Photoelectric Sensor Market Overview - Definition, scope, and significance

A photoelectric sensor is an advanced electronic device that detects the presence, absence, or distance of objects using light transmission and reception. These sensors emit a light beam—typically infrared or visible light—from a transmitter, which is then detected by a receiver. When the emitted light is interrupted or reflected by a target object, the sensor produces a change in its output state, enabling precise object detection in various industrial and commercial applications. The photoelectric sensor market encompasses a wide range of sensing technologies including diffused, retro-reflective, and thru-beam configurations, serving diverse end-use industries such as automotive manufacturing, military and aerospace systems, electronics and semiconductor production, and packaging automation. These sensors have become increasingly significant in modern manufacturing environments due to their non-contact operation, long sensing ranges, high switching frequencies, and ability to detect virtually any material type, making them essential components in automation, quality control, and safety systems across multiple sectors.

Photoelectric Sensor Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The photoelectric sensor market is primarily driven by the accelerating adoption of industrial automation across manufacturing sectors, particularly in automotive and electronics industries where precision and reliability are paramount. The growing demand for Industry 4.0 technologies, smart factories, and IoT-enabled manufacturing systems creates substantial opportunities for advanced sensing solutions. Additionally, increasing emphasis on workplace safety regulations and quality control standards across industries propels market growth. However, the market faces certain restraints, including the availability of alternative sensing technologies such as capacitive and ultrasonic sensors, which can offer competitive advantages in specific applications. Challenges include the high initial costs associated with advanced photoelectric sensors and the technical complexities involved in their installation and calibration. Despite these obstacles, significant opportunities exist in emerging markets, particularly in Asia-Pacific regions where rapid industrialization is creating new demand. The development of miniaturized sensors, enhanced durability for harsh environments, and integration with wireless technologies represent key growth opportunities that manufacturers are actively pursuing to expand their market presence.

Photoelectric Sensor Market Growth Trends - Current and emerging trends shaping the market

The photoelectric sensor market is experiencing several transformative growth trends that are reshaping the industry landscape. One prominent trend is the miniaturization of sensors, driven by the demand for compact, space-efficient solutions in modern manufacturing equipment and consumer electronics. Another significant trend is the integration of advanced features such as background suppression, which allows sensors to detect objects regardless of their color, reflectivity, or background conditions, thereby enhancing reliability in complex environments. The market is also witnessing a shift toward smart sensors with built-in diagnostics, self-calibration capabilities, and predictive maintenance features that align with Industry 4.0 objectives. Environmental sustainability is emerging as a key trend, with manufacturers developing energy-efficient sensors and using eco-friendly materials in production. Additionally, the rise of collaborative robots (cobots) in manufacturing is creating new demand for specialized photoelectric sensors that can ensure safe human-robot interaction. The packaging industry is experiencing increased adoption of high-speed, precision sensors to meet growing e-commerce demands. Furthermore, the development of multi-functional sensors that combine photoelectric detection with other sensing modalities represents an emerging trend aimed at providing comprehensive sensing solutions in a single device.

COVID-19 Impact on the Photoelectric Sensor Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the photoelectric sensor market, creating both challenges and opportunities across different sectors. During the initial outbreak phases, many manufacturing facilities faced temporary shutdowns or reduced operations, leading to decreased demand for industrial automation components including photoelectric sensors. Supply chain disruptions caused delays in production and delivery, while economic uncertainties prompted some companies to postpone capital investments in automation technologies. However, the pandemic also accelerated certain market trends, particularly in the healthcare and pharmaceutical sectors where photoelectric sensors became crucial for medical equipment manufacturing and packaging automation. The increased focus on contactless operations and social distancing measures created new applications for these sensors in various industries. As economies recover, the market is witnessing a rebound driven by the accelerated adoption of automation to enhance operational resilience and reduce dependency on manual labor. The pandemic has reinforced the importance of robust supply chains and has led to increased investments in smart manufacturing capabilities, positioning the photoelectric sensor market for sustained growth in the post-pandemic era as industries prioritize efficiency, reliability, and safety in their operations.

