Modular Data Center Market Overview - Definition, scope, and significance

A modular data center is a portable, scalable, and pre-engineered data center facility that can be rapidly deployed to meet growing computing demands. Unlike traditional brick-and-mortar data centers, modular data centers are built using standardized components and can be shipped as complete units or as containerized solutions. The scope of this market encompasses various form factors including ISO containers, skid-mounted systems, and enclosures, serving diverse end-user segments such as IT and telecom, BFSI, healthcare, government, and media and entertainment. The significance of modular data centers lies in their ability to provide cost-effective, energy-efficient, and quickly deployable infrastructure solutions that address the challenges of traditional data center construction, including long deployment times, high capital expenditure, and inflexible scaling capabilities.

Modular Data Center Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The modular data center market is driven by several key factors including the exponential growth of data generation, increasing adoption of cloud computing, and the need for edge computing infrastructure to support IoT applications. Organizations are seeking flexible and scalable solutions to manage their growing IT infrastructure requirements while minimizing capital expenditure and deployment time. However, the market faces restraints such as high initial investment costs, concerns about security and compliance in portable data centers, and the technical challenges associated with integrating modular solutions with existing IT infrastructure. Challenges include managing power and cooling requirements in compact spaces, ensuring reliability and redundancy, and addressing the skills gap in deploying and maintaining modular data centers. Despite these challenges, significant opportunities exist in emerging markets, the growing demand for disaster recovery solutions, and the increasing need for temporary or rapid-deployment data centers in remote locations or during emergencies.

Modular Data Center Market Growth Trends - Current and emerging trends shaping the market

The modular data center market is experiencing several transformative trends that are shaping its evolution. One prominent trend is the increasing adoption of prefabricated and pre-engineered modular solutions that can be deployed 30-50% faster than traditional data centers. Another significant trend is the integration of advanced cooling technologies and energy-efficient designs to reduce operational costs and environmental impact. The market is also witnessing a shift towards micro data centers and edge computing solutions to support low-latency applications and IoT deployments. Additionally, there is a growing emphasis on modular data centers with built-in disaster recovery capabilities and enhanced security features. The trend towards hybrid cloud architectures is driving demand for modular solutions that can seamlessly integrate with both on-premises and cloud environments, while the increasing focus on sustainability is leading to the development of green modular data centers with renewable energy integration.

COVID-19 Impact on the Modular Data Center Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the modular data center market, initially causing supply chain disruptions and project delays due to lockdowns and restrictions. However, the pandemic also accelerated the digital transformation across industries, leading to increased demand for data center infrastructure to support remote work, online services, and digital operations. The need for rapid deployment of IT infrastructure to enable business continuity drove organizations to consider modular data center solutions that could be implemented quickly compared to traditional facilities. As businesses adapted to the new normal, the market witnessed a recovery trajectory characterized by increased investments in digital infrastructure, growing demand for edge computing solutions, and the adoption of hybrid work models that require flexible and scalable data center solutions. The pandemic highlighted the importance of resilient and adaptable IT infrastructure, positioning modular data centers as a viable solution for future-proofing organizational IT capabilities.

Modular Data Center Market Competitive Landscape - Major competitors and market consolidation

The modular data center market features a competitive landscape with several major players and emerging companies vying for market share. Key competitors include established technology giants such as Dell Technologies, Hewlett Packard Enterprise, and Huawei Digital Power Technologies, alongside specialized infrastructure providers like Vertiv Group, Schneider Electric, and Rittal GmbH. The market is characterized by strategic partnerships, mergers, and acquisitions as companies seek to expand their product portfolios and geographic presence. Competition is intensifying as players focus on innovation, offering integrated solutions that combine hardware, software, and services. The market is also witnessing increased collaboration between technology providers and system integrators to deliver end-to-end modular data center solutions. While the market remains relatively fragmented with numerous regional players, larger companies are gaining prominence through their comprehensive product offerings, global presence, and strong customer relationships.

