Automotive Lidar Market Overview - Definition, scope, and significance

Automotive Lidar (Light Detection and Ranging) refers to a remote sensing technology that uses pulsed laser light to measure distances and create 3D representations of the surrounding environment. In the automotive industry, Lidar systems are crucial components for advanced driver assistance systems (ADAS) and autonomous vehicles, providing high-resolution spatial mapping and object detection capabilities. The technology operates by emitting laser pulses and measuring the time it takes for the reflected light to return, enabling vehicles to perceive their surroundings with exceptional accuracy. Lidar's significance in the automotive sector stems from its ability to enhance vehicle safety, enable autonomous driving functionalities, and improve overall transportation efficiency. As the automotive industry continues its transition toward electrification and automation, Lidar technology has become increasingly vital for enabling next-generation mobility solutions.

Automotive Lidar Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers propelling the Automotive Lidar Market include the rapid advancement of autonomous vehicle technologies, increasing government regulations mandating advanced safety features, and growing consumer demand for enhanced vehicle safety systems. The push toward fully autonomous vehicles by major automotive manufacturers and technology companies has created substantial demand for high-performance Lidar systems. However, the market faces several restraints, including the high cost of Lidar components, technical challenges related to sensor fusion and environmental adaptability, and concerns about system reliability in adverse weather conditions. Key challenges include achieving the necessary performance standards for mass-market adoption, reducing production costs to make the technology economically viable, and addressing regulatory uncertainties surrounding autonomous vehicle deployment. Despite these obstacles, significant opportunities exist in emerging markets, the development of solid-state Lidar technology, and potential applications beyond automotive, such as in smart infrastructure and fleet management systems.

Automotive Lidar Market Growth Trends - Current and emerging trends shaping the market

The Automotive Lidar Market is experiencing several transformative growth trends that are reshaping the industry landscape. One of the most significant trends is the shift toward solid-state Lidar technology, which offers advantages in terms of size, cost, and reliability compared to traditional mechanical systems. Another emerging trend is the development of multi-functional Lidar systems that integrate additional capabilities such as gesture recognition and interior monitoring. The market is also witnessing increased collaboration between automotive manufacturers and Lidar technology providers to develop customized solutions tailored to specific vehicle platforms. Additionally, there is a growing trend toward the miniaturization of Lidar components, enabling their integration into various vehicle designs without compromising aesthetics. The emergence of 4D Lidar technology, which adds velocity dimension to traditional 3D spatial data, represents another significant advancement. Furthermore, the market is seeing increased investment in software development for Lidar data processing and artificial intelligence algorithms to enhance object recognition and decision-making capabilities.

COVID-19 Impact on the Automotive Lidar Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a mixed impact on the Automotive Lidar Market, initially causing disruptions in the supply chain and delaying product launches and testing programs. The temporary shutdown of automotive manufacturing facilities and reduced consumer spending on vehicles led to a short-term decline in market growth. However, the pandemic also accelerated certain trends that benefited the Lidar market, such as increased focus on autonomous delivery vehicles and last-mile logistics solutions. The recovery trajectory has been characterized by a gradual resumption of automotive production, increased investment in autonomous vehicle technologies as part of economic recovery initiatives, and growing recognition of the importance of advanced safety systems. The market has shown resilience through strategic adaptations, including increased emphasis on remote testing and validation, digital collaboration tools for development processes, and accelerated efforts to reduce component costs to address economic uncertainties.

Automotive Lidar Market Competitive Landscape - Major competitors and market consolidation

The Automotive Lidar Market features a dynamic competitive landscape with a mix of established automotive suppliers, specialized Lidar technology companies, and technology giants entering the space. The market is characterized by intense competition and rapid technological advancements, with companies focusing on developing differentiated solutions to gain market share. Continental AG and Delphi Automotive represent the traditional automotive supplier segment, leveraging their extensive industry experience and manufacturing capabilities. Specialized companies like Innoviz Technologies, Quanergy Systems, and Velodyne LiDAR are driving innovation with their focused expertise in Lidar technology development. The competitive landscape is also witnessing increased consolidation through mergers, acquisitions, and strategic partnerships as companies seek to combine complementary technologies and expand their market presence. This consolidation trend is expected to continue as the market matures, with larger players acquiring innovative startups to enhance their technological capabilities and market reach.

