North America Specialty Hospitals Market Overview - Definition, scope, and significance

The North America Specialty Hospitals Market represents a critical segment of the healthcare industry, focusing on facilities that provide specialized medical services for specific patient populations or conditions. These hospitals are distinguished from general acute care hospitals by their concentrated expertise in particular medical fields, such as oncology, pediatrics, rehabilitation, or cardiology. The market encompasses both inpatient and outpatient services across public and private hospital settings, serving as essential healthcare providers that deliver advanced, targeted care for complex medical conditions. With the healthcare landscape evolving toward more specialized and personalized treatment approaches, specialty hospitals play a pivotal role in improving patient outcomes through focused expertise, state-of-the-art technology, and streamlined care pathways. The significance of this market lies in its ability to address specific healthcare needs with higher efficiency and potentially better clinical results than general hospitals, while also contributing to healthcare innovation through specialized research and treatment protocols.

North America Specialty Hospitals Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The North America Specialty Hospitals Market is propelled by several key drivers, including the rising prevalence of chronic diseases, an aging population requiring specialized care, and increasing demand for outpatient services due to their cost-effectiveness and convenience. Technological advancements in medical equipment and treatment methodologies are enabling specialty hospitals to offer cutting-edge therapies, while growing healthcare expenditure and insurance coverage expansion support market growth. However, the market faces significant restraints such as high operational costs, stringent regulatory requirements, and workforce shortages in specialized medical fields. Challenges include reimbursement complexities, the need for continuous technological upgrades, and competition from general hospitals expanding their specialty services. Despite these obstacles, substantial opportunities exist in the form of telehealth integration, personalized medicine advancements, and the growing focus on preventive care. The market also benefits from increasing public-private partnerships and the potential for expansion into underserved regions, creating avenues for specialty hospitals to enhance their service offerings and reach new patient populations.

North America Specialty Hospitals Market Growth Trends - Current and emerging trends shaping the market

The North America Specialty Hospitals Market is experiencing transformative growth trends driven by evolving healthcare needs and technological innovations. One prominent trend is the shift toward outpatient-focused care models, with many specialty hospitals expanding their ambulatory services to provide cost-effective treatments outside traditional inpatient settings. The integration of artificial intelligence and machine learning in diagnostic and treatment processes is enhancing clinical decision-making and operational efficiency. Another significant trend is the emphasis on value-based care, where specialty hospitals are aligning their services with outcome-based reimbursement models to improve patient care quality while managing costs. The market is also witnessing the rise of specialized rehabilitation and long-term care facilities, particularly for aging populations and post-acute care patients. Emerging trends include the adoption of robotic surgery systems, expansion of telemedicine services for specialty consultations, and the development of integrated care delivery networks that connect specialty hospitals with primary care providers and community health resources. These trends collectively indicate a market moving toward more specialized, technology-driven, and patient-centric care delivery models.

COVID-19 Impact on the North America Specialty Hospitals Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has had a profound impact on the North America Specialty Hospitals Market, initially causing significant disruptions in elective procedures and routine specialty care as healthcare resources were redirected to pandemic response. Many specialty hospitals experienced reduced patient volumes, particularly in areas like elective surgeries and non-emergency consultations, leading to financial strain and operational challenges. The pandemic accelerated the adoption of telehealth and remote monitoring technologies, forcing specialty hospitals to rapidly implement digital solutions for patient care and consultation. However, the crisis also highlighted the critical role of specialty hospitals in managing complex cases and providing essential care for patients with chronic conditions who were at higher risk from COVID-19 complications. As the market recovers, specialty hospitals are focusing on building more resilient operational models, enhancing infection control protocols, and developing hybrid care delivery systems that combine in-person and virtual services. The recovery trajectory shows a gradual return to pre-pandemic service levels, with an increased emphasis on preparedness for future healthcare crises and the integration of pandemic lessons into long-term strategic planning.