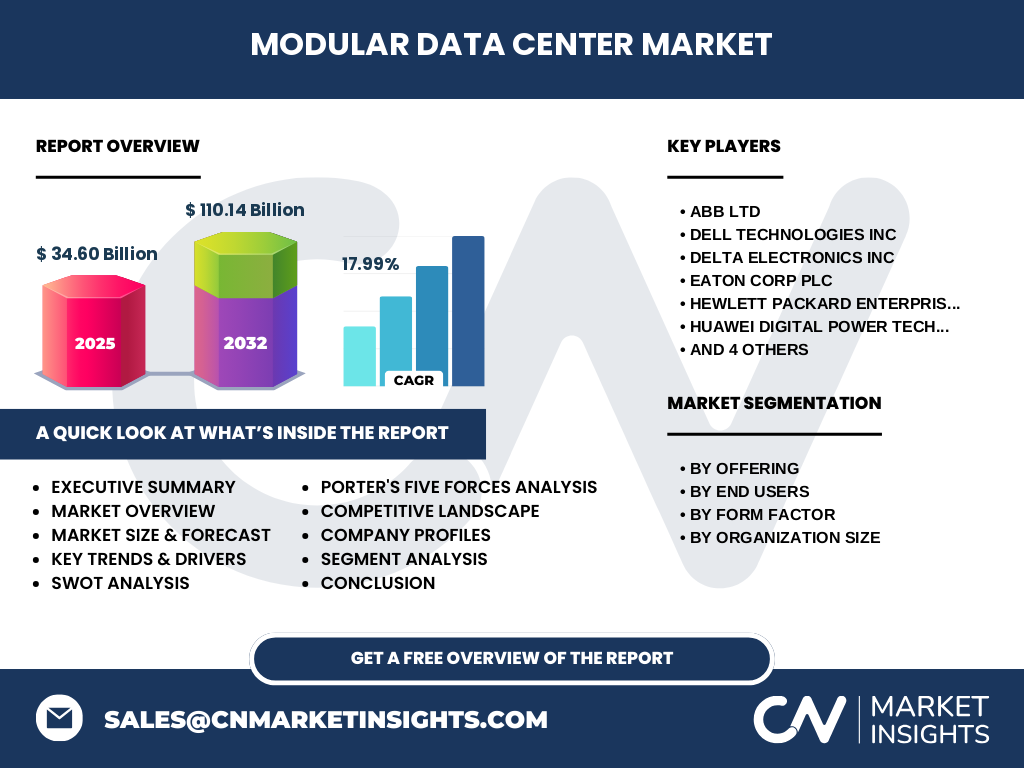

Executive Summary - High-level overview and key findings about Modular Data Center Market

The modular data center market represents a dynamic and rapidly evolving segment of the data center industry, offering innovative solutions to address the growing demand for flexible, scalable, and efficient IT infrastructure. With a market size of USD 34.60 billion in 2025 and projected to reach USD 110.14 billion by 2032, the market is experiencing robust growth driven by a CAGR of 17.99%. The market is characterized by diverse offerings including solutions and services, catering to various end-user segments across different organization sizes. Key trends include the increasing adoption of edge computing, the integration of advanced cooling technologies, and the growing emphasis on sustainability. While the market faces challenges related to initial investment costs and technical integration, significant opportunities exist in emerging markets and the growing demand for disaster recovery solutions. The competitive landscape is marked by strategic partnerships and innovation as companies strive to differentiate their offerings and capture market share in this expanding industry.

Modular Data Center Market Forecast - Projections for 2025-2032 period

The modular data center market is poised for substantial growth over the forecast period from 2025 to 2032, with projections indicating a significant expansion from USD 34.60 billion in 2025 to USD 110.14 billion by 2032. This remarkable growth trajectory represents a compound annual growth rate (CAGR) of 17.99%, reflecting the increasing adoption of modular data center solutions across various industries and regions. The forecast period is expected to witness continued innovation in modular data center technologies, with advancements in cooling systems, power efficiency, and integration capabilities driving market expansion. The growth will be fueled by the increasing demand for edge computing infrastructure, the proliferation of IoT devices, and the ongoing digital transformation initiatives across enterprises of all sizes. Additionally, the market is expected to benefit from the growing emphasis on sustainability and energy efficiency, as organizations seek to reduce their carbon footprint while meeting their expanding IT infrastructure needs.

