North America Warehouse Management System Market Overview - Definition, scope, and significance

A Warehouse Management System (WMS) is a software application designed to support and optimize warehouse functionality and distribution center management. These systems facilitate management of the entire inventory lifecycle from receiving to shipping, enabling real-time visibility into inventory levels, locations, and movements. The North American WMS market encompasses solutions deployed across the United States, Canada, and Mexico, serving diverse industries including manufacturing, automotive, food & beverage, healthcare, and retail & ecommerce. The significance of WMS solutions has grown substantially as businesses face increasing pressure to optimize supply chain operations, reduce costs, and meet rising customer expectations for rapid delivery and accurate order fulfillment. Modern WMS platforms integrate with other enterprise systems such as Enterprise Resource Planning (ERP), Transportation Management Systems (TMS), and Customer Relationship Management (CRM) to provide end-to-end visibility and control over warehouse operations.

North America Warehouse Management System Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The North American WMS market is driven by several key factors including the rapid growth of ecommerce, which has dramatically increased demand for efficient order fulfillment and last-mile delivery solutions. The need for real-time inventory visibility and improved warehouse productivity continues to push adoption of advanced WMS solutions. Additionally, the increasing complexity of global supply chains and the need for better demand forecasting and inventory optimization are driving market growth. However, the market faces restraints such as high implementation costs and the complexity of integrating WMS with existing legacy systems. Organizations often struggle with change management and training requirements when deploying new WMS solutions. Challenges include data security concerns, particularly with cloud-based deployments, and the need for continuous system updates to keep pace with evolving business requirements. Despite these obstacles, significant opportunities exist in emerging technologies such as artificial intelligence, machine learning, and Internet of Things (IoT) integration, which can enhance WMS capabilities and provide competitive advantages to early adopters.

North America Warehouse Management System Market Growth Trends - Current and emerging trends shaping the market

The North American WMS market is experiencing several transformative trends that are reshaping the industry landscape. Cloud-based WMS solutions are gaining significant traction as businesses seek more flexible, scalable, and cost-effective alternatives to traditional on-premises deployments. The integration of advanced analytics and business intelligence capabilities within WMS platforms is enabling data-driven decision-making and predictive analytics for warehouse operations. Mobile technologies are increasingly being incorporated into WMS solutions, allowing warehouse workers to access real-time information and perform tasks using smartphones and tablets. The adoption of automation technologies, including robotics and automated guided vehicles (AGVs), is accelerating, with WMS serving as the central nervous system coordinating these advanced systems. Industry-specific WMS solutions are emerging to address unique requirements in sectors such as food & beverage (with temperature monitoring and expiration date tracking) and healthcare (with regulatory compliance and lot tracking capabilities). Additionally, the trend toward omnichannel retailing is driving demand for WMS solutions that can seamlessly manage inventory across multiple sales channels and fulfillment options.

COVID-19 Impact on the North America Warehouse Management System Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has had a profound impact on the North American WMS market, initially causing disruptions in supply chains and warehouse operations. However, the crisis has also accelerated digital transformation initiatives as businesses recognized the need for greater resilience and agility in their supply chain operations. The pandemic-driven surge in ecommerce has significantly increased demand for WMS solutions that can handle higher order volumes and support contactless operations. Companies have prioritized investments in technologies that enable remote monitoring and management of warehouse operations, as well as solutions that enhance worker safety through automation and social distancing capabilities. The recovery trajectory shows a strong rebound as businesses focus on building more robust and adaptable supply chains. Organizations are increasingly viewing WMS as a critical component of their business continuity strategy, leading to increased investment in both cloud-based and on-premises solutions. The pandemic has also highlighted the importance of real-time visibility and analytics, driving demand for WMS platforms with advanced reporting and forecasting capabilities.

North America Warehouse Management System Market Competitive Landscape - Major competitors and market consolidation

The North American WMS market features a competitive landscape characterized by a mix of established enterprise software vendors, specialized WMS providers, and emerging technology companies. Major players such as Oracle Corporation, SAP SE, and IBM Corporation leverage their extensive enterprise software portfolios to offer comprehensive WMS solutions integrated with their broader ERP and supply chain management platforms. Specialized WMS providers like Manhattan Associates and JDA Software Group focus exclusively on warehouse and supply chain optimization solutions, often providing more tailored functionality for specific industries. The market is witnessing ongoing consolidation through mergers and acquisitions as larger companies seek to expand their capabilities and market presence. For instance, strategic acquisitions have enabled companies to enhance their cloud offerings, expand into new industry verticals, and incorporate advanced technologies such as artificial intelligence and machine learning. The competitive dynamics are also influenced by the entry of new players offering innovative, cloud-native WMS solutions that challenge traditional vendors with more agile and cost-effective alternatives. Companies are increasingly differentiating themselves through vertical-specific expertise, advanced analytics capabilities, and superior integration with emerging technologies.

