Overhead Console Market Overview - Definition, scope, and significance

The overhead console market encompasses automotive components installed in vehicle headliners that provide storage, lighting, and integrated technology features. These systems have evolved from simple storage compartments to sophisticated control centers incorporating telematics, infotainment displays, and driver assistance features. The market serves both passenger cars and commercial vehicles, with applications spanning vehicle telematics and infotainment systems with human-machine interfaces (HMI). As vehicles become increasingly connected and autonomous, overhead consoles are transforming into critical interfaces between drivers, passengers, and vehicle systems.

Overhead Console Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

Market growth is primarily driven by increasing vehicle production, rising consumer demand for connected vehicle features, and the automotive industry's shift toward autonomous driving technologies. The integration of advanced telematics and infotainment systems creates significant opportunities for manufacturers to develop innovative console designs. However, challenges include the high cost of advanced overhead console systems, complexity in integration with existing vehicle architectures, and supply chain disruptions. Opportunities exist in developing lightweight materials, energy-efficient designs, and customizable console solutions for different vehicle segments and regional preferences.

Overhead Console Market Growth Trends - Current and emerging trends shaping the market

Key trends include the miniaturization of electronic components, enabling more compact and feature-rich overhead consoles. There is growing adoption of touch-sensitive controls, gesture recognition, and voice-activated interfaces integrated into console designs. The market is witnessing increased demand for modular console architectures that allow for easier upgrades and customization. Sustainability trends are driving the use of recycled and bio-based materials in console manufacturing. Additionally, the rise of electric vehicles is creating new design opportunities for overhead consoles, including integration with battery management systems and range monitoring displays.

COVID-19 Impact on the Overhead Console Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the overhead console market through manufacturing shutdowns, supply chain interruptions, and reduced vehicle production. Automotive industry slowdowns led to decreased demand for overhead console components during 2020-2021. However, the market has shown resilience with recovery driven by pent-up demand, government stimulus programs supporting automotive manufacturing, and accelerated adoption of digital vehicle features. The pandemic also highlighted the importance of touchless interfaces and antimicrobial materials in vehicle interiors, influencing future console design requirements.

Overhead Console Market Competitive Landscape - Major competitors and market consolidation

The competitive landscape features established automotive component suppliers competing on technological innovation, manufacturing capabilities, and global reach. Key players include Magna International, Gentex Corporation, and Grupo Antolin, which leverage their extensive automotive supply chain relationships. Competition centers on developing advanced features such as integrated cameras, advanced lighting systems, and seamless connectivity solutions. Market consolidation may occur through strategic acquisitions as companies seek to expand their technology portfolios and geographic presence in emerging automotive markets.