North America Specialty Hospitals Market Competitive Landscape - Major competitors and market consolidation

The North America Specialty Hospitals Market features a competitive landscape characterized by a mix of large healthcare systems, specialized independent facilities, and regional providers. Major competitors include established healthcare giants such as HCA Healthcare, Universal Health Services Inc., and Community Health Systems Inc., which operate extensive networks of specialty hospitals across multiple states. These large players benefit from economies of scale, strong brand recognition, and comprehensive service offerings that span various medical specialties. The market also includes specialized institutions like Cleveland Clinic, Johns Hopkins Medicine, and Memorial Sloan Kettering Cancer Center, which have built reputations for excellence in specific medical fields and attract patients seeking top-tier specialized care. Market consolidation is evident through mergers, acquisitions, and strategic partnerships, as healthcare systems seek to expand their geographic reach and service capabilities. Competition is intensifying in areas such as technological innovation, patient experience, and the ability to offer integrated care pathways. The competitive landscape is further shaped by the entry of new players and the expansion of existing facilities into emerging specialty areas, creating a dynamic environment where differentiation through quality, innovation, and specialized expertise is crucial for market success.

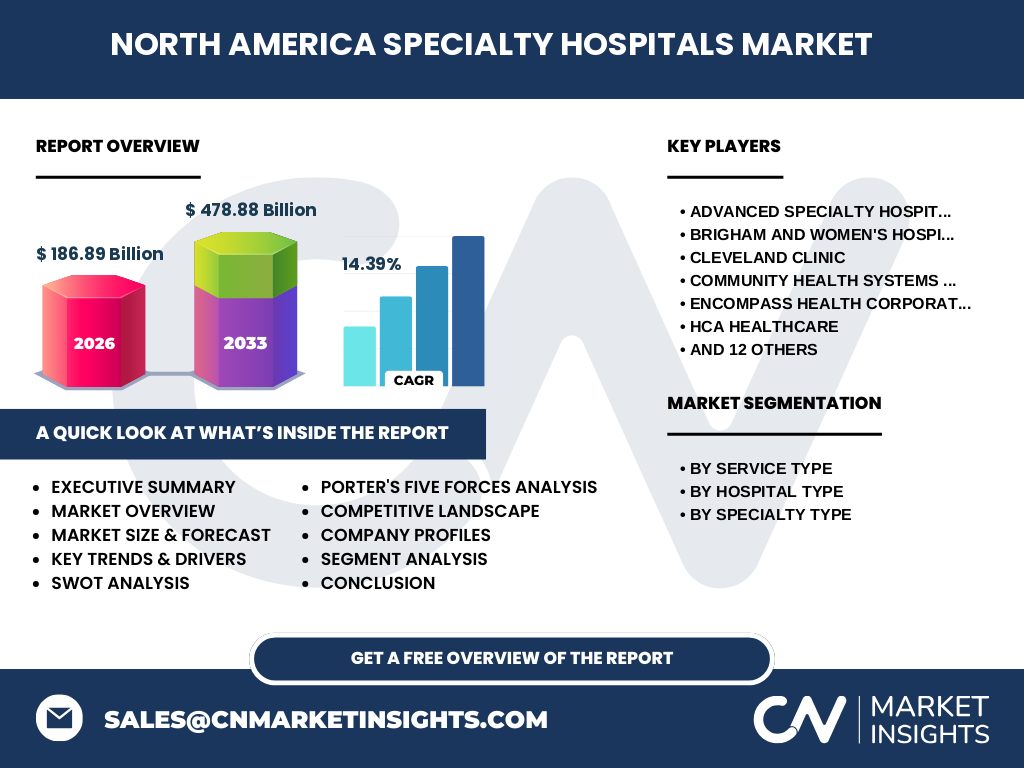

Executive Summary - High-level overview and key findings about North America Specialty Hospitals Market

The North America Specialty Hospitals Market is positioned for substantial growth, with market size projected to reach $186.89 billion by 2026, expanding to $478.88 billion by 2033 at a robust CAGR of 14.39%. This growth trajectory reflects the increasing demand for specialized healthcare services driven by demographic shifts, chronic disease prevalence, and technological advancements in medical treatment. The market demonstrates strong segmentation across service types, hospital ownership structures, and medical specialties, with outpatient services gaining prominence alongside traditional inpatient care. Key findings indicate that pediatric hospitals, oncology centers, and rehabilitation facilities represent significant growth segments, while public and private hospitals continue to play complementary roles in service delivery. The competitive landscape features established healthcare systems alongside specialized institutions, with market dynamics shaped by consolidation trends and the pursuit of technological innovation. Regional variations in market development highlight opportunities for expansion in underserved areas, while the integration of digital health solutions and value-based care models emerges as a critical success factor. Overall, the market presents a compelling growth story supported by strong fundamentals, evolving care delivery models, and the healthcare industry's increasing focus on specialized, high-quality patient care.

