Video Surveillance Market Overview - Definition, scope, and significance

The Video Surveillance Market encompasses the comprehensive ecosystem of technologies, services, and solutions designed to monitor, record, and analyze visual data for security, safety, and operational intelligence purposes. This market includes hardware components such as cameras, recorders, and storage devices, alongside software platforms for video management, analytics, and integration with other security systems. The significance of this market has grown exponentially as organizations across sectors recognize the critical role of visual monitoring in protecting assets, ensuring public safety, and optimizing operational efficiency. From traditional analog systems to modern IP-based networks and AI-powered analytics, video surveillance has evolved into a sophisticated technology platform that serves diverse applications ranging from commercial security and public safety to retail analytics and industrial monitoring. The market's scope extends beyond mere recording capabilities to include advanced features such as facial recognition, behavioral analysis, and real-time alerting systems, making it an integral component of modern security infrastructure and smart city initiatives worldwide.

Video Surveillance Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Video Surveillance Market is propelled by several key drivers including increasing security concerns across commercial and public spaces, rapid urbanization leading to smart city initiatives, and technological advancements in camera resolution and analytics capabilities. The growing adoption of Internet of Things (IoT) technologies and cloud-based surveillance solutions has further accelerated market growth by enabling remote monitoring and centralized management. However, the market faces significant restraints such as high installation and maintenance costs, privacy concerns and regulatory compliance requirements, and the complexity of integrating legacy systems with modern solutions. Major challenges include cybersecurity threats to surveillance networks, the need for skilled personnel to manage sophisticated systems, and the rapid pace of technological obsolescence. Despite these challenges, substantial opportunities exist in emerging markets, the integration of artificial intelligence and machine learning for advanced analytics, the expansion of video surveillance in non-traditional sectors such as healthcare and education, and the development of edge computing solutions that reduce latency and bandwidth requirements. The market also benefits from increasing government initiatives to enhance public safety infrastructure and the growing demand for video surveillance as a service (VSaaS) models that offer cost-effective deployment options for small and medium enterprises.

Video Surveillance Market Growth Trends - Current and emerging trends shaping the market

The Video Surveillance Market is experiencing transformative growth trends driven by technological innovation and changing security requirements. One of the most significant trends is the shift from traditional analog systems to IP-based and network video recorders (NVRs), which offer higher resolution, remote accessibility, and advanced analytics capabilities. The integration of artificial intelligence and deep learning algorithms is revolutionizing the market by enabling features such as facial recognition, object detection, and predictive analytics that go beyond simple recording to provide actionable insights. Cloud-based surveillance solutions are gaining substantial traction, offering scalability, reduced infrastructure costs, and enhanced data accessibility. The market is also witnessing increased adoption of 4K and 8K resolution cameras, providing unprecedented image clarity for critical applications. Mobile surveillance solutions are emerging as a key trend, particularly in temporary installations and rapid deployment scenarios. Additionally, the convergence of video surveillance with other security systems such as access control and alarm systems is creating integrated security platforms that offer comprehensive protection. The rise of thermal imaging cameras for perimeter security and the development of wireless surveillance solutions for challenging installation environments represent further growth trends that are reshaping the market landscape and expanding application possibilities across various industries.

COVID-19 Impact on the Video Surveillance Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has had a profound impact on the Video Surveillance Market, creating both challenges and opportunities that have reshaped market dynamics. During the initial outbreak phases, the market experienced supply chain disruptions, delayed projects, and reduced capital expenditures as organizations prioritized immediate operational needs over security investments. However, the pandemic simultaneously accelerated the adoption of video surveillance solutions for health and safety monitoring, including social distancing compliance, occupancy management, and thermal screening applications. Organizations rapidly deployed video analytics to monitor mask compliance and crowd density, creating new revenue streams for surveillance providers. The shift to remote work and the need for distributed monitoring capabilities drove increased demand for cloud-based surveillance solutions and mobile access platforms. As businesses adapted to new operational models, video surveillance became essential for maintaining security across multiple locations and ensuring business continuity. The recovery trajectory has been characterized by pent-up demand for deferred projects, increased focus on health and safety applications, and accelerated digital transformation initiatives. The pandemic has fundamentally changed perceptions of video surveillance, expanding its role from traditional security applications to include health monitoring and operational intelligence, thereby creating a more resilient and diversified market with sustained growth potential beyond the immediate crisis period.