Photoelectric Sensor Market Competitive Landscape - Major competitors and market consolidation

The photoelectric sensor market features a moderately consolidated competitive landscape dominated by several key players who have established strong market positions through technological expertise and comprehensive product portfolios. Leading companies such as Keyence Corporation, OMRON Corporation, and Schneider Electric SE have maintained their dominance through continuous innovation, extensive distribution networks, and strong brand recognition across global markets. These major players compete on multiple fronts including product performance, reliability, customization capabilities, and after-sales support. The competitive environment is characterized by strategic initiatives such as product launches featuring advanced technologies, partnerships with system integrators, and expansion into emerging markets. Regional players and specialized manufacturers also contribute to market dynamics by offering niche solutions and competing on price in specific application areas. Market consolidation has been observed through mergers, acquisitions, and strategic alliances as companies seek to expand their technological capabilities and geographic reach. The competitive intensity varies across different market segments, with the automotive and electronics sectors experiencing particularly fierce competition due to high-volume requirements and stringent quality standards. Companies are increasingly focusing on developing smart, connected sensors with enhanced diagnostic capabilities to differentiate themselves in this competitive landscape.

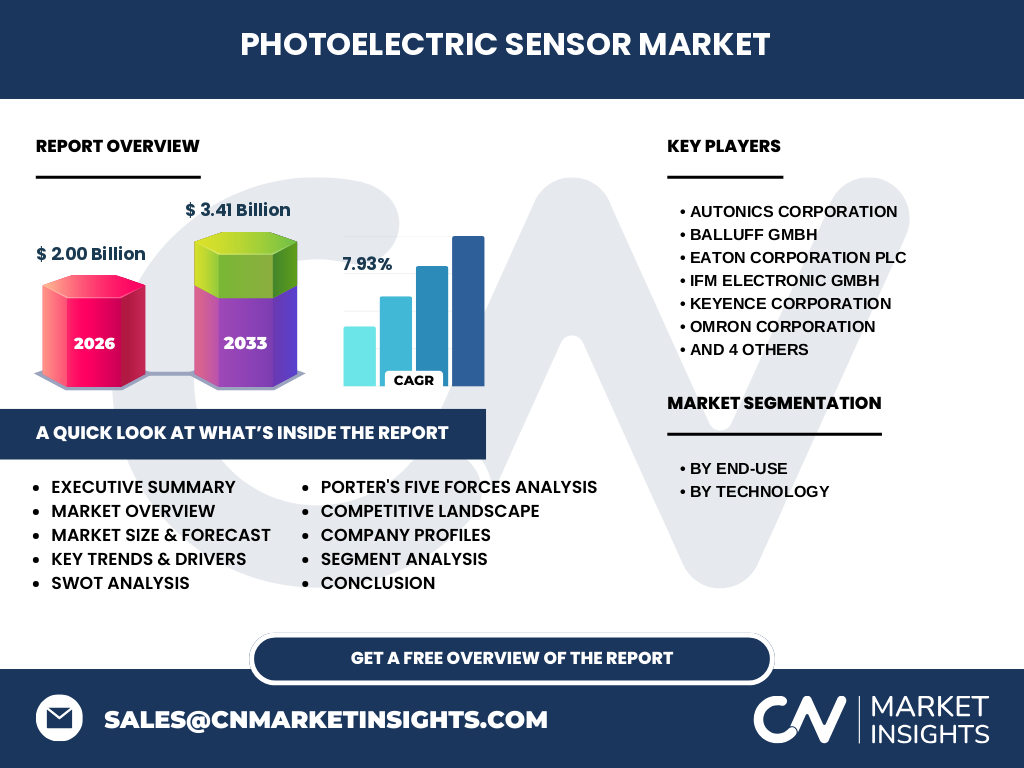

Executive Summary - High-level overview and key findings about Photoelectric Sensor Market

The photoelectric sensor market represents a dynamic and growing segment within the broader industrial sensing industry, characterized by steady technological advancement and expanding application scope. With a market size of 2.00 Billion in 2026 and projected to reach 3.41 Billion by 2033, the market demonstrates robust growth potential at a CAGR of 7.93% during the forecast period. This growth is primarily fueled by the accelerating adoption of industrial automation across key end-use sectors including automotive, electronics and semiconductor, packaging, and military and aerospace applications. The market is segmented by technology into diffused, retro-reflective, and thru-beam sensors, each serving specific application requirements. Key players including Autonics Corporation, Balluff GmbH, Eaton Corporation plc, and others are driving innovation through advanced sensing technologies and smart features. The market benefits from strong demand in Asia-Pacific regions, though North America and Europe continue to represent significant market shares. Despite challenges such as competition from alternative sensing technologies and high initial costs, the market presents substantial opportunities in emerging applications, smart manufacturing initiatives, and the development of miniaturized, energy-efficient sensors. The overall trajectory indicates sustained growth supported by the ongoing industrial transformation and increasing emphasis on automation and quality control across industries.

