Bioethanol Market Overview - Definition, scope, and significance

Bioethanol, also known as ethanol or ethyl alcohol, is a renewable fuel produced from biomass through fermentation and distillation processes. It serves as a sustainable alternative to conventional gasoline, offering reduced greenhouse gas emissions and enhanced energy security. The bioethanol market encompasses the production, distribution, and utilization of this biofuel across various applications, primarily in transportation, but also extending to pharmaceutical, cosmetic, and food & beverage industries. The significance of bioethanol lies in its potential to reduce dependence on fossil fuels, mitigate climate change impacts, and support agricultural economies through the utilization of agricultural residues and dedicated energy crops.

Bioethanol Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The bioethanol market is driven by several key factors, including stringent environmental regulations promoting renewable energy adoption, growing concerns about climate change, and government initiatives supporting biofuel production through subsidies and mandates. Additionally, the increasing demand for cleaner transportation fuels and the need to reduce dependence on imported petroleum contribute to market growth. However, the market faces restraints such as competition with food production for feedstock, land use concerns, and the energy-intensive nature of bioethanol production. Challenges include technological limitations in cellulosic ethanol production, fluctuating feedstock prices, and infrastructure constraints for distribution and blending. Opportunities exist in the development of advanced production technologies, expansion into emerging markets, and the potential for bioethanol to serve as a platform chemical for various industrial applications.

Bioethanol Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the bioethanol market are characterized by the increasing adoption of higher ethanol blends, such as E15 and E85, in compatible vehicles. The development of second-generation bioethanol production technologies, utilizing non-food biomass sources like agricultural residues and municipal waste, is gaining momentum. Additionally, there is a growing trend towards integrated biorefineries that produce multiple products from biomass, enhancing overall process economics. Emerging trends include the use of algae as a feedstock for bioethanol production, the development of hybrid biofuel systems combining bioethanol with other renewable energy sources, and the exploration of bioethanol's potential in aviation and marine fuels. The market is also witnessing increased focus on sustainability and circular economy principles, with efforts to minimize waste and maximize resource efficiency throughout the bioethanol value chain.

COVID-19 Impact on the Bioethanol Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the bioethanol market, primarily through disruptions in supply chains, reduced fuel demand due to lockdowns and travel restrictions, and volatility in feedstock prices. The decline in transportation fuel consumption led to decreased demand for bioethanol, affecting production levels and profitability for many producers. However, the pandemic also highlighted the importance of resilient and sustainable energy systems, potentially accelerating long-term investments in renewable energy technologies, including bioethanol. As economies recover, the bioethanol market is expected to regain momentum, supported by economic stimulus packages promoting green recovery and the continued implementation of renewable fuel standards. The recovery trajectory may be characterized by a gradual increase in demand, with potential for accelerated growth as global energy policies increasingly favor low-carbon alternatives.

Bioethanol Market Competitive Landscape - Major competitors and market consolidation

The bioethanol market features a competitive landscape with several major players and a mix of large multinational corporations and regional producers. Key companies such as ADM, BP, Cargill, and Shell have established significant market presence through extensive production capacities and global distribution networks. The market is characterized by vertical integration, with many companies involved in both feedstock production and bioethanol manufacturing. Consolidation trends are evident, with larger companies acquiring smaller producers to expand market share and technological capabilities. Competition is driven by factors such as production efficiency, feedstock costs, technological innovation, and strategic partnerships. The competitive landscape is also influenced by regional policies and mandates, which can create varying market dynamics across different geographies. As the market evolves, competition is expected to intensify, particularly in the development of advanced bioethanol technologies and the expansion into new application areas.

