Privacy Management Software Market Overview - Definition, scope, and significance

Privacy Management Software refers to a category of solutions designed to help organizations manage, monitor, and ensure compliance with data privacy regulations and policies. These software tools provide comprehensive frameworks for data governance, risk assessment, consent management, and privacy impact analysis. The market encompasses applications that enable businesses to track personal data across their systems, automate compliance workflows, generate regulatory reports, and implement privacy-by-design principles. As data protection regulations like GDPR, CCPA, and other global privacy laws continue to evolve, Privacy Management Software has become essential for organizations handling sensitive personal information, offering capabilities to minimize privacy risks while maintaining operational efficiency.

Privacy Management Software Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the Privacy Management Software market include the increasing stringency of global data protection regulations, rising data breach incidents, and growing consumer awareness about privacy rights. Organizations face mounting pressure to demonstrate compliance and protect sensitive information, creating strong demand for automated privacy solutions. However, the market faces restraints such as high implementation costs, complex integration with existing systems, and the need for specialized expertise. Challenges include keeping pace with rapidly evolving regulatory requirements, managing privacy across multiple jurisdictions, and addressing legacy system limitations. Opportunities exist in emerging markets with developing privacy frameworks, AI-powered privacy automation, and expansion into new industry verticals beyond traditional sectors like BFSI and healthcare.

Privacy Management Software Market Growth Trends - Current and emerging trends shaping the market

The Privacy Management Software market is experiencing several notable growth trends, including the shift toward cloud-based deployment models for enhanced scalability and accessibility. AI and machine learning integration is becoming increasingly prevalent, enabling automated data discovery, risk assessment, and compliance monitoring. The market is also seeing growing adoption of privacy management solutions across SMEs as regulatory pressures extend beyond large enterprises. Integration with other governance, risk, and compliance (GRC) platforms is creating unified compliance ecosystems. Additionally, the rise of privacy-as-a-service offerings and the development of industry-specific privacy solutions are shaping market dynamics, while privacy-enhancing technologies (PETs) are gaining traction as complementary solutions.

COVID-19 Impact on the Privacy Management Software Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly accelerated the Privacy Management Software market as organizations rapidly shifted to remote work models, creating new privacy challenges and compliance requirements. The pandemic highlighted the need for robust privacy frameworks to manage increased data collection for contact tracing, health monitoring, and remote workforce management. Organizations accelerated privacy software adoption to address new regulatory concerns around data handling in distributed work environments. The market experienced temporary supply chain disruptions and implementation delays during initial lockdowns, but demand rebounded strongly as businesses recognized the critical importance of privacy management in the new normal. The pandemic has permanently elevated privacy considerations in digital transformation initiatives.

Privacy Management Software Market Competitive Landscape - Major competitors and market consolidation

The Privacy Management Software market features a competitive landscape with both established technology giants and specialized privacy solution providers. Key players include IBM Corporation with its comprehensive privacy portfolio, OneTrust LLC as a market leader in privacy management platforms, and RSA Security LLC with enterprise-grade privacy solutions. The market is witnessing consolidation through strategic acquisitions as larger companies seek to enhance their privacy capabilities. Competition is intensifying around AI-powered automation, user experience, and integration capabilities. Companies are differentiating through specialized industry expertise, geographic coverage, and the ability to address emerging privacy regulations. The competitive dynamics are shaped by the need for continuous innovation to address evolving privacy challenges and regulatory requirements.