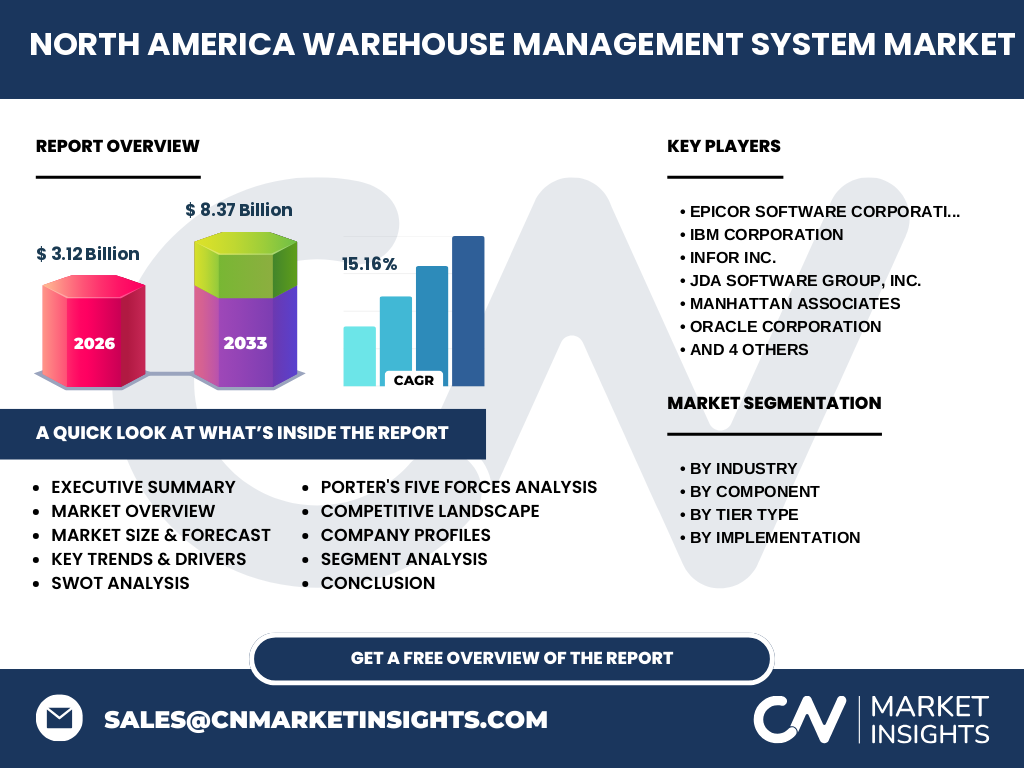

Executive Summary - High-level overview and key findings about North America Warehouse Management System Market

The North American WMS market is experiencing robust growth, driven by the increasing need for supply chain optimization and the rapid expansion of ecommerce. The market is projected to grow from $3.12 billion in 2026 to $8.37 billion by 2033, representing a compound annual growth rate of 15.16%. This growth is fueled by the adoption of cloud-based solutions, the integration of advanced technologies, and the increasing complexity of warehouse operations. The market is segmented by industry, component, tier type, and implementation model, with each segment exhibiting distinct growth patterns and adoption trends. Manufacturing, automotive, food & beverage, healthcare, and retail & ecommerce industries are the primary adopters of WMS solutions, each with unique requirements and challenges. The component segment is dominated by software solutions, although services are also experiencing significant growth as organizations seek implementation support and ongoing optimization. Tier 1 solutions cater to large enterprises with complex operations, while Tier 2 and Tier 3 solutions address the needs of mid-market and small businesses respectively. The implementation model is shifting toward cloud-based solutions, although on-premises deployments remain relevant for organizations with specific security or customization requirements.

North America Warehouse Management System Market Forecast - Projections for 2025-2032 period

The North American WMS market is poised for substantial growth over the forecast period of 2025-2032, with projections indicating a market size of $8.37 billion by 2033, up from $3.12 billion in 2026. This represents a compound annual growth rate of 15.16%, reflecting the increasing adoption of WMS solutions across various industries and the continuous evolution of warehouse management technologies. The forecast period is expected to witness significant shifts in market dynamics, with cloud-based solutions gaining market share at the expense of traditional on-premises deployments. The integration of advanced technologies such as artificial intelligence, machine learning, and Internet of Things (IoT) is expected to drive innovation and create new opportunities for market growth. Industry-specific WMS solutions are likely to see increased adoption as businesses seek tailored functionality to address unique operational challenges. The manufacturing and retail & ecommerce segments are projected to be the fastest-growing end-user categories, driven by the need for greater supply chain visibility and the continued expansion of online retail. The competitive landscape is expected to evolve through strategic partnerships, acquisitions, and the entry of new players offering innovative solutions.