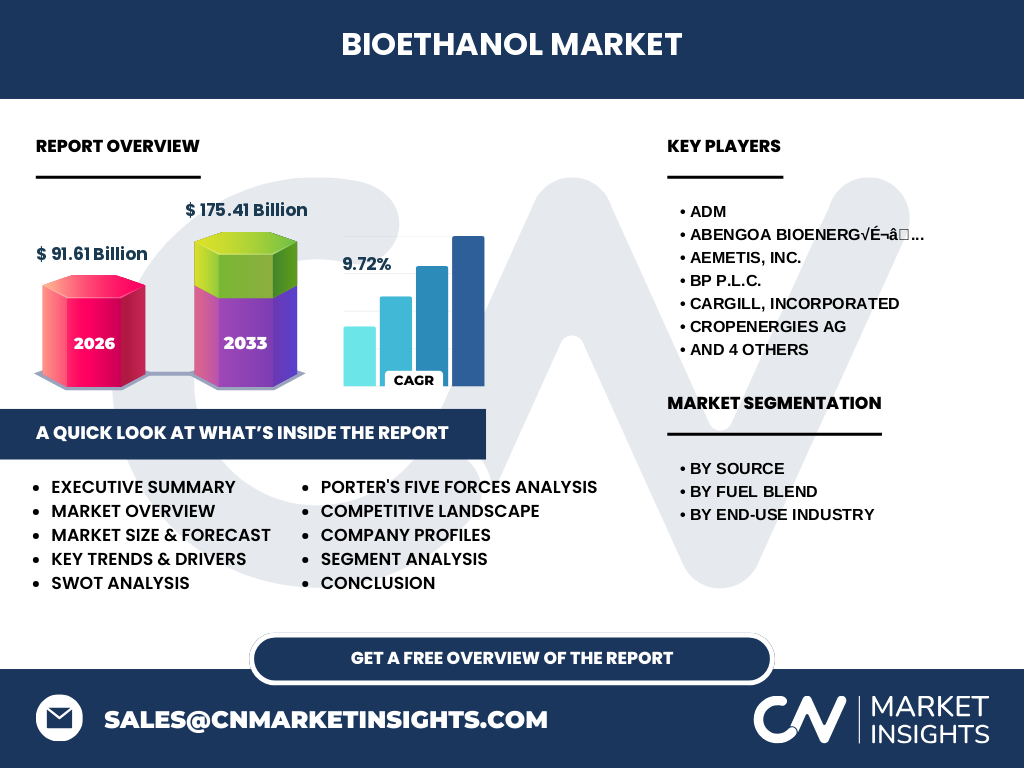

Executive Summary - High-level overview and key findings about Bioethanol Market

The bioethanol market represents a significant segment of the renewable energy industry, driven by the global push for sustainable fuel alternatives and reduced carbon emissions. With a market size of 91.61 Billion in 2026 and a projected growth to 175.41 Billion by 2033 at a CAGR of 9.72%, the market demonstrates strong potential for expansion. Key findings indicate a diverse market segmentation by source, fuel blend, and end-use industry, with transportation remaining the dominant application. The market is characterized by technological advancements in production processes, particularly in cellulosic ethanol, and increasing government support through mandates and incentives. However, challenges such as feedstock competition and infrastructure limitations persist. The competitive landscape is dominated by major players with significant investments in research and development. Overall, the bioethanol market is poised for substantial growth, driven by environmental concerns, energy security needs, and supportive regulatory frameworks.

Bioethanol Market Forecast - Projections for 2025-2032 period

The bioethanol market forecast for the 2025-2032 period indicates robust growth, with the market expected to expand from its 2026 size of 91.61 Billion to 175.41 Billion by 2033. This represents a compound annual growth rate (CAGR) of 9.72%, reflecting strong market momentum and increasing adoption of bioethanol across various applications. The forecast is underpinned by several factors, including the continued implementation of renewable fuel standards, growing environmental concerns, and technological advancements in bioethanol production. The transportation sector is expected to remain the primary driver of demand, particularly with the increasing adoption of higher ethanol blends in compatible vehicles. Additionally, emerging applications in the pharmaceutical, cosmetic, and food & beverage industries are projected to contribute to market growth. Regional variations in growth rates are anticipated, with developing economies potentially showing higher growth rates due to increasing energy demand and supportive government policies.

