Civil Drone Market Overview - Definition, scope, and significance

The civil drone market encompasses the commercial and non-military use of unmanned aerial vehicles (UAVs) across various industries and applications. These remotely piloted or autonomous aircraft systems have revolutionized multiple sectors by providing cost-effective aerial data collection, monitoring, and delivery capabilities. The market includes hardware components (drones, sensors, cameras), software platforms for data analysis and flight control, and services ranging from drone operations to maintenance and training. With a current market size of 15.95 billion and projected growth to 38.82 billion by 2033, civil drones represent a transformative technology with applications spanning agriculture, infrastructure inspection, aerial photography, surveying, mapping, and energy sector monitoring. The significance of this market lies in its ability to enhance operational efficiency, reduce costs, improve safety in hazardous environments, and provide data-driven insights that were previously difficult or impossible to obtain through traditional methods.

Civil Drone Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The civil drone market is driven by several key factors including technological advancements in battery life, payload capacity, and autonomous flight capabilities, which have expanded the range of applications and improved operational efficiency. The increasing adoption of precision agriculture techniques, growing demand for infrastructure inspection and monitoring, and the rising need for rapid disaster response and environmental monitoring continue to fuel market growth. However, the industry faces significant restraints including strict regulatory frameworks governing drone operations, privacy concerns, and limited flight time due to battery constraints. Challenges include the high initial investment costs for advanced drone systems, the need for skilled operators, and the complexity of integrating drone data with existing enterprise systems. Despite these obstacles, substantial opportunities exist in emerging applications such as last-mile delivery, 5G network maintenance, and the development of beyond visual line of sight (BVLOS) operations, which could unlock new revenue streams and expand market penetration across various sectors.

Civil Drone Market Growth Trends - Current and emerging trends shaping the market

The civil drone market is experiencing several transformative growth trends that are reshaping the industry landscape. The integration of artificial intelligence and machine learning capabilities into drone systems is enabling advanced autonomous operations, real-time data analysis, and predictive maintenance features. There is a notable shift toward the development of hybrid and hydrogen fuel cell-powered drones, which promise extended flight times and reduced environmental impact compared to traditional battery-powered systems. The market is also witnessing increased adoption of drone-in-a-box solutions, which allow for automated deployment and charging, making drone operations more scalable and cost-effective. Additionally, the convergence of drones with Internet of Things (IoT) technologies is creating new possibilities for connected operations and data sharing across platforms. The emergence of drone swarms for coordinated missions in agriculture and infrastructure inspection represents another significant trend, while the growing emphasis on drone traffic management systems (UTM) is addressing the challenges of integrating drones into national airspace systems.

COVID-19 Impact on the Civil Drone Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a dual impact on the civil drone market, presenting both challenges and unexpected opportunities. During the initial lockdowns, supply chain disruptions and reduced industrial activity temporarily slowed market growth. However, the pandemic also accelerated the adoption of drone technology for contactless delivery of medical supplies, essential goods, and public health monitoring in affected areas. Drones played a crucial role in enforcing social distancing measures, conducting temperature screening in public spaces, and delivering test kits to remote locations. The crisis highlighted the value of drones in emergency response scenarios and led to increased investment in drone-based solutions for public safety and healthcare logistics. As economies recover, the market is experiencing renewed momentum, with organizations recognizing the resilience and efficiency benefits of drone technology. The pandemic has effectively fast-tracked regulatory approvals for certain drone applications and created new use cases that are likely to persist beyond the immediate crisis, contributing to a stronger post-pandemic growth trajectory.

Civil Drone Market Competitive Landscape - Major competitors and market consolidation

The civil drone market features a dynamic competitive landscape characterized by a mix of established aerospace companies, specialized drone manufacturers, and technology giants. Major players such as SZ DJI Technology Co., Ltd. dominate the consumer and commercial segments with their innovative product offerings and extensive distribution networks. Companies like Intel Corporation and Parrot SA bring significant technological expertise and R&D capabilities to the market. The landscape is witnessing increasing consolidation through strategic partnerships, mergers, and acquisitions as companies seek to expand their technological capabilities and market reach. For instance, hardware manufacturers are increasingly partnering with software companies to offer integrated solutions, while traditional aerospace firms are acquiring drone startups to enter the unmanned systems market. The competitive dynamics are further shaped by regional players who cater to specific geographic markets with localized solutions. This consolidation trend is expected to continue as the market matures, potentially leading to a more concentrated industry structure with a few dominant players offering comprehensive drone solutions across multiple applications and industries.

