Surgical Robots Market Overview - Definition, scope, and significance

Surgical robots are advanced medical devices that assist surgeons in performing complex procedures with enhanced precision, flexibility, and control. These systems combine robotic technology with computer-assisted surgical systems to enable minimally invasive procedures across various medical specialties. The scope of the surgical robots market encompasses robotic surgical systems, instruments and accessories, and related services. This market is significant because it represents a transformative shift in healthcare delivery, enabling procedures that were previously impossible or highly risky, reducing patient recovery times, minimizing surgical complications, and improving overall healthcare outcomes. The technology addresses critical healthcare challenges including aging populations, rising surgical volumes, and the growing demand for minimally invasive procedures.

Surgical Robots Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The surgical robots market is primarily driven by the increasing adoption of minimally invasive surgeries, technological advancements in robotic systems, rising healthcare expenditure, and growing geriatric population requiring surgical interventions. The expanding applications of robotic surgery across multiple specialties and the improving accuracy and precision of robotic systems further accelerate market growth. However, the market faces restraints including high costs of robotic systems and procedures, limited reimbursement policies in certain regions, and the need for specialized training for surgeons. Key challenges include the integration of robotic systems with existing hospital infrastructure, regulatory compliance requirements, and the initial resistance from traditional surgical practitioners. Opportunities exist in emerging markets with improving healthcare infrastructure, the development of AI-powered robotic systems, expansion into new surgical applications, and the growing trend of remote surgery capabilities.

Surgical Robots Market Growth Trends - Current and emerging trends shaping the market

The surgical robots market is experiencing several transformative growth trends. The integration of artificial intelligence and machine learning capabilities is enhancing robotic precision and decision-making during procedures. There is a notable shift toward miniaturized robotic systems that can access smaller surgical sites with greater accuracy. The market is witnessing increased adoption of 5G technology to enable real-time data transmission and potentially facilitate remote robotic surgeries. Another emerging trend is the development of modular robotic systems that offer greater flexibility and cost-effectiveness. The industry is also seeing a rise in collaborative robots that work alongside human surgeons rather than replacing them entirely. Additionally, there is growing interest in developing robotic systems specifically designed for outpatient and ambulatory surgical centers, expanding the accessibility of robotic-assisted procedures beyond traditional hospital settings.

COVID-19 Impact on the Surgical Robots Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the surgical robots market as hospitals postponed elective procedures and focused resources on pandemic response. Supply chain disruptions affected the manufacturing and delivery of robotic systems, while social distancing requirements temporarily limited training programs for surgeons. However, the pandemic also accelerated certain trends in the market, including the adoption of telemedicine and remote surgical consultations. As healthcare systems recover, the market is experiencing a rebound driven by the backlog of postponed procedures and renewed focus on healthcare modernization. The pandemic highlighted the importance of minimally invasive procedures that reduce hospital stays and potential exposure risks, potentially benefiting the long-term adoption of surgical robots. The recovery trajectory shows strong growth as hospitals reinvest in advanced surgical technologies and the backlog of elective procedures is addressed.

Surgical Robots Market Competitive Landscape - Major competitors and market consolidation

The surgical robots market features a mix of established medical device giants and specialized robotic surgery companies competing for market share. The competitive landscape is characterized by intense R&D investments, strategic partnerships, and mergers and acquisitions. Key players are focusing on expanding their product portfolios, enhancing technological capabilities, and securing regulatory approvals in new regions. Market consolidation is evident through strategic collaborations between robotic surgery companies and healthcare providers, as well as acquisitions of innovative startups by larger corporations. The competitive dynamics are shaped by factors such as technological differentiation, pricing strategies, after-sales service quality, and the strength of clinical evidence supporting different systems. Companies are also competing on the breadth of their surgical applications and the comprehensiveness of their training and support programs for healthcare institutions.

Executive Summary - High-level overview and key findings about Surgical Robots Market