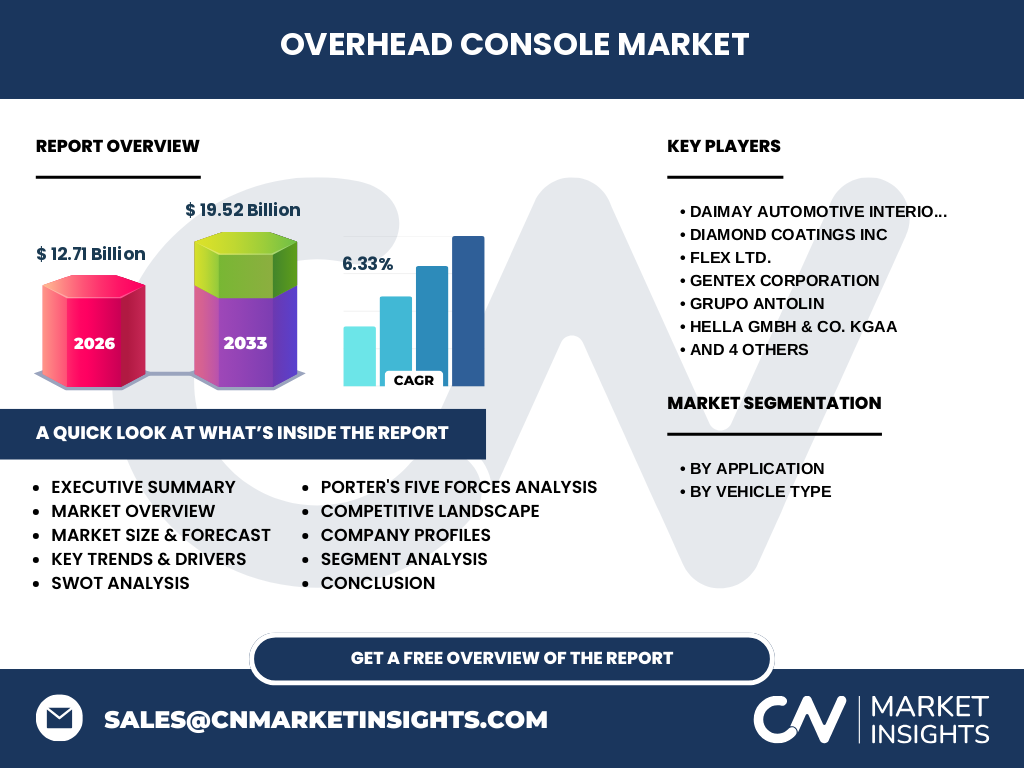

Executive Summary - High-level overview and key findings about Overhead Console Market

The overhead console market is experiencing steady growth driven by technological advancements and increasing vehicle electrification. With a projected market size of $12.71 billion in 2026 and a compound annual growth rate of 6.33%, the industry is positioned for expansion through 2033. Key applications in vehicle telematics and infotainment systems are creating new revenue streams for manufacturers. The market serves both passenger cars and commercial vehicles, with regional variations in adoption rates and feature preferences. Success factors include innovation in user interfaces, integration capabilities, and cost-effective manufacturing processes.

Overhead Console Market Forecast - Projections for 2025-2032 period

Based on available data, the overhead console market is projected to grow from $12.71 billion in 2026 to $19.52 billion by 2033, representing a compound annual growth rate of 6.33%. This growth trajectory suggests steady market expansion driven by increasing vehicle production, technological advancements, and rising consumer expectations for in-vehicle features. The forecast period indicates sustained demand across both passenger car and commercial vehicle segments, with particular growth in applications involving advanced telematics and infotainment systems integration.

Overhead Console Market Size and Share by Segmentation - Breakdown by {segmentData}

The overhead console market is segmented by application and vehicle type. By application, the market is divided into vehicle telematics and infotainment systems with HMI, with telematics applications showing strong growth potential due to increasing demand for connected vehicle features. By vehicle type, the market serves passenger cars and commercial vehicles, with passenger cars representing the larger segment due to higher production volumes. The segmentation reflects diverse customer needs, with commercial vehicles requiring more robust and specialized console solutions for fleet management and driver monitoring applications.

Global Overhead Console Market Size and Share by Region - Geographic distribution

While specific regional market share data is not provided, the global overhead console market shows varying adoption rates across different geographic regions. Developed automotive markets in North America, Europe, and Japan represent mature segments with high feature integration. Emerging markets in Asia-Pacific, particularly China and India, show strong growth potential driven by increasing vehicle production and rising consumer disposable income. Regional variations in vehicle preferences, regulatory requirements, and technological adoption rates influence market dynamics and product development strategies.

Regional Analysis of the Overhead Console Market - Detailed regional market performance

Regional market performance varies significantly based on local automotive manufacturing capabilities, consumer preferences, and economic conditions. North America and Europe lead in advanced feature adoption, with high integration of telematics and infotainment systems. Asia-Pacific represents the fastest-growing region, driven by China's expanding automotive industry and India's emerging market potential. Latin American and Middle Eastern markets show moderate growth, influenced by economic conditions and vehicle import policies. Regional analysis indicates opportunities for localized product development and strategic partnerships with regional automotive manufacturers.

Leading Company Profiles in the Overhead Console Market - Industry players and strategies

Leading companies in the overhead console market include Magna International, Gentex Corporation, and Grupo Antolin, each bringing distinct competitive advantages. Magna leverages its global manufacturing network and extensive automotive relationships. Gentex specializes in electronic mirror and display technologies, providing integrated solutions. Grupo Antolin focuses on innovative interior systems and sustainable materials. Other notable players include Daimay Automotive, Diamond Coatings, Flex Ltd., Hella GmbH, JPC Automotive, KOJIMA INDUSTRIES, and Yanfeng Automotive Interiors, each contributing specialized capabilities in materials, electronics, or manufacturing processes.

