Plasma Fractionation Market Overview - Definition, scope, and significance

Plasma fractionation is the process of separating whole blood plasma into its individual protein components through various physical and biochemical methods. This process involves collecting blood plasma from donors, followed by cold ethanol fractionation or other separation techniques to isolate specific proteins such as immunoglobulins, albumin, and coagulation factors. The plasma fractionation market encompasses the production, processing, and distribution of these therapeutic plasma proteins, which are essential for treating a wide range of medical conditions including immune disorders, bleeding disorders, and critical care situations. The significance of this market lies in its critical role in providing life-saving treatments for patients with rare diseases and chronic conditions, making it an indispensable part of the global healthcare system.

Plasma Fractionation Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The plasma fractionation market is primarily driven by the increasing prevalence of chronic diseases, growing demand for immunoglobulin therapies, and advancements in plasma collection and processing technologies. The rising awareness about rare diseases and improved healthcare infrastructure in developing regions also contribute to market growth. However, the market faces several restraints including the high cost of plasma-derived products, stringent regulatory requirements for plasma collection and processing, and the risk of transmitting infectious diseases through plasma products. Key challenges include maintaining a consistent supply of plasma through voluntary donations, ensuring product safety and efficacy, and managing the complex logistics of plasma collection and distribution. Despite these challenges, significant opportunities exist in expanding applications of plasma-derived products, developing novel fractionation technologies, and entering emerging markets with growing healthcare needs.

Plasma Fractionation Market Growth Trends - Current and emerging trends shaping the market

The plasma fractionation market is experiencing several notable growth trends, including the increasing adoption of recombinant technologies alongside traditional plasma-derived products. There is a growing emphasis on developing more efficient fractionation processes and improving the yield of therapeutic proteins from plasma donations. The market is also witnessing a trend towards the development of higher purity and more concentrated plasma products, which can reduce administration time and improve patient compliance. Another emerging trend is the increasing use of plasma products in emerging therapeutic areas such as neurology and pulmonology, expanding beyond traditional applications in hematology and immunology. Additionally, there is a growing focus on sustainability in plasma collection and processing, with companies investing in more environmentally friendly practices and reducing waste in the fractionation process.

COVID-19 Impact on the Plasma Fractionation Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the plasma fractionation market, primarily through disruptions in plasma collection activities and supply chain operations. Many plasma collection centers were temporarily closed or operated at reduced capacity during the height of the pandemic, leading to concerns about potential shortages of plasma-derived products. However, the pandemic also highlighted the importance of plasma therapies, particularly in the development of convalescent plasma treatments for COVID-19 patients. As the market recovers from the pandemic, there is an increased focus on building more resilient supply chains and improving plasma collection infrastructure. The experience gained during the pandemic has also accelerated the adoption of digital technologies in plasma collection and processing, potentially leading to more efficient operations in the future.

Plasma Fractionation Market Competitive Landscape - Major competitors and market consolidation

The plasma fractionation market is characterized by a relatively consolidated competitive landscape, with a few major players dominating the global market. These companies have established extensive plasma collection networks and advanced processing facilities, allowing them to maintain significant market share. The competitive landscape is shaped by factors such as product portfolio breadth, geographic presence, and technological capabilities in plasma processing. Companies are increasingly focusing on strategic collaborations, mergers, and acquisitions to expand their market presence and enhance their product offerings. The market also sees competition from emerging players developing innovative fractionation technologies and alternative plasma collection methods. However, the high barriers to entry, including the need for substantial capital investment and strict regulatory compliance, continue to limit new entrants in the market.

Executive Summary - High-level overview and key findings about Plasma Fractionation Market

