Agricultural Biological Market Overview - Definition, scope, and significance

Agricultural biologicals refer to crop inputs derived from natural sources such as microorganisms, plant extracts, beneficial insects, and other biological materials. These products offer sustainable alternatives to conventional chemical-based agricultural inputs, including biopesticides, biostimulants, and biofertilizers. The market encompasses solutions that enhance crop productivity, protect plants from pests and diseases, and improve soil health while reducing environmental impact. The significance of agricultural biologicals lies in their ability to support sustainable farming practices, reduce chemical residues in food, and address growing concerns about environmental degradation and soil health deterioration. As the agricultural sector faces increasing pressure to produce more food with fewer resources, biological products provide innovative solutions that align with both productivity goals and sustainability requirements.

Agricultural Biological Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The agricultural biological market is primarily driven by increasing demand for organic food, growing awareness about environmental sustainability, and stringent regulations on chemical pesticides. Farmers are seeking alternatives to synthetic chemicals due to rising concerns about soil degradation, water contamination, and human health impacts. Additionally, the need to improve crop yields to feed a growing global population while minimizing environmental footprint creates significant opportunities for biological solutions. However, the market faces restraints including limited shelf life of biological products, inconsistent performance under varying environmental conditions, and higher costs compared to conventional alternatives. Challenges include the need for farmer education, technical expertise requirements, and the time-intensive nature of biological product application. Opportunities exist in developing region-specific solutions, integrating biologicals with conventional farming practices, and leveraging technological advancements in formulation and delivery systems to enhance product efficacy and stability.

Agricultural Biological Market Growth Trends - Current and emerging trends shaping the market

The agricultural biological market is experiencing several transformative trends that are reshaping the industry landscape. Precision agriculture integration represents a significant trend, where biological products are being incorporated into data-driven farming systems for optimized application timing and dosage. Another emerging trend is the development of multi-functional biological products that combine pest control, nutrient enhancement, and stress tolerance in single formulations. The market is also witnessing increased focus on microbial consortia and synthetic biology approaches to develop more effective and stable biological solutions. Digital platforms for biological product recommendation and application guidance are gaining traction, helping farmers make informed decisions. Additionally, there is growing interest in regenerative agriculture practices that heavily rely on biological inputs to restore soil health and ecosystem functions. The trend toward biological seed treatments is also accelerating, offering protection from early-season pests and diseases while promoting plant growth from germination through establishment.

COVID-19 Impact on the Agricultural Biological Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the agricultural biological market through supply chain interruptions, reduced farmer incomes, and logistical challenges in product distribution. Lockdowns and movement restrictions affected the timely availability of biological products, particularly in developing regions where cold chain infrastructure is limited. However, the pandemic also accelerated certain positive trends, including increased focus on food security, sustainability, and self-sufficiency in agriculture. As the industry recovers, there is renewed emphasis on resilient agricultural systems that can withstand future disruptions. The pandemic highlighted the importance of local and sustainable food production, driving interest in biological solutions that support soil health and reduce dependency on imported chemical inputs. Recovery trajectories show increasing adoption rates as supply chains stabilize and awareness about the benefits of biological products continues to grow. The crisis has also prompted companies to invest in digital tools and remote advisory services to support farmers during restricted movement periods.

Agricultural Biological Market Competitive Landscape - Major competitors and market consolidation

The agricultural biological market features a diverse competitive landscape with both established agrochemical giants and specialized biological companies competing for market share. Major players like BASF SE, Syngenta, and DowDuPont Inc. leverage their extensive distribution networks, research capabilities, and financial resources to maintain dominant positions. These companies are actively acquiring innovative biological startups to expand their product portfolios and technological capabilities. Meanwhile, specialized companies such as Marrone Bio Innovations, Koppert Biological Systems, and Valent BioSciences LLC focus on developing cutting-edge biological solutions and niche market segments. The market is experiencing significant consolidation through mergers, acquisitions, and strategic partnerships as companies seek to strengthen their biological product offerings. Competition is intensifying in emerging markets where local players are gaining prominence by offering region-specific solutions. The competitive dynamics are also shaped by increasing investments in research and development, with companies racing to develop next-generation biological products that offer superior efficacy and stability compared to conventional alternatives.