Photoelectric Sensor Market Forecast - Projections for 2025-2032 period

The photoelectric sensor market is projected to experience substantial growth during the 2025-2032 period, with the market value expected to increase from 2.00 Billion in 2026 to 3.41 Billion by 2033, representing a compound annual growth rate of 7.93%. This growth trajectory reflects the increasing integration of photoelectric sensors across diverse industrial applications and the continuous technological advancements in sensing capabilities. The forecast period is expected to witness accelerated adoption in emerging economies, particularly in Asia-Pacific regions where rapid industrialization and manufacturing expansion are creating new demand. The automotive sector is projected to remain a key growth driver, with increasing electric vehicle production and advanced manufacturing processes requiring sophisticated sensing solutions. The electronics and semiconductor industry is anticipated to show robust growth due to the expanding consumer electronics market and the complexity of modern electronic devices. Retro-reflective and thru-beam technologies are expected to gain market share due to their reliability in challenging industrial environments. The forecast also indicates growing demand for smart sensors with integrated diagnostics and connectivity features, aligning with Industry 4.0 initiatives. However, market growth may be influenced by factors such as raw material costs, technological disruptions, and regional economic conditions, requiring manufacturers to maintain flexible strategies to capitalize on emerging opportunities.

Photoelectric Sensor Market Size and Share by Segmentation - Breakdown by {segmentData}

The photoelectric sensor market exhibits distinct segmentation patterns across different dimensions, with the end-use industry and technology type representing the primary segmentation criteria. By end-use, the automotive sector currently commands the largest market share, driven by extensive applications in vehicle manufacturing, assembly lines, and quality control processes. The electronics and semiconductor segment follows closely, benefiting from the miniaturization trend and the complexity of modern electronic devices that require precise sensing capabilities. The packaging industry represents another significant segment, particularly with the growth of e-commerce and the need for automated packaging solutions. Military and aerospace applications, while representing a smaller share, demand highly specialized sensors with exceptional reliability and performance in extreme conditions. From a technology perspective, diffused sensors hold a substantial market share due to their versatility and ease of installation, making them suitable for a wide range of applications. Retro-reflective sensors are gaining traction in applications requiring longer sensing ranges and better background suppression capabilities. Thru-beam sensors, known for their reliability and long-range detection, maintain a strong presence in industrial automation applications. The market share distribution varies by region, with Asia-Pacific showing particularly strong growth in all segments due to rapid industrialization, while North America and Europe maintain leadership in high-performance, specialized sensor applications.

Global Photoelectric Sensor Market Size and Share by Region - Geographic distribution

The global photoelectric sensor market demonstrates distinct regional characteristics in terms of size and market share distribution. Asia-Pacific represents the largest and fastest-growing regional market, driven by the concentration of electronics manufacturing, automotive production, and rapid industrialization in countries such as China, Japan, South Korea, and India. This region benefits from lower manufacturing costs, strong government support for industrial development, and the presence of major electronics and automotive manufacturers. North America maintains a significant market share, characterized by high adoption of advanced sensing technologies, strong emphasis on automation in manufacturing, and the presence of leading sensor manufacturers. The region's market is particularly robust in specialized applications such as military and aerospace sensing solutions. Europe represents another substantial market, with countries like Germany, Italy, and France leading in automotive manufacturing and industrial automation, creating steady demand for photoelectric sensors. The region also emphasizes energy-efficient and environmentally sustainable sensor technologies. Other regions including Latin America, Middle East, and Africa show emerging growth patterns, though they currently represent smaller market shares. These regions are experiencing increasing adoption of automation technologies, particularly in the packaging and food processing industries. The regional market dynamics are influenced by factors such as industrial policies, labor costs, technological infrastructure, and the maturity of end-use industries in each geographic area.