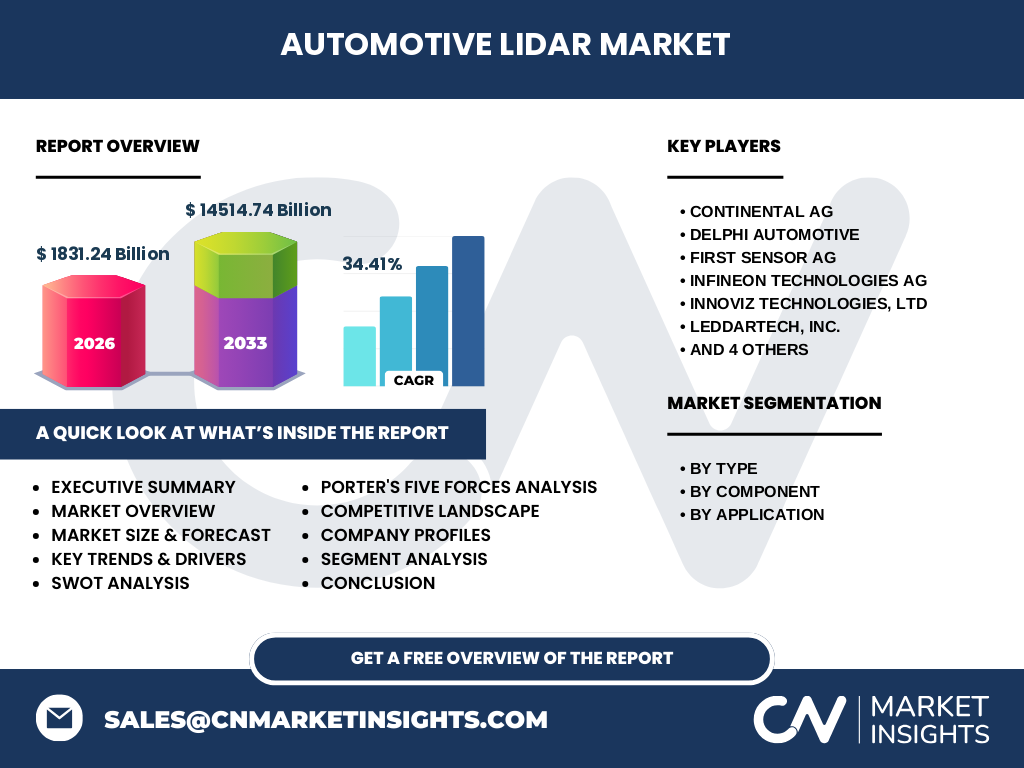

Executive Summary - High-level overview and key findings about Automotive Lidar Market

The Automotive Lidar Market is experiencing unprecedented growth driven by the automotive industry's transition toward autonomous driving and advanced safety systems. With a market size of 1831.24 billion in 2026 and projected to reach 14514.74 billion by 2033, representing a remarkable CAGR of 34.41%, the market presents significant opportunities for stakeholders. The technology's evolution from mechanical to solid-state systems, coupled with decreasing costs and improving performance, is accelerating adoption across various vehicle segments. Key findings indicate that the market is being shaped by technological advancements, regulatory support for vehicle safety, and increasing consumer awareness of autonomous driving benefits. The competitive landscape remains dynamic with both established players and innovative startups contributing to market growth. The market's future trajectory is strongly aligned with the broader automotive industry's transformation toward electrification and automation, with Lidar technology playing a crucial role in enabling safe and reliable autonomous mobility solutions.

Automotive Lidar Market Forecast - Projections for 2025-2032 period

The Automotive Lidar Market forecast for the 2025-2032 period indicates sustained robust growth, building upon the strong foundation established in recent years. The market is expected to continue its impressive expansion trajectory, driven by increasing penetration of advanced driver assistance systems (ADAS) and the gradual commercialization of autonomous vehicles. The forecast period will likely witness significant technological advancements, including improvements in range, resolution, and reliability of Lidar systems, as well as continued cost reductions through economies of scale and manufacturing innovations. Market growth will be particularly strong in regions with supportive regulatory frameworks and high levels of automotive production, such as North America, Europe, and Asia-Pacific. The forecast also suggests increasing adoption of Lidar technology across different vehicle segments, moving beyond premium vehicles to more mainstream models as costs decrease and performance improves. Additionally, the development of new applications and use cases for Lidar technology in automotive contexts is expected to further drive market expansion during this period.