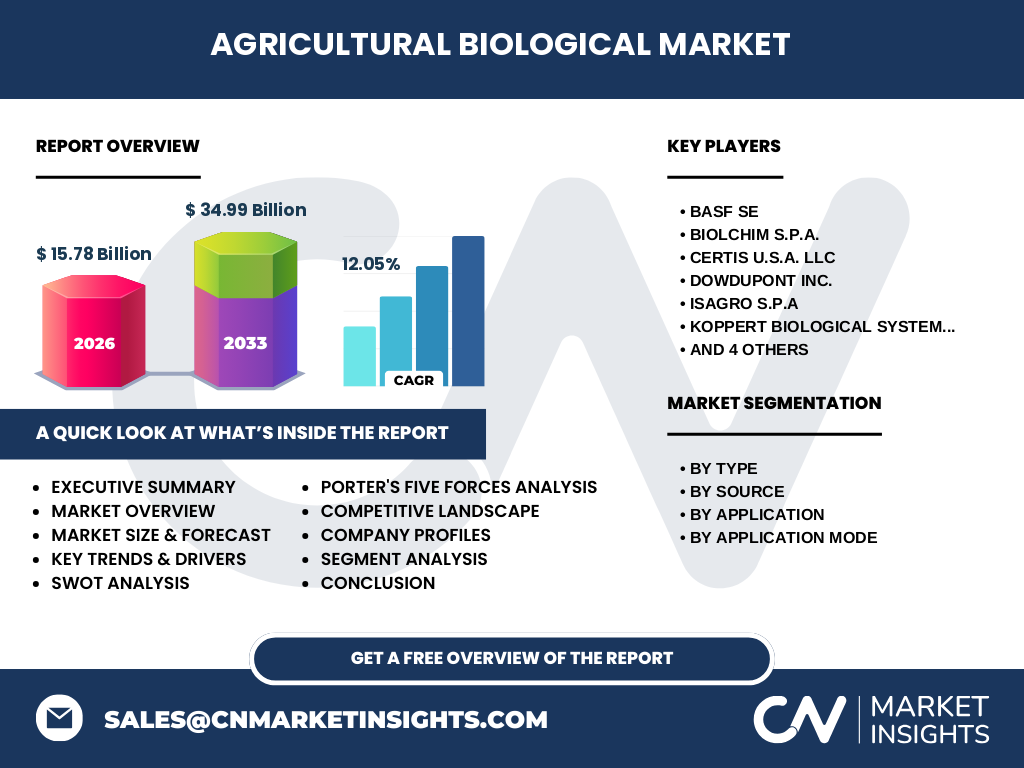

Executive Summary - High-level overview and key findings about Agricultural Biological Market

The agricultural biological market is positioned for substantial growth, with the market size projected to expand from $15.78 billion in 2026 to $34.99 billion by 2033, representing a robust CAGR of 12.05%. This growth trajectory reflects the increasing adoption of sustainable agricultural practices and the growing recognition of biological products' benefits in enhancing crop productivity while minimizing environmental impact. The market is characterized by diverse product categories including biopesticides, biostimulants, and biofertilizers, with applications spanning across major crop segments such as cereals and grains, oilseeds and pulses, and fruits and vegetables. Regional markets show varying adoption rates, with developed regions leading in technology adoption while emerging markets present significant growth opportunities. The competitive landscape features a mix of established agrochemical companies and specialized biological firms, with ongoing consolidation through strategic acquisitions. Key challenges include product stability, efficacy consistency, and farmer education, while opportunities abound in technological innovations, emerging market expansion, and integration with digital farming solutions. The market's future appears promising, driven by sustainability imperatives, regulatory support, and growing consumer demand for residue-free food products.

Agricultural Biological Market Forecast - Projections for 2025-2032 period

The agricultural biological market is projected to experience significant growth during the 2025-2032 period, with market value expected to increase from $15.78 billion to $34.99 billion. This represents a compound annual growth rate of 12.05%, indicating strong market momentum and expanding adoption across global agricultural sectors. The forecast period is characterized by increasing investment in biological research and development, with companies focusing on improving product efficacy, stability, and ease of application. Geographic expansion is expected to be particularly strong in Asia-Pacific and Latin American regions, where agricultural modernization and sustainability initiatives are gaining momentum. The biopesticides segment is anticipated to show the highest growth rate, driven by regulatory pressures on chemical pesticides and increasing pest resistance issues. Biostimulants and biofertilizers are also expected to see substantial growth as farmers recognize their role in improving soil health and crop resilience. Technological advancements in formulation and delivery systems are projected to enhance product performance, further driving market adoption. The forecast suggests that biological products will increasingly complement rather than replace conventional inputs, leading to integrated crop management approaches that optimize both productivity and sustainability.

