Ovarian Cancer Drugs Market Overview - Definition, scope, and significance

The Ovarian Cancer Drugs Market encompasses pharmaceutical products designed for the treatment of ovarian cancer, a malignancy affecting the ovaries in women. This market includes various drug classes such as PARP inhibitors, anti-angiogenesis inhibitors, and chemotherapy agents targeting different types of ovarian cancer including epithelial ovarian cancer, germ cell ovarian cancer, and stromal tumors. The significance of this market lies in its critical role in addressing a life-threatening disease that ranks as the fifth leading cause of cancer deaths among women, with approximately 21,000 new cases diagnosed annually in the United States alone. The market serves a pressing healthcare need given the high mortality rate associated with ovarian cancer and the continuous demand for more effective treatment options.

Ovarian Cancer Drugs Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the Ovarian Cancer Drugs Market include the increasing incidence of ovarian cancer globally, rising awareness about early detection, and advancements in targeted therapies that offer improved efficacy and reduced side effects. The growing geriatric population, which is more susceptible to cancer, also contributes to market expansion. However, the market faces several restraints including the high cost of novel therapies, particularly PARP inhibitors, which can limit accessibility in developing regions. Challenges include the complex nature of ovarian cancer with multiple subtypes requiring different treatment approaches, and the development of drug resistance over time. Opportunities exist in the form of emerging markets with improving healthcare infrastructure, the potential for combination therapies that enhance treatment outcomes, and the ongoing research into personalized medicine approaches that could revolutionize treatment protocols.

Ovarian Cancer Drugs Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the Ovarian Cancer Drugs Market are characterized by a shift toward targeted therapies and immunotherapy approaches, moving away from traditional chemotherapy regimens. The market is witnessing increased investment in research and development for next-generation PARP inhibitors with improved efficacy and reduced resistance mechanisms. Another significant trend is the growing adoption of combination therapies that integrate different drug classes to enhance treatment outcomes. The market is also experiencing a trend toward personalized medicine, where treatment decisions are based on specific genetic markers and tumor characteristics. Additionally, there is a growing emphasis on developing drugs that can address platinum-resistant ovarian cancer, a particularly challenging form of the disease. The increasing collaboration between pharmaceutical companies and research institutions is accelerating the pace of drug development and bringing innovative therapies to market more quickly.

COVID-19 Impact on the Ovarian Cancer Drugs Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a multifaceted impact on the Ovarian Cancer Drugs Market. Initially, the market experienced disruptions due to delayed clinical trials, interrupted supply chains, and reduced patient access to healthcare facilities as resources were redirected to pandemic response. Many routine cancer screenings and treatments were postponed, potentially affecting early diagnosis rates. However, the market demonstrated resilience as healthcare systems adapted to new protocols and telemedicine became more widely adopted for patient monitoring. The pandemic also accelerated certain trends, including the adoption of digital health technologies and the prioritization of research funding for critical healthcare needs. As the world recovers from the pandemic, the market is showing signs of recovery with renewed focus on cancer research, resumption of clinical trials, and increased healthcare spending. The experience gained during the pandemic has also led to improved preparedness for future healthcare challenges.

Ovarian Cancer Drugs Market Competitive Landscape - Major competitors and market consolidation

The Ovarian Cancer Drugs Market features a competitive landscape with several major pharmaceutical companies vying for market share through innovative drug development and strategic partnerships. Key players include AstraZeneca, Roche (GeneTech), GSK, and Eli Lilly, among others, each bringing unique strengths to the market. The competitive environment is characterized by intense research and development activities, with companies racing to develop more effective therapies and gain regulatory approvals. Market consolidation is occurring through mergers, acquisitions, and licensing agreements as companies seek to strengthen their product portfolios and expand their geographic presence. The competition is particularly fierce in the PARP inhibitors segment, where multiple companies are developing next-generation drugs with improved efficacy. Companies are also competing on the basis of pricing strategies, with some offering patient assistance programs to improve drug accessibility.

