What is the Cling Films Market and why is it significant?

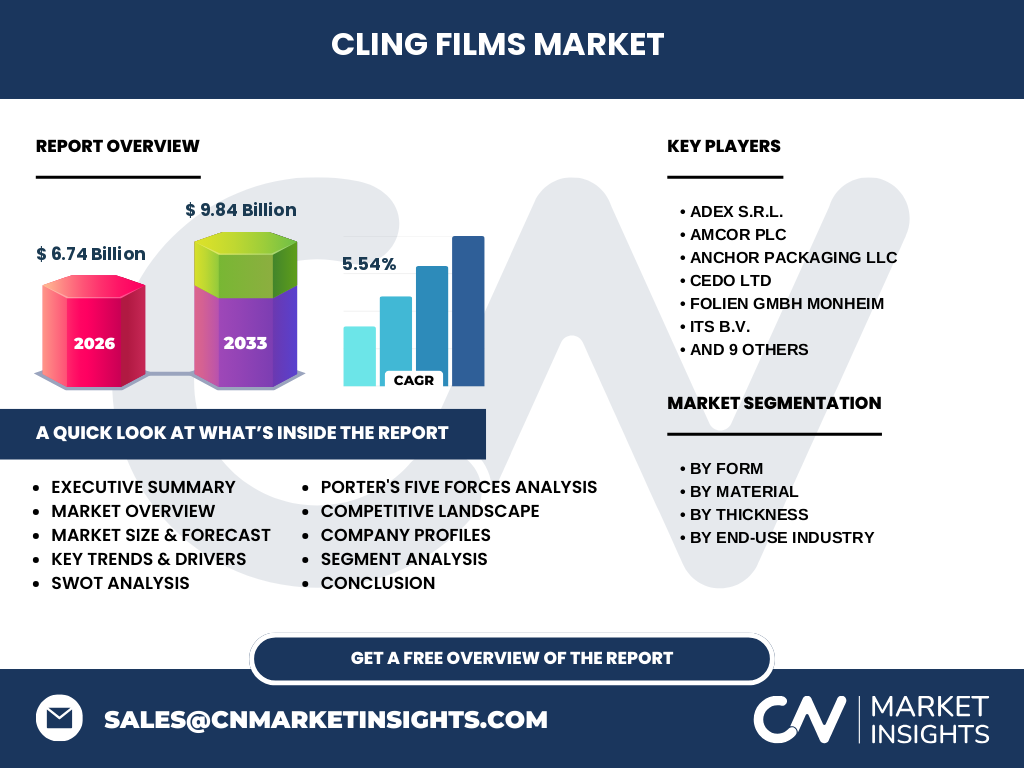

Cling films are thin plastic wraps used primarily for food preservation and packaging, designed to cling to surfaces through static electricity or self-adhesion. The global cling films market has emerged as a critical component of modern packaging solutions, valued at 6.74 billion in 2026 and projected to reach 9.84 billion by 2033, growing at a CAGR of 5.54%. These versatile films serve multiple industries including food, healthcare, consumer goods, and industrial applications, providing essential functions such as extending shelf life, preventing contamination, and offering convenient storage solutions. The market's significance stems from its role in reducing food waste, maintaining product integrity, and meeting the growing demand for convenient packaging solutions in both developed and emerging economies.

What are the key drivers, restraints, challenges, and opportunities in the Cling Films Market?

The cling films market is primarily driven by increasing consumer demand for convenient food packaging, rising awareness about food safety, and the growing retail and foodservice sectors. The food industry remains the largest end-user segment, with cling films playing a crucial role in preserving freshness and extending shelf life. However, the market faces restraints from environmental concerns and regulatory pressures regarding plastic usage, particularly around single-use plastics and non-biodegradable materials. Challenges include raw material price volatility and the need for sustainable alternatives. Opportunities exist in developing biodegradable and compostable cling films, expanding into emerging markets, and innovating with antimicrobial and smart packaging features that can monitor food freshness.

What are the current and emerging trends shaping the Cling Films Market?

The cling films market is witnessing several transformative trends, including the shift toward sustainable packaging solutions with bio-based and recyclable materials gaining traction. There's growing adoption of thinner films that reduce material usage while maintaining performance, driven by cost efficiency and environmental considerations. Smart packaging innovations incorporating sensors for freshness monitoring represent an emerging trend, particularly in premium food segments. The market is also seeing increased demand for specialized films with enhanced barrier properties for specific applications. E-commerce growth has created new packaging requirements, with films needing to provide additional protection during transit. Additionally, there's a trend toward customized films for specific food types and applications, reflecting the market's evolution from commodity products to specialized solutions.

