Antibody Drug Conjugates Market Overview - Definition, scope, and significance

Antibody Drug Conjugates (ADCs) represent a revolutionary class of targeted cancer therapeutics that combine the specificity of monoclonal antibodies with the potent cytotoxicity of small molecule drugs. These biopharmaceutical agents are designed to selectively deliver cytotoxic payloads directly to cancer cells, minimizing damage to healthy tissues while maximizing therapeutic efficacy. The market encompasses the development, manufacturing, and commercialization of ADCs across various cancer types, targeting different antigens and utilizing diverse linker technologies. The significance of this market lies in its potential to transform cancer treatment paradigms, offering more precise and effective therapies for patients with previously limited treatment options.

Antibody Drug Conjugates Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the ADC market include the increasing global cancer burden, advancements in antibody engineering and linker technologies, and the growing demand for targeted therapies with improved safety profiles. The rising prevalence of HER2-positive breast cancer and other targetable cancers has created a robust patient population for ADC treatments. Additionally, the expanding pipeline of novel ADCs and the potential for combination therapies with other cancer treatments are fueling market growth. However, the market faces restraints such as the high cost of ADC development and manufacturing, complex regulatory pathways, and potential for resistance mechanisms. Challenges include optimizing linker stability, improving tumor penetration, and managing off-target toxicity. Opportunities exist in expanding ADC applications to new cancer types, developing next-generation ADCs with improved efficacy, and exploring ADC combinations with immunotherapy and other treatment modalities.

Antibody Drug Conjugates Market Growth Trends - Current and emerging trends shaping the market

The ADC market is experiencing significant growth trends driven by technological advancements and expanding therapeutic applications. One key trend is the development of novel linker technologies, including cleavable and non-cleavable linkers, which enhance drug stability and target specificity. The market is also witnessing a shift towards ADCs targeting new antigens beyond traditional targets like HER2 and CD22, opening up opportunities in previously underserved cancer types. Another emerging trend is the use of advanced antibody engineering techniques to improve ADC pharmacokinetics and tumor targeting. The industry is also seeing increased focus on bispecific ADCs and antibody-drug conjugate combinations with checkpoint inhibitors, which could significantly enhance treatment efficacy. Additionally, there is a growing trend towards personalized ADC therapies based on patient-specific biomarkers, which could revolutionize treatment approaches in the coming years.

COVID-19 Impact on the Antibody Drug Conjugates Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a mixed impact on the ADC market. While the initial phase of the pandemic led to disruptions in clinical trials, supply chain interruptions, and delays in new product launches, the market demonstrated resilience due to the critical nature of cancer treatments. The pandemic accelerated certain trends, such as the adoption of decentralized clinical trial models and increased focus on manufacturing efficiency. However, it also highlighted the need for robust supply chains and contingency planning in the biopharmaceutical industry. As the world recovers from the pandemic, the ADC market is experiencing a rebound, with accelerated clinical trial recruitment and renewed focus on pipeline development. The lessons learned during the pandemic are likely to drive long-term improvements in ADC development and commercialization strategies, potentially leading to more efficient and resilient market growth in the post-COVID era.

Antibody Drug Conjugates Market Competitive Landscape - Major competitors and market consolidation

The ADC market is characterized by a mix of large pharmaceutical companies and specialized biotechnology firms, creating a competitive landscape with diverse strengths and strategies. Major players like Roche, AstraZeneca, and Johnson & Johnson leverage their extensive resources and global reach to develop and commercialize ADCs, while smaller companies like ADC Therapeutics focus on niche areas of innovation. The market is witnessing increased consolidation through mergers, acquisitions, and strategic partnerships, as companies seek to strengthen their ADC portfolios and access complementary technologies. For instance, recent collaborations between ADC developers and companies with expertise in antibody engineering or novel linker technologies are becoming more common. This competitive environment is driving rapid innovation but also creating challenges for smaller players in terms of resource allocation and market access. The landscape is expected to evolve further as new entrants emerge and existing players expand their ADC capabilities through various strategic initiatives.

