North America Automotive Semiconductor Market Overview - Definition, scope, and significance

The North America Automotive Semiconductor Market encompasses the design, manufacturing, and distribution of semiconductor components specifically engineered for automotive applications across the United States, Canada, and Mexico. This market includes integrated circuits, sensors, microcontrollers, and other electronic components that power modern vehicles' advanced systems, from basic engine control units to sophisticated autonomous driving technologies. The significance of this market lies in its critical role in enabling vehicle electrification, connectivity, safety features, and the overall digital transformation of the automotive industry. As vehicles become increasingly software-defined and electronics-intensive, automotive semiconductors have emerged as essential enablers of innovation, performance, and functionality in modern transportation.

North America Automotive Semiconductor Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The North America Automotive Semiconductor Market is primarily driven by the accelerating adoption of electric vehicles, the proliferation of advanced driver assistance systems, and the increasing demand for vehicle connectivity and infotainment features. Government mandates for vehicle safety and emissions reduction, along with consumer preferences for technologically advanced vehicles, further propel market growth. However, the market faces restraints including supply chain disruptions, semiconductor shortages, and the high costs associated with advanced automotive electronics development. Challenges include the need for rigorous testing and validation to meet automotive quality standards, the complexity of integrating multiple semiconductor components, and the rapid pace of technological change requiring continuous innovation. Opportunities exist in the development of specialized semiconductors for autonomous vehicles, the expansion of electric vehicle infrastructure, and the growing aftermarket for automotive electronics upgrades and replacements.

North America Automotive Semiconductor Market Growth Trends - Current and emerging trends shaping the market

The North America Automotive Semiconductor Market is experiencing several transformative growth trends that are reshaping the industry landscape. The shift toward electric and hybrid vehicles is driving demand for power management semiconductors and battery management systems. The advancement of autonomous driving technologies is creating a need for high-performance processors, sensors, and AI accelerators. Vehicle-to-everything (V2X) communication is emerging as a key trend, requiring specialized semiconductors for seamless connectivity. The integration of artificial intelligence and machine learning in automotive applications is leading to the development of intelligent semiconductors capable of real-time data processing and decision-making. Additionally, the trend toward software-defined vehicles is increasing the demand for flexible, upgradable semiconductor solutions that can support over-the-air updates and feature enhancements throughout the vehicle's lifecycle.

COVID-19 Impact on the North America Automotive Semiconductor Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly disrupted the North America Automotive Semiconductor Market, causing production halts, supply chain bottlenecks, and a temporary decline in vehicle sales that directly impacted semiconductor demand. Factory closures and workforce limitations led to production delays and inventory shortages, while the global semiconductor shortage that followed the initial pandemic shock created severe constraints on automotive production capacity. However, the market demonstrated resilience through accelerated digital transformation initiatives and the prioritization of semiconductor manufacturing for critical automotive applications. The recovery trajectory shows a strong rebound as vehicle production resumes, with increased investments in semiconductor manufacturing capacity and a renewed focus on supply chain resilience. The pandemic has also accelerated certain trends, such as the adoption of electric vehicles and the integration of advanced connectivity features, creating new opportunities for semiconductor innovation and market expansion.

North America Automotive Semiconductor Market Competitive Landscape - Major competitors and market consolidation

The North America Automotive Semiconductor Market features a competitive landscape dominated by both established semiconductor giants and specialized automotive electronics suppliers. Major players such as Infineon Technologies, NXP Semiconductors, and Texas Instruments leverage their extensive experience in automotive-grade semiconductors to maintain strong market positions. The competitive dynamics are characterized by strategic partnerships between semiconductor manufacturers and automotive OEMs, vertical integration initiatives, and ongoing research and development investments to develop next-generation automotive semiconductor solutions. Market consolidation is evident through mergers, acquisitions, and collaborative ventures aimed at enhancing technological capabilities and expanding product portfolios. Competition is intensifying as new entrants from the technology sector, including companies like NVIDIA and Intel, expand their presence in automotive applications, bringing advanced computing capabilities and AI expertise to the market.