How did COVID-19 impact the Cling Films Market and what is the recovery trajectory?

The COVID-19 pandemic initially disrupted the cling films market through supply chain interruptions and manufacturing slowdowns. However, the market demonstrated resilience as demand surged in key sectors like food packaging and healthcare. Lockdowns and increased home cooking drove higher consumption of packaged foods, boosting cling film usage in retail applications. The healthcare sector saw increased demand for medical packaging applications. Supply chain challenges led to inventory shortages and price volatility in the short term. As economies recover, the market is experiencing a rebound with renewed focus on food safety and hygiene, accelerating trends toward convenient packaging solutions. The recovery trajectory shows steady growth, with the market expected to reach 9.84 billion by 2033, indicating strong post-pandemic momentum.

Who are the major competitors in the Cling Films Market and what is the competitive landscape?

The cling films market features a competitive landscape with both global and regional players. Major companies include Amcor Plc, Mitsubishi Chemical Group Corp, Polycart S.p.A., and POLIFILM, alongside specialized manufacturers like Adex S.r.l. and Melitta Group. The market shows moderate consolidation with leading players holding significant market share through their extensive product portfolios and global distribution networks. Competition centers on product innovation, quality, pricing, and sustainability initiatives. Companies are investing in R&D to develop eco-friendly alternatives and advanced film technologies. The competitive dynamics also involve strategic partnerships, mergers, and acquisitions to expand geographical presence and technological capabilities. Regional manufacturers maintain strong positions in their local markets, creating a balanced competitive environment between multinational corporations and domestic players.

What are the key findings and high-level overview of the Cling Films Market?

The cling films market presents a robust growth trajectory with a current valuation of 6.74 billion in 2026, expanding to 9.84 billion by 2033 at a 5.54% CAGR. The market demonstrates strong fundamentals driven by food industry applications, which represent the largest end-use segment. Material preferences show polyethylene dominance, while innovations in bio-based alternatives are gaining momentum. The market is segmented by form (cast and blow cling films), material type, thickness, and end-use industry, with each segment showing distinct growth patterns. North America and Europe lead in terms of market maturity, while Asia-Pacific presents the highest growth potential. The competitive landscape features established players focusing on sustainability and technological advancement. Overall, the market shows resilience and adaptability, with opportunities in sustainable solutions and emerging market expansion counterbalancing challenges from environmental regulations.

What is the market forecast for Cling Films from 2025 to 2032?

The cling films market is projected to experience steady growth from 2025 to 2032, with the market size expanding from 6.74 billion in 2026 to 9.84 billion by 2033. This represents a compound annual growth rate of 5.54% over the forecast period. The growth trajectory is supported by increasing demand across key end-use industries, particularly food packaging and healthcare. The forecast indicates consistent year-on-year growth, with particular acceleration expected in emerging markets as economic development drives packaging demand. Technological advancements in film properties and the introduction of sustainable alternatives are expected to create new growth opportunities. The market is likely to see continued innovation in material science, with bio-based and recyclable films gaining market share. Regional growth will vary, with Asia-Pacific showing the highest growth rates while mature markets in North America and Europe maintain steady expansion through value-added products.

How is the Cling Films Market segmented by form, material, thickness, and end-use industry?

The cling films market is segmented across multiple dimensions. By form, the market includes cast cling film and blow cling film, with cast films typically dominating due to their superior clarity and consistent thickness. Material segmentation shows polyethylene as the dominant material due to its cost-effectiveness and versatility, followed by biaxially oriented polypropylene and polyvinyl chloride. The thickness segment is categorized into upto 9 microns, 9-12 microns, and above 12 microns, with thinner films gaining popularity for cost and environmental reasons. By end-use industry, food industry applications represent the largest segment, driven by retail packaging and food service needs. Healthcare applications are growing due to medical packaging requirements. Consumer goods, industrial applications, and other sectors complete the segmentation, each with specific film requirements and growth trajectories.

How is the Global Cling Films Market distributed across different regions?