Automotive Lidar Market Size and Share by Segmentation - Breakdown by {segmentData}

The Automotive Lidar Market segmentation reveals distinct patterns in technology adoption and application across different market segments. In terms of type, solid-state Lidar technology is gaining significant market share due to its advantages in terms of size, cost, and reliability compared to traditional mechanical systems. Flash Lidar, while currently representing a smaller segment, is showing promising growth potential due to its ability to capture entire scenes instantaneously. By component, the market is segmented into photodetectors, lasers, integrated circuits, and optical elements, with integrated circuits expected to see substantial growth due to increasing demand for sophisticated signal processing capabilities. The application segment analysis shows that autonomous shuttles and robotaxis are emerging as significant growth areas, driven by commercial deployment initiatives, while passenger cars continue to represent the largest market segment in terms of volume. This segmentation analysis provides valuable insights into the diverse applications and technological approaches within the Automotive Lidar Market, highlighting the varying growth rates and adoption patterns across different segments.

Global Automotive Lidar Market Size and Share by Region - Geographic distribution

The global Automotive Lidar Market exhibits distinct regional variations in terms of market size and share, reflecting differences in automotive production, technological adoption rates, and regulatory environments across different geographies. Asia-Pacific currently represents the largest regional market, driven by the presence of major automotive manufacturing hubs in countries like China, Japan, and South Korea, as well as strong government support for autonomous vehicle development. North America follows as the second-largest market, characterized by significant investment in autonomous vehicle technologies and a robust ecosystem of automotive and technology companies. Europe maintains a strong position in the market, supported by stringent vehicle safety regulations and the presence of leading automotive manufacturers. The regional distribution of the market is also influenced by factors such as infrastructure development, consumer preferences for advanced vehicle technologies, and the pace of regulatory approvals for autonomous vehicles. Emerging markets in regions such as Latin America and the Middle East & Africa are showing increasing potential as automotive industries in these regions continue to develop and adopt advanced technologies.

Regional Analysis of the Automotive Lidar Market - Detailed regional market performance

The regional analysis of the Automotive Lidar Market reveals distinct performance characteristics and growth patterns across different geographical areas. In North America, the market is characterized by strong technological innovation, significant investment in autonomous vehicle development, and a supportive regulatory environment for advanced automotive technologies. The region benefits from the presence of major technology companies and automotive manufacturers actively involved in Lidar development and deployment. Europe's market performance is driven by stringent vehicle safety regulations, strong automotive manufacturing capabilities, and increasing focus on autonomous public transportation solutions. The region is also witnessing growing collaboration between automotive companies and technology providers to develop next-generation Lidar systems. Asia-Pacific demonstrates the fastest growth rate, fueled by rapid automotive production expansion, government initiatives supporting autonomous vehicle technologies, and increasing consumer demand for advanced safety features. China, in particular, is emerging as a significant player in both Lidar technology development and automotive production. The regional analysis also highlights varying levels of infrastructure readiness, consumer acceptance, and regulatory frameworks that influence the adoption and deployment of Lidar technology across different markets.

Leading Company Profiles in the Automotive Lidar Market - Industry players and strategies

The Automotive Lidar Market features several leading companies with distinct strategic approaches and technological capabilities. Continental AG has established itself as a key player through its comprehensive automotive electronics portfolio and strong relationships with major vehicle manufacturers. The company's strategy focuses on integrating Lidar technology with its existing sensor and control systems to provide complete autonomous driving solutions. Delphi Automotive has positioned itself as an innovator in advanced driver assistance systems, leveraging its engineering expertise to develop sophisticated Lidar solutions for various vehicle platforms. First Sensor AG specializes in high-performance optical sensors, bringing critical component expertise to the Lidar market. Infineon Technologies AG contributes its semiconductor technology capabilities to enable more efficient and cost-effective Lidar systems. Innoviz Technologies has gained attention for its solid-state Lidar solutions, targeting mass-market adoption through cost reduction and performance optimization. Quanergy Systems focuses on developing scalable Lidar solutions with an emphasis on software integration and data processing capabilities. Texas Instruments leverages its semiconductor expertise to provide critical components for Lidar systems. Velodyne LiDAR remains a pioneer in the industry, known for its high-performance mechanical Lidar systems and continued innovation in the field. ZF Friedrichshafen AG combines its automotive manufacturing experience with advanced sensing technologies to develop integrated Lidar solutions for various vehicle applications.