Video Surveillance Market Competitive Landscape - Major competitors and market consolidation

The Video Surveillance Market features a dynamic competitive landscape characterized by the presence of established technology giants, specialized security companies, and emerging players offering innovative solutions. Major competitors such as Axis Communications, Dahua Technologies, and Bosch Security Systems dominate the market with comprehensive product portfolios and extensive global distribution networks. The competitive environment is marked by continuous innovation, with companies investing heavily in research and development to enhance camera resolution, analytics capabilities, and integration features. Market consolidation is evident through strategic acquisitions, partnerships, and collaborations as companies seek to expand their technological capabilities and geographic presence. The landscape includes a mix of vertically integrated companies offering end-to-end solutions and specialized providers focusing on specific market segments or technologies. Competition is particularly intense in the IP camera segment, where manufacturers compete on resolution, low-light performance, and intelligent analytics features. The market also features strong competition in the software segment, with video management system providers differentiating themselves through user interface design, scalability, and integration capabilities with third-party systems. Emerging competitors from Asia-Pacific regions are challenging established players with cost-competitive solutions, while traditional security companies are expanding their offerings to include advanced analytics and cloud-based services, creating a multi-faceted competitive environment that drives continuous innovation and market evolution.

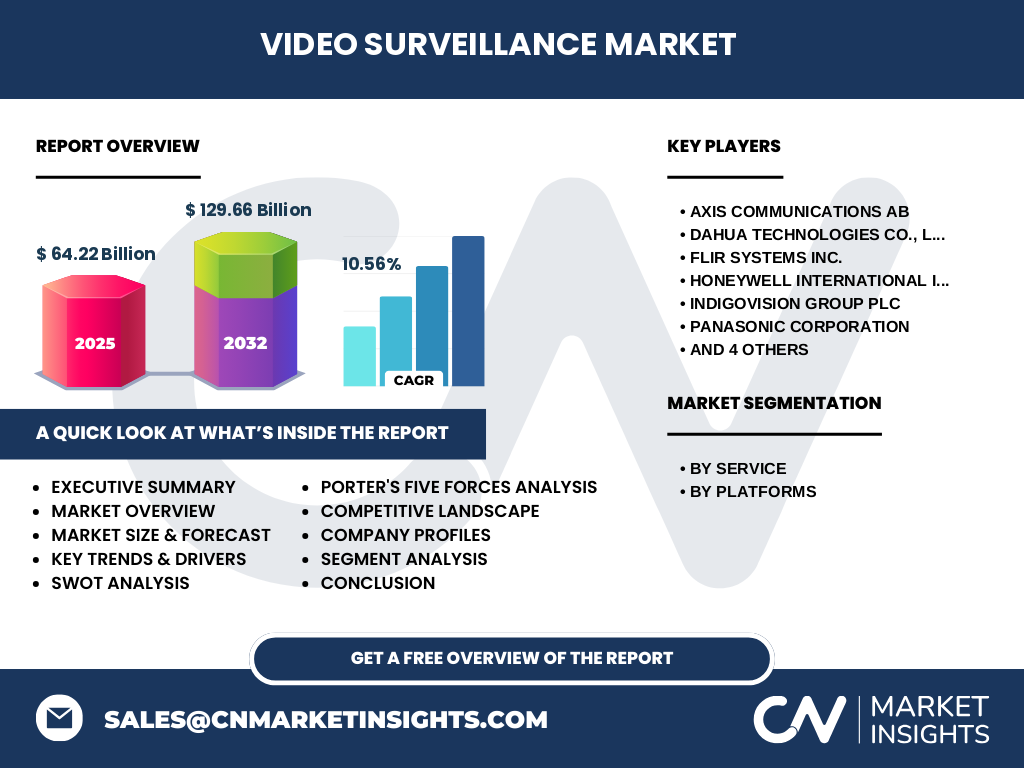

Executive Summary - High-level overview and key findings about Video Surveillance Market

