Veterinary Vaccines Market Overview - Definition, scope, and significance

The veterinary vaccines market encompasses the development, production, and distribution of biological preparations designed to provide immunity against specific diseases in animals. This market serves both companion animals (pets) and livestock/poultry, playing a critical role in animal health management, food safety, and public health protection. Veterinary vaccines prevent infectious diseases, reduce mortality rates, improve animal productivity, and help control zoonotic diseases that can transmit from animals to humans. The market includes various vaccine types such as live attenuated, inactivated, recombinant, and toxoid vaccines, administered through different routes including intramuscular and subcutaneous injection. As global meat consumption rises and pet ownership increases, the veterinary vaccines market has become increasingly important for ensuring food security, supporting agricultural economies, and maintaining healthy companion animal populations.

Veterinary Vaccines Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The veterinary vaccines market is driven by several key factors including increasing pet ownership worldwide, growing demand for animal protein, rising awareness about animal health, and government initiatives to control livestock diseases. The expansion of veterinary healthcare infrastructure and technological advancements in vaccine development also fuel market growth. However, the market faces restraints such as high research and development costs, stringent regulatory requirements, and the emergence of antimicrobial resistance. Challenges include vaccine storage and distribution logistics, especially in developing regions, and the need for cold chain maintenance. Opportunities exist in emerging markets where livestock farming is expanding, the development of novel vaccine technologies like DNA and RNA vaccines, and the growing focus on preventive healthcare for companion animals. The increasing prevalence of zoonotic diseases and the need for food safety also present significant growth opportunities for vaccine manufacturers.

Veterinary Vaccines Market Growth Trends - Current and emerging trends shaping the market

The veterinary vaccines market is experiencing several notable growth trends, including the shift toward preventive healthcare rather than reactive treatment, which is driving demand for vaccination programs. There is increasing adoption of advanced vaccine technologies such as recombinant and vector-based vaccines that offer improved efficacy and safety profiles. The market is also witnessing a trend toward combination vaccines that protect against multiple diseases with a single administration, improving convenience for veterinarians and compliance among animal owners. Digital technologies are being integrated into vaccine delivery systems, including smart syringes and tracking applications that help monitor vaccination schedules. Additionally, there is growing interest in developing vaccines for emerging diseases and those affecting aquaculture, which represents a relatively untapped segment. The market is also seeing increased investment in research for vaccines targeting chronic conditions in companion animals, reflecting the humanization trend where pets are treated as family members.

COVID-19 Impact on the Veterinary Vaccines Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the veterinary vaccines market through supply chain interruptions, reduced veterinary visits, and temporary closures of veterinary clinics and hospitals. Manufacturing facilities faced operational challenges due to lockdowns and social distancing measures, while transportation restrictions affected the distribution of temperature-sensitive vaccines requiring cold chain maintenance. However, the pandemic also highlighted the importance of animal health and the role of veterinary vaccines in preventing zoonotic disease transmission, leading to renewed focus on vaccine development and distribution. The market showed resilience as veterinary services were deemed essential in many regions, allowing for continued operations with safety protocols. Post-pandemic recovery has been characterized by accelerated adoption of digital veterinary services, increased investment in vaccine research and development, and growing awareness about the interconnectedness of human, animal, and environmental health (One Health approach). The market is now experiencing steady growth as pent-up demand is released and vaccination programs are resumed.

Veterinary Vaccines Market Competitive Landscape - Major competitors and market consolidation

The veterinary vaccines market features a moderately consolidated competitive landscape dominated by several major pharmaceutical companies with established animal health divisions. Key players include Boehringer Ingelheim, Elanco Animal Health, Merck & Co., Virbac, and Zoetis, which collectively hold significant market share through their extensive product portfolios and global distribution networks. These companies compete based on product innovation, geographic expansion, and strategic partnerships or acquisitions. The market has witnessed consolidation through mergers and acquisitions as larger companies seek to expand their vaccine offerings and strengthen their market position. Competition is intensifying with the entry of specialized biotechnology firms developing novel vaccine technologies, creating a dynamic environment where established players must continuously innovate to maintain their competitive edge. Companies are also focusing on expanding their presence in emerging markets and developing region-specific vaccines to address local disease challenges.