North America Warehouse Management System Market Size and Share by Segmentation - Breakdown by {segmentData}

The North American WMS market is segmented by industry, component, tier type, and implementation model, each contributing differently to the overall market size and growth. By industry, the retail & ecommerce segment is expected to hold the largest market share due to the explosive growth of online shopping and the need for efficient order fulfillment. The manufacturing segment follows closely, driven by the need for lean inventory management and just-in-time production capabilities. By component, software solutions dominate the market, accounting for the majority of revenue, while services including implementation, training, and support represent a significant but smaller portion of the market. The tier type segmentation reveals that Tier 1 solutions, designed for large enterprises with complex warehouse operations, command the highest market share in terms of revenue, although Tier 2 and Tier 3 solutions are experiencing faster growth rates as mid-market and small businesses increasingly adopt WMS technologies. Regarding implementation models, cloud-based solutions are rapidly gaining market share, driven by their lower upfront costs, scalability, and ease of deployment, while on-premises solutions continue to serve organizations with specific security, customization, or integration requirements.

Global North America Warehouse Management System Market Size and Share by Region - Geographic distribution

The North American WMS market encompasses the United States, Canada, and Mexico, with the United States representing the largest market share due to its advanced logistics infrastructure, high ecommerce penetration, and concentration of large enterprises. The U.S. market benefits from early technology adoption, significant investments in supply chain innovation, and the presence of major WMS vendors and technology companies. Canada, while smaller in absolute market size, demonstrates strong growth potential driven by increasing ecommerce adoption and investments in warehouse automation. The Canadian market is characterized by a focus on cold chain logistics and cross-border trade with the United States, creating unique requirements for WMS solutions. Mexico's WMS market is growing rapidly, fueled by the country's role as a manufacturing hub and the increasing adoption of modern warehouse management practices by both domestic and international companies. Regional differences in market maturity, regulatory environments, and industry concentrations create distinct opportunities and challenges for WMS providers operating across North America. The market is also influenced by cross-border trade agreements and the integration of supply chains across the three countries.

Regional Analysis of the North America Warehouse Management System Market - Detailed regional market performance

The United States dominates the North American WMS market, accounting for the largest share of revenue and installations. The U.S. market is characterized by high technology adoption rates, significant investments in supply chain innovation, and the presence of major ecommerce players and logistics companies. Key growth drivers in the U.S. include the rapid expansion of ecommerce, the need for omnichannel fulfillment capabilities, and the increasing adoption of automation technologies in warehouses. Canada's WMS market, while smaller than the U.S., is experiencing steady growth driven by increasing ecommerce penetration, investments in cold chain logistics, and the need for cross-border supply chain optimization with the United States. The Canadian market is particularly strong in industries such as food & beverage and pharmaceuticals, where temperature-controlled warehousing and regulatory compliance are critical. Mexico's WMS market is emerging as a significant growth opportunity, driven by the country's manufacturing sector, particularly in automotive and electronics, and the increasing adoption of modern warehouse management practices by both domestic and international companies. The Mexican market is also benefiting from nearshoring trends, as companies seek to relocate supply chain operations closer to the United States.

Leading Company Profiles in the North America Warehouse Management System Market - Industry players and strategies

The North American WMS market features several leading companies with distinct strategies and competitive advantages. Oracle Corporation leverages its extensive enterprise software portfolio to offer integrated WMS solutions that seamlessly connect with its ERP and supply chain management platforms. The company's strategy focuses on providing comprehensive, enterprise-grade solutions with strong analytics capabilities and industry-specific functionality. SAP SE similarly offers WMS solutions integrated with its broader enterprise software suite, emphasizing end-to-end supply chain visibility and advanced planning capabilities. Manhattan Associates has established itself as a leader in supply chain and warehouse management solutions, with a strategy focused on innovation in areas such as omnichannel fulfillment and labor management. The company's strong presence in retail and ecommerce has been a key differentiator. JDA Software Group (now part of Blue Yonder) specializes in supply chain and retail planning solutions, with a strategy centered on AI-driven optimization and advanced analytics. Other notable players such as Epicor Software Corporation, Infor Inc., and TECSYS focus on providing industry-specific WMS solutions with strong vertical expertise, particularly in manufacturing, distribution, and healthcare. These companies differentiate themselves through deep domain knowledge and tailored functionality for specific industry requirements.

