Fiber Cement Market Overview - Definition, scope, and significance

Fiber cement is a composite building material made from cement reinforced with cellulose fibers, synthetic fibers, or other additives. This versatile material is primarily used in construction for applications such as siding, roofing, and facade systems. The fiber cement market encompasses the production, distribution, and installation of these materials across residential, commercial, and industrial sectors. The significance of this market lies in its ability to provide durable, weather-resistant, and aesthetically pleasing alternatives to traditional building materials like wood, vinyl, and brick. Fiber cement products offer superior performance characteristics including fire resistance, termite resistance, and minimal maintenance requirements, making them increasingly popular in both new construction and renovation projects worldwide.

Fiber Cement Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The fiber cement market is driven by several key factors including increasing construction activities in emerging economies, growing demand for sustainable and eco-friendly building materials, and the rising preference for low-maintenance exterior cladding solutions. Urbanization and infrastructure development in developing countries are creating substantial demand for durable construction materials. However, the market faces restraints such as the high initial cost compared to traditional materials, the weight of fiber cement products which can increase transportation and installation costs, and the availability of alternative materials. Challenges include the need for specialized installation skills and concerns about silica dust exposure during cutting and installation. Opportunities exist in developing innovative products with enhanced properties, expanding into emerging markets, and leveraging the growing trend toward sustainable construction practices that prioritize materials with low environmental impact and long service life.

Fiber Cement Market Growth Trends - Current and emerging trends shaping the market

The fiber cement market is experiencing several notable growth trends. One prominent trend is the increasing adoption of fiber cement in both residential and commercial construction, driven by its superior durability and aesthetic versatility. Manufacturers are developing products that mimic natural materials like wood and stone while offering enhanced performance characteristics. Another significant trend is the growing focus on sustainability, with manufacturers incorporating recycled materials and developing products with lower environmental footprints. The market is also witnessing technological advancements in manufacturing processes that improve product quality and reduce production costs. Additionally, there is a rising demand for fiber cement products in regions prone to extreme weather conditions due to their resilience against hurricanes, wildfires, and other natural disasters. The trend toward prefabrication and modular construction is also creating new opportunities for fiber cement applications in building systems.

COVID-19 Impact on the Fiber Cement Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a mixed impact on the fiber cement market. During the initial lockdowns in 2020, construction activities were significantly disrupted due to supply chain interruptions, labor shortages, and restrictions on building sites. This led to temporary declines in demand for fiber cement products. However, the market demonstrated resilience as construction activities resumed with enhanced safety protocols. The pandemic also accelerated certain trends, including increased home renovation projects as people spent more time at home, which boosted demand for exterior remodeling materials including fiber cement siding. Additionally, the emphasis on health and safety in buildings has reinforced the value of durable, low-maintenance materials like fiber cement. As economies recover and construction activities normalize, the fiber cement market is expected to regain momentum, with the long-term growth trajectory remaining positive despite the short-term disruptions caused by the pandemic.

Fiber Cement Market Competitive Landscape - Major competitors and market consolidation

The fiber cement market features a competitive landscape characterized by several major players and ongoing consolidation through mergers and acquisitions. Key companies such as James Hardie Industries, Compagnie de Saint Gobain, Etex NV, and CSR Ltd dominate the market with their extensive product portfolios and global distribution networks. These companies compete on factors such as product quality, innovation, pricing, and customer service. The market is witnessing increased consolidation as larger companies acquire smaller regional players to expand their geographic presence and product offerings. This consolidation trend is driven by the desire to achieve economies of scale, enhance research and development capabilities, and strengthen market position. Competition is also intensifying with the entry of new players in emerging markets, particularly in Asia-Pacific and Latin America, where construction activity is booming. The competitive landscape is further shaped by the focus on developing sustainable products and improving manufacturing efficiency to meet evolving customer demands and regulatory requirements.