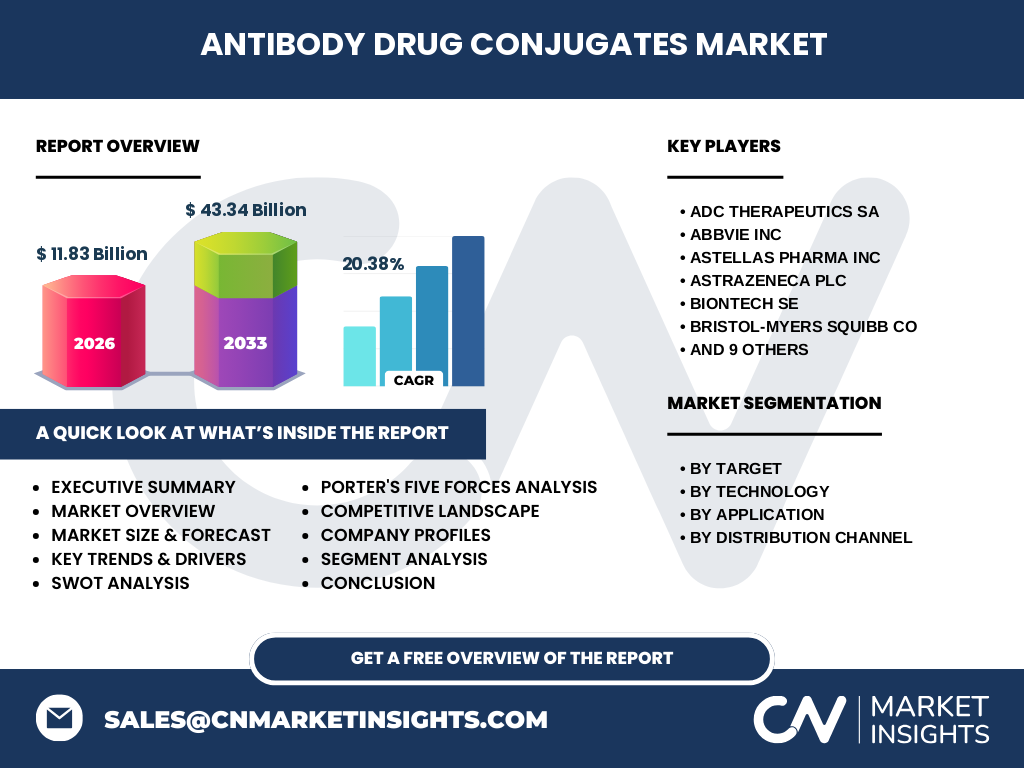

Executive Summary - High-level overview and key findings about Antibody Drug Conjugates Market

The Antibody Drug Conjugates market is poised for substantial growth, with the market size expected to increase from 11.83 Billion in 2026 to 43.34 Billion by 2033, representing a robust CAGR of 20.38%. This growth is driven by the increasing demand for targeted cancer therapies, advancements in ADC technologies, and the expanding pipeline of novel ADCs. The market is characterized by diverse segmentation across targets, technologies, applications, and distribution channels, with HER2-targeted ADCs and cleavable linker technologies currently dominating the market. Blood cancer remains the largest application segment, while retail pharmacies are the primary distribution channel. The competitive landscape is dynamic, with both established pharmaceutical giants and specialized biotech firms vying for market share through innovation and strategic partnerships. Despite challenges related to development costs and regulatory complexities, the market presents significant opportunities for growth, particularly in emerging markets and through the development of next-generation ADCs targeting new cancer types.

Antibody Drug Conjugates Market Forecast - Projections for 2025-2032 period

The ADC market is projected to experience robust growth over the forecast period from 2025 to 2032, with the market size expected to increase from 11.83 Billion in 2026 to 43.34 Billion by 2033. This represents a compound annual growth rate (CAGR) of 20.38%, indicating strong market momentum. The forecast is based on several factors, including the increasing prevalence of targetable cancers, the expanding pipeline of novel ADCs, and the growing adoption of targeted therapies in oncology. Key drivers of this growth include the successful commercialization of recently approved ADCs, the potential for combination therapies, and the expansion of ADC applications to new cancer types. The market is also expected to benefit from advancements in ADC technologies, such as improved linker designs and novel payload molecules. However, the forecast takes into account potential challenges such as regulatory hurdles, manufacturing complexities, and pricing pressures that may impact market growth.