Bioethanol Market Size and Share by Segmentation - Breakdown by {segmentData}

The bioethanol market segmentation reveals a diverse landscape across various categories. By source, the market is divided into starch-based, sugar-based, and cellulose-based bioethanol. Starch-based bioethanol, derived from corn and other grains, currently dominates the market due to established production technologies and economies of scale. Sugar-based bioethanol, produced from sugarcane and sugar beet, is particularly prevalent in Brazil and other tropical regions. Cellulose-based bioethanol, although representing a smaller share currently, is expected to grow significantly due to its potential for utilizing non-food biomass. By fuel blend, the market is segmented into E5 to E10, E15 to E70, and E75 to E85. E5 to E10 blends are widely used in conventional vehicles, while higher blends require flex-fuel vehicles. The end-use industry segmentation includes transportation, pharmaceutical, cosmetic, and food & beverage sectors, with transportation accounting for the largest share due to bioethanol's primary use as a fuel additive and alternative fuel.

Global Bioethanol Market Size and Share by Region - Geographic distribution

The global bioethanol market exhibits significant regional variations in terms of production, consumption, and market share. North America, particularly the United States, represents a major market due to extensive corn-based bioethanol production and supportive government policies such as the Renewable Fuel Standard. South America, led by Brazil, is another significant region, known for its sugarcane-based bioethanol industry and widespread use of flex-fuel vehicles. Europe shows growing adoption of bioethanol, driven by EU renewable energy targets and carbon reduction goals. The Asia-Pacific region is emerging as a potential growth market, with countries like China and India exploring bioethanol production to address energy security concerns and reduce air pollution. Africa, while currently a smaller market, presents opportunities for growth due to abundant agricultural resources and increasing energy demand. Regional market shares are influenced by factors such as feedstock availability, government policies, vehicle fleet composition, and existing fuel infrastructure.

Regional Analysis of the Bioethanol Market - Detailed regional market performance

The regional analysis of the bioethanol market reveals distinct performance characteristics across different geographies. In North America, the United States leads with a mature bioethanol industry, driven by corn-based production and the Renewable Fuel Standard. The region benefits from advanced production technologies and a well-established distribution network. South America, particularly Brazil, showcases a unique model of bioethanol integration, with widespread use of flex-fuel vehicles and a strong sugarcane-based industry. The region's tropical climate favors sugarcane cultivation, providing a competitive advantage in production costs. Europe's bioethanol market is characterized by a focus on sustainability and advanced production technologies, with countries like Germany and France leading in production capacity. The Asia-Pacific region presents a diverse landscape, with countries like China and India showing increasing interest in bioethanol to address energy security and environmental concerns. Africa's potential is significant due to abundant agricultural resources, but market development is hindered by infrastructure challenges and policy uncertainties in many countries.

Leading Company Profiles in the Bioethanol Market - Industry players and strategies

The bioethanol market is dominated by several key players, each with distinct strategies and market positions. ADM, a global leader in agricultural processing, has a strong presence in bioethanol production, leveraging its extensive supply chain and research capabilities. Abengoa Bioenergía, a Spanish multinational, specializes in advanced bioethanol technologies and has significant production capacity in Europe and the Americas. Aemetis, Inc., based in the United States, focuses on renewable fuels and biochemicals, with a growing bioethanol portfolio. BP p.l.c., a major oil and gas company, has invested in bioethanol production as part of its renewable energy strategy. Cargill, Incorporated, another agricultural giant, integrates bioethanol production with its broader agribusiness operations. CropEnergies AG, a European leader, emphasizes sustainable bioethanol production and has a strong presence in the German market. POET, LLC, based in the United States, is one of the largest bioethanol producers globally, known for its innovative production processes. Shell, a major oil company, has invested in bioethanol as part of its transition to lower-carbon energy solutions. Tereos, a French cooperative, is a significant player in sugar-based bioethanol production. The Andersons, Inc., an American company, has a diversified agribusiness portfolio that includes bioethanol production.