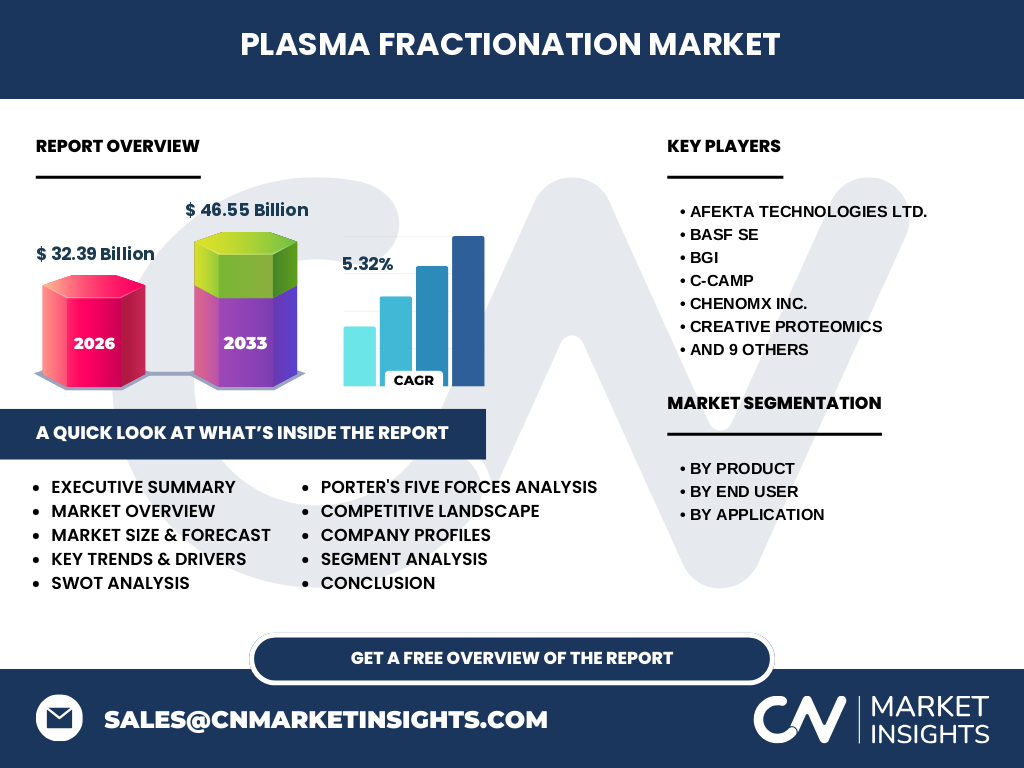

The plasma fractionation market represents a critical segment of the biopharmaceutical industry, with a current market size of $32.39 billion and a projected growth to $46.55 billion by 2033, representing a CAGR of 5.32%. The market is driven by the increasing prevalence of chronic diseases, growing demand for immunoglobulin therapies, and advancements in plasma collection and processing technologies. Key product segments include immunoglobulin, albumin, and coagulation factor concentrates, with applications spanning neurology, immunology, hematology, and critical care. The market faces challenges related to supply chain resilience, regulatory compliance, and the need for continuous innovation in fractionation technologies. Despite these challenges, the market presents significant opportunities for growth through expansion into emerging markets, development of novel therapeutic applications, and investment in more efficient processing technologies.

Plasma Fractionation Market Forecast - Projections for 2025-2032 period

The plasma fractionation market is projected to experience steady growth from 2025 to 2032, with the market size expected to increase from $32.39 billion to $46.55 billion by 2033. This growth is driven by several factors, including the increasing prevalence of chronic diseases, growing demand for plasma-derived therapies, and advancements in fractionation technologies. The immunoglobulin segment is expected to maintain its dominance due to the rising incidence of immune disorders and the expanding applications of immunoglobulin therapies. Hospitals and clinics are likely to remain the largest end-user segment, driven by the increasing use of plasma products in critical care and emergency medicine. The market is also expected to see growth in emerging regions, particularly in Asia-Pacific and Latin America, as healthcare infrastructure improves and awareness of plasma therapies increases.

Plasma Fractionation Market Size and Share by Segmentation - Breakdown by {segmentData}

The plasma fractionation market is segmented by product, end user, and application. By product, the immunoglobulin segment is expected to hold the largest market share, driven by the increasing prevalence of immune disorders and the expanding use of immunoglobulin therapies. The albumin segment is also significant, particularly in critical care and emergency medicine applications. By end user, hospitals and clinics are projected to be the largest segment, followed by clinical research laboratories and academic institutes. In terms of application, neurology and immunology are expected to be the leading segments, with growing use of plasma products in treating neurological disorders and immune-related conditions. The critical care segment is also anticipated to see substantial growth, driven by the increasing use of plasma products in intensive care units and emergency departments.