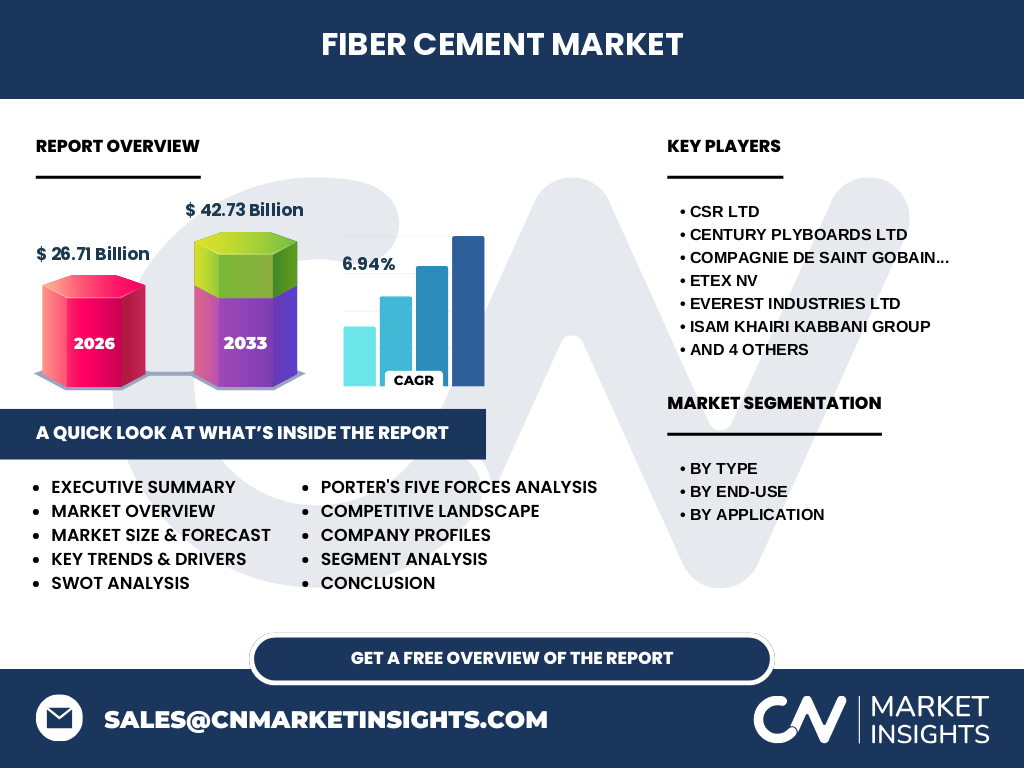

Executive Summary - High-level overview and key findings about Fiber Cement Market

The fiber cement market is experiencing steady growth driven by increasing construction activities, particularly in emerging economies, and the growing demand for durable, low-maintenance building materials. With a market size of $26.71 billion in 2026 and a projected growth to $42.73 billion by 2033, representing a CAGR of 6.94%, the industry demonstrates strong potential for expansion. Key findings indicate that the residential segment continues to dominate the market, with siding applications being the primary driver of demand. The market is characterized by intense competition among major players who are focusing on product innovation, sustainability, and geographic expansion to maintain their market positions. The COVID-19 pandemic caused temporary disruptions but also accelerated certain trends such as home renovation. Looking ahead, the market is expected to benefit from the increasing focus on sustainable construction practices and the growing preference for materials that offer both aesthetic appeal and superior performance characteristics.

Fiber Cement Market Forecast - Projections for 2025-2032 period

The fiber cement market is projected to experience robust growth during the 2025-2032 period, with the market expanding from $26.71 billion in 2026 to $42.73 billion by 2033, representing a compound annual growth rate of 6.94%. This growth trajectory is underpinned by several factors including the recovery of the global construction industry, increasing urbanization in developing regions, and the rising adoption of sustainable building materials. The forecast period is expected to witness continued innovation in product development, with manufacturers focusing on enhancing the aesthetic appeal, durability, and environmental performance of fiber cement products. Geographic expansion into emerging markets, particularly in Asia-Pacific and Latin America, is anticipated to be a significant growth driver. The residential construction segment is expected to remain the largest end-use category, while commercial and industrial applications are projected to show strong growth rates. Additionally, the market is likely to benefit from the increasing frequency of extreme weather events, which is driving demand for resilient building materials.

Fiber Cement Market Size and Share by Segmentation - Breakdown by {segmentData}

The fiber cement market can be segmented by type, end-use, and application, each contributing differently to the overall market size and share. By type, the market is divided into air-cured and autoclaved fiber cement products, with autoclaved fiber cement typically commanding a larger share due to its superior strength and dimensional stability. In terms of end-use, the residential segment dominates the market, accounting for the largest share as homeowners increasingly opt for durable and low-maintenance siding solutions. The non-residential segment, including commercial and industrial buildings, represents a growing market share driven by the demand for fire-resistant and weather-resistant materials. By application, siding remains the largest segment, followed by roofing and facade applications. The siding segment's dominance is attributed to the widespread use of fiber cement as an exterior cladding material in both new construction and renovation projects. Roofing applications are gaining traction due to the material's durability and resistance to harsh weather conditions.

Global Fiber Cement Market Size and Share by Region - Geographic distribution

The global fiber cement market exhibits varying growth patterns and market shares across different regions, influenced by factors such as construction activity, economic development, and regional preferences for building materials. North America represents a significant market share, driven by the strong presence of established manufacturers and the high demand for renovation and remodeling projects in the United States and Canada. Europe follows closely, with countries like Germany, the UK, and France contributing to market growth through stringent building regulations and the emphasis on energy-efficient construction. The Asia-Pacific region is emerging as the fastest-growing market, fueled by rapid urbanization, infrastructure development, and increasing disposable incomes in countries such as China, India, and Southeast Asian nations. Latin America and the Middle East & Africa regions also contribute to the global market, albeit with smaller shares, as construction activities expand in these areas. The regional distribution of the fiber cement market reflects the global construction industry's dynamics and the varying adoption rates of innovative building materials across different geographic areas.