North America Specialty Hospitals Market Forecast - Projections for 2025-2032 period

The North America Specialty Hospitals Market is projected to experience significant expansion during the 2025-2032 period, building upon the strong foundation established in previous years. Starting from a market size of $186.89 billion in 2026, the market is forecast to reach $478.88 billion by 2033, representing a compound annual growth rate of 14.39%. This robust growth projection reflects multiple converging factors, including the continued aging of the population, rising prevalence of chronic and complex medical conditions, and increasing healthcare expenditure across North America. The forecast period will likely see accelerated adoption of advanced medical technologies, expansion of outpatient specialty services, and growing integration of digital health solutions into specialty hospital operations. Key growth drivers during this period include the increasing demand for specialized cancer treatment centers, rehabilitation facilities, and pediatric specialty hospitals. The market is also expected to benefit from ongoing healthcare reforms, insurance coverage expansions, and the shift toward value-based care models. However, the forecast acknowledges potential challenges such as regulatory changes, workforce shortages, and economic uncertainties that could impact growth rates. Overall, the 2025-2032 projection indicates a market characterized by strong demand fundamentals, technological innovation, and evolving care delivery models that support sustained expansion in the specialty hospital sector.

North America Specialty Hospitals Market Size and Share by Segmentation - Breakdown by {segmentData}

The North America Specialty Hospitals Market exhibits distinct segmentation patterns across service types, hospital ownership structures, and medical specialties. By service type, the market is divided between outpatient and inpatient services, with outpatient services gaining increasing market share due to their cost-effectiveness and patient convenience. The outpatient segment is particularly strong in rehabilitation, diagnostic services, and minor surgical procedures, reflecting the healthcare industry's shift toward ambulatory care models. By hospital type, the market encompasses both public hospitals, which often serve broader community needs and receive government funding, and private hospitals, which typically offer more specialized services and operate on a for-profit or non-profit basis. The private segment currently dominates the market, driven by higher investment capacity and ability to adopt advanced technologies. By specialty type, the market demonstrates diverse segmentation with pediatric hospitals addressing specialized children's healthcare needs, obstetrics-gynecology hospitals focusing on women's health, and oncology hospitals providing cancer treatment services. Other significant specialty segments include ENT hospitals, rehabilitation hospitals for post-acute care, orthopedic hospitals for musculoskeletal conditions, neurology hospitals for brain and nervous system disorders, cardiology hospitals for heart-related conditions, and IVF hospitals for fertility treatments. This comprehensive segmentation allows for targeted service delivery and specialized expertise development across different medical domains.

Global North America Specialty Hospitals Market Size and Share by Region - Geographic distribution

The North America Specialty Hospitals Market demonstrates varied geographic distribution across the United States, Canada, and Mexico, with the United States representing the dominant share of the regional market. Within the United States, market concentration is highest in major metropolitan areas and regions with large populations, advanced healthcare infrastructure, and higher healthcare spending capacity. States such as California, Texas, Florida, and New York lead in specialty hospital development due to their large patient populations, strong healthcare economies, and concentration of medical research institutions. The geographic distribution reflects healthcare accessibility patterns, with urban centers hosting a higher density of specialty hospitals compared to rural areas where healthcare resources are more limited. Canada's specialty hospital market, while smaller in absolute terms, shows strong development in provinces with universal healthcare systems and established medical research communities, particularly in Ontario, Quebec, and British Columbia. Mexico's specialty hospital market is experiencing growth, particularly in major cities like Mexico City, Monterrey, and Guadalajara, driven by increasing healthcare investment and medical tourism initiatives. The regional distribution also highlights disparities in specialty hospital availability, with some areas experiencing oversaturation while others face shortages, creating opportunities for market expansion and the development of new specialty facilities in underserved regions.