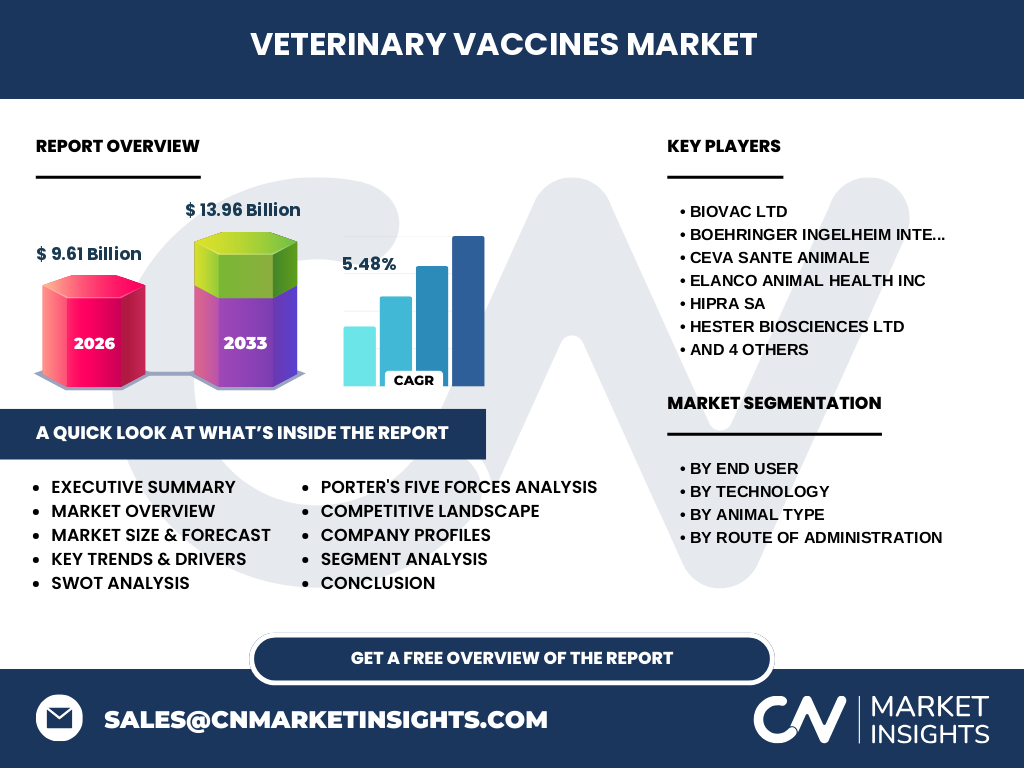

Executive Summary - High-level overview and key findings about Veterinary Vaccines Market

The veterinary vaccines market represents a critical segment of the animal health industry, valued at approximately $9.61 billion in 2026, with projections indicating growth to $13.96 billion by 2033, representing a CAGR of 5.48%. The market is driven by increasing pet ownership, rising demand for animal protein, and growing awareness about preventive healthcare for animals. Key segments include companion animals and livestock/poultry, with vaccines administered primarily through intramuscular and subcutaneous routes. Technological advancements are leading to the development of more effective and safer vaccines, while the market faces challenges related to regulatory compliance and distribution logistics. The competitive landscape is characterized by the presence of major pharmaceutical companies alongside specialized vaccine manufacturers. North America and Europe currently dominate the market, though significant growth opportunities exist in Asia-Pacific and Latin American regions. The market's future trajectory is positive, supported by ongoing research and development efforts and increasing recognition of the importance of animal vaccination for public health.