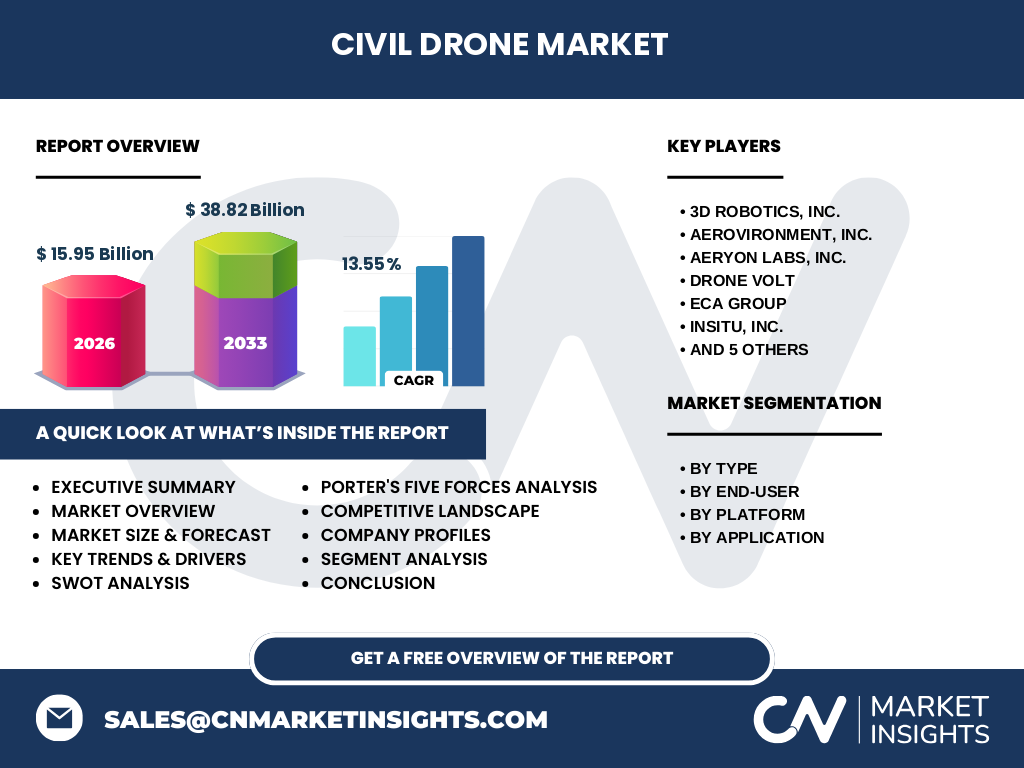

Executive Summary - High-level overview and key findings about Civil Drone Market

The civil drone market is positioned for substantial growth, with projections indicating expansion from 15.95 billion to 38.82 billion by 2033, representing a robust CAGR of 13.55%. This growth is underpinned by the technology's expanding applications across agriculture, infrastructure, energy, and real estate sectors, driven by the need for efficient data collection, monitoring, and operational capabilities. The market is characterized by rapid technological innovation, with advancements in AI integration, autonomous flight, and extended battery life opening new possibilities for drone applications. While regulatory challenges and operational limitations remain significant hurdles, the industry is witnessing increasing regulatory support for commercial drone operations, particularly in areas such as beyond visual line of sight (BVLOS) flights and autonomous delivery systems. The competitive landscape is evolving with strategic partnerships and technological convergence, as companies seek to offer integrated hardware-software solutions. Key investment opportunities lie in the development of advanced sensors, AI-powered analytics platforms, and specialized applications for emerging use cases in smart cities, environmental monitoring, and emergency response scenarios.

Civil Drone Market Forecast - Projections for 2025-2032 period

The civil drone market is projected to experience significant growth during the 2025-2032 period, building on the strong foundation established in previous years. With a current market size of 15.95 billion and a CAGR of 13.55%, the market is expected to reach approximately 38.82 billion by 2033. This growth trajectory is driven by the continued expansion of commercial applications, technological advancements in drone capabilities, and increasing regulatory support for unmanned aircraft operations. The forecast period will likely see accelerated adoption in precision agriculture, where drones are used for crop monitoring, spraying, and yield optimization. Infrastructure inspection and maintenance applications are expected to grow substantially as aging infrastructure worldwide requires more frequent and cost-effective monitoring solutions. The development of autonomous delivery systems and the expansion of BVLOS operations will create new market opportunities, particularly in logistics and emergency services. Regional markets in Asia-Pacific and North America are expected to lead growth, supported by strong technological infrastructure and favorable regulatory environments. However, market growth may be tempered by ongoing challenges related to airspace integration, privacy concerns, and the need for standardized operational protocols across different jurisdictions.