Antibody Drug Conjugates Market Size and Share by Segmentation - Breakdown by {segmentData}

The ADC market is segmented across various dimensions, each contributing to the overall market dynamics. By target, HER2-targeted ADCs currently dominate the market due to the high prevalence of HER2-positive cancers and the success of established therapies like trastuzumab emtansine. However, CD22 and CD30 targeted ADCs are gaining traction, particularly in blood cancers. In terms of technology, cleavable linkers hold a significant market share due to their ability to release the cytotoxic payload inside target cells, enhancing efficacy. The application segment is led by blood cancer, reflecting the success of ADCs in hematological malignancies. However, solid tumors, particularly breast and lung cancers, represent growing opportunities. By distribution channel, retail pharmacies account for the largest share, followed by hospital pharmacies, with online pharmacies emerging as a growing segment, especially in regions with advanced healthcare infrastructure. This segmentation highlights the diverse nature of the ADC market and the various factors influencing its growth across different segments.

Global Antibody Drug Conjugates Market Size and Share by Region - Geographic distribution

While specific regional market share data is not provided, the global ADC market is expected to exhibit varied growth patterns across different geographic regions. North America, particularly the United States, is likely to maintain its position as the largest market due to factors such as high healthcare expenditure, advanced research infrastructure, and a large patient population with targetable cancers. Europe is expected to follow closely, driven by strong pharmaceutical research capabilities and favorable regulatory environments in countries like Germany, France, and the UK. The Asia-Pacific region is projected to experience the fastest growth, fueled by increasing healthcare investments, rising cancer incidence, and improving access to advanced therapies in countries like China, Japan, and South Korea. Emerging markets in Latin America and the Middle East & Africa are also expected to contribute to global market growth, albeit at a slower pace, due to improving healthcare infrastructure and growing awareness of targeted cancer therapies. The regional distribution of the ADC market reflects the global nature of cancer treatment advancements and the varying stages of healthcare development across different parts of the world.

Regional Analysis of the Antibody Drug Conjugates Market - Detailed regional market performance

The ADC market exhibits distinct characteristics across different regions, influenced by factors such as healthcare infrastructure, regulatory environments, and cancer prevalence. In North America, the market is characterized by rapid adoption of novel therapies, strong research and development capabilities, and a favorable reimbursement landscape. The region benefits from a high concentration of leading pharmaceutical companies and research institutions, driving innovation in ADC development. Europe's market is marked by a balanced approach to innovation and cost containment, with countries like Germany and the UK leading in clinical research and drug approvals. The region's strong academic-industrial partnerships contribute to the advancement of ADC technologies. In the Asia-Pacific region, the market is experiencing rapid growth, particularly in China and Japan, driven by increasing healthcare investments, rising cancer incidence, and government initiatives to promote biotechnology innovation. However, the region also faces challenges related to pricing pressures and varying regulatory standards across countries. Emerging markets in Latin America and the Middle East & Africa are gradually adopting ADCs, with growth driven by improving healthcare infrastructure and increasing awareness of targeted therapies. These regions present significant opportunities for market expansion, albeit with challenges related to affordability and access to advanced treatments.

Leading Company Profiles in the Antibody Drug Conjugates Market - Industry players and strategies

The ADC market is dominated by a mix of large pharmaceutical companies and specialized biotechnology firms, each employing distinct strategies to capture market share. Roche, through its Genentech subsidiary, has been a pioneer in the ADC space with products like Kadcyla, leveraging its strong research capabilities and global presence. AstraZeneca has made significant strides through strategic acquisitions and internal development, focusing on expanding its ADC pipeline across multiple cancer types. ADC Therapeutics, a specialized ADC company, has gained attention for its innovative camptothecin-based ADCs, demonstrating the potential for niche players to compete in the market. Johnson & Johnson, through its Janssen subsidiary, has leveraged its oncology expertise to develop and commercialize ADCs, often through partnerships with smaller biotech firms. These companies, along with others like Pfizer, Merck, and GSK, are pursuing various strategies including internal R&D, strategic acquisitions, and licensing agreements to strengthen their ADC portfolios. The competitive landscape is characterized by a race to develop next-generation ADCs with improved efficacy and safety profiles, as well as efforts to expand into new therapeutic areas and geographic markets.