Porter's Five Forces Analysis of the Automotive Lidar Market - Competitive forces assessment

The Automotive Lidar Market's competitive dynamics can be analyzed through Porter's Five Forces framework, revealing insights into the industry's attractiveness and profitability potential. The threat of new entrants remains moderate due to high technological barriers, significant capital requirements, and the need for extensive automotive industry experience. However, the market continues to attract new players due to its growth potential and technological opportunities. The bargaining power of suppliers is relatively high, given the specialized nature of Lidar components and the limited number of suppliers capable of meeting automotive-grade quality standards. Conversely, the bargaining power of buyers (automotive manufacturers) is also significant, as they often have multiple technology options and can influence pricing and development priorities. The threat of substitute technologies, such as camera-based systems and radar, exists but is mitigated by Lidar's unique capabilities in terms of accuracy and reliability. Competitive rivalry within the market is intense, characterized by rapid technological advancements, price competition, and the race to achieve mass-market adoption. This analysis suggests that while the market offers substantial growth opportunities, companies must navigate complex competitive dynamics to achieve sustainable success.

SWOT Analysis of the Automotive Lidar Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Automotive Lidar Market reveals key factors influencing its development and potential. The market's strengths include the technology's proven effectiveness in enhancing vehicle safety and enabling autonomous driving, strong support from major automotive manufacturers, and continuous technological advancements improving performance and reducing costs. However, weaknesses such as high initial costs, technical challenges in adverse weather conditions, and integration complexities with existing vehicle systems present obstacles to widespread adoption. Significant opportunities exist in emerging markets, the development of solid-state Lidar technology, and potential applications beyond traditional automotive use cases. The market also faces threats from alternative sensing technologies, regulatory uncertainties surrounding autonomous vehicle deployment, and potential economic downturns affecting automotive sales. This SWOT analysis highlights the market's dynamic nature and the need for companies to leverage strengths, address weaknesses, capitalize on opportunities, and mitigate threats to succeed in this rapidly evolving industry.

Automotive Lidar Market Value Chain Analysis - Industry structure and value flow

The Automotive Lidar Market value chain encompasses a complex network of activities and participants, each contributing to the development and deployment of Lidar technology in vehicles. The chain begins with raw material suppliers providing essential components such as semiconductors, optical elements, and mechanical parts. These materials flow to component manufacturers who produce specialized Lidar elements including lasers, photodetectors, and integrated circuits. System integrators then combine these components into functional Lidar units, incorporating software for data processing and system control. Automotive manufacturers serve as the primary customers, integrating Lidar systems into vehicle platforms and often working closely with suppliers to optimize designs for specific applications. The value chain also includes testing and validation services, regulatory compliance support, and aftermarket services. Throughout this chain, various intermediaries such as distributors and technology partners facilitate the flow of products and information. Understanding this value chain structure is crucial for identifying key opportunities for value creation, potential bottlenecks, and strategic partnership opportunities within the Automotive Lidar Market.

Key Investment Insights in the Automotive Lidar Market - Strategic investment recommendations

The Automotive Lidar Market presents compelling investment opportunities driven by the technology's critical role in advancing autonomous driving capabilities and vehicle safety systems. Strategic investment insights suggest focusing on companies developing solid-state Lidar technology, which offers significant potential for cost reduction and mass-market adoption. Investments in software development for Lidar data processing and artificial intelligence integration represent another promising area, as these capabilities become increasingly important for system performance. The market also offers opportunities in companies working on multi-functional Lidar systems that combine traditional sensing capabilities with additional features such as gesture recognition or interior monitoring. Strategic partnerships between Lidar technology providers and automotive manufacturers represent a key investment consideration, as these collaborations often lead to innovative solutions and accelerated market adoption. Additionally, investments in companies with strong intellectual property portfolios and those demonstrating successful cost reduction strategies are likely to yield favorable returns as the market continues to mature and expand.