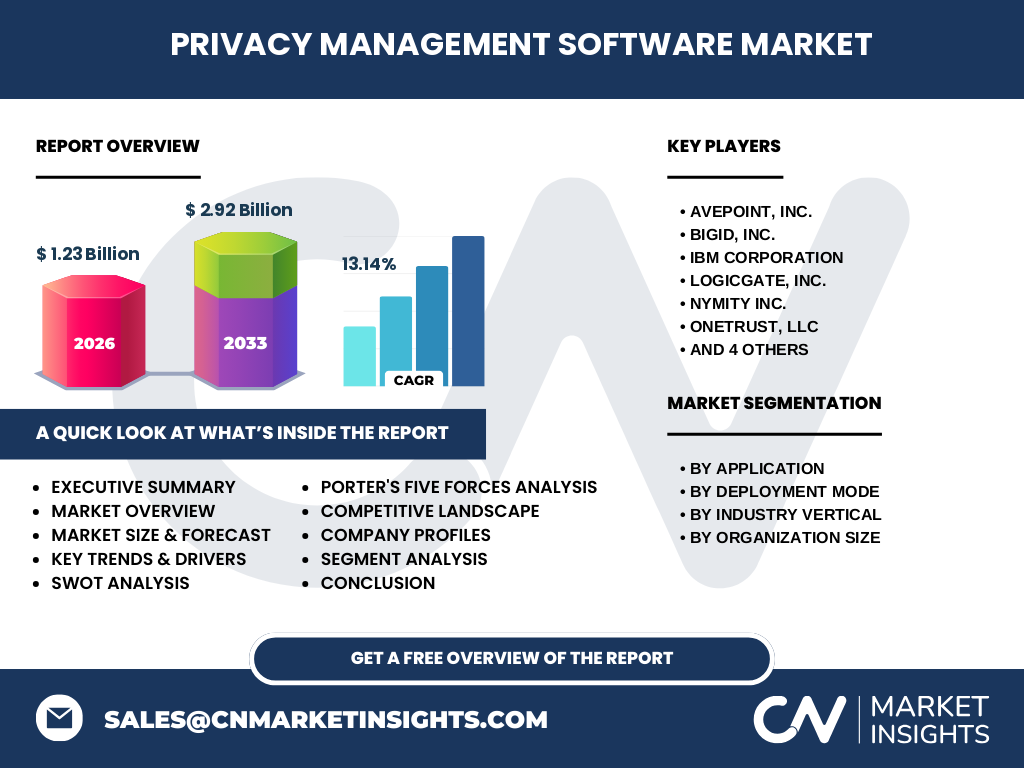

Executive Summary - High-level overview and key findings about Privacy Management Software Market

The Privacy Management Software market is experiencing robust growth driven by increasing regulatory pressures and growing awareness of data privacy importance. The market is projected to grow from $1.23 billion in 2026 to $2.92 billion by 2033, representing a strong CAGR of 13.14%. Organizations across all industry verticals are recognizing the critical need for comprehensive privacy management solutions to navigate complex regulatory landscapes and protect sensitive data. The market is characterized by rapid technological innovation, particularly in AI and automation capabilities, and a shift toward cloud-based deployment models. As privacy regulations continue to evolve globally, the demand for sophisticated privacy management tools is expected to accelerate, creating significant opportunities for solution providers who can deliver comprehensive, scalable, and user-friendly platforms.

Privacy Management Software Market Forecast - Projections for 2025-2032 period

The Privacy Management Software market is projected to experience substantial growth during the 2025-2032 period, with the market size expected to reach $2.92 billion by 2033 from $1.23 billion in 2026. This represents a compound annual growth rate (CAGR) of 13.14% over the forecast period. The growth trajectory is supported by increasing regulatory enforcement, expanding digital transformation initiatives, and growing awareness of privacy risks across organizations of all sizes. The forecast period will likely see accelerated adoption of AI-powered privacy solutions, increased integration with existing enterprise systems, and expansion into emerging markets with developing privacy frameworks. Cloud-based solutions are expected to dominate deployment preferences, while industry-specific solutions will gain traction in highly regulated sectors.

Privacy Management Software Market Size and Share by Segmentation - Breakdown by {segmentData}

The Privacy Management Software market is segmented across multiple dimensions, with Compliance Management applications representing the largest segment due to regulatory requirements driving primary adoption. Risk Management solutions are experiencing the fastest growth as organizations prioritize proactive privacy risk assessment. Cloud deployment is gaining market share over on-premises solutions, driven by scalability and cost advantages. The BFSI sector currently dominates industry vertical adoption, followed by Government and Defense due to strict regulatory requirements. Large Enterprises account for the majority of market share, though SME adoption is accelerating as privacy regulations extend to smaller organizations. The market shows strong growth potential across all segments, with emerging applications in reporting and analytics gaining traction as organizations seek comprehensive privacy insights.