The Video Surveillance Market represents a dynamic and rapidly evolving industry poised for substantial growth, with market projections indicating expansion from $64.22 billion in 2025 to $129.66 billion by 2032, representing a robust compound annual growth rate of 10.56%. This growth is driven by increasing security concerns, technological advancements, and the expanding scope of video surveillance applications beyond traditional security to include operational intelligence and health monitoring. The market is characterized by a shift toward IP-based systems, cloud solutions, and AI-powered analytics that are transforming surveillance from passive recording to active intelligence gathering. Key segments include hosted, managed, and hybrid service models, alongside hardware and software platforms that cater to diverse customer needs across commercial, residential, and government sectors. The competitive landscape features established players and innovative newcomers competing on technological capabilities, integration features, and cost-effectiveness. Regional analysis reveals varying adoption rates and growth opportunities, with developed markets focusing on advanced analytics and emerging markets prioritizing basic security infrastructure. The COVID-19 pandemic has accelerated digital transformation in the sector, creating new applications while highlighting the critical role of video surveillance in modern security and operational management strategies. Overall, the market demonstrates strong fundamentals with multiple growth drivers, technological innovation, and expanding application areas that position it for sustained long-term growth.

Video Surveillance Market Forecast - Projections for 2025-2032 period

The Video Surveillance Market is projected to experience significant growth over the 2025-2032 period, with comprehensive market analysis indicating expansion from $64.22 billion to $129.66 billion, representing a compound annual growth rate of 10.56%. This robust growth trajectory is underpinned by several key factors including the continued digital transformation of security infrastructure, increasing adoption of cloud-based surveillance solutions, and the integration of artificial intelligence and advanced analytics capabilities. The forecast period will witness accelerated demand across all market segments, with particular emphasis on hosted and managed services that offer cost-effective deployment options for organizations of all sizes. Hardware segment growth will be driven by the transition to higher resolution cameras, thermal imaging solutions, and specialized surveillance equipment for emerging applications. The software segment is expected to experience the highest growth rate as organizations increasingly demand sophisticated video management systems, analytics platforms, and integration capabilities with other security and operational systems. Geographic expansion will be particularly strong in emerging markets where infrastructure development and urbanization are driving security investments, while developed markets will focus on upgrading existing systems with advanced features. The forecast also accounts for the sustained impact of COVID-19 on market dynamics, including the permanent adoption of health and safety monitoring applications and the accelerated shift toward remote surveillance capabilities. Overall, the market demonstrates strong fundamentals with multiple growth drivers ensuring sustained expansion throughout the forecast period.

Video Surveillance Market Size and Share by Segmentation - Breakdown by {segmentData}

The Video Surveillance Market segmentation reveals distinct patterns in market size and share distribution across different service and platform categories. In the service segment, hosted solutions command the largest market share due to their scalability, reduced infrastructure requirements, and appeal to small and medium enterprises seeking cost-effective surveillance options. Managed services represent the second-largest segment, particularly popular among organizations requiring comprehensive security management without internal expertise. The hybrid service model is experiencing the fastest growth rate as organizations seek balanced approaches that combine on-premises control with cloud flexibility. On the platform side, hardware components including cameras, storage devices, and network infrastructure account for the largest revenue share, driven by continuous technological advancements and replacement cycles. However, the software segment is demonstrating the highest growth rate, reflecting the increasing importance of video management systems, analytics platforms, and integration capabilities. Within the hardware segment, IP cameras dominate market share over analog systems, with 4K and higher resolution cameras showing particularly strong growth. The storage segment is evolving rapidly with the transition from traditional DVRs to network video recorders and cloud storage solutions. Analytics software represents a growing sub-segment as artificial intelligence and machine learning capabilities become standard requirements. This segmentation analysis highlights the market's evolution toward more sophisticated, integrated solutions while maintaining strong demand for fundamental hardware components that form the foundation of surveillance infrastructure.

Global Video Surveillance Market Size and Share by Region - Geographic distribution

The global Video Surveillance Market exhibits distinct regional variations in size, growth rates, and adoption patterns, reflecting diverse economic conditions, security priorities, and technological infrastructure across different geographic areas. North America maintains the largest market share, driven by advanced technological infrastructure, high security awareness, and substantial investments in smart city initiatives and commercial security systems. The region benefits from early adoption of IP-based surveillance and advanced analytics solutions, with the United States leading in both market size and technological innovation. Europe represents the second-largest regional market, characterized by stringent data privacy regulations that influence surveillance system design and implementation while driving demand for compliant solutions. The Asia-Pacific region demonstrates the highest growth rate, fueled by rapid urbanization, increasing security concerns, and substantial government investments in public safety infrastructure across countries like China, India, and Southeast Asian nations. This region is also witnessing significant manufacturing capabilities, with many surveillance equipment manufacturers based in China and other Asian countries. The Middle East and Africa region shows strong growth potential, particularly in Gulf Cooperation Council countries investing heavily in smart city projects and security infrastructure. Latin America presents moderate growth opportunities, with increasing adoption in commercial sectors and gradual modernization of existing surveillance systems. Regional variations in market size and share reflect different stages of technological adoption, regulatory environments, and economic development levels, creating diverse opportunities for market participants across the global landscape.