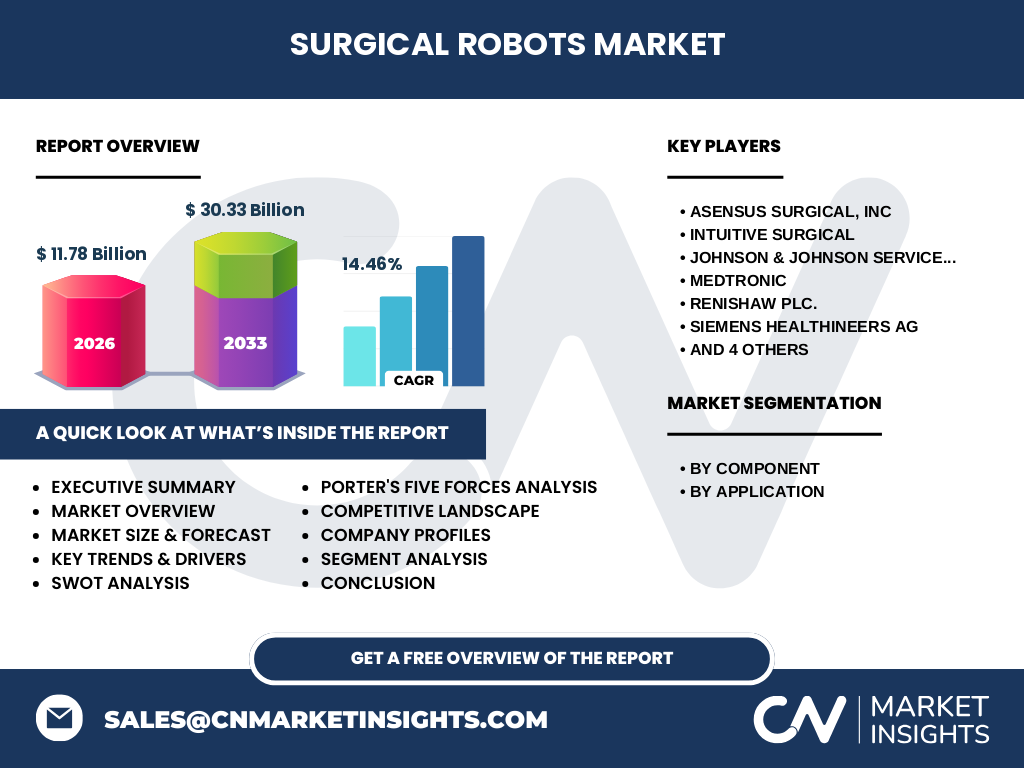

The surgical robots market represents a dynamic and rapidly evolving segment of the medical device industry, characterized by technological innovation and expanding clinical applications. The market is experiencing robust growth driven by the increasing demand for minimally invasive procedures, technological advancements, and the expanding geriatric population requiring surgical interventions. Key findings indicate strong market potential across multiple surgical specialties, with particular growth in urological, orthopedic, and general surgery applications. The competitive landscape features both established medical device companies and specialized robotic surgery firms, with innovation being a critical differentiator. The market faces challenges related to high costs and the need for specialized training, but opportunities abound in emerging markets and new technological developments. Overall, the surgical robots market is positioned for significant expansion, with a projected CAGR of 14.46% from 2027 to 2033, reflecting the transformative impact of robotic-assisted surgery on healthcare delivery.

Surgical Robots Market Forecast - Projections for 2025-2032 period

The surgical robots market is projected to experience substantial growth during the 2025-2032 period, with the market size expected to increase from 11.78 billion in 2026 to 30.33 billion by 2033. This represents a compound annual growth rate of 14.46%, indicating strong market momentum. The forecast is driven by several factors including the continued expansion of robotic surgery applications, technological advancements improving system capabilities and reducing costs, and the increasing adoption of robotic systems in emerging markets. The growth trajectory suggests that the market will continue to benefit from the rising demand for minimally invasive procedures, the aging global population requiring more surgical interventions, and the ongoing healthcare modernization efforts in developing regions. The forecast period is expected to see increased market penetration in previously underserved regions and the emergence of new applications for robotic surgery technology.

Surgical Robots Market Size and Share by Segmentation - Breakdown by {segmentData}

The surgical robots market is segmented by component and application, each showing distinct growth patterns and market dynamics. By component, the market includes Instruments & Accessories, Robotic Systems, and Services. Robotic Systems currently represent the largest segment due to the high cost of surgical robot platforms, while Instruments & Accessories show strong recurring revenue potential through disposable components. The Services segment is growing as hospitals require ongoing maintenance, training, and support. By application, the market spans Urological Surgery, Orthopedic Surgery, General Surgery, Gynecological Surgery, Cardiothoracic Surgery, and Neurosurgery. Urological and gynecological surgeries currently represent the largest application segments due to the established use of robotic systems in these procedures, while orthopedic and neurosurgery applications are experiencing the fastest growth rates as robotic technology proves its value in these complex procedures. The segmentation analysis reveals that while all segments are growing, the rate of adoption and market share varies significantly by application type and geographic region.

Global Surgical Robots Market Size and Share by Region - Geographic distribution

The global surgical robots market exhibits varying adoption rates and growth patterns across different regions, reflecting differences in healthcare infrastructure, economic development, and regulatory environments. North America currently dominates the market, driven by advanced healthcare systems, high healthcare expenditure, and early adoption of innovative technologies. Europe represents the second-largest market, with strong growth in countries with robust public healthcare systems. The Asia-Pacific region is experiencing the fastest growth rate, fueled by improving healthcare infrastructure, rising disposable incomes, and increasing awareness of robotic surgery benefits. Latin America and the Middle East & Africa regions are also showing growth potential, though at a slower pace due to economic constraints and developing healthcare systems. The regional distribution analysis indicates that while developed markets continue to expand through technological advancements and new applications, emerging markets present significant growth opportunities as healthcare infrastructure improves and awareness increases.