Global Privacy Management Software Market Size and Share by Region - Geographic distribution

The global Privacy Management Software market demonstrates varied regional adoption patterns, with North America currently holding the largest market share due to stringent privacy regulations like CCPA and high awareness levels. Europe follows closely, driven by GDPR requirements and mature privacy frameworks. The Asia-Pacific region is experiencing the fastest growth rate, fueled by emerging privacy regulations in countries like China, India, and Japan, along with rapid digital transformation. Latin America and Middle East & Africa regions are showing increasing adoption as privacy awareness grows and regulations develop. Regional variations in regulatory requirements, digital maturity, and privacy awareness levels create distinct market dynamics, with mature markets focusing on advanced features while emerging markets prioritize basic compliance capabilities.

Regional Analysis of the Privacy Management Software Market - Detailed regional market performance

Regional analysis reveals distinct market characteristics across different geographies. North America leads in market maturity and technology adoption, with strong demand for advanced privacy management solutions and integration capabilities. Europe maintains high standards for privacy compliance, driving demand for comprehensive GDPR-focused solutions. The Asia-Pacific region presents significant growth opportunities, with countries like Singapore, Australia, and Japan showing strong adoption rates, while emerging economies are beginning to implement privacy frameworks. Latin America is experiencing gradual adoption growth as privacy regulations develop, with Brazil's LGPD driving initial market development. Middle East & Africa regions are showing increasing interest in privacy management, particularly in Gulf Cooperation Council countries implementing new data protection regulations.

Leading Company Profiles in the Privacy Management Software Market - Industry players and strategies

Leading companies in the Privacy Management Software market include AvePoint, Inc., known for its comprehensive compliance and privacy solutions for enterprise collaboration platforms. BigID, Inc. specializes in AI-powered data discovery and privacy management, offering advanced capabilities for identifying and protecting sensitive information. IBM Corporation provides enterprise-grade privacy solutions as part of its broader governance portfolio. LogicGate, Inc. offers integrated risk and compliance platforms with strong privacy management capabilities. Nymity Inc. focuses on privacy research and benchmarking services. OneTrust, LLC has emerged as a market leader with its comprehensive privacy management platform. Protiviti Inc. provides consulting and technology solutions for privacy compliance. RSA Security LLC offers enterprise privacy and security solutions. SureCloud provides integrated governance, risk, and compliance platforms. TrustArc Inc. specializes in privacy compliance and risk management solutions.

Porter's Five Forces Analysis of the Privacy Management Software Market - Competitive forces assessment

Porter's Five Forces analysis reveals a moderately competitive market structure in the Privacy Management Software industry. The threat of new entrants is moderate due to high technical requirements and regulatory complexity, though emerging startups continue to enter the market with innovative solutions. Supplier power is relatively low as software components are widely available, though specialized privacy expertise remains valuable. Buyer power is increasing as organizations become more sophisticated in their privacy requirements and demand integrated solutions. The threat of substitutes is low as privacy management requires specialized capabilities that general compliance tools cannot fully provide. Competitive rivalry is intense, with numerous players competing on features, pricing, and integration capabilities, driving continuous innovation and market consolidation.

SWOT Analysis of the Privacy Management Software Market - Strengths, weaknesses, opportunities, threats

Strengths of the Privacy Management Software market include strong regulatory tailwinds driving demand, growing awareness of privacy importance, and technological advancements in AI and automation. Weaknesses include high implementation complexity, integration challenges with legacy systems, and the need for specialized expertise. Opportunities exist in emerging markets with developing privacy frameworks, expansion into new industry verticals, and the integration of privacy with broader governance platforms. Threats include rapidly evolving regulatory requirements creating uncertainty, potential market saturation in mature regions, and competition from established enterprise software vendors expanding into privacy management. The market's future success will depend on addressing implementation challenges while capitalizing on growing privacy awareness and regulatory developments.

Privacy Management Software Market Value Chain Analysis - Industry structure and value flow

The Privacy Management Software market value chain encompasses several key components, beginning with technology providers who develop core privacy management platforms and tools. System integrators and implementation partners play a crucial role in deploying and customizing solutions for specific organizational needs. Consulting firms provide strategic guidance and compliance expertise to complement software capabilities. Training and support services ensure successful adoption and ongoing compliance. Value flows from technology innovation through implementation services to end-user organizations, with differentiation occurring through specialized features, industry expertise, and integration capabilities. The value chain is characterized by strong interdependencies between technology providers, implementation partners, and consulting firms, creating an ecosystem approach to privacy management solutions.