Regional Analysis of the North America Specialty Hospitals Market - Detailed regional market performance

The North America Specialty Hospitals Market exhibits distinct regional characteristics that influence market performance and development patterns across different geographic areas. The United States represents the largest regional market, characterized by high healthcare expenditure, advanced medical infrastructure, and a competitive specialty hospital landscape. Within the U.S., regional variations are significant, with the Northeast region showing strong concentration of academic medical centers and research-focused specialty hospitals, while the Southeast demonstrates rapid growth in rehabilitation and long-term care specialty facilities. The Midwest region features a mix of large healthcare systems and independent specialty hospitals, with particular strength in orthopedic and cardiovascular specialty centers. The Western region, particularly California and the Pacific Northwest, leads in technological innovation adoption and alternative medicine integration within specialty hospital settings. Canada's regional market is shaped by its universal healthcare system, with Ontario and Quebec hosting the majority of specialty hospitals, while Western provinces show growing demand for specialized services. Mexico's regional market is developing rapidly, with urban centers in central and northern regions leading specialty hospital expansion, driven by both domestic demand and medical tourism. Regional performance differences are influenced by factors such as population demographics, insurance coverage patterns, regulatory environments, and economic conditions, creating a diverse market landscape across North America.

Leading Company Profiles in the North America Specialty Hospitals Market - Industry players and strategies

The North America Specialty Hospitals Market features several prominent companies that have established themselves as leaders through strategic positioning, specialized expertise, and comprehensive service offerings. Advanced Specialty Hospitals has built a strong reputation for providing high-quality specialized care across multiple medical disciplines, focusing on patient-centered approaches and technological innovation. Brigham and Women's Hospital, affiliated with Harvard Medical School, represents the academic medical center model, combining cutting-edge research with specialized clinical care in areas such as oncology, cardiology, and neurology. Cleveland Clinic has established itself as a global leader in cardiac care while expanding into other specialty areas, leveraging its integrated healthcare system approach and international reputation for excellence. Community Health Systems Inc. operates a large network of specialty hospitals across multiple states, focusing on accessibility and comprehensive care delivery in both urban and rural markets. Encompass Health Corporation specializes in post-acute care and rehabilitation services, representing the growing importance of long-term care and recovery services in the specialty hospital market. HCA Healthcare, one of the largest healthcare providers in the United States, operates numerous specialty hospitals and continuously expands its service offerings through strategic acquisitions and organic growth. These leading companies employ various strategies including technological innovation, strategic partnerships, geographic expansion, and specialization in high-demand medical fields to maintain their competitive positions and drive market growth.

Porter's Five Forces Analysis of the North America Specialty Hospitals Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics shaping the North America Specialty Hospitals Market. The threat of new entrants remains moderate due to high barriers to entry, including substantial capital requirements, complex regulatory compliance, need for specialized medical expertise, and established brand loyalty among patients toward existing providers. However, opportunities exist for new entrants who can offer innovative care models or serve underserved markets. The bargaining power of buyers (patients and insurance companies) is increasing as patients become more informed healthcare consumers and insurance companies negotiate reimbursement rates, putting pressure on specialty hospitals to demonstrate value and cost-effectiveness. The bargaining power of suppliers, including medical equipment manufacturers and pharmaceutical companies, varies by specialty but generally remains moderate, as hospitals can often source from multiple suppliers and some have developed in-house capabilities. The threat of substitute services is growing with the expansion of outpatient surgery centers, telemedicine options, and alternative care delivery models that may compete with traditional specialty hospital services. Competitive rivalry within the market is intense, characterized by price competition, service differentiation, technological innovation races, and geographic market share battles among large healthcare systems, specialized independent hospitals, and new market entrants. Overall, the five forces analysis indicates a market where established players maintain strong positions but face increasing pressure from various competitive forces requiring continuous adaptation and innovation.

SWOT Analysis of the North America Specialty Hospitals Market - Strengths, weaknesses, opportunities, threats

A comprehensive SWOT analysis of the North America Specialty Hospitals Market reveals key internal and external factors influencing market dynamics. Strengths of the market include advanced medical technology adoption, highly skilled specialized medical professionals, strong research and development capabilities, and established healthcare infrastructure that supports high-quality specialized care delivery. The market benefits from growing patient demand for specialized services, favorable reimbursement environments in many areas, and the ability to provide focused expertise that often results in better clinical outcomes than general hospitals. Weaknesses include high operational costs, workforce shortages in specialized medical fields, vulnerability to regulatory changes, and the challenge of maintaining technological currency in rapidly evolving medical fields. The market also faces limitations in geographic accessibility, with specialty hospitals often concentrated in urban areas, leaving rural populations underserved. Opportunities abound in the form of telehealth expansion, personalized medicine advancements, aging population demographics driving demand for specialized care, and potential for market expansion into underserved regions. The integration of artificial intelligence and data analytics presents opportunities for improved diagnostic accuracy and operational efficiency. Threats to the market include increasing competition from alternative care delivery models, potential healthcare policy changes affecting reimbursement, economic downturns impacting healthcare spending, and the ongoing challenge of cybersecurity risks as hospitals become more digitally connected. Additionally, the market faces threats from potential public health crises and the need for continuous adaptation to changing patient expectations and care delivery preferences.