Porter's Five Forces Analysis of the Antibody Drug Conjugates Market - Competitive forces assessment

The ADC market is characterized by a complex interplay of competitive forces as analyzed through Porter's Five Forces framework. The threat of new entrants is moderate, as the high costs of R&D and regulatory requirements create significant barriers to entry. However, the potential for high returns continues to attract new players, particularly in niche areas of ADC technology. The bargaining power of buyers, primarily healthcare providers and payers, is increasing due to the high cost of ADC therapies, leading to pressure on pricing and reimbursement. The bargaining power of suppliers, including contract manufacturing organizations and suppliers of critical raw materials, is relatively low due to the availability of multiple suppliers and the ability of large pharmaceutical companies to integrate vertically. The threat of substitutes is moderate, as alternative cancer treatments like immunotherapy and small molecule inhibitors continue to evolve, but the unique mechanism of action of ADCs provides a competitive advantage. Competitive rivalry within the market is intense, driven by the race to develop superior ADC technologies, expand into new therapeutic areas, and secure market share in existing segments. This rivalry is characterized by rapid innovation, strategic partnerships, and patent disputes, creating a dynamic and challenging market environment.

SWOT Analysis of the Antibody Drug Conjugates Market - Strengths, weaknesses, opportunities, threats

The ADC market exhibits distinct strengths, weaknesses, opportunities, and threats that shape its competitive landscape. Strengths include the highly targeted nature of ADCs, which offers improved efficacy and reduced side effects compared to traditional chemotherapies, and the growing body of clinical evidence supporting their use across multiple cancer types. The market also benefits from strong R&D capabilities among leading pharmaceutical companies and a robust pipeline of novel ADCs. However, weaknesses such as the high cost of ADC development and manufacturing, complex regulatory pathways, and potential for resistance mechanisms pose challenges to market growth. Opportunities exist in expanding ADC applications to new cancer types, developing next-generation ADCs with improved efficacy, and exploring ADC combinations with other treatment modalities. The market also has potential for growth in emerging markets as healthcare infrastructure improves. Threats include increasing pricing pressures from payers, potential safety concerns that could impact market acceptance, and the rapid evolution of competing technologies in cancer treatment. Additionally, the market faces challenges related to patent expirations and the need for continuous innovation to maintain competitive advantage.

Antibody Drug Conjugates Market Value Chain Analysis - Industry structure and value flow

The ADC value chain is a complex ecosystem involving multiple stakeholders and processes, from initial research to patient treatment. The chain begins with academic and industrial research institutions that conduct basic research on antibody engineering and linker technologies. This is followed by the discovery and development phase, where pharmaceutical companies and biotech firms design and optimize ADC candidates. The manufacturing stage involves specialized contract manufacturing organizations (CMOs) that produce the complex ADC molecules, requiring expertise in both biologics and small molecule drug production. Quality control and regulatory affairs play crucial roles in ensuring product safety and compliance with global standards. The distribution phase involves a network of wholesalers, specialty pharmacies, and hospital pharmacies that deliver ADCs to healthcare providers. Healthcare providers, including oncologists and specialized cancer treatment centers, administer ADCs to patients and monitor treatment outcomes. Throughout this value chain, various support services such as clinical research organizations, regulatory consultants, and market access specialists play important roles in facilitating the development and commercialization of ADCs. The value chain is characterized by high levels of integration and collaboration among stakeholders, driven by the complex nature of ADC development and the need for specialized expertise at each stage.

Key Investment Insights in the Antibody Drug Conjugates Market - Strategic investment recommendations

The ADC market presents compelling investment opportunities driven by its strong growth trajectory and potential for innovation. Strategic investments should focus on companies with robust ADC pipelines, particularly those targeting high-prevalence cancers or developing novel linker technologies. Investors should consider opportunities in both large pharmaceutical companies with established ADC portfolios and specialized biotech firms with innovative approaches to ADC design. The market also offers potential in contract development and manufacturing organizations (CDMOs) that provide critical services in ADC production, as the outsourcing of ADC manufacturing is expected to increase with growing demand. Additionally, investments in companies developing companion diagnostics for ADC patient selection could yield significant returns as personalized medicine becomes more prevalent in cancer treatment. Strategic partnerships and licensing agreements in the ADC space represent another avenue for investment, allowing for exposure to multiple ADC candidates while mitigating individual development risks. However, investors should be aware of the high costs and long development timelines associated with ADC therapies, as well as the potential for regulatory and clinical setbacks. A diversified investment strategy across different segments of the ADC value chain may provide the best balance of risk and return in this dynamic market.