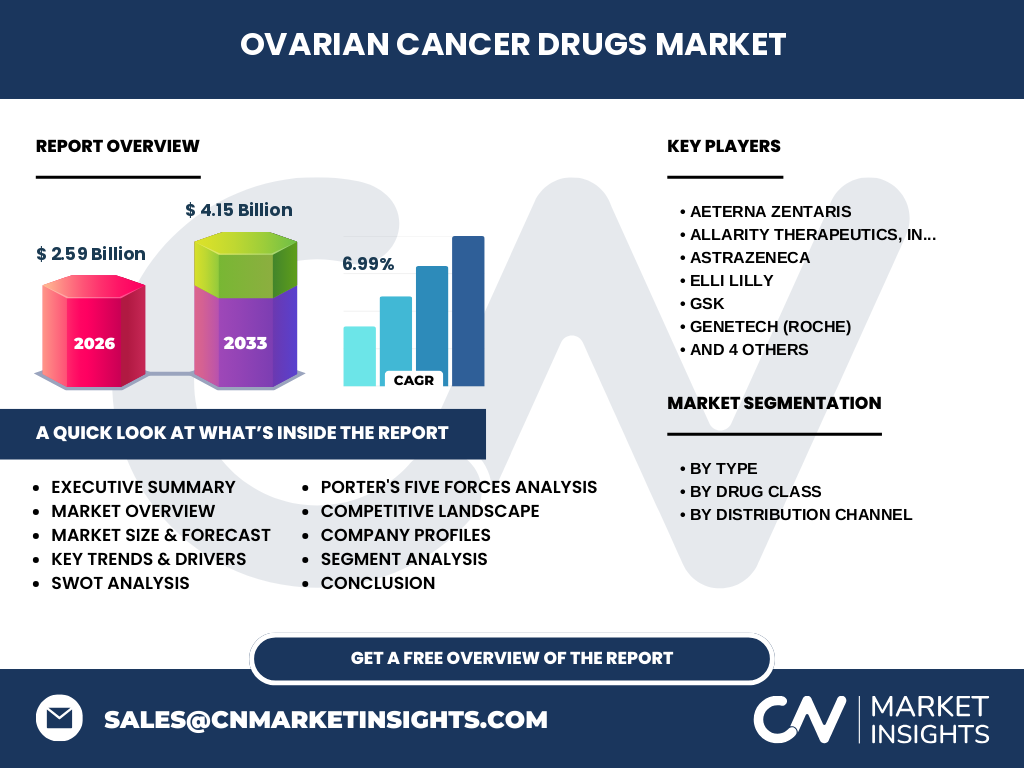

Executive Summary - High-level overview and key findings about Ovarian Cancer Drugs Market

The Ovarian Cancer Drugs Market represents a critical segment of oncology pharmaceuticals, addressing a significant unmet medical need with a market size of 2.59 billion in 2026 and projected to reach 4.15 billion by 2033, growing at a CAGR of 6.99%. The market is characterized by ongoing innovations in targeted therapies, particularly PARP inhibitors and anti-angiogenesis agents, which are transforming treatment paradigms. Key findings indicate that the market is driven by increasing cancer incidence, aging populations, and technological advancements in drug development. The competitive landscape is dynamic, with major pharmaceutical companies investing heavily in R&D to gain market advantage. Distribution channels are evolving, with hospital pharmacies maintaining dominance while retail pharmacies are gaining traction. The market faces challenges including high treatment costs and drug resistance, but opportunities exist in emerging markets and combination therapy approaches. Overall, the market demonstrates strong growth potential with continuous innovations shaping its future trajectory.