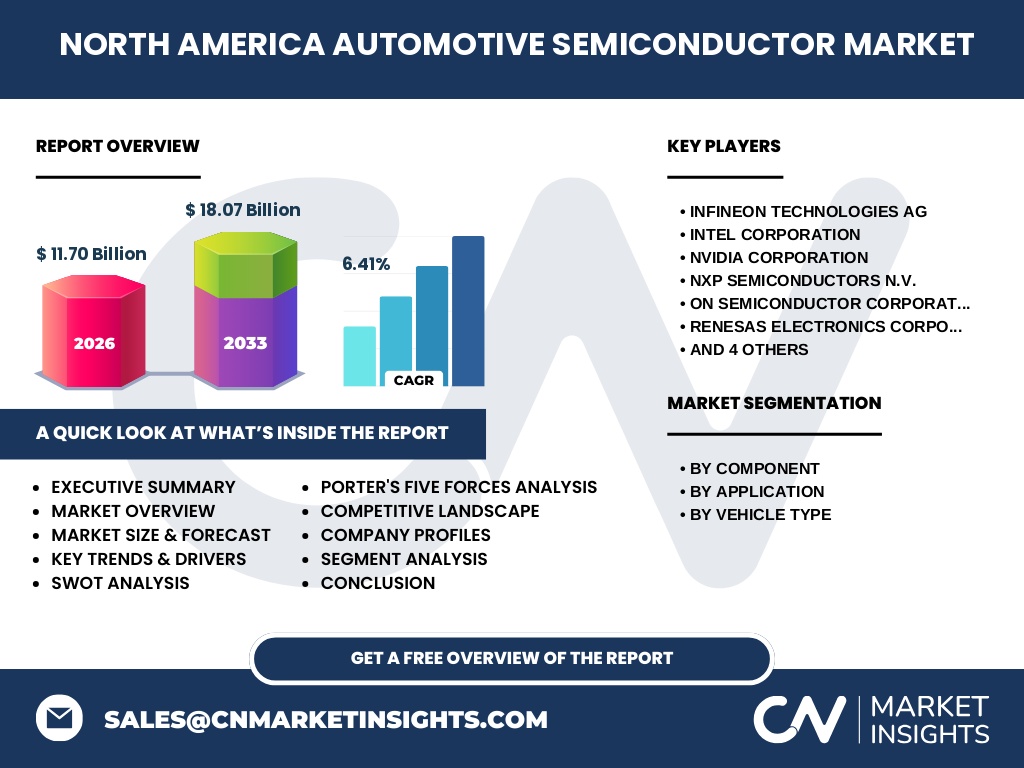

Executive Summary - High-level overview and key findings about North America Automotive Semiconductor Market

The North America Automotive Semiconductor Market is positioned for substantial growth, with the market size reaching 11.70 billion in 2026 and projected to expand to 18.07 billion by 2033, reflecting a robust CAGR of 6.41%. This growth is driven by the convergence of multiple technological and market forces, including the transition to electric vehicles, the advancement of autonomous driving capabilities, and the increasing integration of connected car technologies. The market demonstrates strong segmentation across components, applications, and vehicle types, with each segment presenting unique growth opportunities and challenges. Key findings indicate that microcontrollers and sensors represent significant growth areas, while applications in advanced driver assistance systems and powertrain management show the highest growth potential. The competitive landscape is characterized by technological innovation, strategic partnerships, and increasing investments in manufacturing capacity to address supply chain vulnerabilities exposed by recent global disruptions.

North America Automotive Semiconductor Market Forecast - Projections for 2025-2032 period

The North America Automotive Semiconductor Market forecast for 2025-2032 indicates a sustained growth trajectory, with the market expected to maintain its CAGR of 6.41% throughout the forecast period. This growth projection is based on the continued expansion of electric vehicle adoption, the increasing penetration of advanced driver assistance systems, and the ongoing development of autonomous driving technologies. The forecast suggests that component segments such as power devices, sensors, and microcontrollers will experience above-average growth rates due to their critical roles in emerging automotive applications. Application segments related to vehicle electrification and connectivity are expected to show the strongest growth, while vehicle type segmentation indicates that passenger vehicles will continue to dominate the market, with light commercial vehicles showing the highest growth rate as electrification expands to commercial applications. The forecast also accounts for potential market disruptions and technological breakthroughs that could accelerate or modify the projected growth trajectory.

North America Automotive Semiconductor Market Size and Share by Segmentation - Breakdown by {segmentData}

The North America Automotive Semiconductor Market segmentation reveals distinct patterns in component, application, and vehicle type distribution. By component, the market is divided into optical devices, sensors & actuators, memory, microcontrollers, analog ICs, and logic and discrete power devices, with each category serving specific automotive functions and experiencing varying growth rates. The application segmentation includes advanced driver assistance systems, body electronics, infotainment, powertrain, and safety systems, with ADAS and powertrain applications showing the highest growth potential due to increasing vehicle electrification and automation. Vehicle type segmentation encompasses passenger vehicles, light commercial vehicles, and heavy commercial vehicles, with passenger vehicles currently representing the largest market share while light commercial vehicles demonstrate the fastest growth rate as commercial fleet electrification accelerates. This segmentation analysis provides insights into market opportunities and helps identify high-growth areas for strategic investment and development.