Regional Analysis of the Video Surveillance Market - Detailed regional market performance

Regional analysis of the Video Surveillance Market reveals distinct performance patterns and growth dynamics across different geographic areas, each characterized by unique market drivers, adoption rates, and technological preferences. North America demonstrates mature market conditions with sophisticated demand for advanced analytics, integration capabilities, and cloud-based solutions, driven by high security awareness and substantial commercial sector investments. The region's market performance is bolstered by regulatory requirements, insurance incentives, and the presence of major technology companies that drive innovation and adoption. Europe presents a complex regional landscape where data privacy regulations such as GDPR significantly influence surveillance system design and implementation, creating demand for compliant solutions while potentially limiting certain advanced features like facial recognition. The region shows strong performance in smart city initiatives and critical infrastructure protection, with countries like the UK, Germany, and France leading in surveillance technology adoption. Asia-Pacific emerges as the fastest-growing region, with market performance driven by rapid urbanization, increasing disposable incomes, and substantial government investments in public safety infrastructure. China leads regional growth with massive deployments in both public and private sectors, while India and Southeast Asian countries show accelerating adoption rates. The Middle East demonstrates strong market performance in high-security applications and smart city projects, particularly in Gulf nations with significant infrastructure investments. Latin America shows moderate but steady growth, with market performance influenced by economic conditions and security challenges that drive surveillance adoption in commercial and public sectors. Regional performance analysis highlights the importance of understanding local market conditions, regulatory environments, and specific security requirements when developing market entry and expansion strategies.

Leading Company Profiles in the Video Surveillance Market - Industry players and strategies

The Video Surveillance Market features several leading companies that have established strong market positions through technological innovation, comprehensive product portfolios, and strategic market approaches. Axis Communications AB has maintained its leadership position through continuous innovation in network camera technology and a strong focus on open platform solutions that enable integration with third-party systems. The company's strategy emphasizes high-quality imaging, cybersecurity, and analytics capabilities that address evolving market demands. Dahua Technologies Co., Ltd has emerged as a dominant global player through cost-competitive solutions and extensive manufacturing capabilities, particularly strong in the Asia-Pacific region while expanding its global footprint through strategic partnerships and local presence establishment. FLIR Systems Inc. specializes in thermal imaging and advanced sensing technologies, differentiating itself through superior performance in challenging environmental conditions and specialized applications such as perimeter security and critical infrastructure protection. Honeywell International Inc. leverages its extensive experience in building management and industrial applications to provide integrated security solutions that combine video surveillance with access control, fire systems, and building automation. IndigoVision Group Plc focuses on high-end IP video solutions with emphasis on reliability, scalability, and advanced features for mission-critical applications. Panasonic Corporation brings its extensive electronics expertise to deliver high-quality imaging solutions with strong performance in low-light conditions and challenging environments. Robert Bosch GmbH combines its engineering excellence with comprehensive security solutions that integrate video surveillance with other safety and security systems. Samsung Electronics Co., Ltd offers a broad range of surveillance solutions leveraging its display and semiconductor expertise to deliver high-resolution imaging and advanced analytics capabilities. Schneider Electric provides integrated security solutions that combine video surveillance with energy management and building automation, targeting commercial and industrial applications. Sony Corporation contributes its imaging technology leadership to deliver high-quality cameras with superior image processing and low-light performance. These leading companies employ diverse strategies including technological differentiation, vertical integration, geographic expansion, and strategic partnerships to maintain competitive advantages and address evolving market requirements across different segments and regions.