Ovarian Cancer Drugs Market Forecast - Projections for 2025-2032 period

The Ovarian Cancer Drugs Market is projected to experience steady growth from 2025 to 2032, with the market expanding from its 2026 size of 2.59 billion to reach 4.15 billion by 2033. This represents a compound annual growth rate of 6.99% over the forecast period. The growth trajectory is supported by several factors including the continued development of novel therapies, increasing global cancer prevalence, and expanding healthcare access in emerging markets. The PARP inhibitors segment is expected to maintain strong growth due to their effectiveness in treating BRCA-mutated ovarian cancer. Anti-angiogenesis inhibitors are also projected to see significant adoption as combination therapies become more prevalent. The market forecast indicates particularly strong growth in regions with improving healthcare infrastructure and increasing healthcare expenditure. However, growth may be tempered by pricing pressures and the need for cost-effective treatment solutions. Overall, the forecast suggests a robust and expanding market with opportunities for both established players and new entrants.

Ovarian Cancer Drugs Market Size and Share by Segmentation - Breakdown by {segmentData}

The Ovarian Cancer Drugs Market can be segmented by type, drug class, and distribution channel. By type, epithelial ovarian cancer represents the largest segment due to its higher prevalence, accounting for approximately 85-90% of all ovarian cancer cases. Germ cell ovarian cancer and stromal tumors represent smaller but significant segments with distinct treatment requirements. By drug class, PARP inhibitors have emerged as a dominant category, driven by their effectiveness in treating BRCA-mutated cancers and their expanding indications. Anti-angiogenesis inhibitors represent another substantial segment, particularly for recurrent ovarian cancer. In terms of distribution channels, hospital pharmacies currently hold the largest market share due to the specialized nature of cancer treatment and the need for professional medical supervision. Retail pharmacies are gaining market share, particularly for maintenance therapies and supportive care medications. The segmentation analysis reveals that targeted therapies, particularly PARP inhibitors, are driving market growth across all segments.

Global Ovarian Cancer Drugs Market Size and Share by Region - Geographic distribution

The global Ovarian Cancer Drugs Market exhibits varying dynamics across different geographic regions. North America currently dominates the market, accounting for the largest share due to advanced healthcare infrastructure, high healthcare expenditure, and the presence of major pharmaceutical companies. Europe represents the second-largest market, driven by strong research initiatives and comprehensive healthcare systems. The Asia-Pacific region is emerging as the fastest-growing market, with increasing cancer incidence, improving healthcare access, and growing economic development driving expansion. Latin America and the Middle East & Africa represent smaller but growing markets, with increasing awareness about ovarian cancer and improving healthcare infrastructure contributing to market growth. The regional distribution reflects disparities in healthcare access, economic development, and cancer awareness, with developed regions maintaining larger market shares while emerging regions show the highest growth potential.

Regional Analysis of the Ovarian Cancer Drugs Market - Detailed regional market performance

Regional analysis of the Ovarian Cancer Drugs Market reveals distinct patterns of market development and growth potential across different geographic areas. In North America, particularly the United States, the market benefits from advanced research capabilities, high healthcare spending, and favorable reimbursement policies, resulting in early adoption of novel therapies. Europe demonstrates strong market performance with countries like Germany, France, and the UK leading in terms of research and development activities and patient access to innovative treatments. The Asia-Pacific region shows the most dynamic growth, with countries like China, Japan, and South Korea investing heavily in healthcare infrastructure and cancer research. However, the region faces challenges including varying levels of healthcare access across countries. Latin America presents opportunities for market expansion, particularly in Brazil and Mexico, where improving economic conditions are driving healthcare investment. The Middle East & Africa region, while currently representing a smaller market share, shows potential for growth as healthcare systems develop and awareness about ovarian cancer increases.

Leading Company Profiles in the Ovarian Cancer Drugs Market - Industry players and strategies

The Ovarian Cancer Drugs Market features several leading companies with distinct strategies and market positions. AstraZeneca has established itself as a key player through its PARP inhibitor portfolio, particularly with drugs like Lynparza, which has gained approval for multiple cancer indications. Roche (GeneTech) leverages its extensive research capabilities and global presence to develop innovative therapies, with a focus on combination approaches. GSK has strengthened its market position through strategic acquisitions and a robust pipeline of targeted therapies. Eli Lilly brings strong research expertise and has been expanding its oncology portfolio through both internal development and partnerships. Other notable players include ImmunoGen, known for its antibody-drug conjugates, and Allarity Therapeutics, which focuses on personalized medicine approaches. These companies employ various strategies including continuous R&D investment, strategic collaborations, geographic expansion, and patient assistance programs to maintain and enhance their market positions.