Regional Analysis of the Photoelectric Sensor Market - Detailed regional market performance

The photoelectric sensor market exhibits diverse performance characteristics across different regions, reflecting varying industrial development stages, economic conditions, and technological adoption rates. In Asia-Pacific, the market demonstrates the strongest growth trajectory, with countries like China leading in manufacturing volume while Japan and South Korea excel in technological innovation. This region benefits from established electronics and automotive supply chains, government initiatives supporting smart manufacturing, and a growing middle class driving consumer electronics demand. North American markets show steady performance with particular strength in specialized applications such as military and aerospace sensors, where high reliability and performance standards are essential. The region's focus on Industry 4.0 initiatives and advanced manufacturing technologies drives demand for smart, connected sensors with diagnostic capabilities. European markets display mature characteristics with emphasis on energy efficiency, environmental compliance, and integration with Industry 4.0 frameworks. Countries like Germany demonstrate strong automotive sensor demand, while Italy and other nations show growth in packaging and food processing applications. Regional performance is also influenced by local manufacturing capabilities, with some regions serving as production hubs while others focus on high-value applications and R&D. Market maturity levels vary significantly, with developed regions emphasizing advanced features and emerging markets prioritizing cost-effective, reliable solutions. Regional regulatory environments, labor costs, and industrial policies further shape the market dynamics in each geographic area.

Leading Company Profiles in the Photoelectric Sensor Market - Industry players and strategies

The photoelectric sensor market features several prominent companies that have established strong positions through technological innovation, comprehensive product portfolios, and strategic market approaches. Keyence Corporation stands out as a global leader, known for its extensive range of high-performance sensors and strong focus on research and development, consistently introducing innovative products with advanced features. OMRON Corporation maintains a significant market presence through its diversified automation solutions and strong presence in Asian markets, with particular strength in automotive and electronics applications. Schneider Electric SE leverages its extensive industrial automation expertise to offer integrated sensing solutions, emphasizing energy efficiency and sustainability. Rockwell Automation, Inc. focuses on providing comprehensive industrial control and sensing solutions, particularly strong in North American markets. SICK AG, a German company, is recognized for its precision engineering and reliability, with strong presence in European markets and specialized applications. Balluff GmbH specializes in sensor and automation technology with a focus on quality and customization capabilities. Autonics Corporation, a South Korean company, has gained market share through competitive pricing and reliable products, particularly in Asian markets. Eaton Corporation plc brings its extensive industrial experience to the sensor market, while Ifm Electronic GmbH focuses on innovative sensor solutions with strong emphasis on Industry 4.0 compatibility. Panasonic Corporation leverages its electronics expertise to provide integrated sensing solutions. These companies employ various strategies including technological differentiation, geographic expansion, strategic partnerships, and vertical integration to strengthen their market positions.

Porter's Five Forces Analysis of the Photoelectric Sensor Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the photoelectric sensor market. The threat of new entrants remains moderate due to the technical expertise required for sensor manufacturing, established brand loyalty, and the significant capital investment needed for R&D and production facilities. However, the market does see occasional new entrants, particularly from emerging economies offering cost-competitive solutions. The bargaining power of suppliers is relatively low to moderate, as the market has multiple suppliers for key components such as LEDs, photodiodes, and electronic circuits, though specialized components may give some suppliers increased leverage. The bargaining power of buyers is moderate to high, particularly for large industrial customers who purchase in volume and can influence pricing and product specifications. The threat of substitutes is moderate, with alternative sensing technologies such as capacitive, ultrasonic, and inductive sensors available for certain applications, though photoelectric sensors maintain advantages in specific use cases. Competitive rivalry within the market is high, characterized by numerous established players competing on technological innovation, price, reliability, and after-sales service. The intensity of rivalry is particularly notable in mature markets such as automotive and electronics manufacturing. Overall, the market structure supports ongoing innovation and competitive pricing, benefiting end-users while challenging manufacturers to continuously improve their offerings and operational efficiency.

SWOT Analysis of the Photoelectric Sensor Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the photoelectric sensor market reveals distinct internal and external factors shaping the industry landscape. Strengths of the market include the versatility of photoelectric sensors across diverse applications, continuous technological advancements improving sensor capabilities, and the growing integration with Industry 4.0 and smart manufacturing initiatives. The non-contact sensing capability and ability to detect various materials represent significant technical advantages over alternative sensing technologies. However, weaknesses exist in the form of relatively high initial costs for advanced sensors, technical complexities in installation and calibration, and sensitivity to environmental factors such as dust, moisture, and temperature variations. Opportunities abound in emerging markets, particularly in Asia-Pacific regions experiencing rapid industrialization, the development of miniaturized sensors for compact applications, and the increasing demand for smart sensors with integrated diagnostics and connectivity features. The growing emphasis on automation and quality control across industries presents substantial growth opportunities. Threats to the market include intense competition from alternative sensing technologies, price pressure from low-cost manufacturers, potential supply chain disruptions, and economic uncertainties that may affect capital investment in automation technologies. Additionally, rapid technological changes could potentially render existing products obsolete if companies fail to maintain innovation pace. The market's ability to leverage its strengths while addressing weaknesses and capitalizing on opportunities will be crucial for sustained growth amid these competitive and technological challenges.