Modular Data Center Market Size and Share by Segmentation - Breakdown by {segmentData}

The modular data center market exhibits diverse segmentation across multiple dimensions, reflecting the varied needs of different industries and organization sizes. By offering, the market is divided into solutions and services, with solutions typically comprising the larger share due to the core infrastructure requirements. In terms of end users, the IT and telecom sector dominates the market, followed by BFSI, healthcare, government, and media and entertainment segments, each with distinct requirements for data center infrastructure. The form factor segmentation includes ISO containers, skid-mounted systems, and enclosures, with ISO containers gaining popularity for their portability and scalability. Organization size segmentation reveals that large enterprises currently account for a significant market share due to their extensive IT infrastructure needs, while the SME segment is expected to witness faster growth as modular solutions become more accessible and cost-effective for smaller organizations. This multi-dimensional segmentation highlights the market's ability to cater to diverse customer needs and its potential for continued expansion across different segments.

Global Modular Data Center Market Size and Share by Region - Geographic distribution

The global modular data center market exhibits varying growth patterns and adoption rates across different regions, reflecting the diverse technological infrastructure and economic conditions worldwide. North America currently leads the market, driven by the presence of major technology companies, early adoption of advanced data center solutions, and significant investments in digital infrastructure. Europe follows as the second-largest market, characterized by stringent data protection regulations and a strong focus on energy-efficient solutions. The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, fueled by rapid digitalization, increasing cloud adoption, and expanding IT infrastructure in emerging economies such as China and India. Latin America and the Middle East & Africa regions are also showing promising growth potential, albeit from a smaller base, driven by increasing internet penetration and government initiatives to develop digital infrastructure. The regional distribution of the market underscores the global nature of the modular data center industry and its ability to address diverse market needs across different geographic areas.

Regional Analysis of the Modular Data Center Market - Detailed regional market performance

Regional analysis of the modular data center market reveals distinct characteristics and growth drivers across different geographic areas. In North America, the market is characterized by high adoption rates of advanced technologies, strong presence of major data center operators, and significant investments in edge computing infrastructure. The region's mature IT ecosystem and focus on innovation drive demand for cutting-edge modular solutions. Europe's market is shaped by strict environmental regulations and energy efficiency standards, leading to increased adoption of green modular data centers. The region also benefits from a well-established digital infrastructure and growing demand for data sovereignty solutions. The Asia-Pacific region presents a dynamic market landscape, with rapid urbanization, expanding digital economies, and government initiatives driving growth. Countries like China, Japan, and India are witnessing significant investments in data center infrastructure to support their growing digital economies. Latin America and the Middle East & Africa regions, while currently smaller markets, are showing increasing potential due to improving internet connectivity, rising smartphone penetration, and growing awareness of the benefits of modular data center solutions.

Leading Company Profiles in the Modular Data Center Market - Industry players and strategies

The modular data center market features several prominent players employing diverse strategies to maintain their competitive edge. ABB Ltd focuses on providing integrated electrical solutions and automation technologies for modular data centers, emphasizing energy efficiency and reliability. Dell Technologies leverages its extensive portfolio of IT infrastructure solutions to offer comprehensive modular data center offerings, targeting both enterprise and service provider markets. Delta Electronics specializes in power management and thermal solutions, positioning itself as a key player in the energy-efficient modular data center segment. Eaton Corp Plc brings its expertise in power management to deliver innovative modular solutions with advanced UPS systems and intelligent power distribution. Hewlett Packard Enterprise combines its server and storage technologies with modular infrastructure to provide end-to-end data center solutions. Huawei Digital Power Technologies leverages its strong presence in the Asia-Pacific region to offer integrated power and cooling solutions for modular data centers. PCX Holding LLC focuses on providing customizable modular solutions for various industries, while Rittal GmbH & Co KG emphasizes its expertise in enclosure systems and thermal management. Schneider Electric SE positions itself as a leader in sustainable energy management solutions, and Vertiv Group Corp specializes in critical infrastructure technologies for data centers of all sizes.