Porter's Five Forces Analysis of the Bioethanol Market - Competitive forces assessment

Porter's Five Forces analysis provides insight into the competitive dynamics of the bioethanol market. The threat of new entrants is moderate, as significant capital investment is required for production facilities, but technological advancements may lower barriers to entry over time. The bargaining power of suppliers, primarily feedstock producers, is moderate to high, as feedstock costs significantly impact production economics. However, diversification of feedstock sources can mitigate this risk. The bargaining power of buyers, including fuel distributors and end-users, is moderate, influenced by the availability of alternative fuels and government mandates. The threat of substitutes is moderate, with electric vehicles and other alternative fuels presenting competition, but bioethanol's established infrastructure and compatibility with existing engines provide a competitive advantage. Competitive rivalry within the industry is high, driven by the presence of large multinational companies and regional producers competing on factors such as production efficiency, cost, and sustainability credentials.

SWOT Analysis of the Bioethanol Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the bioethanol market reveals several key factors. Strengths include the renewable nature of bioethanol, its potential for reducing greenhouse gas emissions, and its compatibility with existing fuel infrastructure. The established production technologies and growing government support also contribute to the market's strengths. Weaknesses encompass the competition with food production for feedstock, the energy-intensive nature of production processes, and the limited availability of advanced production technologies for cellulosic ethanol. Opportunities in the market include the development of second-generation bioethanol technologies, expansion into emerging markets, and the potential for bioethanol to serve as a platform chemical for various industrial applications. Threats to the market include fluctuating feedstock prices, potential changes in government policies and mandates, and the increasing adoption of electric vehicles as an alternative to liquid fuels. Additionally, environmental concerns related to land use changes and water consumption in bioethanol production present ongoing challenges.

Bioethanol Market Value Chain Analysis - Industry structure and value flow

The bioethanol market value chain encompasses several key stages, from feedstock production to end-use consumption. The chain begins with feedstock cultivation, which includes crops like corn, sugarcane, and other biomass sources. This is followed by feedstock processing and transportation to production facilities. The core of the value chain is the bioethanol production process, involving fermentation and distillation. Quality control and blending with gasoline occur at production facilities or distribution terminals. The distribution stage involves transportation via pipelines, rail, or trucks to fuel retailers. At the retail level, bioethanol blends are made available to consumers through gas stations. Throughout the value chain, various stakeholders add value, including farmers, processors, producers, distributors, and retailers. The value chain is characterized by significant capital investments, particularly in production facilities, and is influenced by factors such as feedstock prices, energy costs, and government policies. Emerging trends in the value chain include the development of integrated biorefineries and efforts to improve overall sustainability and efficiency.

Key Investment Insights in the Bioethanol Market - Strategic investment recommendations

Investment insights in the bioethanol market highlight several strategic considerations for potential investors. The market presents opportunities for investment in production capacity expansion, particularly in regions with supportive government policies and abundant feedstock resources. Investments in advanced production technologies, such as cellulosic ethanol and integrated biorefineries, offer potential for higher returns and reduced environmental impact. Strategic partnerships between feedstock producers, technology providers, and fuel distributors can create synergies and mitigate risks throughout the value chain. Geographic diversification is recommended to balance exposure to regional policy changes and market dynamics. Additionally, investments in research and development to improve production efficiency and explore new applications for bioethanol beyond fuel can provide competitive advantages. Investors should also consider the potential impact of electric vehicle adoption on long-term demand for bioethanol and explore opportunities in emerging markets with growing energy needs. Sustainability and carbon footprint reduction are becoming increasingly important factors in investment decisions within the bioethanol sector.