Porter's Five Forces Analysis of the Video Surveillance Market - Competitive forces assessment

Porter's Five Forces analysis of the Video Surveillance Market reveals a competitive landscape shaped by multiple strategic forces that influence market attractiveness and profitability. The threat of new entrants remains moderate despite technological advancements, as significant capital requirements, established distribution networks, and the need for technical expertise create substantial barriers to entry. However, the market continues to attract new players, particularly from technology sectors and emerging economies, who leverage innovative approaches and cost advantages to gain market share. The bargaining power of buyers is increasing as organizations become more sophisticated in their security requirements and have access to multiple vendor options, particularly in the commercial sector where price competition and feature comparisons are intense. Large enterprise customers and government agencies wield significant bargaining power due to their substantial purchasing volumes and ability to influence product development through specific requirements. The bargaining power of suppliers varies across the value chain, with component suppliers for specialized technologies like image sensors and analytics chips holding moderate power, while suppliers of commoditized components face intense competition. The threat of substitute products is relatively low as video surveillance provides unique capabilities that are difficult to replace, although convergence with other security technologies and the emergence of alternative monitoring solutions create some substitution pressure. Competitive rivalry is intense, characterized by price competition, rapid technological innovation, and the constant need to differentiate through features, quality, and service offerings. The market experiences frequent new product introductions, aggressive marketing strategies, and competitive pricing that impact profit margins. Overall, the five forces analysis indicates a market with moderate to high competitive intensity, where success depends on technological innovation, cost management, customer relationships, and the ability to provide integrated solutions that address evolving security requirements.

SWOT Analysis of the Video Surveillance Market - Strengths, weaknesses, opportunities, threats

A comprehensive SWOT analysis of the Video Surveillance Market reveals critical internal and external factors that shape market dynamics and competitive positioning. The market's strengths include robust technological innovation driving continuous product improvement, strong demand across multiple sectors creating diverse revenue streams, and the essential nature of security solutions that ensures sustained market relevance. Advanced analytics capabilities, integration with other security systems, and the emergence of cloud-based solutions represent significant technological strengths that differentiate modern surveillance from traditional systems. However, the market faces notable weaknesses including high implementation and maintenance costs that can limit adoption in price-sensitive segments, complex integration requirements with existing infrastructure, and concerns about privacy and data security that can create regulatory challenges. The market also struggles with rapid technological obsolescence that requires continuous investment in upgrades and replacements. Significant opportunities exist in emerging markets where infrastructure development and urbanization are driving security investments, the expansion of video surveillance applications into non-traditional sectors such as healthcare and retail analytics, and the growing demand for integrated security solutions that combine multiple functionalities. The increasing adoption of artificial intelligence and machine learning presents substantial opportunities for advanced analytics and predictive capabilities. Threats to market growth include intense price competition that can erode profit margins, cybersecurity vulnerabilities that can compromise system integrity, and evolving regulatory environments that may restrict certain surveillance applications or technologies. Economic uncertainties, supply chain disruptions, and the rapid pace of technological change also pose significant threats that require strategic adaptation and risk management approaches to ensure sustained market success.

Video Surveillance Market Value Chain Analysis - Industry structure and value flow

The Video Surveillance Market value chain encompasses a complex network of activities and participants that collectively deliver comprehensive surveillance solutions to end-users across various sectors. The value chain begins with component suppliers who provide essential elements such as image sensors, processors, storage devices, and network components that form the foundation of surveillance systems. These components flow to original equipment manufacturers who integrate them into cameras, recorders, and other hardware devices, adding value through design, quality control, and performance optimization. System integrators and solution providers represent a critical value chain segment, combining hardware components with software platforms, analytics capabilities, and integration services to deliver complete surveillance solutions tailored to specific customer requirements. Value is added through installation services, system configuration, and the development of customized applications that address unique security challenges. Software developers and platform providers contribute significant value through video management systems, analytics engines, and integration capabilities that transform basic recording functions into intelligent surveillance solutions. Distribution channels including direct sales, value-added resellers, and system integrators facilitate market access and provide essential services such as technical support, training, and maintenance. Managed service providers represent an emerging value chain segment, offering hosted surveillance solutions that reduce customer infrastructure requirements and provide scalable, subscription-based access to advanced surveillance capabilities. End-users across commercial, government, industrial, and residential sectors represent the final value chain stage, where surveillance solutions deliver security, operational intelligence, and compliance benefits that justify the investment. The value chain is characterized by increasing integration and convergence, with traditional boundaries between hardware, software, and services becoming less distinct as comprehensive solutions become the market standard. Value flow is optimized through strategic partnerships, technological innovation, and the development of open platforms that enable seamless integration across different value chain segments.