Civil Drone Market Size and Share by Segmentation - Breakdown by {segmentData}

The civil drone market can be segmented by type, end-user, platform, and application, each contributing differently to the overall market dynamics. By type, the market is divided between fixed-wing drones and rotary-wing drones, with rotary-wing drones currently dominating due to their versatility and ability to hover, making them ideal for applications like aerial photography and inspection. In terms of end-users, agriculture represents a significant segment, driven by the need for precision farming techniques, followed by real estate and infrastructure development, which utilize drones for site surveys and project monitoring. The energy and power sector is emerging as a key end-user, employing drones for infrastructure inspection and maintenance of power lines, wind turbines, and solar farms. By platform, the market is segmented into hardware, software, and services, with hardware currently accounting for the largest share due to the high cost of advanced drone systems. However, the software and services segments are expected to grow faster as the industry matures and data analytics become increasingly important. Application-wise, aerial photography continues to be a major driver, while surveying and mapping, and inspection applications are gaining traction due to their critical role in infrastructure development and maintenance.

Global Civil Drone Market Size and Share by Region - Geographic distribution

The global civil drone market exhibits varying growth patterns across different geographic regions, influenced by factors such as regulatory environments, technological infrastructure, and industry adoption rates. North America currently holds a significant share of the global market, driven by strong technological capabilities, supportive regulatory frameworks, and high adoption rates in commercial applications. The United States, in particular, leads in terms of innovation and market size, with substantial investments in drone technology across various sectors. Europe represents another major market, characterized by a growing emphasis on drone integration into national airspace systems and increasing applications in agriculture and infrastructure inspection. The Asia-Pacific region is emerging as the fastest-growing market, fueled by rapid industrialization, government initiatives supporting drone technology, and the presence of major drone manufacturers such as SZ DJI Technology Co., Ltd. Countries like China, Japan, and Australia are at the forefront of regional growth, with expanding applications in agriculture, construction, and logistics. Latin America and the Middle East & Africa regions are also showing promising growth potential, particularly in agriculture and infrastructure development, although market penetration remains lower compared to other regions due to regulatory and infrastructure challenges.

Regional Analysis of the Civil Drone Market - Detailed regional market performance

The regional performance of the civil drone market reveals distinct patterns of growth and adoption across different geographic areas. In North America, the market is characterized by advanced technological infrastructure and a mature regulatory environment, particularly in the United States where the Federal Aviation Administration (FAA) has been proactive in establishing drone operation guidelines. The region benefits from strong demand in commercial applications, including precision agriculture, infrastructure inspection, and media production. Europe presents a diverse market landscape, with countries like France and the UK leading in drone technology adoption and integration. The European Union Aviation Safety Agency (EASA) has implemented comprehensive regulations that facilitate cross-border drone operations, supporting market growth. In the Asia-Pacific region, rapid economic development and government support for technological innovation are driving significant market expansion. China, as both a major manufacturer and user of drones, plays a pivotal role in regional market dynamics. The region is witnessing increasing adoption in agriculture, construction, and logistics applications. Latin America and the Middle East & Africa regions are experiencing gradual market growth, primarily driven by agriculture and infrastructure development needs, although regulatory frameworks and technological infrastructure remain areas for improvement.

Leading Company Profiles in the Civil Drone Market - Industry players and strategies

The civil drone market features several key players with distinct strategic approaches and market positioning. SZ DJI Technology Co., Ltd. stands out as a global leader, particularly strong in consumer and commercial drone segments, with a focus on innovation in camera technology and flight control systems. 3D Robotics, Inc. has established itself as a significant player in the enterprise drone market, emphasizing software integration and data analytics capabilities. Aerovironment, Inc. specializes in military and commercial drones, with a strong focus on tactical unmanned aircraft systems and electric vehicle charging solutions. Parrot SA, a French company, offers a diverse portfolio ranging from consumer drones to professional solutions for agriculture and inspection. Yuneec International, based in China, competes in the consumer and commercial markets with an emphasis on electric aviation technology. Precisionhawk Inc. has carved out a niche in data analytics and drone-based mapping solutions, particularly for agriculture and construction. These companies are pursuing various strategies including product innovation, strategic partnerships, and geographic expansion to strengthen their market positions and address the evolving needs of different industry verticals.