Porter's Five Forces Analysis of the Overhead Console Market - Competitive forces assessment

The overhead console market exhibits moderate competitive intensity with several key forces at play. Supplier power is moderate, with established relationships between console manufacturers and automotive OEMs. Buyer power is significant, as automotive manufacturers demand high quality, reliability, and cost-effectiveness. New entrants face high barriers due to capital requirements and established relationships. Substitute threats are low, as overhead consoles serve specific functional requirements. Competitive rivalry is intense, with companies competing on technology, price, and integration capabilities. The market shows characteristics of an oligopoly with a few dominant players controlling significant market share.

SWOT Analysis of the Overhead Console Market - Strengths, weaknesses, opportunities, threats

Strengths in the overhead console market include established supplier relationships with major automotive manufacturers, technological expertise in electronics integration, and global manufacturing capabilities. Weaknesses involve dependency on automotive industry cycles, high development costs, and complex integration requirements. Opportunities exist in emerging electric vehicle markets, autonomous driving applications, and advanced connectivity features. Threats include intense price competition, potential supply chain disruptions, and rapid technological changes that could render existing designs obsolete. The market's ability to adapt to changing automotive trends will determine long-term success.

Overhead Console Market Value Chain Analysis - Industry structure and value flow

The overhead console value chain begins with raw material suppliers providing plastics, metals, and electronic components. These materials flow to component manufacturers who produce individual console parts and electronic systems. Assembly plants integrate these components into complete overhead console units, which are then distributed to automotive OEMs. Value is added at each stage through design innovation, quality improvements, and cost optimization. The chain includes aftermarket services and potential upgrades, creating additional value streams. Effective coordination across the value chain is essential for meeting automotive industry quality standards and delivery requirements.

Key Investment Insights in the Overhead Console Market - Strategic investment recommendations

Investment opportunities in the overhead console market focus on technological innovation, particularly in areas such as advanced displays, touchless interfaces, and integrated connectivity solutions. Companies should consider investments in sustainable materials and manufacturing processes to meet evolving environmental regulations. Geographic expansion into emerging automotive markets offers growth potential, while strategic partnerships with technology companies can accelerate innovation. Investment in automation and digitalization of manufacturing processes can improve cost competitiveness. The market also presents opportunities for vertical integration to control quality and reduce supply chain risks.

Overhead Console Market Conclusion - Summary and key takeaways

The overhead console market represents a dynamic segment of the automotive industry with strong growth potential through 2033. Driven by technological advancements and increasing vehicle electrification, the market is evolving from simple storage compartments to sophisticated control centers. Key success factors include innovation in user interfaces, integration capabilities, and cost-effective manufacturing. The market serves diverse applications across passenger cars and commercial vehicles, with regional variations in adoption rates and feature preferences. Companies that can navigate technological changes, supply chain challenges, and evolving customer requirements will be best positioned for success.

Research Methodology - How this research was conducted

This market research report was compiled using a comprehensive methodology combining primary and secondary research sources. Primary research included interviews with industry experts, suppliers, and automotive manufacturers to gather insights on market trends and competitive dynamics. Secondary research involved analysis of company financial reports, industry publications, and market databases. The research methodology incorporated both bottom-up and top-down approaches to validate market size estimates and growth projections. Data triangulation techniques were used to ensure accuracy and reliability of the findings presented in this report.

Research Scope - Coverage and limitations

This research report covers the global overhead console market with focus on key applications, vehicle types, and major geographic regions. The scope includes analysis of market drivers, restraints, competitive landscape, and future growth opportunities through 2033. Limitations include the availability of detailed regional market share data and specific company-level financial information for all market participants. The report focuses on commercially available overhead console systems and does not include custom or experimental applications. Coverage is primarily based on publicly available information and industry expert insights.

Key Companies and Recent Developments in the Overhead Console Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Key companies in the overhead console market have been actively pursuing technological advancements and strategic partnerships. Magna International has expanded its electronics integration capabilities for connected vehicle applications. Gentex Corporation has introduced advanced camera systems integrated into overhead consoles for driver monitoring. Grupo Antolin has launched sustainable material solutions for console manufacturing. Other companies including Daimay Automotive, Diamond Coatings, Flex Ltd., Hella GmbH, JPC Automotive, KOJIMA INDUSTRIES, and Yanfeng Automotive Interiors have announced new product developments focusing on lightweight materials, advanced lighting systems, and improved user interfaces. These developments reflect the industry's focus on innovation and meeting evolving automotive requirements.