Porter's Five Forces Analysis of the Modular Data Center Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the modular data center market. The threat of new entrants is moderate, as the market requires significant capital investment and technical expertise, but lower barriers to entry compared to traditional data centers create opportunities for innovative startups. The bargaining power of buyers is relatively high due to the availability of multiple vendors and the commoditization of certain components, forcing companies to differentiate through value-added services and customization options. Suppliers' bargaining power varies depending on the component, with some specialized parts having limited suppliers, while standardized components are readily available from multiple sources. The threat of substitute products is moderate, as traditional data centers and cloud services can serve as alternatives, but the unique benefits of modular solutions in terms of speed and flexibility provide a competitive advantage. Competitive rivalry is intense, with numerous players competing on price, technology, and service offerings, driving continuous innovation and market consolidation through strategic partnerships and acquisitions.

SWOT Analysis of the Modular Data Center Market - Strengths, weaknesses, opportunities, threats

A comprehensive SWOT analysis of the modular data center market reveals several key factors influencing its growth and development. Strengths include the rapid deployment capabilities of modular solutions, scalability to meet changing demands, and potential for cost savings compared to traditional data centers. The flexibility to deploy in various environments and the integration of advanced technologies are additional strengths that position modular data centers as attractive solutions for modern IT infrastructure needs. Weaknesses include the perception of lower reliability compared to traditional data centers, potential security concerns in portable solutions, and the challenge of integrating with existing legacy systems. Opportunities abound in emerging markets, the growing demand for edge computing infrastructure, and the increasing focus on sustainable and energy-efficient data center solutions. The market can also capitalize on the rising adoption of IoT devices and the need for disaster recovery solutions. Threats include intense competition leading to price pressures, rapid technological changes that may render current solutions obsolete, and potential economic downturns affecting IT spending. Additionally, regulatory challenges and environmental concerns related to data center operations pose ongoing threats to market growth.

Modular Data Center Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the modular data center market reveals a complex ecosystem of interconnected activities and stakeholders. At the core of the value chain are the technology providers who design and manufacture modular data center components, including servers, storage systems, networking equipment, and power distribution units. These components are then integrated by system integrators and solution providers who assemble complete modular data center solutions tailored to specific customer requirements. The value chain also includes component suppliers who provide raw materials and specialized parts, as well as software developers who create management and monitoring solutions for modular data centers. Distribution channels play a crucial role in bringing these solutions to end-users, with direct sales teams, channel partners, and system integrators serving as key intermediaries. The value chain extends to service providers who offer installation, maintenance, and support services throughout the lifecycle of modular data centers. Finally, end-users across various industries, including IT and telecom, BFSI, healthcare, government, and media and entertainment, form the ultimate beneficiaries of the value created by this ecosystem, driving demand for innovative and efficient modular data center solutions.

Key Investment Insights in the Modular Data Center Market - Strategic investment recommendations

Investment insights in the modular data center market highlight several strategic opportunities for stakeholders looking to capitalize on the market's growth potential. Investors should focus on companies that are developing innovative cooling technologies and energy-efficient solutions, as sustainability becomes increasingly important in data center operations. There is significant potential in companies offering integrated edge computing solutions, as the demand for low-latency processing continues to grow with the proliferation of IoT devices. Investments in firms with strong capabilities in artificial intelligence and machine learning for data center management and optimization are likely to yield substantial returns, given the increasing complexity of IT infrastructure. The market for modular data centers in emerging economies presents attractive investment opportunities, particularly in regions experiencing rapid digital transformation. Additionally, companies that can provide comprehensive lifecycle services, including design, deployment, and ongoing management of modular data centers, are well-positioned for growth. Investors should also consider opportunities in the development of modular data centers specifically designed for harsh environments or disaster-prone areas, as these specialized solutions address critical infrastructure needs in various regions.