Regional Analysis of the Fiber Cement Market - Detailed regional market performance

The fiber cement market's regional performance varies significantly across different geographic areas. In North America, the market is characterized by high product awareness and established distribution channels, with the United States being a major contributor to regional growth. The region benefits from a strong renovation and remodeling sector, particularly in mature housing markets. Europe's fiber cement market is driven by stringent building codes and energy efficiency regulations, with countries like Germany and the UK leading in adoption rates. The Asia-Pacific region presents a dynamic growth landscape, with China and India emerging as key markets due to rapid urbanization and infrastructure development. Japan and Australia also contribute significantly to regional market performance with their advanced construction industries. Latin America's market is growing steadily, with Brazil and Mexico being the primary drivers of demand. The Middle East & Africa region, while currently smaller in market size, shows potential for growth due to increasing construction activities in Gulf Cooperation Council countries and South Africa. Each region's market performance is influenced by local economic conditions, construction trends, and regulatory environments.

Leading Company Profiles in the Fiber Cement Market - Industry players and strategies

The fiber cement market is dominated by several key players who have established strong market positions through product innovation, strategic partnerships, and geographic expansion. James Hardie Industries plc, a market leader, has built its success on a diverse product portfolio and strong brand recognition, particularly in North America and Australia. Compagnie de Saint Gobain SA leverages its extensive global presence and diversified building materials portfolio to maintain a competitive edge. Etex NV has focused on expanding its product range and strengthening its position in emerging markets through strategic acquisitions. CSR Ltd, based in Australia, has capitalized on the region's construction boom and established a strong presence in the Asia-Pacific market. Century Plyboards Ltd and Everest Industries Ltd are notable players in the Indian market, benefiting from the country's growing construction sector. These companies employ various strategies including investment in research and development, focus on sustainable products, and expansion into new geographic markets to maintain their competitive positions and drive growth in the fiber cement industry.

Porter's Five Forces Analysis of the Fiber Cement Market - Competitive forces assessment

Porter's Five Forces analysis provides insights into the competitive dynamics of the fiber cement market. The threat of new entrants is moderate due to the significant capital requirements for manufacturing facilities and the need for technical expertise, but it remains possible for established building materials companies to diversify into fiber cement. The bargaining power of suppliers is relatively low as raw materials for fiber cement production are widely available, although suppliers of specialized additives may have some leverage. The bargaining power of buyers is moderate, with large construction companies and distributors having some influence on pricing and product specifications. The threat of substitutes is significant, with alternatives such as vinyl siding, wood, and brick competing with fiber cement products. Competitive rivalry within the industry is intense, with major players competing on product quality, innovation, pricing, and customer service. The intensity of competitive rivalry is further heightened by the presence of both global and regional players, as well as the ongoing consolidation through mergers and acquisitions.

SWOT Analysis of the Fiber Cement Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the fiber cement market reveals several key factors influencing its development. Strengths of the market include the superior durability and performance characteristics of fiber cement products, their versatility in applications, and the growing awareness of their benefits among consumers and builders. The material's resistance to fire, termites, and harsh weather conditions represents a significant competitive advantage. However, weaknesses exist in the form of higher initial costs compared to some alternatives and the weight of the products, which can increase transportation and installation expenses. Opportunities in the market are abundant, including the growing demand for sustainable building materials, expansion into emerging markets, and the potential for product innovation to address specific regional needs. Threats to the market include the volatility of raw material prices, the availability of substitute materials, and potential regulatory changes regarding silica dust exposure during installation. Additionally, economic downturns can impact construction activity and, consequently, demand for fiber cement products.

Fiber Cement Market Value Chain Analysis - Industry structure and value flow

The fiber cement market's value chain encompasses several key stages, from raw material procurement to end-user application. The chain begins with the sourcing of primary raw materials such as cement, cellulose fibers, and additives from suppliers. These materials are then processed by manufacturers who produce fiber cement boards, sheets, and other products through specialized manufacturing processes. The manufacturing stage involves significant capital investment in production facilities and quality control measures to ensure product consistency and performance. Following production, the products are distributed through various channels including direct sales to large contractors, distribution through building materials suppliers, and retail channels for smaller projects. The installation phase requires skilled labor to ensure proper application, which is crucial for the product's performance and longevity. Finally, the value chain extends to after-sales services and potential recycling or disposal of the materials at the end of their lifecycle. Each stage of the value chain presents opportunities for value addition and efficiency improvements, contributing to the overall competitiveness of the fiber cement market.