Porter's Five Forces Analysis of the Ovarian Cancer Drugs Market - Competitive forces assessment

Porter's Five Forces analysis of the Ovarian Cancer Drugs Market reveals a competitive landscape shaped by several key factors. The threat of new entrants is moderate due to the high barriers to entry, including substantial R&D costs, complex regulatory requirements, and the need for extensive clinical trial data. The bargaining power of buyers, primarily hospitals and healthcare providers, is moderate as they seek cost-effective solutions but are often limited by the specialized nature of cancer treatments. Suppliers, mainly raw material and contract manufacturing organizations, have relatively low bargaining power due to the availability of alternatives and the scale of pharmaceutical companies. The threat of substitutes is low as ovarian cancer treatments have limited alternatives, though research into alternative therapies continues. Competitive rivalry among existing players is high, characterized by intense R&D competition, patent races, and marketing efforts. Overall, the analysis suggests a market with high entry barriers but significant opportunities for established players who can navigate the complex competitive landscape.

SWOT Analysis of the Ovarian Cancer Drugs Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Ovarian Cancer Drugs Market reveals several key factors influencing its development. Strengths include the continuous innovation in targeted therapies, strong R&D capabilities of major pharmaceutical companies, and growing awareness about ovarian cancer leading to earlier diagnosis. The market also benefits from supportive regulatory environments in many countries and increasing healthcare expenditure. Weaknesses include the high cost of novel therapies, which can limit patient access, and the challenge of drug resistance developing over time. The complexity of ovarian cancer with multiple subtypes also presents treatment challenges. Opportunities exist in emerging markets with improving healthcare infrastructure, the potential for combination therapies to enhance efficacy, and the growing field of personalized medicine. Threats include pricing pressures from healthcare systems seeking cost containment, potential regulatory hurdles, and the risk of more effective competitive therapies emerging. The analysis suggests a market with significant potential but also notable challenges that need to be addressed.

Ovarian Cancer Drugs Market Value Chain Analysis - Industry structure and value flow

The value chain of the Ovarian Cancer Drugs Market encompasses several interconnected stages, each contributing to the delivery of effective treatments to patients. The chain begins with research and development, where pharmaceutical companies invest heavily in discovering and developing new drug candidates. This is followed by preclinical testing and clinical trials to establish safety and efficacy. Regulatory approval represents a critical stage, with companies navigating complex approval processes in different markets. Manufacturing involves the production of drugs at scale, often requiring specialized facilities and quality control measures. Distribution channels, primarily hospital and retail pharmacies, ensure drugs reach healthcare providers and patients. Healthcare providers, including oncologists and specialized cancer centers, administer treatments and monitor patient responses. Support services, such as patient assistance programs and education initiatives, complete the value chain by improving access and adherence. Each stage of the value chain presents opportunities for value creation and efficiency improvements, with companies increasingly focusing on streamlining processes to reduce costs and improve patient outcomes.

Key Investment Insights in the Ovarian Cancer Drugs Market - Strategic investment recommendations

Key investment insights for the Ovarian Cancer Drugs Market suggest several strategic opportunities for investors and companies. The PARP inhibitors segment represents a particularly attractive investment area, given its growing importance in treating BRCA-mutated ovarian cancer and its expanding indications. Investment in combination therapies, which pair different drug classes to enhance efficacy, is another promising area as this approach shows potential for improving treatment outcomes. The emerging markets, particularly in Asia-Pacific, offer significant growth potential due to improving healthcare infrastructure and increasing cancer prevalence. Companies focusing on personalized medicine approaches, which tailor treatments to individual patient characteristics, represent another strategic investment opportunity. Additionally, investments in technologies that improve drug delivery or reduce side effects could yield substantial returns. However, investors should be aware of the high R&D costs and regulatory risks inherent in pharmaceutical development. A diversified investment approach across different segments and geographic regions may help mitigate these risks while capitalizing on the market's growth potential.