Modular Data Center Market Conclusion - Summary and key takeaways

The modular data center market represents a dynamic and rapidly evolving segment of the broader data center industry, offering innovative solutions to address the growing demand for flexible, scalable, and efficient IT infrastructure. With a market size of USD 34.60 billion in 2025 and projected to reach USD 110.14 billion by 2032, growing at a CAGR of 17.99%, the market demonstrates significant growth potential driven by factors such as increasing data generation, cloud adoption, and the need for edge computing infrastructure. The market's diverse segmentation across offerings, end-users, form factors, and organization sizes highlights its ability to cater to a wide range of customer needs and its potential for continued expansion. While facing challenges related to initial investment costs and technical integration, the market presents numerous opportunities in emerging markets, disaster recovery solutions, and the growing demand for sustainable data center infrastructure. The competitive landscape is characterized by innovation and strategic partnerships as key players strive to differentiate their offerings and capture market share. As organizations across industries continue to prioritize digital transformation and resilient IT infrastructure, the modular data center market is well-positioned for sustained growth and technological advancement in the coming years.

Research Methodology - How this research was conducted

The research methodology for this modular data center market analysis involved a comprehensive approach combining primary and secondary research techniques to ensure accurate and reliable findings. Primary research included interviews with industry experts, key opinion leaders, and executives from leading companies in the modular data center ecosystem. These interviews provided valuable insights into market trends, competitive dynamics, and future growth prospects. Secondary research involved extensive analysis of industry reports, company annual reports, press releases, and other relevant documents to gather quantitative and qualitative data on market size, segmentation, and regional performance. The research also incorporated data from trade associations, government publications, and technology forums to validate findings and ensure a holistic view of the market. Market size and forecast calculations were based on a combination of top-down and bottom-up approaches, considering factors such as technological advancements, economic conditions, and industry-specific trends. The research methodology was designed to provide a robust and comprehensive analysis of the modular data center market, offering stakeholders valuable insights for strategic decision-making.

Research Scope - Coverage and limitations

The research scope for this modular data center market analysis encompasses a comprehensive examination of the global market, covering key aspects such as market size, growth trends, competitive landscape, and regional performance. The study focuses on the period from 2025 to 2032, with 2025 as the base year, providing insights into historical trends and future projections. The research covers various market segments including offerings (solutions and services), end-users (IT and telecom, BFSI, healthcare, government, and media and entertainment), form factors (ISO containers, skid-mounted systems, and enclosures), and organization sizes (large enterprises and SMEs). The geographic scope includes major regions such as North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. While the research provides a detailed analysis of the market's current state and future prospects, it is important to note that the study's limitations include potential variations in market conditions due to unforeseen economic or geopolitical events, the rapidly evolving nature of technology that may impact market dynamics, and the challenge of obtaining precise data for certain niche segments or emerging markets. Despite these limitations, the research aims to provide a comprehensive and insightful overview of the modular data center market to support informed decision-making by industry stakeholders.

Key Companies and Recent Developments in the Modular Data Center Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The modular data center market has witnessed significant activity from key players, with companies introducing innovative solutions and forming strategic partnerships to strengthen their market position. ABB Ltd recently announced the expansion of its modular data center portfolio with enhanced energy management capabilities, focusing on improving efficiency and reducing operational costs for customers. Dell Technologies launched a new line of modular data center solutions designed specifically for edge computing applications, featuring advanced cooling technologies and integrated management software. Delta Electronics unveiled its latest modular data center platform with improved power density and smart monitoring capabilities, targeting the growing demand for high-performance computing infrastructure. Eaton Corp Plc introduced a new range of modular UPS systems with increased scalability and energy efficiency, catering to the needs of large enterprises and hyperscale data center operators. Hewlett Packard Enterprise announced a strategic partnership with a leading cloud service provider to deliver integrated modular data center solutions for hybrid cloud environments. Huawei Digital Power Technologies launched its next-generation modular data center solution with advanced AI-powered management features, emphasizing its commitment to innovation in the Asian market. PCX Holding LLC expanded its product offerings with the introduction of customizable modular solutions for harsh environments, addressing the needs of industries such as oil and gas and mining. Rittal GmbH & Co KG unveiled its latest enclosure systems with improved thermal management and cybersecurity features, targeting the growing concerns around data center security. Schneider Electric SE announced a collaboration with a major technology company to develop sustainable modular data center solutions with integrated renewable energy systems. Vertiv Group Corp launched its new edge computing platform with modular components designed for rapid deployment in urban environments, focusing on the increasing demand for localized data processing capabilities.