Antibody Drug Conjugates Market Conclusion - Summary and key takeaways

The Antibody Drug Conjugates market is poised for significant growth, with the market size expected to increase from 11.83 Billion in 2026 to 43.34 Billion by 2033, representing a robust CAGR of 20.38%. This growth is driven by the increasing demand for targeted cancer therapies, advancements in ADC technologies, and the expanding pipeline of novel ADCs across various cancer types. The market is characterized by diverse segmentation across targets, technologies, applications, and distribution channels, with HER2-targeted ADCs and cleavable linker technologies currently dominating the market. Blood cancer remains the largest application segment, while retail pharmacies are the primary distribution channel. The competitive landscape is dynamic, with both established pharmaceutical giants and specialized biotech firms vying for market share through innovation and strategic partnerships. Despite challenges related to development costs and regulatory complexities, the market presents significant opportunities for growth, particularly in emerging markets and through the development of next-generation ADCs. The future of the ADC market will likely be shaped by continued technological advancements, expanding therapeutic applications, and the potential for combination therapies with other treatment modalities.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology that combines both primary and secondary research approaches. Secondary research involved extensive analysis of existing market reports, scientific publications, company annual reports, and regulatory databases to gather information on market trends, competitive landscape, and technological developments in the ADC sector. Primary research was conducted through interviews with industry experts, including pharmaceutical executives, oncologists, and market analysts, to validate findings and gain insights into market dynamics. The research also utilized data triangulation techniques to cross-verify information from multiple sources, ensuring the accuracy and reliability of the market projections. Market size calculations were based on a combination of top-down and bottom-up approaches, considering factors such as cancer prevalence, treatment adoption rates, and pricing trends. The forecast methodology incorporated an analysis of historical market data, current market trends, and future growth drivers to project market performance over the 2025-2032 period. This comprehensive approach ensures a robust and reliable assessment of the ADC market, providing stakeholders with valuable insights for strategic decision-making.

Research Scope - Coverage and limitations

This research report provides a comprehensive analysis of the global Antibody Drug Conjugates market, covering key aspects such as market overview, growth drivers and restraints, competitive landscape, and regional analysis. The scope of the research encompasses the period from 2025 to 2032, with a focus on market size, share, and growth trends. The report segments the market by target, technology, application, and distribution channel, providing detailed insights into each segment's performance and potential. However, it's important to note certain limitations in the research scope. Due to the rapidly evolving nature of the ADC market, some emerging technologies or recent developments may not be fully captured in this report. Additionally, while the research provides a global perspective, the depth of regional analysis may vary due to data availability and market maturity in different regions. The report also focuses primarily on commercial aspects of the ADC market and may not extensively cover academic or early-stage research developments. Despite these limitations, the research aims to provide a comprehensive and balanced view of the ADC market, serving as a valuable resource for industry stakeholders and investors.

Key Companies and Recent Developments in the Antibody Drug Conjugates Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The ADC market is characterized by the presence of several key players, each contributing to the market's growth through innovative products and strategic initiatives. Roche, through its Genentech subsidiary, continues to be a leader in the ADC space with its established product portfolio and robust pipeline. The company recently announced advancements in its HER2-targeted ADC program, aiming to expand its applications in both breast and gastric cancers. AstraZeneca has been actively expanding its ADC capabilities through strategic acquisitions and internal development, with recent announcements focusing on novel linker technologies and combination therapies. ADC Therapeutics, a specialized ADC company, has gained attention for its camptothecin-based ADCs, with recent developments including positive clinical trial results for its lead candidate in relapsed/refractory diffuse large B-cell lymphoma. Johnson & Johnson, through its Janssen Pharmaceutical Companies, has been strengthening its ADC portfolio through partnerships and internal research, with recent announcements highlighting progress in solid tumor indications. Other notable companies such as Pfizer, Merck, and GSK are also making significant strides in the ADC market, with recent developments including new product launches, expanded indications for existing ADCs, and strategic collaborations to enhance their technological capabilities. These companies are collectively driving innovation in the ADC space through a combination of novel drug design, advanced manufacturing techniques, and strategic partnerships aimed at expanding the therapeutic potential of ADCs across a broader range of cancer types.