Porter's Five Forces Analysis of the Civil Drone Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the civil drone market. The threat of new entrants is moderate to high, as technological advancements have lowered barriers to entry, allowing new companies to develop specialized drone solutions. However, established players benefit from brand recognition, extensive distribution networks, and regulatory compliance experience. The bargaining power of suppliers is relatively low due to the availability of multiple component suppliers and the commoditization of certain drone parts. Conversely, the bargaining power of buyers is increasing as they become more informed and demand integrated solutions combining hardware, software, and services. The threat of substitutes is moderate, with alternative technologies such as satellites and manned aircraft offering some competition, particularly for large-scale mapping and surveillance applications. Competitive rivalry within the industry is intense, characterized by rapid technological innovation, price competition, and the constant introduction of new features and capabilities. Companies are increasingly focusing on software and data analytics to differentiate their offerings and create higher switching costs for customers. The overall industry attractiveness is high, driven by growing market demand and technological opportunities, but companies must navigate complex regulatory environments and address concerns about privacy and safety to maintain competitive advantage.

SWOT Analysis of the Civil Drone Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the civil drone market reveals several key factors influencing its development and growth potential. Strengths of the market include rapid technological advancements in drone capabilities, increasing applications across diverse industries, and growing acceptance of drone technology for commercial use. The market benefits from strong R&D investments, leading to innovations in battery life, payload capacity, and autonomous flight capabilities. However, weaknesses exist in the form of regulatory challenges that vary by region, limited flight times due to battery constraints, and the need for skilled operators to manage complex drone systems. Opportunities in the market are abundant, including the expansion of drone applications in emerging areas such as delivery services, emergency response, and environmental monitoring. The development of beyond visual line of sight (BVLOS) operations and the integration of drones with 5G networks present significant growth avenues. Threats to the market include potential privacy concerns and public resistance to drone operations, cybersecurity risks associated with connected drone systems, and the possibility of stricter regulations in response to safety incidents or misuse of drone technology. Additionally, economic downturns could impact investment in drone technology across various sectors.

Civil Drone Market Value Chain Analysis - Industry structure and value flow

The civil drone market value chain encompasses multiple stages, from component manufacturing to end-user applications, with value added at each step. At the beginning of the chain, component manufacturers produce essential parts such as motors, electronic speed controllers, flight controllers, and sensors. These components are then integrated by drone manufacturers to create complete systems, with companies like SZ DJI Technology Co., Ltd. and Parrot SA adding significant value through design, software integration, and quality control. The next stage involves distributors and retailers who facilitate the market reach of drone products to various end-users. Service providers play a crucial role in the value chain by offering specialized applications such as aerial photography, surveying, mapping, and inspection services. These service providers often add substantial value by combining drone operations with data analytics and industry-specific expertise. At the end of the chain, software developers create value-added applications for data processing, analysis, and visualization, which are critical for translating raw drone data into actionable insights. The value chain is characterized by increasing integration between hardware and software providers, with companies seeking to offer comprehensive solutions that address specific industry needs. This integration is creating new opportunities for value creation, particularly in areas such as AI-powered analytics and real-time data processing.

Key Investment Insights in the Civil Drone Market - Strategic investment recommendations

The civil drone market presents several compelling investment opportunities driven by technological advancements and expanding applications across industries. Strategic investments in companies developing advanced sensors and imaging technologies are particularly promising, as these components are critical for enhancing drone capabilities in areas such as precision agriculture and infrastructure inspection. The software and data analytics segment represents another attractive investment area, with growing demand for platforms that can process and analyze the vast amounts of data collected by drones. Investments in companies working on beyond visual line of sight (BVLOS) technology and drone traffic management systems (UTM) are likely to yield significant returns as regulatory frameworks evolve to support more complex drone operations. The emerging market for autonomous delivery drones and urban air mobility solutions offers high growth potential, albeit with higher regulatory and technical risks. Additionally, investments in companies developing hybrid and hydrogen fuel cell-powered drones could be strategic, given the industry's need for extended flight times and reduced environmental impact. For investors seeking exposure to the market, a diversified approach across hardware manufacturers, software developers, and service providers may help mitigate risks while capturing growth across different segments of the value chain.