Global Plasma Fractionation Market Size and Share by Region - Geographic distribution

The global plasma fractionation market exhibits varying dynamics across different regions, with North America currently holding the largest market share due to its advanced healthcare infrastructure and high prevalence of chronic diseases. Europe is the second-largest market, driven by strong healthcare systems and increasing awareness of plasma therapies. The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, fueled by improving healthcare infrastructure, rising disposable incomes, and increasing prevalence of chronic diseases. Latin America and the Middle East & Africa regions are also showing promising growth, albeit from a smaller base, as healthcare systems in these regions continue to develop and awareness of plasma therapies increases. The regional distribution of the market is influenced by factors such as regulatory frameworks, healthcare spending, and the prevalence of diseases requiring plasma-derived therapies.

Regional Analysis of the Plasma Fractionation Market - Detailed regional market performance

Regional analysis of the plasma fractionation market reveals distinct patterns of growth and development across different geographic areas. In North America, the market is characterized by advanced plasma collection infrastructure, high healthcare spending, and a strong focus on research and development. Europe shows a similar trend, with additional emphasis on regulatory compliance and product safety. The Asia-Pacific region is experiencing rapid growth, driven by increasing healthcare investments, improving regulatory frameworks, and a large patient population. However, challenges such as varying levels of healthcare infrastructure and regulatory differences across countries in the region impact market dynamics. Latin America and the Middle East & Africa regions, while currently smaller markets, are showing potential for growth as healthcare systems develop and awareness of plasma therapies increases. These regions face unique challenges including limited plasma collection infrastructure and varying levels of regulatory oversight.

Leading Company Profiles in the Plasma Fractionation Market - Industry players and strategies

The plasma fractionation market is dominated by several key players, each with their own strategies for maintaining and expanding their market position. These companies typically have extensive plasma collection networks, advanced processing facilities, and diverse product portfolios. Their strategies often include investments in research and development to improve fractionation technologies, expansion into emerging markets, and strategic partnerships or acquisitions to enhance their capabilities. Many of these companies are also focusing on developing more efficient processing methods to increase yield and reduce costs, as well as expanding their product lines to include new therapeutic applications. The competitive strategies of these leading companies significantly influence market dynamics, driving innovation and shaping industry trends.

Porter's Five Forces Analysis of the Plasma Fractionation Market - Competitive forces assessment

Porter's Five Forces analysis of the plasma fractionation market reveals a complex competitive landscape. The threat of new entrants is relatively low due to high barriers to entry, including the need for substantial capital investment, strict regulatory requirements, and the necessity of establishing plasma collection networks. The bargaining power of suppliers, primarily plasma donors, is moderate, as the need for voluntary donations and the risk of shortages can impact supply. The bargaining power of buyers, such as hospitals and clinics, is also moderate, influenced by factors such as product differentiation and the critical nature of plasma-derived therapies. The threat of substitutes is low, given the unique properties of plasma-derived products and the limited alternatives for many applications. Competitive rivalry among existing players is high, driven by the market's consolidated nature and the constant need for innovation and efficiency improvements.

SWOT Analysis of the Plasma Fractionation Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the plasma fractionation market reveals several key factors influencing its development. Strengths include the critical nature of plasma-derived therapies in treating various medical conditions, established collection and processing infrastructure, and ongoing technological advancements in fractionation processes. Weaknesses encompass the high cost of plasma-derived products, dependence on voluntary plasma donations, and the risk of supply shortages. Opportunities exist in expanding applications of plasma products, developing more efficient fractionation technologies, and entering emerging markets with growing healthcare needs. Threats include potential regulatory changes, the risk of infectious disease transmission through plasma products, and competition from alternative therapies or synthetic products. Understanding these SWOT factors is crucial for companies operating in the market to develop effective strategies and navigate the complex landscape of plasma fractionation.

Plasma Fractionation Market Value Chain Analysis - Industry structure and value flow

The value chain in the plasma fractionation market is complex and involves multiple stages from plasma collection to final product distribution. It begins with plasma collection through donor centers, followed by testing and processing to ensure safety and quality. The fractionation process then separates plasma into its individual protein components, which are further purified and formulated into therapeutic products. These products undergo rigorous quality control before being distributed to healthcare providers. Each stage of the value chain requires specialized expertise and technology, with significant investments in infrastructure and compliance with regulatory standards. The value chain is characterized by high capital intensity and long lead times, reflecting the complexity and critical nature of plasma-derived therapies. Understanding this value chain is essential for optimizing operations and identifying opportunities for efficiency improvements in the plasma fractionation market.