Ovarian Cancer Drugs Market Conclusion - Summary and key takeaways

The Ovarian Cancer Drugs Market represents a critical and growing segment of the pharmaceutical industry, addressing a significant healthcare need with a market size of 2.59 billion in 2026 and projected to reach 4.15 billion by 2033. Key takeaways include the market's strong growth trajectory driven by continuous innovation in targeted therapies, particularly PARP inhibitors and anti-angiogenesis agents. The competitive landscape is dynamic, with major pharmaceutical companies investing heavily in R&D to gain market advantage. Regional variations exist, with North America and Europe currently dominating but Asia-Pacific showing the highest growth potential. The market faces challenges including high treatment costs and drug resistance, but opportunities abound in emerging markets, combination therapies, and personalized medicine approaches. Overall, the market demonstrates resilience and strong growth potential, supported by ongoing research efforts and increasing global awareness about ovarian cancer. Success in this market requires a strategic approach that balances innovation, cost-effectiveness, and accessibility to meet the diverse needs of patients worldwide.

Research Methodology - How this research was conducted

The research methodology for this Ovarian Cancer Drugs Market analysis employed a comprehensive approach combining both primary and secondary research methods. Primary research involved interviews with industry experts, including oncologists, pharmaceutical company representatives, and market analysts, to gather firsthand insights into market dynamics and emerging trends. Secondary research encompassed a thorough review of industry reports, scientific publications, company financial statements, and regulatory databases to validate market data and identify key developments. Market sizing was conducted using a bottom-up approach, analyzing data from various segments and regions to build a complete market picture. The research also utilized data triangulation to cross-verify information from multiple sources, ensuring accuracy and reliability. Forecasting was based on historical growth patterns, current market trends, and expert opinions about future developments. The methodology aimed to provide a balanced and comprehensive view of the market, acknowledging both the opportunities and challenges facing the industry.

Research Scope - Coverage and limitations

The research scope for this Ovarian Cancer Drugs Market analysis covers the period from 2025 to 2032, with a particular focus on the forecast period of 2027 to 2033. The analysis encompasses major geographic regions including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, providing a global perspective on market dynamics. The scope includes various market segments such as drug classes (PARP inhibitors, anti-angiogenesis inhibitors), cancer types (epithelial, germ cell, stromal tumors), and distribution channels (hospital and retail pharmacies). Key companies analyzed include major pharmaceutical players such as AstraZeneca, Roche, GSK, and Eli Lilly, among others. The research also covers market drivers, restraints, opportunities, and competitive landscape analysis. Limitations of the research include the availability of public data for certain regions, potential discrepancies in reporting standards across countries, and the inherent uncertainty in forecasting long-term market developments. Additionally, the rapidly evolving nature of pharmaceutical research means that some developments may occur outside the research timeline.

Key Companies and Recent Developments in the Ovarian Cancer Drugs Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Ovarian Cancer Drugs Market features several key companies driving innovation and market growth through strategic developments. AstraZeneca has made significant strides with its PARP inhibitor Lynparza, which recently received expanded indications for maintenance treatment in advanced ovarian cancer. The company has also announced partnerships to explore combination therapies, enhancing its market position. Roche (GeneTech) continues to strengthen its portfolio through the development of novel antibody-drug conjugates and has announced collaborations with academic institutions to accelerate research in ovarian cancer treatments. GSK has focused on expanding its presence in emerging markets and recently launched a patient assistance program to improve drug accessibility. Eli Lilly has been active in acquiring promising drug candidates and has announced plans to invest in next-generation targeted therapies. ImmunoGen has gained attention for its antibody-drug conjugate approach and recently reported positive clinical trial results for its lead candidate. These companies, along with others like Allarity Therapeutics and Luye Pharma, are shaping the market through continuous innovation, strategic partnerships, and efforts to address unmet medical needs in ovarian cancer treatment.