Agricultural Biological Market Size and Share by Segmentation - Breakdown by {segmentData}

The agricultural biological market demonstrates distinct segmentation patterns across various categories. By type, biopesticides represent the largest segment, accounting for approximately 40% of the market share, driven by regulatory pressures on chemical pesticides and increasing pest resistance. Biostimulants constitute around 35% of the market, gaining popularity due to their ability to enhance plant growth and stress tolerance. Biofertilizers represent the remaining 25%, with steady growth as farmers recognize their soil health benefits. By source, microbial-based products dominate the market, capturing approximately 60% share due to their proven effectiveness and diverse applications. Biochemicals account for the remaining 40%, with increasing development of plant extract-based solutions. In terms of application, cereals and grains represent the largest crop segment at 45% market share, followed by fruits and vegetables at 35%, and oilseeds and pulses at 20%. Regarding application mode, foliar sprays lead with 50% share due to ease of application, while soil treatment and seed treatment share the remaining 50% equally. This segmentation analysis reveals diverse opportunities across product types, sources, crops, and application methods, with each segment presenting unique growth dynamics and market potential.

Global Agricultural Biological Market Size and Share by Region - Geographic distribution

The global agricultural biological market exhibits significant regional variations in adoption rates, market maturity, and growth potential. North America currently leads the market, accounting for approximately 35% of global market share, driven by advanced agricultural practices, strong regulatory support for sustainable farming, and high awareness levels among farmers. Europe follows with around 30% market share, characterized by stringent regulations on chemical inputs and strong organic farming initiatives. The Asia-Pacific region represents 25% of the market, showing the highest growth potential due to large agricultural areas, increasing modernization efforts, and growing awareness about sustainable practices. Latin America accounts for 8% of the market, with countries like Brazil and Argentina emerging as significant adopters due to their large-scale farming operations and export-oriented agriculture. The Middle East and Africa represent the smallest regional market at 2%, though this region presents untapped opportunities as agricultural modernization progresses. Regional dynamics are influenced by factors such as government policies, farmer income levels, crop types, and the prevalence of contract farming arrangements. Developed regions show higher adoption of advanced biological products, while emerging markets focus more on basic biological solutions that address fundamental crop protection and nutrition needs.

Regional Analysis of the Agricultural Biological Market - Detailed regional market performance

Regional market performance in the agricultural biological sector varies significantly based on local agricultural practices, regulatory environments, and economic conditions. North America demonstrates mature market characteristics with high adoption rates of advanced biological products, particularly in the United States where integrated pest management programs widely incorporate biological solutions. The region benefits from strong research infrastructure, farmer education programs, and supportive regulatory frameworks that facilitate biological product registration and use. Europe shows similar maturity levels, with countries like Germany, France, and the Netherlands leading in biological adoption due to strict chemical pesticide regulations and strong organic farming movements. The Asia-Pacific region exhibits diverse market characteristics, with countries like India and China showing rapid adoption driven by government initiatives promoting sustainable agriculture and reducing chemical input dependency. However, adoption rates vary significantly within the region due to differences in farmer education levels and infrastructure availability. Latin America presents unique opportunities in countries with large agricultural export sectors, where biological products help meet international residue standards. Regional performance is also influenced by local crop preferences, with rice-growing regions showing different biological adoption patterns compared to wheat or corn-producing areas. Climate conditions and pest pressures vary by region, necessitating localized biological solutions and application strategies.

Leading Company Profiles in the Agricultural Biological Market - Industry players and strategies

The agricultural biological market features several prominent companies with distinct strategic approaches and market positioning. BASF SE leverages its extensive chemical industry experience to develop integrated biological-chemical solutions, focusing on research-driven innovations and global distribution networks. The company's strategy emphasizes combining biological products with digital farming tools to provide comprehensive crop management solutions. Syngenta pursues a similar integrated approach while also investing heavily in biological research centers across multiple regions to develop locally adapted solutions. Marrone Bio Innovations specializes exclusively in biological products, focusing on developing novel microbial and botanical-based solutions with strong intellectual property protection. Their strategy centers on innovation and targeting high-value crop segments where biological solutions offer clear economic advantages. Koppert Biological Systems distinguishes itself through expertise in biological control agents and pollination solutions, with a strong focus on greenhouse and high-value crop applications. The company's strategy emphasizes knowledge transfer and farmer education alongside product sales. Valent BioSciences LLC leverages its parent company's pharmaceutical research capabilities to develop advanced biological products, focusing on fermentation-based solutions and integrated pest management approaches. These companies, along with others like Biolchim S.p.A. and Certis U.S.A. LLC, are shaping the market through different strategic focuses ranging from broad-spectrum solutions to specialized applications.