North America Specialty Hospitals Market Value Chain Analysis - Industry structure and value flow

The North America Specialty Hospitals Market value chain encompasses a complex network of activities and stakeholders that contribute to the delivery of specialized healthcare services. The value chain begins with primary healthcare providers and patient referrals, where general practitioners and primary care physicians identify patients requiring specialized treatment and initiate the referral process to specialty hospitals. This upstream activity is crucial as it determines patient flow and specialty hospital utilization rates. The core value chain activities within specialty hospitals include patient assessment and diagnosis, treatment planning, specialized medical procedures, and post-treatment care management. These activities are supported by essential support functions such as medical research and development, staff training and education, quality assurance programs, and patient experience management. The technology and equipment segment represents a critical value chain component, encompassing medical devices, diagnostic equipment, treatment technologies, and information systems that enable specialized care delivery. Supply chain management for medical supplies, pharmaceuticals, and specialized equipment forms another vital link, ensuring hospitals have the necessary resources for patient care. The downstream value chain includes patient recovery and rehabilitation services, follow-up care coordination, and outcomes monitoring. Additionally, the value chain extends to include insurance and reimbursement processes, medical education and training institutions that supply specialized healthcare professionals, and regulatory bodies that ensure quality and safety standards. This comprehensive value chain structure highlights the interconnected nature of specialty hospital operations and the multiple stakeholders involved in delivering specialized healthcare services.

Key Investment Insights in the North America Specialty Hospitals Market - Strategic investment recommendations

The North America Specialty Hospitals Market presents compelling investment opportunities characterized by strong growth fundamentals and evolving healthcare delivery models. Strategic investment insights indicate that the rehabilitation and long-term care specialty segment represents particularly attractive opportunities, driven by aging population demographics and increasing demand for post-acute care services. Investments in oncology specialty hospitals are also promising, given rising cancer prevalence and the continuous advancement of cancer treatment technologies. The market shows strong potential for investments in outpatient specialty services, which offer higher operational efficiency and meet growing patient preferences for convenient, cost-effective care options. Technology-focused investments represent another key opportunity, particularly in areas such as telemedicine platforms, artificial intelligence for diagnostic support, robotic surgery systems, and data analytics for personalized treatment planning. Geographic expansion investments targeting underserved markets or regions with growing populations present opportunities for first-mover advantages and market share capture. Strategic partnerships and joint ventures between specialty hospitals and technology companies, research institutions, or insurance providers offer investment pathways that combine clinical expertise with innovative care delivery models. Additionally, investments in workforce development and training programs are critical to address the ongoing shortage of specialized healthcare professionals. The market also presents opportunities for investments in sustainable healthcare practices and energy-efficient hospital designs, aligning with growing environmental concerns and potential cost savings. Overall, successful investment strategies in this market require a balanced approach that considers demographic trends, technological innovation, regulatory environments, and evolving patient care preferences.

North America Specialty Hospitals Market Conclusion - Summary and key takeaways

The North America Specialty Hospitals Market represents a dynamic and rapidly evolving segment of the healthcare industry, characterized by strong growth projections, technological innovation, and changing patient care paradigms. The market's trajectory from $186.89 billion in 2026 to $478.88 billion by 2033 at a 14.39% CAGR underscores the increasing importance of specialized healthcare services in meeting complex medical needs. Key takeaways from the market analysis include the growing dominance of outpatient services, the critical role of technological advancement in care delivery, and the importance of specialized expertise in achieving superior patient outcomes. The market demonstrates resilience and adaptability, as evidenced by its response to COVID-19 challenges and the accelerated adoption of digital health solutions. Competitive dynamics are shaped by large healthcare systems, specialized institutions, and emerging players, creating a diverse market landscape with opportunities for both established and new entrants. Regional variations highlight the importance of understanding local market conditions and demographic trends when developing market strategies. The value chain analysis reveals the complexity of specialty hospital operations and the multiple stakeholders involved in delivering high-quality specialized care. Investment insights point to promising opportunities in rehabilitation services, oncology, outpatient care, and technology integration. Overall, the North America Specialty Hospitals Market is positioned for continued growth and innovation, driven by demographic shifts, technological advancement, and the healthcare industry's ongoing focus on specialized, high-quality patient care.