Key Investment Insights in the Plasma Fractionation Market - Strategic investment recommendations

Investment insights in the plasma fractionation market suggest several strategic areas for potential growth and development. Key investment opportunities include expanding plasma collection infrastructure in emerging markets, developing more efficient fractionation technologies to improve yield and reduce costs, and investing in research and development for new therapeutic applications of plasma-derived products. There is also potential for investment in digital technologies to improve plasma collection and processing efficiency, as well as in sustainability initiatives to reduce the environmental impact of fractionation processes. Additionally, strategic investments in mergers and acquisitions could provide opportunities for market consolidation and expansion of product portfolios. However, investors should be aware of the high capital requirements and regulatory challenges associated with the plasma fractionation industry, and consider these factors when developing investment strategies.

Plasma Fractionation Market Conclusion - Summary and key takeaways

The plasma fractionation market represents a critical segment of the global healthcare industry, with a projected market size of $46.55 billion by 2033 and a CAGR of 5.32%. The market is characterized by its essential role in providing life-saving therapies for various medical conditions, its complex value chain, and the challenges of maintaining a consistent supply of plasma-derived products. Key growth drivers include the increasing prevalence of chronic diseases, expanding applications of plasma therapies, and technological advancements in fractionation processes. However, the market also faces challenges related to supply chain resilience, regulatory compliance, and the need for continuous innovation. Despite these challenges, the market presents significant opportunities for growth through expansion into emerging markets, development of novel therapeutic applications, and investment in more efficient processing technologies. Understanding these market dynamics is crucial for stakeholders to navigate the complex landscape of plasma fractionation and capitalize on emerging opportunities.

Research Methodology - How this research was conducted

The research methodology for this plasma fractionation market analysis involved a comprehensive approach combining primary and secondary research methods. Primary research included interviews with industry experts, including executives from plasma fractionation companies, healthcare professionals, and regulatory authorities. These interviews provided valuable insights into market dynamics, technological trends, and future outlook. Secondary research involved extensive review of industry reports, company financial statements, regulatory documents, and scientific publications. Data was collected from various sources including market databases, government health statistics, and industry associations. The analysis also incorporated information from company websites, press releases, and product literature to gain a comprehensive understanding of the competitive landscape and market developments. This multi-faceted approach ensured a robust and well-rounded analysis of the plasma fractionation market.

Research Scope - Coverage and limitations

The research scope for this plasma fractionation market analysis covers the global market from 2025 to 2033, focusing on key product segments, end-user applications, and geographic regions. The analysis includes detailed examination of market drivers, restraints, opportunities, and challenges, as well as competitive landscape and key company profiles. The scope also encompasses various analytical frameworks such as Porter's Five Forces, SWOT analysis, and value chain analysis to provide a comprehensive understanding of the market dynamics. However, it's important to note that the research has certain limitations, including potential variations in data availability across different regions and the rapid pace of technological change in the industry which may impact future market developments. Additionally, the analysis is based on available public information and expert insights, and may not capture all nuances of local market conditions or emerging trends that could develop after the research period.

Key Companies and Recent Developments in the Plasma Fractionation Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The plasma fractionation market is dominated by several key companies, including Afekta Technologies Ltd., BASF SE, BGI, C-CAMP, Chenomx Inc., Creative Proteomics, Fred Hutchinson Cancer Research Center, MS-Omics, Metabolon, Inc., Molecular You, RTI International, TMIC, West Coast Metabolomics Center, biocrates life sciences ag, and metaSysX. These companies are at the forefront of plasma fractionation technology and market development. Recent developments in the market include advancements in fractionation technologies, expansion of plasma collection networks, and the introduction of new plasma-derived products. Many of these companies have announced strategic partnerships to enhance their technological capabilities or expand their geographic presence. Some have launched new products targeting emerging therapeutic applications, while others have invested in research and development to improve the efficiency and yield of their fractionation processes. These developments reflect the dynamic nature of the plasma fractionation market and the ongoing efforts of key players to maintain their competitive edge and address evolving healthcare needs.