Regional Analysis of the Surgical Robots Market - Detailed regional market performance

Regional analysis of the surgical robots market reveals distinct market characteristics and growth drivers across different geographic areas. In North America, particularly the United States, the market benefits from favorable reimbursement policies, high healthcare spending, and a strong culture of technological adoption in healthcare. European markets show steady growth with significant variations between Western and Eastern European countries, where healthcare system maturity and economic factors influence adoption rates. The Asia-Pacific region presents a diverse landscape, with countries like Japan and South Korea leading in adoption due to their advanced healthcare systems, while China and India offer substantial growth potential as their healthcare infrastructure develops. Japan's aging population creates unique demand for robotic surgery, while China's large population and improving healthcare access drive market expansion. Latin American markets are characterized by growing middle-class populations and increasing healthcare investments, particularly in Brazil and Mexico. The Middle East shows strong growth in countries like the UAE and Saudi Arabia, where healthcare modernization initiatives are driving technology adoption.

Leading Company Profiles in the Surgical Robots Market - Industry players and strategies

The surgical robots market features several prominent companies with distinct strategic approaches and technological capabilities. Intuitive Surgical has established itself as a market leader through its da Vinci Surgical System, focusing on continuous innovation and expanding applications. Medtronic has entered the market with its Hugo platform, leveraging its extensive medical device experience and global distribution network. Johnson & Johnson Services, Inc is developing the Ottava system, emphasizing user-friendly design and versatility. Stryker and Zimmer Biomet are focusing on orthopedic surgical robots, leveraging their expertise in joint replacement procedures. THINK Surgical specializes in orthopedic applications with its TMINI and TSolution One systems. Asensus Surgical, Inc is developing AI-enhanced robotic systems with its Senhance platform. Renishaw plc focuses on neurosurgery applications, while Siemens Healthineers AG and Smith + Nephew are expanding their presence through strategic acquisitions and partnerships. These companies are pursuing various strategies including technological differentiation, expanding into new surgical specialties, and developing cost-effective solutions for emerging markets.

Porter's Five Forces Analysis of the Surgical Robots Market - Competitive forces assessment

Porter's Five Forces analysis of the surgical robots market reveals the competitive dynamics shaping the industry. The threat of new entrants is moderate due to high R&D costs, regulatory requirements, and the need for extensive clinical validation, though specialized startups continue to emerge. Bargaining power of suppliers is relatively low as companies can source components from multiple suppliers and develop proprietary technologies. The bargaining power of buyers (hospitals and surgical centers) is increasing as they become more informed and demand better pricing and service agreements. The threat of substitutes is moderate, as traditional laparoscopic and open surgical methods remain viable alternatives, though robotic surgery's advantages continue to reduce this threat. Competitive rivalry is intense among established players, characterized by rapid technological innovation, price competition, and the race to expand into new applications and geographic markets. The analysis suggests that while barriers to entry are significant, the market remains dynamic with ongoing competitive pressures driving innovation and cost optimization.

SWOT Analysis of the Surgical Robots Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the surgical robots market reveals key strategic insights. Strengths include the proven clinical benefits of robotic surgery, continuous technological advancements, and strong intellectual property portfolios held by leading companies. The market also benefits from growing surgeon expertise and expanding clinical evidence supporting robotic procedures. Weaknesses include the high costs of systems and procedures, the learning curve for surgeons, and the need for specialized infrastructure. Opportunities abound in emerging markets, the development of AI-enhanced systems, expansion into new surgical specialties, and the potential for remote surgery applications. Threats include potential regulatory changes, economic downturns affecting healthcare spending, and the emergence of alternative technologies that could disrupt the market. The analysis indicates that while the market faces certain challenges, its strengths and opportunities position it for continued growth, particularly as technological barriers decrease and applications expand.

Surgical Robots Market Value Chain Analysis - Industry structure and value flow

The surgical robots market value chain encompasses several interconnected stages from research and development through to end-user application. The chain begins with component suppliers providing sensors, actuators, and other critical parts. These components are integrated by robotic system manufacturers who develop the surgical platforms through extensive R&D efforts. The manufacturing stage involves precision assembly and rigorous quality control processes. Distributors and direct sales teams then deliver the systems to hospitals and surgical centers. Training providers play a crucial role in educating surgeons and operating room staff on system usage. Healthcare providers integrate the systems into their surgical programs and conduct procedures. Finally, post-market surveillance and ongoing support services ensure system performance and safety. The value chain also includes regulatory bodies that oversee approvals and standards organizations that establish safety guidelines. This analysis reveals that success in the market requires excellence across multiple value chain stages, with particular emphasis on R&D, clinical validation, and after-sales support.