Bioethanol Market Conclusion - Summary and key takeaways

The bioethanol market represents a significant component of the global renewable energy landscape, characterized by steady growth and evolving technologies. Key takeaways from the market analysis include the strong projected growth trajectory, with the market expected to nearly double in size by 2033, driven by a CAGR of 9.72%. The market's diversity in terms of feedstock sources, fuel blends, and end-use applications provides resilience and multiple avenues for expansion. While the transportation sector remains the dominant application, emerging uses in pharmaceutical, cosmetic, and food & beverage industries offer additional growth opportunities. The competitive landscape is dominated by major players with significant investments in production capacity and technology development. However, challenges such as feedstock competition, infrastructure limitations, and the rise of alternative technologies like electric vehicles present ongoing considerations for market participants. Overall, the bioethanol market is poised for continued growth, supported by environmental concerns, energy security needs, and supportive government policies, but success will depend on addressing technological and sustainability challenges while adapting to changing market dynamics.

Research Methodology - How this research was conducted

The research methodology for this bioethanol market analysis involved a comprehensive approach combining primary and secondary research methods. Primary research included interviews with industry experts, bioethanol producers, and market analysts to gather insights on current market trends, challenges, and future projections. Secondary research involved extensive review of industry reports, government publications, and company financial statements to compile quantitative data on market size, growth rates, and competitive landscape. Data triangulation techniques were employed to validate findings across multiple sources. The analysis incorporated both top-down and bottom-up approaches to estimate market size and forecast future growth. Regional variations were considered by examining country-specific policies, production capacities, and consumption patterns. The research also took into account technological developments in bioethanol production and emerging applications to provide a holistic view of the market. Limitations of the study include potential data gaps in certain regions and the inherent uncertainties in long-term market forecasting.

Research Scope - Coverage and limitations

The research scope for this bioethanol market analysis encompasses a comprehensive examination of the global bioethanol industry, covering market size, growth trends, competitive landscape, and regional variations. The study includes detailed segmentation by source (starch-based, sugar-based, and cellulose-based), fuel blend (E5 to E10, E15 to E70, and E75 to E85), and end-use industry (transportation, pharmaceutical, cosmetic, and food & beverage). The analysis covers the period from 2026 to 2033, with a focus on the projected growth from 91.61 Billion to 175.41 Billion at a CAGR of 9.72%. The research includes profiles of key market players and an assessment of market dynamics using tools such as Porter's Five Forces and SWOT analysis. Limitations of the study include the exclusion of certain niche bioethanol applications and potential regional data gaps. The analysis is based on available public information and expert insights, and actual market conditions may vary due to unforeseen economic, technological, or policy changes.

Key Companies and Recent Developments in the Bioethanol Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The bioethanol market features several key players with significant recent developments shaping the industry landscape. ADM has been focusing on expanding its production capacity and investing in advanced biofuel technologies. Abengoa Bioenergía has announced partnerships to develop new bioethanol production facilities, particularly in emerging markets. Aemetis, Inc. has made headlines with its plans to convert traditional ethanol plants to produce sustainable aviation fuel. BP p.l.c. has been actively investing in bioenergy projects, including bioethanol production, as part of its transition strategy towards lower-carbon energy solutions. Cargill, Incorporated has announced collaborations to improve the sustainability of its bioethanol supply chain and explore new feedstock options. CropEnergies AG has been investing in research to enhance production efficiency and reduce carbon intensity. POET, LLC has launched initiatives to expand its market presence and develop new applications for bioethanol beyond fuel. Shell has been involved in strategic partnerships to advance bioethanol technologies and explore opportunities in sustainable aviation fuels. Tereos has announced plans to increase its bioethanol production capacity and improve the sustainability of its operations. The Andersons, Inc. has been focusing on optimizing its production processes and exploring new market opportunities for its bioethanol products. These developments reflect the industry's focus on technological advancement, sustainability, and market expansion.