The global cling films market shows distinct regional patterns in terms of market size and growth rates. North America and Europe represent mature markets with established infrastructure and high per capita consumption, driven by sophisticated food packaging industries and stringent food safety regulations. Asia-Pacific emerges as the fastest-growing region, fueled by rapid industrialization, expanding food retail sectors, and growing middle-class populations in countries like China and India. Latin America shows steady growth with increasing adoption in food processing and packaging. The Middle East and Africa region presents emerging opportunities, particularly in the Gulf Cooperation Council countries with their growing food service sectors. Regional variations in consumer preferences, regulatory environments, and economic development create differentiated market dynamics, with developed regions focusing on premium and sustainable solutions while emerging markets prioritize cost-effective options.

What are the detailed regional market performances in the Cling Films Market?

Regional market performances in the cling films industry reflect diverse economic conditions and industry structures. North America demonstrates stable growth with high adoption rates in food service and retail packaging, driven by convenience culture and food safety awareness. Europe shows mature market characteristics with strong emphasis on sustainability and regulatory compliance, particularly regarding plastic usage and recycling. The Asia-Pacific region exhibits the most dynamic growth, with countries like China, India, and Southeast Asian nations experiencing rapid expansion in food processing and retail sectors. Japan and South Korea show advanced adoption of innovative packaging solutions. Latin America presents moderate growth with Brazil and Mexico as key markets, while the Middle East and Africa region shows emerging potential, particularly in urban centers and tourism-driven economies. Each region's performance is influenced by local factors including economic development, regulatory frameworks, and cultural preferences regarding food storage and packaging.

Who are the leading companies in the Cling Films Market and what are their strategies?

Leading companies in the cling films market include Amcor Plc, Mitsubishi Chemical Group Corp, Polycart S.p.A., and POLIFILM, among others. These companies employ diverse strategies to maintain competitive advantage. Amcor focuses on sustainable packaging solutions and global market expansion through strategic acquisitions. Mitsubishi Chemical emphasizes technological innovation and high-performance films for specialized applications. Polycart and POLIFILM concentrate on European market leadership through product quality and customer service. Companies like Melitta Group leverage their brand reputation in food-related products to expand into packaging solutions. Common strategies across the industry include investment in R&D for sustainable materials, expansion into emerging markets, vertical integration to control supply chains, and development of value-added products with enhanced properties. Many companies are also pursuing partnerships with food manufacturers to develop customized solutions and strengthen market positions.

What does Porter's Five Forces analysis reveal about the Cling Films Market?

Porter's Five Forces analysis of the cling films market reveals a moderately competitive industry structure. The threat of new entrants is moderate due to significant capital requirements and established distribution networks, though regional players can still enter local markets. Bargaining power of suppliers is relatively low as raw material suppliers are numerous and alternative sources exist. Buyer power varies by segment, with large food manufacturers having significant influence while smaller buyers have less negotiating leverage. The threat of substitutes exists through alternative packaging materials like foil, paper, and rigid containers, though cling films maintain advantages in specific applications. Competitive rivalry is intense among established players, characterized by price competition, product differentiation, and innovation. The overall industry attractiveness is moderate, with growth opportunities balanced against environmental pressures and regulatory challenges.

What does the SWOT analysis reveal about the Cling Films Market?

The SWOT analysis of the cling films market reveals several key insights. Strengths include the product's essential role in food preservation, established manufacturing processes, and wide application across multiple industries. Weaknesses encompass environmental concerns about plastic usage, dependence on petroleum-based raw materials, and vulnerability to regulatory changes. Opportunities exist in developing sustainable alternatives, expanding into emerging markets, and creating value-added products with enhanced properties. Threats include increasing environmental regulations, competition from alternative packaging materials, and raw material price volatility. The analysis indicates that companies focusing on sustainability and innovation can leverage strengths to capitalize on opportunities while addressing weaknesses and mitigating threats. The market's adaptability to changing consumer preferences and regulatory requirements will be crucial for long-term success.

How does the value chain analysis explain the Cling Films Market structure?

The value chain analysis of the cling films market reveals a structured industry flow from raw materials to end consumers. The chain begins with polymer resin suppliers providing polyethylene, polypropylene, and other base materials. These materials are processed by film manufacturers who extrude and convert them into cling films through various technologies. The films are then distributed through various channels including direct sales to large manufacturers, distributors, and retailers. Key value-adding activities include material formulation, film production technology, quality control, and customization for specific applications. Support activities such as R&D for new materials and technologies, logistics, and marketing play crucial roles in competitive differentiation. The value chain demonstrates opportunities for efficiency improvements, particularly in sustainable material development and production processes. Companies that can optimize their value chain operations while maintaining quality and sustainability standards are best positioned for success.