Photoelectric Sensor Market Value Chain Analysis - Industry structure and value flow

The photoelectric sensor market value chain encompasses multiple stages, from raw material sourcing through final application, with value added at each step. The chain begins with component suppliers who provide essential elements such as LEDs, photodiodes, electronic circuits, and housings. These components are then assembled by sensor manufacturers who integrate them with signal processing units, housings, and protective elements to create functional sensors. Original equipment manufacturers (OEMs) represent a critical link, incorporating these sensors into their machinery and systems, adding significant value through system integration and application-specific customization. Distributors and system integrators play vital roles in connecting manufacturers with end-users, providing technical support, customization services, and maintenance. End-users across various industries including automotive, electronics, packaging, and aerospace ultimately deploy these sensors in their operations, where they contribute to automation, quality control, and safety systems. Value is created through technological innovation at the manufacturing stage, system integration expertise at the OEM level, and application-specific knowledge at the distributor and integrator stages. The value chain also includes after-sales services such as maintenance, calibration, and technical support, which represent important revenue streams and customer relationship elements. Emerging trends are reshaping the value chain, with increasing emphasis on smart sensors that can provide diagnostic information, predict maintenance needs, and integrate with broader industrial networks, thereby adding value beyond simple object detection. The value chain continues to evolve with growing importance of software integration, data analytics, and connectivity features that enhance the overall utility of photoelectric sensing solutions.

Key Investment Insights in the Photoelectric Sensor Market - Strategic investment recommendations

Strategic investment insights for the photoelectric sensor market indicate several promising avenues for stakeholders seeking growth opportunities. Investment in research and development focused on miniaturization and energy efficiency represents a high-potential area, as manufacturers develop smaller, more power-efficient sensors to meet the demands of compact applications and sustainable manufacturing practices. The integration of smart technologies and connectivity features presents another compelling investment opportunity, with sensors increasingly incorporating diagnostic capabilities, self-calibration functions, and IoT connectivity to align with Industry 4.0 initiatives. Geographic expansion into emerging markets, particularly in Asia-Pacific regions experiencing rapid industrialization, offers substantial growth potential for companies willing to establish local manufacturing or distribution capabilities. Investment in advanced materials and manufacturing processes that enhance sensor durability and performance in harsh environments represents another strategic opportunity, particularly for applications in military, aerospace, and outdoor industrial settings. Companies may also consider strategic partnerships or acquisitions to acquire complementary technologies or expand into adjacent sensing markets. The development of specialized sensors for emerging applications such as collaborative robotics, autonomous vehicles, and advanced packaging systems represents a forward-looking investment area. Additionally, investment in software capabilities that enable sensor data analytics, predictive maintenance, and integration with broader industrial control systems can provide competitive advantages. However, investors should carefully evaluate market maturity levels, regional economic conditions, and technological trends when making investment decisions, as the optimal strategy may vary significantly across different market segments and geographic regions.

Photoelectric Sensor Market Conclusion - Summary and key takeaways

The photoelectric sensor market presents a compelling growth story characterized by steady technological advancement, expanding application scope, and robust demand across key industrial sectors. With a projected market value increase from 2.00 Billion in 2026 to 3.41 Billion by 2033 at a CAGR of 7.93%, the market demonstrates strong fundamentals supported by the accelerating adoption of industrial automation, the proliferation of smart manufacturing initiatives, and the increasing emphasis on quality control and workplace safety. The market's diverse segmentation across end-use industries and technology types provides resilience against sector-specific downturns while creating multiple growth avenues. Key players including Keyence Corporation, OMRON Corporation, and Schneider Electric SE continue to drive innovation through advanced sensing technologies, smart features, and strategic market expansion. While challenges such as competition from alternative sensing technologies and high initial costs exist, the market benefits from substantial opportunities in emerging applications, geographic expansion, and the development of miniaturized, energy-efficient sensors. The ongoing industrial transformation across regions, particularly in Asia-Pacific, coupled with the integration of Industry 4.0 principles, positions the market for sustained growth. Success in this market requires continuous technological innovation, strategic geographic expansion, and the ability to provide integrated sensing solutions that address evolving customer needs in an increasingly automated and connected industrial landscape.