Key Investment Insights in the Surgical Robots Market - Strategic investment recommendations

Investment insights in the surgical robots market indicate several strategic opportunities for stakeholders. Companies should prioritize R&D investments in AI and machine learning capabilities to enhance system intelligence and automation. There is strong potential for investment in miniaturized robotic systems that can access smaller surgical sites and reduce costs. Emerging markets represent attractive investment opportunities, particularly in Asia-Pacific and Latin America, where healthcare infrastructure is improving. Investors should consider the growing trend toward specialized robotic systems for specific surgical procedures rather than general-purpose platforms. Strategic partnerships between robotic surgery companies and healthcare providers can create value through shared investment in infrastructure and joint clinical studies. Additionally, investments in training and education programs for surgeons will be critical as the technology continues to evolve. The market also presents opportunities for vertical integration, with some companies expanding into adjacent areas such as preoperative planning software and postoperative monitoring systems.

Surgical Robots Market Conclusion - Summary and key takeaways

The surgical robots market represents a transformative force in modern healthcare, characterized by robust growth, technological innovation, and expanding clinical applications. With a projected market size increase from 11.78 billion in 2026 to 30.33 billion by 2033, representing a CAGR of 14.46%, the market demonstrates strong momentum and significant potential. Key takeaways include the market's resilience despite initial pandemic disruptions, the ongoing shift toward minimally invasive procedures, and the critical role of technological advancement in driving adoption. The competitive landscape features both established medical device giants and specialized robotic surgery companies, with innovation and strategic partnerships being key differentiators. While challenges exist in terms of costs and training requirements, the market's strengths in clinical outcomes and expanding applications position it for continued growth. The analysis suggests that stakeholders who focus on technological advancement, emerging market expansion, and strategic partnerships will be best positioned to capitalize on the market's growth trajectory.

Research Methodology - How this research was conducted

The research methodology for this surgical robots market analysis employed a comprehensive approach combining primary and secondary research methods. Primary research included interviews with industry experts, surgeons, hospital administrators, and company executives to gather firsthand insights on market trends, challenges, and opportunities. Secondary research involved extensive review of industry reports, company financial statements, regulatory filings, clinical studies, and market databases. The analysis incorporated both top-down and bottom-up approaches to validate market size estimates and growth projections. Data triangulation was used to cross-verify information from multiple sources, ensuring accuracy and reliability. The research methodology also included competitive analysis frameworks and trend assessment models to provide a holistic view of the market. Geographic segmentation was analyzed using regional healthcare expenditure data, regulatory environments, and adoption rates of medical technologies. The methodology was designed to provide actionable insights while acknowledging the limitations of available public data and the rapidly evolving nature of the surgical robots market.

Research Scope - Coverage and limitations

The research scope for this surgical robots market analysis encompasses the global market for surgical robotic systems, instruments and accessories, and related services from 2025 to 2032. The coverage includes major geographic regions (North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa), key market segments by component and application, and profiles of leading companies in the industry. The analysis focuses on commercially available robotic surgical systems and excludes experimental or research-stage technologies. Limitations of the research include the availability of public data for certain emerging markets, the rapidly changing competitive landscape due to ongoing mergers and acquisitions, and the challenge of quantifying certain market factors such as the impact of regulatory changes or economic fluctuations. The scope also acknowledges that technological advancements may create new market segments or applications not currently included in the analysis. Despite these limitations, the research provides a comprehensive overview of the market based on available data and industry expertise.

Key Companies and Recent Developments in the Surgical Robots Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The surgical robots market features several key companies driving innovation and market growth through recent developments. Intuitive Surgical continues to expand its da Vinci system's capabilities with new instrument launches and enhanced visualization technologies. Medtronic has announced regulatory approvals for its Hugo™ robotic-assisted surgery (RAS) system in multiple markets, marking its entry into the competitive landscape. Johnson & Johnson Services, Inc has unveiled the Ottava™ system, emphasizing its modular design and user-friendly interface. Stryker has strengthened its orthopedic robotics portfolio through strategic acquisitions and the launch of next-generation systems. Zimmer Biomet has introduced advanced planning software integration with its ROSA™ and Rosa One™ systems. THINK Surgical has announced expanded applications for its TMINI™ system in various orthopedic procedures. Asensus Surgical, Inc has secured additional funding to advance its AI-enhanced Senhance® platform development. Renishaw plc has announced partnerships with neurosurgery centers to validate its robotic systems for brain surgery applications. Siemens Healthineers AG has unveiled plans for integrated imaging and robotic surgery solutions. These developments reflect the industry's focus on technological advancement, application expansion, and strategic positioning in an increasingly competitive market.