What are the key investment insights for the Cling Films Market?

Key investment insights for the cling films market indicate strong growth potential balanced with strategic considerations. Investors should focus on companies with robust R&D capabilities in sustainable materials, as environmental regulations are likely to intensify. The Asia-Pacific region presents the most attractive growth opportunities due to expanding food processing industries and rising disposable incomes. Investment in automation and efficiency improvements in manufacturing processes can provide competitive advantages through cost reduction. Companies with strong distribution networks and established customer relationships in key end-use industries offer more stable investment prospects. The shift toward thinner, more efficient films represents an investment trend that can reduce material costs while meeting sustainability goals. Additionally, investments in smart packaging technologies and antimicrobial films could capture premium market segments. Overall, a balanced approach considering both growth potential and environmental compliance will yield the best investment outcomes.

What are the key conclusions and takeaways from the Cling Films Market analysis?

The cling films market analysis reveals a dynamic industry with strong fundamentals and significant growth potential. Key conclusions include the market's resilience demonstrated through pandemic recovery, the importance of food industry applications as the primary growth driver, and the increasing focus on sustainability as a critical success factor. The market is characterized by steady growth at a 5.54% CAGR, with expansion from 6.74 billion in 2026 to 9.84 billion by 2033. Regional variations show mature markets in developed economies while emerging markets, particularly in Asia-Pacific, offer the highest growth potential. The competitive landscape features both global leaders and regional players, with innovation and sustainability as key differentiators. Companies that can navigate environmental regulations while meeting growing demand for convenient packaging solutions are best positioned for success. The market's future will be shaped by technological advancements, regulatory developments, and changing consumer preferences toward sustainable packaging.

How was this research on the Cling Films Market conducted?

This comprehensive research on the cling films market was conducted using a rigorous methodology combining multiple data sources and analytical approaches. Primary research involved interviews with industry experts, manufacturers, distributors, and end-users to gather firsthand insights on market dynamics, trends, and challenges. Secondary research encompassed extensive review of industry reports, company publications, trade journals, and government databases to validate and supplement primary findings. Market size and forecast calculations utilized both top-down and bottom-up approaches, considering historical data, current market conditions, and future growth projections. Data triangulation ensured accuracy by cross-verifying information from multiple sources. The research methodology also included competitive analysis, regional assessments, and segment-specific evaluations to provide a comprehensive market understanding. All findings were subjected to quality checks and validation processes to ensure reliability and relevance for strategic decision-making.

What is the scope and coverage of this Cling Films Market research?

This research on the cling films market provides comprehensive coverage of the global industry, encompassing market size, growth trends, competitive landscape, and future projections. The scope includes detailed analysis by form (cast and blow cling films), material type (polyethylene, BOPP, PVC, PVDC, and others), thickness categories (upto 9 microns, 9-12 microns, above 12 microns), and end-use industries (food, healthcare, consumer goods, industrial, and others). Regional coverage spans North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis for key markets. The research examines market drivers, restraints, opportunities, and challenges, along with impact analysis of COVID-19. Competitive analysis includes profiling of major players and their strategies. The forecast period extends to 2033, providing long-term growth projections. Limitations include potential data availability constraints in certain emerging markets and the inherent uncertainty in long-term projections due to changing market conditions.

Who are the key companies in the Cling Films Market and what are their recent developments?

The key companies in the cling films market include Amcor Plc, Mitsubishi Chemical Group Corp, Polycart S.p.A., POLIFILM, and others such as Adex S.r.l., Melitta Group, and Multiwrap. Recent developments across these companies reflect industry-wide trends toward sustainability and innovation. Amcor has announced investments in recyclable film technologies and expanded its sustainable packaging portfolio. Mitsubishi Chemical has focused on developing high-performance films with enhanced barrier properties for specialized applications. Polycart and POLIFILM have strengthened their European market positions through capacity expansions and product line enhancements. Companies like Melitta Group have leveraged their food industry expertise to develop integrated packaging solutions. Recent strategic moves include mergers and acquisitions to expand technological capabilities, partnerships with food manufacturers for customized solutions, and investments in automation to improve production efficiency. Many companies have also announced commitments to reduce plastic usage and increase recycled content in their products, aligning with growing environmental concerns.