Porter's Five Forces Analysis of the North America Warehouse Management System Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the North American WMS market. The threat of new entrants is moderate, as the market requires significant technological expertise, substantial R&D investments, and established relationships with large enterprises. However, the emergence of cloud-native WMS solutions has lowered barriers to entry somewhat, allowing innovative startups to challenge established players. The bargaining power of buyers is high, as large enterprises have multiple options when selecting WMS providers and can demand customized solutions, competitive pricing, and integration capabilities. The bargaining power of suppliers is relatively low, as WMS providers have access to a wide range of technology components and development resources. The threat of substitute products or services is moderate, with alternative approaches to warehouse management such as manual processes or basic inventory management systems still present in some organizations, though these are increasingly inadequate for complex operations. Competitive rivalry among existing WMS providers is intense, characterized by continuous innovation, aggressive pricing strategies, and efforts to expand into new industry verticals or geographic regions. Companies compete on factors such as functionality, scalability, ease of integration, and total cost of ownership.

SWOT Analysis of the North America Warehouse Management System Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the North American WMS market reveals several key factors influencing its development. Strengths of the market include the advanced technological infrastructure in North America, high ecommerce penetration driving demand for efficient fulfillment solutions, and the presence of major WMS vendors with strong R&D capabilities. The region's sophisticated logistics networks and early adoption of automation technologies also represent significant strengths. Weaknesses include the high costs associated with WMS implementation and integration, particularly for small and medium-sized businesses, and the complexity of managing change within organizations when deploying new systems. Additionally, data security concerns and the need for continuous system updates can be challenging for some organizations. Opportunities abound in emerging technologies such as artificial intelligence, machine learning, and Internet of Things (IoT) integration, which can enhance WMS capabilities and provide competitive advantages. The growing trend of omnichannel retailing and the increasing complexity of global supply chains also present significant opportunities for WMS providers. Threats to the market include economic uncertainties that could impact IT spending, the potential for cybersecurity breaches, and the rapid pace of technological change that could render existing solutions obsolete if companies fail to innovate continuously.

North America Warehouse Management System Market Value Chain Analysis - Industry structure and value flow

The North American WMS market value chain encompasses several key stages, each contributing to the delivery of comprehensive warehouse management solutions. At the foundation are technology providers and component suppliers who deliver the hardware, software frameworks, and development tools that enable WMS functionality. These include providers of cloud infrastructure, database management systems, and development platforms. The next stage involves WMS software developers and vendors who create the core applications, incorporating features such as inventory tracking, order management, and labor optimization. These companies invest heavily in R&D to enhance their solutions with advanced analytics, AI capabilities, and industry-specific functionality. System integrators and implementation partners play a crucial role in customizing WMS solutions for specific client needs, managing the integration with existing enterprise systems, and ensuring smooth deployment. Value-added resellers (VARs) and managed service providers extend the reach of WMS solutions, particularly to mid-market and small businesses that may require additional support. Consulting firms provide strategic guidance on WMS selection and implementation, helping organizations align their warehouse management strategies with broader supply chain objectives. Finally, end-user industries including manufacturing, retail, healthcare, and logistics benefit from the value created by WMS solutions through improved operational efficiency, reduced costs, and enhanced customer satisfaction.

Key Investment Insights in the North America Warehouse Management System Market - Strategic investment recommendations

Strategic investment in the North American WMS market should focus on several key areas to capitalize on growth opportunities and address emerging challenges. Cloud-based WMS solutions represent a significant investment opportunity, as businesses increasingly seek flexible, scalable, and cost-effective alternatives to traditional on-premises deployments. Investors should look for companies offering robust cloud platforms with strong security features, seamless integration capabilities, and pay-as-you-go pricing models. Another promising investment area is the integration of advanced technologies such as artificial intelligence and machine learning into WMS solutions, which can provide predictive analytics, optimize warehouse operations, and enable autonomous decision-making. Companies developing industry-specific WMS solutions for high-growth sectors such as ecommerce, healthcare, and cold chain logistics offer attractive investment prospects due to their tailored functionality and specialized expertise. Additionally, investments in companies offering comprehensive implementation services, training, and ongoing support can be valuable, as these services are critical for successful WMS adoption and optimization. The growing trend of warehouse automation presents opportunities to invest in WMS providers that offer strong integration with robotics, automated guided vehicles, and other advanced material handling systems. Finally, companies focusing on mobile and IoT-enabled WMS solutions are well-positioned to benefit from the increasing need for real-time visibility and workforce mobility in warehouse operations.

