate insights. Primary research forms the foundation, including interviews with industry experts, manufacturers, distributors, and end-users to gather firsthand perspectives on market dynamics, technological trends, and future outlook. These qualitative insights are supplemented by extensive secondary research, drawing from company annual reports, industry publications, regulatory documents, and market databases to establish historical trends and current market conditions. The analysis incorporates both top-down and bottom-up approaches to validate market size estimates and growth projections, with careful consideration of macroeconomic factors, regulatory developments, and technological advancements. Data triangulation across multiple sources ensures reliability, while scenario analysis accounts for potential variations in regulatory environments and market conditions. The research also leverages proprietary analytical frameworks including Porter's Five Forces and SWOT analysis to provide structured assessments of competitive dynamics and market positioning. Throughout the process, particular attention is paid to emerging trends and disruptive innovations that could reshape the market landscape in the coming years.

Research Scope - Coverage and limitations

The research scope for this low GWP refrigerants market analysis encompasses a comprehensive examination of the industry from 2025 through 2032, with particular focus on the 2026 baseline and 2033 projections. The analysis covers all major market segments including natural and synthetic refrigerants across heat pump, air conditioning, and refrigeration applications. Geographic coverage includes key global regions with detailed assessments of North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, though the depth of regional analysis varies based on data availability and market significance. The research examines market dynamics including drivers, restraints, opportunities, and challenges, while also providing competitive landscape analysis of major industry players. Limitations of the research include potential data gaps in certain emerging markets where information may be less readily available, the inherent uncertainty in long-term market projections given potential regulatory changes or technological disruptions, and the challenge of accurately capturing the impact of macroeconomic factors on market growth. Additionally, the rapidly evolving nature of refrigerant technologies means that some emerging innovations may not be fully reflected in current market data.

Key Companies and Recent Developments in the Low GWP Refrigerants Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The low GWP refrigerants market features several key companies driving innovation and market development through strategic initiatives. Honeywell International Inc. has made significant strides with its Solstice® refrigerant portfolio, recently announcing expanded production capacity to meet growing global demand and introducing new formulations optimized for specific applications including commercial refrigeration and mobile air conditioning. The Chemours Company continues to strengthen its position with the Opteon™ product line, most recently launching low GWP solutions designed for heat pump applications and forming strategic partnerships with major equipment manufacturers to ensure seamless integration. Arkema Inc. has focused on both natural and synthetic refrigerant development, with recent announcements including investments in production facilities in key growth markets and the introduction of new refrigerant blends offering improved performance characteristics. Daikin America Inc. has leveraged its dual role as equipment manufacturer and refrigerant producer to develop integrated solutions, with recent developments including next-generation refrigerant formulations and expanded technical support programs for contractors transitioning to low GWP alternatives. These companies, along with other significant players like Dongyue Group and Shandong Yuean Chemical Industry, are actively pursuing strategies that include capacity expansions, new product launches, and strategic collaborations to capture growing market opportunities while addressing evolving regulatory requirements and sustainability expectations.