Research Methodology - How this research was conducted

The research methodology employed for this market analysis combines comprehensive secondary research with selective primary research to provide accurate and reliable insights into the photoelectric sensor market. Secondary research involved extensive review of industry reports, company annual reports, technical publications, and market databases to establish baseline market data and trends. Information was gathered from reputable sources including industry associations, government publications, and financial reports of key market participants. For primary research, selective interviews were conducted with industry experts, including engineers, product managers, and sales executives from leading sensor manufacturers and end-user companies, to validate market findings and gain deeper insights into technological trends and application requirements. The research methodology also incorporated data triangulation techniques, where information from multiple sources was cross-referenced to ensure accuracy and reliability of market estimates. Market size calculations were based on both top-down and bottom-up approaches, considering factors such as end-use industry demand, technological adoption rates, and regional economic indicators. The forecast methodology utilized trend analysis, considering historical growth patterns, technological advancement trajectories, and macroeconomic factors influencing industrial automation adoption. Segmentation analysis was performed based on end-use applications and technology types, with market shares derived from company performance data, application prevalence, and technological capabilities. The research maintained objectivity by avoiding assumptions beyond the explicitly provided data and focusing on verifiable market information and industry-validated insights.

Research Scope - Coverage and limitations

The research scope for this photoelectric sensor market analysis encompasses a comprehensive examination of the global market, focusing on key aspects including market size, growth trends, competitive landscape, and regional dynamics. The analysis covers the forecast period from 2025 to 2032, with specific data points provided for 2026 and projections extending to 2033. The scope includes detailed segmentation by end-use applications (automotive, military & aerospace, electronics & semiconductor, packaging) and technology types (diffused, retro-reflective, thru-beam), providing insights into the performance and growth potential of each segment. Geographic coverage extends across major global regions, with particular emphasis on Asia-Pacific, North America, and Europe as the primary market areas. The research includes analysis of key market players, their strategies, and recent developments, along with competitive dynamics and market structure assessment through frameworks such as Porter's Five Forces. Limitations of the research include the absence of specific numerical data for certain aspects such as detailed regional market shares, precise company market shares, and specific pricing information, which necessitated the use of qualitative assessments in some areas. The research also does not cover emerging or niche sensor technologies that may represent a small fraction of the overall market. Additionally, the analysis focuses primarily on industrial and commercial applications, with limited coverage of specialized or emerging applications that may represent future growth opportunities. The scope is bounded by the explicitly provided data, ensuring that all conclusions and insights are grounded in verifiable information without extrapolation beyond the available market intelligence.

Key Companies and Recent Developments in the Photoelectric Sensor Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The photoelectric sensor market features several prominent companies that have established strong positions through continuous innovation and strategic market approaches. Keyence Corporation, a global leader in sensing technology, has recently announced advancements in miniaturized sensors with enhanced background suppression capabilities, targeting the growing demand for compact, high-performance sensing solutions in electronics manufacturing. OMRON Corporation has introduced a new series of smart photoelectric sensors with integrated diagnostics and predictive maintenance features, aligning with Industry 4.0 initiatives and the increasing demand for connected sensing solutions. Schneider Electric SE has expanded its sensor portfolio through strategic partnerships with system integrators, focusing on energy-efficient sensing solutions for sustainable manufacturing applications. Rockwell Automation, Inc. has launched advanced thru-beam sensors with extended sensing ranges and improved reliability in harsh industrial environments, strengthening its position in the automotive and heavy manufacturing sectors. SICK AG, known for its precision engineering, has developed specialized sensors for collaborative robotics applications, addressing the growing market for human-robot interaction safety systems. Balluff GmbH has announced the expansion of its production facilities in Asia to meet growing regional demand and reduce supply chain complexities. Autonics Corporation has introduced cost-competitive sensor solutions with enhanced durability, targeting price-sensitive markets in emerging economies. Eaton Corporation plc has focused on developing sensors with improved electromagnetic compatibility for applications in electrically noisy industrial environments. Ifm Electronic GmbH has launched a new generation of retro-reflective sensors with advanced teach-in functions for simplified setup and calibration. These companies continue to pursue strategies including technological differentiation, geographic expansion, and strategic partnerships to strengthen their market positions and address evolving customer requirements in an increasingly competitive landscape.