Key Investment Insights in the Fiber Cement Market - Strategic investment recommendations

Investment in the fiber cement market presents several strategic opportunities for stakeholders. One key insight is the potential for growth in emerging markets, particularly in Asia-Pacific and Latin America, where rapid urbanization and infrastructure development are driving demand for durable building materials. Investors should consider opportunities in expanding manufacturing capacity in these regions to capitalize on local market growth and reduce transportation costs. Another investment avenue is in research and development to create innovative products that address specific market needs, such as improved fire resistance or enhanced aesthetic options. The trend toward sustainable construction also presents investment opportunities in developing eco-friendly fiber cement products with lower environmental impact. Additionally, investments in advanced manufacturing technologies can improve production efficiency and product quality, providing a competitive edge. Strategic partnerships or acquisitions of regional players can offer a faster route to market expansion compared to organic growth. Investors should also consider the potential for vertical integration, particularly in controlling the supply of key raw materials to mitigate price volatility risks.

Fiber Cement Market Conclusion - Summary and key takeaways

The fiber cement market is positioned for steady growth, driven by increasing construction activities, particularly in emerging economies, and the growing demand for durable, low-maintenance building materials. With a projected market size of $42.73 billion by 2033 and a CAGR of 6.94%, the industry demonstrates strong potential for expansion. Key takeaways from the market analysis include the dominance of the residential segment, the importance of product innovation in maintaining competitive advantage, and the significant opportunities in emerging markets. The market is characterized by intense competition among major players who are focusing on sustainability, geographic expansion, and product diversification to strengthen their market positions. While challenges such as high initial costs and the weight of products exist, the superior performance characteristics of fiber cement continue to drive its adoption in both new construction and renovation projects. The COVID-19 pandemic caused temporary disruptions but also accelerated certain trends, ultimately reinforcing the market's long-term growth trajectory.

Research Methodology - How this research was conducted

The research methodology employed for this fiber cement market analysis combines both primary and secondary research approaches to ensure comprehensive and accurate insights. Primary research involved interviews with industry experts, including manufacturers, suppliers, distributors, and end-users, to gather firsthand information on market trends, challenges, and opportunities. These interviews provided valuable qualitative data on market dynamics and future outlook. Secondary research encompassed the analysis of industry reports, company annual reports, trade publications, and government statistics to obtain quantitative data on market size, growth rates, and competitive landscape. The research also utilized data triangulation techniques to validate findings across multiple sources, ensuring the reliability of the market projections. Geographic segmentation was achieved through a combination of country-specific data analysis and regional economic indicators. The research methodology also included a thorough review of recent developments, product launches, and strategic initiatives by key market players to provide a current and forward-looking perspective on the fiber cement market.

Research Scope - Coverage and limitations

The research scope for this fiber cement market analysis covers a comprehensive examination of the global market from 2020 to 2033, with a particular focus on the forecast period of 2025-2032. The study encompasses market segmentation by type (air-cured and autoclaved), end-use (residential and non-residential), and application (roofing, outside siding or facade). Geographic coverage includes major regions such as North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The research provides detailed analysis of market size, growth trends, competitive landscape, and key player strategies. However, limitations exist in terms of the availability of granular data for certain emerging markets and the potential for rapid changes in market dynamics due to unforeseen economic or regulatory developments. The research also acknowledges the challenges in accurately forecasting market growth in the face of global uncertainties such as economic fluctuations and geopolitical events. Despite these limitations, the study aims to provide a robust and insightful analysis of the fiber cement market to support strategic decision-making for industry stakeholders.

Key Companies and Recent Developments in the Fiber Cement Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The fiber cement market is characterized by the presence of several key companies that have been driving innovation and market growth through strategic initiatives. James Hardie Industries plc, a market leader, has recently announced the expansion of its product line to include more sustainable options and has invested in advanced manufacturing technologies to improve production efficiency. Compagnie de Saint Gobain SA has focused on strengthening its global presence through strategic acquisitions and partnerships, particularly in emerging markets. Etex NV has launched several new product lines featuring enhanced durability and aesthetic options, responding to evolving consumer preferences. CSR Ltd has announced plans to expand its manufacturing capacity in Australia to meet growing domestic and regional demand. NICHIHA Corp has introduced innovative fiber cement products with improved insulation properties, targeting the energy-efficient construction market. These companies, along with others such as Century Plyboards Ltd, Everest Industries Ltd, and Swisspearl Group AG, continue to shape the market through product innovations, strategic partnerships, and geographic expansions. Recent developments also include increased focus on sustainability, with many companies investing in eco-friendly manufacturing processes and developing products with recycled content.