Key Investment Insights in the Video Surveillance Market - Strategic investment recommendations

The Video Surveillance Market presents compelling investment opportunities characterized by strong growth projections, technological innovation, and expanding application areas that create multiple strategic investment pathways. Investors should prioritize companies demonstrating strong capabilities in artificial intelligence and advanced analytics, as these technologies represent the primary drivers of market differentiation and value creation in modern surveillance solutions. Cloud-based surveillance platforms and software-as-a-service models offer attractive investment opportunities due to their recurring revenue characteristics, scalability, and alignment with digital transformation trends across all sectors. Companies with strong intellectual property portfolios in areas such as video analytics, edge computing, and cybersecurity protection represent particularly valuable investment targets given the increasing importance of these capabilities in competitive differentiation. Geographic expansion strategies, particularly in high-growth emerging markets, present significant investment opportunities as urbanization and infrastructure development drive surveillance adoption. Investors should seek companies with established distribution networks and local market expertise in these regions to maximize growth potential. The integration of video surveillance with other security and operational systems represents a key investment theme, with companies offering comprehensive, integrated solutions positioned for superior market performance. Strategic investments in companies developing specialized surveillance applications for emerging use cases such as health monitoring, retail analytics, and industrial safety can capture high-growth niche markets. Cybersecurity capabilities represent a critical investment consideration given the increasing vulnerability of connected surveillance systems to cyber threats. Companies demonstrating strong cybersecurity expertise and compliance with evolving data protection regulations offer reduced investment risk and sustainable competitive advantages. Overall, successful investment strategies should focus on companies combining technological innovation, market expansion capabilities, and strong operational execution to capitalize on the market's robust growth trajectory and evolving requirements.

Video Surveillance Market Conclusion - Summary and key takeaways

The Video Surveillance Market presents a compelling growth narrative characterized by technological evolution, expanding applications, and robust market fundamentals that position it for sustained long-term success. The market's projected growth from $64.22 billion to $129.66 billion by 2032, representing a 10.56% CAGR, reflects strong underlying demand drivers including increasing security concerns, technological advancements, and the expanding scope of surveillance applications beyond traditional security to include operational intelligence and health monitoring. Key market segments including hosted services, managed solutions, and hybrid models demonstrate diverse growth patterns that cater to different customer needs and preferences, while platform innovations in hardware and software continue to drive market evolution. The competitive landscape features established players and innovative newcomers competing on technological capabilities, integration features, and cost-effectiveness, creating a dynamic environment that fosters continuous innovation. Regional analysis reveals varying adoption rates and growth opportunities, with developed markets focusing on advanced analytics and emerging markets prioritizing basic security infrastructure development. The COVID-19 pandemic has accelerated digital transformation in the sector, creating new applications while highlighting the critical role of video surveillance in modern security and operational management strategies. Investment opportunities abound across technological innovation, geographic expansion, and application diversification, with particular emphasis on artificial intelligence, cloud solutions, and integrated security platforms. Overall, the Video Surveillance Market demonstrates strong fundamentals with multiple growth drivers, technological innovation, and expanding application areas that ensure sustained market expansion and attractive opportunities for stakeholders across the value chain.

Research Methodology - How this research was conducted

The research methodology employed for this Video Surveillance Market analysis combines comprehensive primary and secondary research approaches to ensure accuracy, reliability, and depth of market insights. Primary research involved extensive interviews with industry stakeholders including manufacturers, system integrators, end-users, and technology providers to gather firsthand market intelligence, validate assumptions, and understand emerging trends and challenges. These interviews were conducted across multiple geographic regions to capture diverse market perspectives and regional variations in adoption patterns and requirements. Secondary research encompassed a thorough review of industry reports, market databases, company financial statements, technical publications, and regulatory documents to establish baseline market data and historical trends. Market size calculations were derived using both top-down and bottom-up approaches, triangulating data from multiple sources to ensure accuracy and reliability. The analysis incorporated detailed segmentation studies examining service models, platform categories, and geographic distributions to provide comprehensive market coverage. Competitive landscape assessment involved detailed company profiling, market share analysis, and strategic capability evaluation based on public information, industry interviews, and market observations. The research methodology also included technology trend analysis examining patent filings, product launches, and innovation patterns to understand technological evolution and future market directions. Data validation processes involved cross-referencing information from multiple independent sources and applying statistical analysis techniques to ensure consistency and reliability of market projections. The methodology accounts for various market dynamics including economic conditions, regulatory environments, and technological disruptions that influence market growth and competitive positioning. This comprehensive research approach ensures that the analysis provides accurate, actionable insights for stakeholders seeking to understand and capitalize on opportunities within the Video Surveillance Market.