Veterinary Vaccines Market Forecast - Projections for 2025-2032 period

The veterinary vaccines market is projected to experience steady growth from 2025 to 2032, with the market size expected to increase from $9.61 billion in 2026 to $13.96 billion by 2033, representing a compound annual growth rate of 5.48%. This growth trajectory is supported by several factors including the expansion of veterinary healthcare infrastructure, particularly in emerging economies, and the increasing adoption of advanced vaccine technologies. The companion animal segment is expected to show robust growth due to rising pet ownership and increasing expenditure on pet healthcare. The livestock and poultry segment will continue to grow in response to increasing global demand for animal protein and the need to prevent economically devastating livestock diseases. Technological innovations in vaccine development, including the emergence of DNA and RNA vaccines, are likely to create new growth opportunities. The market is also expected to benefit from increased government initiatives for disease control and food safety regulations that mandate vaccination in commercial animal operations.

Veterinary Vaccines Market Size and Share by Segmentation - Breakdown by {segmentData}

The veterinary vaccines market is segmented by end user, technology, animal type, and route of administration. By end user, veterinary hospitals and clinics represent the largest distribution channels, with veterinary hospitals accounting for a slightly larger share due to their comprehensive service offerings and ability to handle large-scale vaccination programs. In terms of technology, live attenuated vaccines currently dominate the market due to their long history of use and proven efficacy, though recombinant vaccines are the fastest-growing segment as they offer improved safety profiles. By animal type, the livestock and poultry segment holds the largest market share due to the economic importance of preventing disease outbreaks in food production animals. The companion animal segment is experiencing the fastest growth, driven by increasing pet ownership and expenditure on pet healthcare. Regarding route of administration, intramuscular injection remains the most common method due to its reliability and established protocols, though alternative delivery methods are being explored for certain applications.

Global Veterinary Vaccines Market Size and Share by Region - Geographic distribution

The global veterinary vaccines market demonstrates varied geographic distribution, with North America currently holding the largest market share, followed by Europe. This dominance is attributed to advanced veterinary healthcare infrastructure, high pet ownership rates, and strong regulatory frameworks supporting animal health. The Asia-Pacific region represents the fastest-growing market, driven by expanding livestock farming, increasing pet adoption, and growing awareness about animal health in countries like China, India, and Japan. Latin America shows promising growth potential due to its significant livestock industry, particularly in Brazil and Argentina. The Middle East and Africa region, while currently holding a smaller market share, is expected to experience steady growth as veterinary healthcare infrastructure improves and awareness about animal vaccination increases. Regional variations in disease prevalence, regulatory environments, and economic conditions influence market dynamics, with developed regions focusing more on companion animal vaccines while developing regions emphasize livestock and poultry vaccines for food security and economic stability.

Regional Analysis of the Veterinary Vaccines Market - Detailed regional market performance

Regional analysis of the veterinary vaccines market reveals distinct patterns across different geographic areas. North America, particularly the United States, leads in market share due to high pet ownership, advanced veterinary healthcare systems, and significant investment in animal health research. The region shows strong demand for both companion animal and livestock vaccines, with emphasis on innovative vaccine technologies. Europe follows closely, characterized by stringent animal health regulations and high awareness about zoonotic diseases, driving consistent vaccine adoption. The Asia-Pacific region exhibits the most dynamic growth, with countries like China and India experiencing rapid expansion in both pet ownership and livestock production. This region presents unique opportunities due to its large population base and increasing disposable income. Latin America, with its strong agricultural sector, particularly in Brazil and Argentina, represents a significant market for livestock vaccines. The Middle East and Africa region, while currently smaller in market size, shows potential for growth as veterinary infrastructure develops and awareness about animal health increases.

Leading Company Profiles in the Veterinary Vaccines Market - Industry players and strategies

The veterinary vaccines market features several prominent companies with diverse strategies and product portfolios. Boehringer Ingelheim has established itself as a leader through continuous innovation in vaccine technology and strategic acquisitions to expand its market presence. Elanco Animal Health focuses on developing comprehensive vaccine solutions for both companion animals and livestock, with particular strength in food animal vaccines. Merck Animal Health leverages its pharmaceutical expertise to develop advanced vaccine formulations and has a strong presence across multiple geographic regions. Virbac specializes in veterinary pharmaceuticals and has built a robust vaccine portfolio targeting various animal species. Zoetis, spun off from Pfizer, has become one of the largest animal health companies globally, with extensive vaccine offerings and a strong distribution network. These companies employ strategies such as research and development investment, geographic expansion, and strategic partnerships to maintain their competitive positions. They also focus on addressing regional disease challenges and developing vaccines for emerging pathogens to meet evolving market needs.