North America Warehouse Management System Market Conclusion - Summary and key takeaways

The North American WMS market is experiencing robust growth, driven by the increasing complexity of supply chain operations, the explosive expansion of ecommerce, and the continuous evolution of warehouse management technologies. With a projected market size of $8.37 billion by 2033 and a compound annual growth rate of 15.16%, the market presents significant opportunities for both established players and innovative new entrants. The shift toward cloud-based solutions, the integration of advanced technologies such as AI and IoT, and the growing demand for industry-specific functionality are reshaping the competitive landscape. While challenges such as high implementation costs and integration complexities remain, the market's strengths—including advanced technological infrastructure and high ecommerce penetration—provide a solid foundation for continued growth. Key investment opportunities exist in cloud-based solutions, advanced technology integration, and industry-specific offerings. As businesses increasingly recognize the strategic importance of efficient warehouse management in maintaining competitive advantage, the demand for sophisticated WMS solutions is expected to remain strong, driving innovation and market expansion across the United States, Canada, and Mexico.

Research Methodology - How this research was conducted

This research on the North American WMS market was conducted using a comprehensive methodology combining primary and secondary research approaches. Primary research involved interviews with industry experts, WMS vendors, system integrators, and end-users across various sectors to gather insights on market trends, challenges, and growth opportunities. These interviews provided valuable qualitative data on market dynamics, competitive strategies, and emerging technologies. Secondary research encompassed a thorough review of company annual reports, financial statements, press releases, and product documentation from leading WMS providers. Industry publications, market research reports, and trade journals were analyzed to understand broader market trends and competitive developments. Government statistics and economic data were examined to assess the impact of macroeconomic factors on market growth. The research also included a detailed analysis of patent filings and academic publications to identify technological innovations and emerging trends in warehouse management. Data triangulation techniques were employed to validate findings and ensure accuracy, with particular attention paid to market sizing and forecasting methodologies. The research team also conducted an extensive review of recent mergers, acquisitions, and strategic partnerships to understand the evolving competitive landscape.

Research Scope - Coverage and limitations

This research report covers the North American WMS market across the United States, Canada, and Mexico, providing a comprehensive analysis of market size, growth trends, competitive landscape, and key industry segments. The scope includes an examination of WMS solutions by industry vertical (manufacturing, automotive, food & beverage, healthcare, and retail & ecommerce), component (software and services), tier type (Tier 1, Tier 2, and Tier 3), and implementation model (on-premises and cloud-based). The research timeframe extends from historical data through 2026 to a forecast period extending to 2033, allowing for both retrospective analysis and future projections. The report provides detailed company profiles of major WMS providers, including Epicor Software Corporation, IBM Corporation, Infor Inc., JDA Software Group, Manhattan Associates, Oracle Corporation, PSI Software AG, PTC Inc., SAP SE, and TECSYS. However, the research has certain limitations, including the exclusion of smaller regional players and niche solution providers that may have limited market presence. Additionally, while the report provides a comprehensive overview of market trends and dynamics, it does not include detailed financial data for private companies or granular regional breakdowns within each country. The research also focuses primarily on commercial WMS solutions, with limited coverage of open-source or custom-developed systems used by some large enterprises.

Key Companies and Recent Developments in the North America Warehouse Management System Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The North American WMS market features several key companies that have recently announced significant developments, product launches, and strategic initiatives. Oracle Corporation has continued to enhance its WMS offerings with the introduction of advanced analytics and machine learning capabilities, focusing on providing real-time visibility and predictive insights for warehouse operations. The company has also announced several strategic partnerships with logistics providers to expand its market reach and integration capabilities. SAP SE has launched new cloud-native WMS solutions designed to provide greater flexibility and scalability for businesses of all sizes, with particular emphasis on supporting omnichannel fulfillment strategies. Manhattan Associates has introduced innovative labor management features within its WMS platform, leveraging AI to optimize workforce planning and productivity in response to the growing challenges of labor shortages in the logistics industry. JDA Software Group (now part of Blue Yonder) has announced the integration of its WMS with advanced robotics and automation systems, enabling more sophisticated warehouse orchestration and material handling capabilities. Epicor Software Corporation has expanded its industry-specific WMS solutions for manufacturing and distribution, with new features supporting lot tracking, quality control, and regulatory compliance. Infor Inc. has launched a new version of its WMS with enhanced mobile capabilities and improved user interfaces, aimed at increasing adoption among warehouse workers and reducing training requirements. These developments reflect the industry's focus on innovation, cloud adoption, and the integration of advanced technologies to address evolving market needs.