Civil Drone Market Conclusion - Summary and key takeaways

The civil drone market is on a robust growth trajectory, with projections indicating expansion from 15.95 billion to 38.82 billion by 2033, representing a CAGR of 13.55%. This growth is driven by the technology's expanding applications across agriculture, infrastructure, energy, and real estate sectors, supported by continuous technological advancements in AI integration, autonomous flight, and extended battery life. While the market faces challenges including regulatory hurdles, privacy concerns, and operational limitations, the overall industry outlook remains positive. Key trends shaping the market include the development of hybrid power systems, the emergence of drone-in-a-box solutions, and the increasing convergence of drones with IoT and 5G technologies. The competitive landscape is characterized by a mix of established aerospace companies, specialized drone manufacturers, and technology giants, with ongoing consolidation through strategic partnerships and acquisitions. For stakeholders, the market presents significant opportunities in areas such as precision agriculture, infrastructure inspection, and autonomous delivery systems. Success in this evolving market will depend on companies' ability to navigate complex regulatory environments, address safety and privacy concerns, and deliver integrated solutions that meet the specific needs of different industry verticals.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology combining both primary and secondary research approaches. Primary research involved interviews with industry experts, drone manufacturers, end-users, and regulatory bodies to gather firsthand insights into market dynamics, technological trends, and application-specific requirements. Secondary research encompassed the analysis of company annual reports, financial statements, industry publications, and regulatory documents to validate market size estimates and growth projections. Data triangulation techniques were employed to cross-verify information from multiple sources, ensuring the accuracy and reliability of the findings. The research methodology also included a detailed analysis of patent filings, product launches, and strategic developments by key market players to understand competitive positioning and technological trends. Market size calculations were based on a bottom-up approach, considering individual segment revenues and extrapolating to the total market. Regional market analyses were conducted by examining country-specific adoption rates, regulatory environments, and economic factors influencing drone technology implementation. The forecast period of 2025-2032 was determined based on current market trends, technological roadmaps, and anticipated regulatory developments.

Research Scope - Coverage and limitations

This research report covers the global civil drone market, focusing on commercial and non-military applications of unmanned aerial vehicles across various industries and use cases. The scope includes an analysis of market size, growth trends, competitive landscape, and regional performance, with projections extending to 2033. The report examines key market segments including type (fixed-wing and rotary-wing drones), end-user industries (agriculture, real estate/infrastructure, energy and power), platforms (hardware, software, services), and applications (aerial photography, surveying & mapping, inspection). The research also covers major geographic regions including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. However, it's important to note certain limitations in the research scope. The report does not cover military drone applications or consumer drone use for personal recreation, focusing exclusively on commercial and civil applications. Additionally, while the research provides comprehensive market analysis, specific financial figures for individual companies or detailed market share breakdowns by country are not included due to data availability constraints. The report also does not delve into highly specialized niche applications that may represent a small fraction of the overall market.

Key Companies and Recent Developments in the Civil Drone Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The civil drone market features several prominent companies driving innovation and market growth through strategic developments and product launches. SZ DJI Technology Co., Ltd. continues to lead the market with its advanced consumer and commercial drone offerings, recently announcing the expansion of its agricultural drone lineup with enhanced spraying capabilities and AI-powered crop analysis features. 3D Robotics, Inc. has strengthened its position in the enterprise market through partnerships with major software companies to integrate drone data with enterprise resource planning systems. Aerovironment, Inc. has made significant strides in the defense and commercial sectors, launching new tactical unmanned aircraft systems with improved endurance and payload capacity. Parrot SA has focused on developing specialized solutions for agriculture and inspection, with recent announcements including the launch of a new drone-based crop monitoring system that integrates with precision farming software. Intel Corporation has leveraged its expertise in AI and computer vision to enhance drone capabilities for industrial inspections and public safety applications. Yuneec International has expanded its product portfolio with the introduction of hybrid VTOL (vertical take-off and landing) drones designed for long-range commercial operations. These companies, along with others like Drone Volt, ECA Group, Insitu Inc., Precisionhawk Inc., and Aeryon Labs Inc., continue to shape the market through ongoing research and development efforts, strategic partnerships, and targeted product innovations aimed at addressing specific industry needs and regulatory requirements.