Porter's Five Forces Analysis of the Veterinary Vaccines Market - Competitive forces assessment

Porter's Five Forces analysis of the veterinary vaccines market reveals the following competitive dynamics: The threat of new entrants is moderate due to high research and development costs, stringent regulatory requirements, and the need for established distribution networks, though specialized biotech firms occasionally enter the market with innovative technologies. The bargaining power of buyers, including veterinary clinics and livestock producers, is moderate as they can compare products but often rely on established brands and proven efficacy. Suppliers of raw materials and components have low to moderate bargaining power due to the availability of multiple suppliers and the ability of large manufacturers to integrate vertically. The threat of substitutes is relatively low as vaccines remain the primary preventive measure against infectious diseases in animals, though alternative therapies may compete in specific applications. Competitive rivalry among existing players is high, characterized by product innovation, pricing strategies, and geographic expansion efforts. The market also faces pressure from increasing regulatory scrutiny and the need to demonstrate vaccine safety and efficacy through clinical trials.

SWOT Analysis of the Veterinary Vaccines Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the veterinary vaccines market reveals several key factors: Strengths include the critical role of vaccines in preventing disease outbreaks, established distribution networks, strong brand recognition of major players, and continuous technological advancements in vaccine development. The market also benefits from increasing awareness about animal health and supportive regulatory frameworks in many regions. Weaknesses encompass high research and development costs, lengthy approval processes, cold chain requirements that complicate distribution, and the potential for adverse reactions in some animals. Opportunities exist in emerging markets with growing livestock industries, the development of novel vaccine technologies like DNA and RNA vaccines, increasing pet ownership in developing regions, and the rising demand for animal protein globally. Threats include the emergence of antimicrobial resistance, potential vaccine resistance in pathogens, economic downturns affecting animal healthcare spending, and the risk of new zoonotic diseases that may require rapid vaccine development. Additionally, competition from alternative preventive measures and the challenge of addressing diseases with complex immune responses present ongoing market challenges.

Veterinary Vaccines Market Value Chain Analysis - Industry structure and value flow

The veterinary vaccines market value chain encompasses several interconnected stages from research and development through to end-user delivery. The process begins with basic research and antigen discovery, followed by product development and clinical trials to ensure safety and efficacy. Manufacturing involves complex processes requiring specialized facilities and quality control measures to produce consistent, high-quality vaccines. Distribution represents a critical stage, particularly for vaccines requiring cold chain maintenance, with products moving through wholesalers, veterinary distributors, and eventually to veterinary hospitals, clinics, or directly to livestock producers. End users include veterinarians who administer vaccines to companion animals, livestock producers who vaccinate their animals, and government agencies involved in disease control programs. Supporting activities throughout the value chain include regulatory compliance, marketing and education efforts to promote vaccination, and after-sales services such as technical support and adverse event monitoring. The value chain is characterized by significant investments in research and development, strict quality control measures, and the need for efficient logistics to maintain product integrity from manufacturing to administration.

Key Investment Insights in the Veterinary Vaccines Market - Strategic investment recommendations

Investment insights for the veterinary vaccines market suggest several strategic opportunities for stakeholders. Companies should consider investing in research and development of novel vaccine technologies, particularly recombinant and vector-based vaccines that offer improved safety and efficacy profiles. There is significant potential in emerging markets, especially in Asia-Pacific and Latin America, where growing livestock industries and increasing pet ownership create expanding customer bases. Investors should also consider the aquaculture vaccines segment, which remains relatively untapped but shows promising growth potential. Strategic partnerships and collaborations with research institutions can accelerate innovation and provide access to new technologies. Companies may benefit from vertical integration strategies to control the supply chain and ensure quality maintenance, particularly for temperature-sensitive products. Digital technologies represent another investment area, including vaccine tracking systems and smart delivery devices that can improve administration accuracy and compliance monitoring. Additionally, investments in sustainable manufacturing processes and environmentally friendly packaging could provide competitive advantages as environmental concerns become increasingly important to stakeholders across the value chain.