Automotive Lidar Market Conclusion - Summary and key takeaways

The Automotive Lidar Market represents a dynamic and rapidly evolving sector at the forefront of automotive technology innovation. With a projected market size growing from 1831.24 billion in 2026 to 14514.74 billion by 2033 at a CAGR of 34.41%, the market demonstrates exceptional growth potential driven by the automotive industry's transition toward autonomous driving and advanced safety systems. Key takeaways include the technology's critical role in enabling next-generation vehicle capabilities, the ongoing shift toward solid-state solutions, and the importance of software integration in maximizing system performance. The market's future will be shaped by continued technological advancements, cost reduction efforts, and the successful commercialization of autonomous vehicle applications. As the industry matures, companies that can effectively navigate the complex competitive landscape, address technical challenges, and capitalize on emerging opportunities are likely to emerge as leaders in this transformative market.

Research Methodology - How this research was conducted

The research methodology employed for this Automotive Lidar Market analysis combines multiple approaches to ensure comprehensive and accurate insights. Primary research involved interviews with industry experts, automotive manufacturers, and technology providers to gather firsthand information about market trends, technological developments, and competitive dynamics. Secondary research encompassed extensive review of industry reports, company publications, technical papers, and market data to build a robust understanding of the market landscape. Data triangulation techniques were applied to validate findings across multiple sources, ensuring reliability and accuracy. The analysis also incorporated patent analysis to identify technological trends and innovation patterns within the industry. Market size and forecast calculations were based on both top-down and bottom-up approaches, considering factors such as vehicle production volumes, technology adoption rates, and pricing trends. This rigorous methodology ensures that the research findings provide valuable and actionable insights for stakeholders in the Automotive Lidar Market.

Research Scope - Coverage and limitations

The research scope for this Automotive Lidar Market analysis encompasses a comprehensive examination of the global market, including technology trends, competitive landscape, regional variations, and future growth projections. The analysis covers key market segments such as solid-state and flash Lidar technologies, various component types, and major application areas including autonomous shuttles, robotaxis, and passenger vehicles. The research also examines the roles of major industry players and their strategic approaches to market development. However, certain limitations exist within the research scope, including the rapid pace of technological change which may affect the relevance of some findings over time, potential variations in market data availability across different regions, and the inherent challenges in forecasting highly dynamic technology markets. Additionally, the analysis focuses primarily on automotive applications, with limited coverage of potential non-automotive uses of Lidar technology. Despite these limitations, the research provides a thorough and current assessment of the Automotive Lidar Market, offering valuable insights for industry stakeholders.

Key Companies and Recent Developments in the Automotive Lidar Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Automotive Lidar Market features several key companies driving innovation and market development through strategic initiatives and technological advancements. Continental AG recently announced expanded partnerships with automotive manufacturers to integrate its advanced Lidar systems into next-generation vehicle platforms, focusing on enhanced safety and autonomous driving capabilities. Delphi Automotive has introduced new solid-state Lidar solutions designed for mass-market adoption, emphasizing cost reduction and improved performance. First Sensor AG unveiled advanced photodetector technologies that significantly enhance Lidar system sensitivity and range. Infineon Technologies AG launched new integrated circuit solutions specifically optimized for automotive Lidar applications, enabling more compact and energy-efficient systems. Innoviz Technologies announced successful completion of production validation for its latest solid-state Lidar, marking a significant milestone toward commercial deployment. Quanergy Systems introduced a new generation of 4D Lidar technology, adding velocity dimension to traditional 3D spatial data for improved object tracking. Texas Instruments released a comprehensive Lidar development kit to accelerate innovation in the automotive sector. Velodyne LiDAR unveiled its next-generation mechanical Lidar system with enhanced range and resolution capabilities. ZF Friedrichshafen AG announced strategic partnerships with technology companies to develop integrated sensing solutions combining Lidar with other automotive sensors. These developments reflect the dynamic nature of the market and the ongoing efforts by key players to advance Lidar technology for automotive applications.