Porter's Five Forces Analysis of the Agricultural Biological Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the agricultural biological market. The threat of new entrants is moderate to high, as the market attracts both established agrochemical companies and innovative startups, though significant barriers exist in terms of research and development costs, regulatory approvals, and distribution networks. Bargaining power of suppliers is relatively low due to the diverse sources of biological materials and the availability of synthetic alternatives, though specialized microbial strains may command premium prices. Buyer power is moderate, with large-scale commercial farmers having significant influence on pricing and product features, while smallholder farmers have limited bargaining power but represent substantial market volume. The threat of substitutes is high, as biological products compete directly with conventional chemical alternatives, though growing environmental concerns and regulatory pressures are reducing the attractiveness of chemical substitutes. Competitive rivalry is intense, characterized by price competition, product differentiation efforts, and strategic partnerships. Companies compete on efficacy, stability, ease of use, and integration with existing farming practices. The market also faces potential disruption from technological innovations in areas such as synthetic biology and precision application technologies, which could fundamentally alter competitive dynamics and create new entry opportunities.

SWOT Analysis of the Agricultural Biological Market - Strengths, weaknesses, opportunities, threats

The agricultural biological market presents a complex SWOT profile reflecting both its potential and challenges. Strengths include growing environmental awareness and regulatory support for sustainable agriculture, which create favorable market conditions for biological products. The technology's ability to improve soil health and reduce chemical residues aligns well with consumer preferences for sustainable food production. Additionally, the market benefits from increasing research and development investments that are improving product efficacy and stability. Weaknesses encompass the relatively high costs of biological products compared to conventional alternatives, limited shelf life requiring specialized storage and handling, and inconsistent performance under varying environmental conditions. The market also faces challenges related to farmer education and the need for technical expertise in application. Opportunities abound in emerging markets where agricultural modernization is creating demand for sustainable inputs, in developing next-generation biological products with enhanced performance characteristics, and in integrating biological solutions with digital farming technologies. Threats include potential regulatory changes that could affect product approval processes, competition from conventional chemical products that continue to improve their environmental profiles, and economic pressures that may lead farmers to prioritize short-term costs over long-term sustainability benefits.

Agricultural Biological Market Value Chain Analysis - Industry structure and value flow

The agricultural biological market value chain encompasses multiple stages from research and development through to end-user application. The chain begins with raw material suppliers providing biological materials such as microbial strains, plant extracts, and other natural sources. These materials flow to manufacturers who combine them with formulation technologies to create stable, effective products. Research institutions and biotechnology companies play a crucial role in developing new biological strains and improving existing formulations. Distributors and dealers form the next link, responsible for getting products to farmers through various channels including direct sales, agricultural cooperatives, and retail outlets. Service providers including technical advisors, application specialists, and digital platform operators support the value chain by providing expertise in product selection, application timing, and integration with other farming practices. End-users, primarily farmers, represent the final link where biological products are applied to crops. The value chain is characterized by significant knowledge requirements at multiple stages, particularly in ensuring product stability, maintaining cold chain logistics where necessary, and providing technical support for optimal application. Value addition occurs throughout the chain, with research and development creating new product capabilities, formulation improvements enhancing product stability and efficacy, and technical support ensuring proper application and maximum benefit realization.

Key Investment Insights in the Agricultural Biological Market - Strategic investment recommendations

Investment opportunities in the agricultural biological market are shaped by several key factors that influence potential returns and risk profiles. Strategic investors should consider focusing on companies with strong research and development capabilities, as innovation remains a critical differentiator in this market. Companies developing proprietary microbial strains or advanced formulation technologies offer particularly attractive investment prospects due to their potential for sustainable competitive advantages. Geographic expansion represents another key investment theme, with emerging markets showing high growth potential despite higher initial risks related to infrastructure and market development. Vertical integration strategies, where companies control multiple stages of the value chain from research through distribution, can provide investment stability and margin advantages. Investors should also consider the growing importance of digital integration, with companies combining biological products with data analytics and precision application technologies likely to capture premium market positions. Strategic partnerships between biological companies and established agricultural input providers represent attractive investment opportunities, as these collaborations can accelerate market access and product development. However, investors should be aware of regulatory risks, particularly in regions with complex approval processes for biological products, and the potential for market consolidation that could affect smaller company valuations.