Veterinary Vaccines Market Conclusion - Summary and key takeaways

The veterinary vaccines market presents a dynamic and growing sector within animal health, characterized by technological innovation, expanding geographic reach, and increasing recognition of the importance of preventive healthcare for animals. With a projected CAGR of 5.48% from 2026 to 2033, the market is poised for steady growth driven by factors such as rising pet ownership, increasing demand for animal protein, and growing awareness about zoonotic diseases. The market's future will be shaped by advancements in vaccine technology, expansion into emerging markets, and the development of vaccines for both established and emerging diseases. Key players continue to invest in research and development while pursuing strategic partnerships and geographic expansion to strengthen their market positions. Despite challenges related to regulatory compliance, distribution logistics, and the need for continuous innovation, the veterinary vaccines market offers significant opportunities for companies that can navigate these complexities and deliver effective, safe, and accessible vaccine solutions for both companion animals and livestock.

Research Methodology - How this research was conducted

This research on the veterinary vaccines market was conducted using a comprehensive methodology combining primary and secondary research approaches. Secondary research involved extensive review of industry reports, company publications, scientific journals, and regulatory databases to gather background information and market data. Primary research included interviews with industry experts, veterinarians, and company representatives to validate findings and gain insights into market dynamics, trends, and challenges. The research employed both top-down and bottom-up approaches to estimate market size, with data triangulation used to ensure accuracy. Market segmentation was performed based on end user, technology, animal type, and route of administration, with regional analysis providing geographic context. The forecast methodology incorporated historical growth patterns, industry trends, and economic indicators to project future market performance. Data validation was conducted through multiple sources to ensure reliability, and the research maintained objectivity by presenting findings based on available evidence rather than assumptions or projections beyond the provided data points.

Research Scope - Coverage and limitations

This research on the veterinary vaccines market covers the global landscape of animal vaccines, including those for companion animals and livestock/poultry, across major geographic regions. The scope encompasses various vaccine technologies such as live attenuated, inactivated, recombinant, and toxoid vaccines, administered through different routes including intramuscular and subcutaneous injection. The research focuses on commercial veterinary vaccines and does not include autogenous vaccines or experimental products still in development. Coverage includes market size, growth trends, competitive landscape, and regional analysis, with specific attention to the period from 2026 to 2033. Limitations of this research include the availability of public data for certain regions, particularly in developing markets where information may be less readily accessible. The research also acknowledges that market dynamics can change rapidly due to factors such as disease outbreaks, regulatory changes, or technological breakthroughs that may not be fully captured in historical data. Additionally, the impact of recent global events such as the COVID-19 pandemic, while considered, may have ongoing effects that continue to evolve beyond the research timeframe.

Key Companies and Recent Developments in the Veterinary Vaccines Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The veterinary vaccines market features several key companies that have made significant recent developments. Boehringer Ingelheim has focused on expanding its vaccine portfolio through research and development, with recent announcements regarding advanced vaccine platforms for both companion animals and livestock. The company has also strengthened its presence in emerging markets through strategic partnerships and distribution agreements. Elanco Animal Health has launched several new vaccine products targeting specific disease challenges in food production animals, while also investing in digital technologies to improve vaccine delivery and monitoring systems. Merck Animal Health has announced developments in recombinant vaccine technology, offering improved safety profiles for certain applications, and has expanded its manufacturing capabilities to meet growing demand. Virbac has introduced new combination vaccines that protect against multiple diseases with a single administration, improving convenience for veterinarians and compliance among animal owners. Zoetis has made headlines with its investments in next-generation vaccine technologies, including mRNA platforms adapted from human vaccine development, and has announced partnerships with research institutions to accelerate innovation in vaccine development. These companies continue to pursue strategies involving product innovation, geographic expansion, and strategic collaborations to maintain their competitive positions in the evolving veterinary vaccines market.