Key Investment Insights in the Privacy Management Software Market - Strategic investment recommendations

Strategic investment insights for the Privacy Management Software market indicate strong potential in AI-powered automation capabilities, which can significantly reduce manual compliance efforts and improve accuracy. Investment in cloud-native solutions is recommended as organizations increasingly prefer scalable, accessible platforms. Geographic expansion into emerging markets with developing privacy regulations presents attractive opportunities, particularly in Asia-Pacific and Latin American regions. Integration capabilities with existing enterprise systems represent a key investment area, as organizations seek unified governance platforms. Investment in industry-specific solutions for highly regulated sectors like healthcare and financial services can provide competitive advantages. Additionally, development of privacy-enhancing technologies and advanced analytics capabilities are recommended investment areas to address evolving market needs.

Privacy Management Software Market Conclusion - Summary and key takeaways

The Privacy Management Software market is positioned for significant growth, driven by increasing regulatory requirements, growing privacy awareness, and technological advancements. With a projected market size of $2.92 billion by 2033 and a strong CAGR of 13.14%, the market presents substantial opportunities for solution providers who can address evolving privacy challenges. Key success factors include the ability to provide comprehensive, integrated solutions that address multiple privacy requirements while offering user-friendly interfaces and automation capabilities. The market is characterized by rapid innovation, particularly in AI and cloud technologies, and shows strong potential for geographic expansion and industry-specific solutions. Organizations that can navigate regulatory complexity while delivering scalable, accessible solutions will be well-positioned to capture market opportunities.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology combining primary and secondary research approaches. Primary research involved interviews with industry experts, privacy professionals, and technology providers to gather insights on market trends, challenges, and opportunities. Secondary research included analysis of company reports, regulatory documents, industry publications, and market data to validate findings and establish market size estimates. The research methodology employed both top-down and bottom-up approaches to ensure accurate market sizing and forecasting. Data triangulation techniques were used to cross-verify information from multiple sources, while expert validation ensured the reliability of key findings and projections. The research covered the period from 2025 to 2032, with 2026 established as the base year for market calculations.

Research Scope - Coverage and limitations

The research scope encompasses the global Privacy Management Software market, including analysis of market size, growth trends, competitive landscape, and regional dynamics from 2025 to 2032. The study covers key market segments including application types, deployment modes, industry verticals, and organization sizes. Geographic coverage includes major regions such as North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The research focuses on commercial Privacy Management Software solutions, excluding open-source tools and internal development projects. Limitations include the exclusion of certain emerging markets with limited available data, potential variations in regional privacy regulation interpretation, and the rapid evolution of privacy technologies that may impact long-term projections. The research provides insights based on available data and expert analysis, acknowledging that market dynamics may evolve differently than projected.

Key Companies and Recent Developments in the Privacy Management Software Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Key companies in the Privacy Management Software market have demonstrated significant recent developments and strategic initiatives. AvePoint, Inc. has expanded its privacy compliance solutions for Microsoft 365 environments, enhancing data governance capabilities for enterprise collaboration platforms. BigID, Inc. launched advanced AI-powered privacy automation tools, improving data discovery and classification accuracy. IBM Corporation announced enhanced privacy management integration with its broader Watson AI platform, providing more sophisticated privacy analytics capabilities. LogicGate, Inc. formed strategic partnerships with major consulting firms to expand its integrated risk management platform adoption. Nymity Inc. released updated privacy benchmarking frameworks and compliance assessment tools. OneTrust, LLC introduced new automation features and expanded its global compliance coverage. Protiviti Inc. launched enhanced privacy consulting services integrated with technology solutions. RSA Security LLC announced improved privacy analytics and reporting capabilities. SureCloud expanded its integrated GRC platform with enhanced privacy management features. TrustArc Inc. released updated compliance automation tools and expanded its regulatory coverage. These developments reflect the market's focus on automation, integration, and expanded capabilities to address evolving privacy requirements.