Research Scope - Coverage and limitations

The research scope for this Video Surveillance Market analysis encompasses a comprehensive examination of market dynamics, trends, competitive landscape, and growth opportunities across global regions and market segments. The study covers the period from 2025 through 2032, with detailed analysis of market size, segmentation, regional distribution, and competitive positioning within the video surveillance industry. The research includes detailed examination of service models including hosted, managed, and hybrid solutions, alongside platform analysis covering hardware and software components that constitute the surveillance ecosystem. Geographic coverage extends across major global regions including North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America, with analysis of regional market characteristics, growth drivers, and adoption patterns. The scope encompasses both established market segments and emerging applications, including traditional security surveillance, smart city initiatives, commercial security, and innovative applications such as health monitoring and retail analytics. Competitive analysis includes profiling of major market players, assessment of strategic capabilities, and evaluation of market positioning across different segments and regions. The research examines technological trends including artificial intelligence integration, cloud-based solutions, and advanced analytics capabilities that are reshaping the market landscape. Limitations of the research scope include the exclusion of certain niche surveillance applications and specialized market segments that represent minimal market share, as well as the focus on commercial and public sector applications while excluding detailed residential market analysis. The study also does not cover related but distinct markets such as access control systems or intrusion detection as standalone segments, though their integration with video surveillance is analyzed where relevant. These scope limitations ensure focused analysis while acknowledging areas outside the primary research coverage that may influence market dynamics indirectly.

Key Companies and Recent Developments in the Video Surveillance Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Video Surveillance Market features several key companies that have demonstrated leadership through continuous innovation, strategic partnerships, and market expansion initiatives. Axis Communications AB has strengthened its market position through the launch of advanced network cameras featuring enhanced artificial intelligence capabilities and improved cybersecurity features, while expanding its cloud-based surveillance offerings through strategic partnerships with major cloud service providers. The company recently announced the integration of deep learning processing units in its camera lineup, enabling advanced analytics at the edge and reducing bandwidth requirements for large-scale deployments. Dahua Technologies Co., Ltd has focused on expanding its global presence through strategic acquisitions and the establishment of local subsidiaries in key growth markets, particularly in Asia-Pacific and Latin America regions. The company recently unveiled its latest generation of AI-powered cameras with enhanced facial recognition and behavioral analysis capabilities, targeting both security and commercial analytics applications. FLIR Systems Inc. has leveraged its thermal imaging expertise to launch innovative perimeter security solutions that combine thermal and visible light imaging for enhanced detection capabilities in challenging environmental conditions. The company's recent partnership with major security system integrators has expanded its market reach in critical infrastructure protection applications. Honeywell International Inc. has advanced its integrated security platform strategy through the acquisition of complementary technology companies and the launch of unified security management solutions that combine video surveillance with access control and building automation systems. IndigoVision Group Plc has focused on enhancing its high-end IP video solutions with advanced cybersecurity features and improved scalability for large enterprise deployments, while expanding its presence in mission-critical applications through strategic partnerships with government agencies. Panasonic Corporation has introduced its latest 4K and 8K resolution cameras with enhanced low-light performance and AI-powered analytics capabilities, targeting high-end commercial and industrial applications. Robert Bosch GmbH has expanded its video surveillance portfolio through strategic acquisitions and the development of integrated security solutions that combine video analytics with IoT sensors and building management systems. Samsung Electronics Co., Ltd has launched its next-generation video management systems with enhanced cloud capabilities and mobile access features, while expanding its presence in emerging markets through local manufacturing partnerships. Schneider Electric has strengthened its integrated security offerings through the acquisition of specialized video analytics companies and the launch of energy-efficient surveillance solutions that combine security with sustainability objectives. Sony Corporation has introduced advanced imaging technologies in its latest camera lineup, featuring enhanced image processing capabilities and improved performance in challenging lighting conditions, while expanding its presence in the analytics software market through strategic partnerships with AI technology providers. These key companies continue to drive market innovation through product development, strategic partnerships, and geographic expansion initiatives that address evolving customer requirements and emerging market opportunities.