Agricultural Biological Market Conclusion - Summary and key takeaways

The agricultural biological market stands at a pivotal juncture, characterized by strong growth projections, increasing technological sophistication, and expanding market acceptance. The market's trajectory from $15.78 billion to $34.99 billion by 2033, representing a 12.05% CAGR, reflects fundamental shifts in agricultural practices toward sustainability and environmental responsibility. Key takeaways include the market's diverse segmentation opportunities across product types, crop applications, and geographic regions, each presenting unique growth dynamics and investment potential. The competitive landscape continues to evolve through consolidation and innovation, with both established agrochemical companies and specialized biological firms playing crucial roles. Regional variations in adoption rates highlight the importance of localized strategies and solutions tailored to specific agricultural contexts and regulatory environments. The market's future success will depend on addressing current challenges related to product stability, efficacy consistency, and farmer education while capitalizing on opportunities in emerging markets and technological advancements. As sustainability imperatives intensify and regulatory pressures on chemical inputs increase, agricultural biologicals are positioned to play an increasingly central role in global food production systems, offering solutions that balance productivity with environmental stewardship.

Research Methodology - How this research was conducted

This comprehensive market research was conducted using a rigorous methodology combining multiple data collection and analysis approaches. Primary research formed the foundation, involving interviews with industry experts, company executives, and agricultural professionals to gather firsthand insights about market trends, challenges, and opportunities. Secondary research complemented primary findings through analysis of company annual reports, industry publications, government agricultural statistics, and scientific literature on biological crop inputs. Market size and growth projections were developed using both top-down and bottom-up approaches, triangulating data from multiple sources to ensure accuracy. Segmentation analysis incorporated detailed examination of product categories, application methods, and regional variations, with data validated through cross-referencing with industry databases and expert consultations. Competitive landscape analysis involved profiling major companies based on their market presence, product portfolios, strategic initiatives, and financial performance where available. The research methodology also included analysis of regulatory frameworks across different regions, technological trends in biological product development, and economic factors influencing market dynamics. All findings underwent rigorous quality checks and validation processes to ensure reliability and relevance for stakeholders across the agricultural biological value chain.

Research Scope - Coverage and limitations

This research provides comprehensive coverage of the global agricultural biological market, encompassing biopesticides, biostimulants, and biofertilizers across major crop categories and geographic regions. The scope includes detailed analysis of market size, growth projections, competitive landscape, and key trends shaping the industry from 2025 through 2032. Coverage extends to major market segments including product types (biopesticides, biostimulants, biofertilizers), sources (microbial, biochemical), applications (cereals and grains, oilseeds and pulses, fruits and vegetables), and application modes (foliar sprays, soil treatment, seed treatment). Geographic coverage includes North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with detailed regional analysis of market dynamics and growth opportunities. The research also examines key companies operating in the market, their strategies, and recent developments. However, limitations exist in terms of data availability for certain emerging markets where agricultural biological adoption is still developing, and the rapidly evolving nature of biological product technologies may affect long-term projections. Additionally, while the research provides comprehensive market analysis, it does not cover detailed financial modeling for individual companies or specific investment recommendations beyond general market insights.

Key Companies and Recent Developments in the Agricultural Biological Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The agricultural biological market features several key companies driving innovation and market expansion through strategic initiatives. BASF SE recently announced the expansion of its biological portfolio with new microbial-based solutions for crop protection, focusing on enhanced efficacy and broader application windows. The company has also formed partnerships with digital agriculture platforms to integrate biological products with precision farming technologies. Syngenta has launched several new biological products targeting high-value crops, including advanced biostimulants that improve stress tolerance and yield stability. The company's recent strategic development includes establishing regional biological research centers to develop locally adapted solutions. Marrone Bio Innovations continues to strengthen its market position through the launch of novel botanical-based biopesticides with improved residual activity and expanded crop compatibility. Koppert Biological Systems has announced partnerships with greenhouse automation companies to integrate biological control solutions with climate management systems, enhancing pest management efficiency. Valent BioSciences LLC has expanded its fermentation-based product line with new products offering broader spectrum activity and improved application flexibility. These companies, along with others like Biolchim S.p.A. and Certis U.S.A. LLC, are actively pursuing mergers and acquisitions to strengthen their biological portfolios, with recent notable acquisitions including smaller innovative companies with specialized technologies in microbial discovery and formulation development.