Research Methodology - How this research was conducted

The research methodology employed for this North America Specialty Hospitals Market analysis combines comprehensive secondary research, selective primary research, and rigorous data validation processes to ensure accuracy and reliability. Secondary research formed the foundation of the analysis, drawing from a wide range of credible sources including industry reports, market databases, government publications, healthcare statistics, company annual reports, and academic journals. This extensive secondary research provided historical market data, industry trends, competitive landscape information, and regulatory framework insights. Primary research complemented secondary findings through interviews with industry experts, healthcare professionals, and market analysts to gain qualitative insights into market dynamics, emerging trends, and future growth prospects. The research methodology also incorporated data triangulation techniques, where information from multiple sources was cross-validated to ensure consistency and accuracy. Market size calculations and growth projections were developed using both top-down and bottom-up approaches, considering factors such as demographic trends, disease prevalence rates, healthcare expenditure patterns, and technological adoption rates. The forecast methodology accounted for various scenarios and sensitivity analyses to address potential market uncertainties. Segmentation analysis was conducted using detailed classification criteria across service types, hospital ownership structures, and medical specialties to provide comprehensive market insights. The research also included competitive analysis frameworks to evaluate market positioning and strategic developments of key players. Throughout the research process, data quality was maintained through systematic verification procedures and adherence to established market research standards.

Research Scope - Coverage and limitations

The research scope for this North America Specialty Hospitals Market analysis encompasses a comprehensive examination of the market across the United States, Canada, and Mexico, with a focus on current market conditions, growth projections, competitive landscape, and emerging trends. The analysis covers all major specialty hospital segments, including pediatric, oncology, rehabilitation, orthopedic, neurology, cardiology, and other specialized medical facilities, providing detailed insights into each segment's market dynamics and growth potential. The research scope includes both inpatient and outpatient specialty hospital services, examining how the shift toward ambulatory care models is impacting market development. Geographic coverage extends to major metropolitan areas and regions with significant specialty hospital concentrations, while also identifying opportunities in underserved markets. The analysis timeframe extends from historical data through current market conditions to future projections, with detailed forecasts covering the 2025-2032 period. Limitations of the research include the availability and reliability of public healthcare data, particularly in certain regions or for specific market segments where comprehensive statistics may be limited. The rapidly evolving nature of healthcare technology and regulatory environments also presents challenges in forecasting long-term market developments with complete certainty. Additionally, the research scope acknowledges that market dynamics can vary significantly based on local factors such as insurance coverage patterns, healthcare policies, and demographic characteristics, which may not be fully captured in broader regional analyses. Despite these limitations, the research provides a comprehensive and well-validated assessment of the North America Specialty Hospitals Market based on available data and established market research methodologies.

Key Companies and Recent Developments in the North America Specialty Hospitals Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The North America Specialty Hospitals Market features several key companies that have established themselves as industry leaders through strategic developments, innovative service offerings, and market expansion initiatives. Advanced Specialty Hospitals has focused on expanding its network of specialized facilities, with recent announcements highlighting investments in advanced diagnostic technologies and patient care improvement programs. Brigham and Women's Hospital, affiliated with Harvard Medical School, continues to strengthen its position through research partnerships and the development of specialized treatment protocols for complex medical conditions. Cleveland Clinic has announced expansion plans for its specialty hospital network, including new facilities focused on cardiovascular care and oncology services, while also investing in telemedicine capabilities to extend its reach. Community Health Systems Inc. has pursued a strategy of strategic acquisitions and facility upgrades, with recent developments including the integration of advanced surgical technologies across its specialty hospital portfolio. Encompass Health Corporation has expanded its rehabilitation specialty hospital offerings through both organic growth and acquisitions, with recent announcements focusing on enhanced post-acute care services and technology integration. HCA Healthcare has invested significantly in oncology specialty centers and announced partnerships with pharmaceutical companies for clinical trial programs. Other notable companies including Johns Hopkins Medicine, Memorial Sloan Kettering Cancer Center, and NYU Langone Hospitals have launched new specialized treatment programs, formed research collaborations, and expanded their geographic presence through strategic development initiatives. These companies continue to drive market innovation through technological adoption, service specialization, and strategic partnerships that enhance their competitive positions and market reach.