Global North America Automotive Semiconductor Market Size and Share by Region - Geographic distribution

The North America Automotive Semiconductor Market exhibits distinct regional characteristics across the United States, Canada, and Mexico, each contributing differently to the overall market dynamics. The United States represents the largest regional market, driven by its substantial automotive manufacturing base, high technology adoption rates, and significant investments in electric vehicle infrastructure and autonomous driving research. Canada's market is characterized by its focus on electric vehicle development and strong presence of automotive research institutions, while Mexico benefits from its growing automotive manufacturing sector and increasing integration into North American supply chains. Regional distribution patterns show varying levels of market maturity, with the United States leading in advanced technology adoption, Canada focusing on sustainable transportation solutions, and Mexico experiencing rapid growth in automotive production capacity. These regional differences create a diverse market landscape with opportunities for both established players and emerging companies to establish strong regional presences.

Regional Analysis of the North America Automotive Semiconductor Market - Detailed regional market performance

Regional analysis of the North America Automotive Semiconductor Market reveals significant variations in market performance, growth drivers, and competitive dynamics across different geographic areas. The United States automotive semiconductor market benefits from a mature automotive industry, strong R&D capabilities, and substantial investments in electric vehicle infrastructure, particularly in states like Michigan, California, and Texas. Canada's market is characterized by its focus on electric vehicle innovation, with strong government support for clean technology initiatives and a growing ecosystem of automotive technology startups. Mexico's automotive semiconductor market is experiencing rapid growth due to increasing foreign direct investment, the expansion of automotive manufacturing facilities, and the country's integration into North American automotive supply chains. Regional performance variations are influenced by factors such as local government policies, availability of skilled workforce, infrastructure development, and proximity to major automotive manufacturing hubs, creating distinct opportunities and challenges in each regional market.

Leading Company Profiles in the North America Automotive Semiconductor Market - Industry players and strategies

The North America Automotive Semiconductor Market features several leading companies that have established strong market positions through technological innovation, strategic partnerships, and comprehensive product portfolios. Infineon Technologies has emerged as a key player through its focus on power semiconductors and microcontrollers for automotive applications, while NXP Semiconductors leverages its expertise in secure connectivity and processing solutions. Texas Instruments maintains a strong presence through its analog and embedded processing technologies, and ON Semiconductor has positioned itself as a leader in power management and image sensing solutions. Intel Corporation and NVIDIA Corporation are expanding their automotive presence through advanced computing platforms and AI accelerators for autonomous driving applications. These companies employ diverse strategies including vertical integration, strategic acquisitions, and collaborative research initiatives to strengthen their market positions and address the evolving needs of automotive manufacturers and consumers.

Porter's Five Forces Analysis of the North America Automotive Semiconductor Market - Competitive forces assessment

Porter's Five Forces analysis of the North America Automotive Semiconductor Market reveals a complex competitive landscape shaped by multiple strategic forces. The threat of new entrants is moderate, as the high capital requirements for semiconductor manufacturing and the need for automotive-grade certification create significant barriers to entry, though technology companies are increasingly entering the market through strategic partnerships and acquisitions. Bargaining power of suppliers is relatively high due to the specialized nature of automotive semiconductor components and the limited number of suppliers capable of meeting automotive quality standards. The bargaining power of buyers, primarily automotive OEMs, is strong due to their large purchase volumes and ability to influence design specifications. The threat of substitute products is low, as automotive semiconductors have unique specifications and requirements that limit direct substitution. Competitive rivalry among existing players is intense, characterized by rapid technological innovation, price competition, and the need for continuous product development to meet evolving automotive requirements.

SWOT Analysis of the North America Automotive Semiconductor Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the North America Automotive Semiconductor Market reveals distinct strategic factors influencing market dynamics. Strengths include the region's advanced technological infrastructure, strong automotive manufacturing base, and significant investments in research and development that drive innovation in automotive semiconductor solutions. Weaknesses encompass supply chain vulnerabilities, the high costs associated with automotive semiconductor development and certification, and the complexity of integrating multiple semiconductor components into vehicle systems. Opportunities exist in the growing electric vehicle market, the advancement of autonomous driving technologies, and the increasing demand for connected car features that require sophisticated semiconductor solutions. Threats include intense global competition from Asian semiconductor manufacturers, potential supply chain disruptions, rapid technological changes that could render existing solutions obsolete, and the regulatory challenges associated with automotive safety and emissions standards that impact semiconductor design and deployment.

North America Automotive Semiconductor Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the North America Automotive Semiconductor Market reveals a complex network of interconnected activities and stakeholders that create and deliver value across the automotive semiconductor ecosystem. The chain begins with raw material suppliers providing silicon, metals, and other essential materials, followed by semiconductor manufacturers who design and produce automotive-grade components. System integrators combine these components into complete solutions, while automotive OEMs incorporate them into vehicle designs and manufacturing processes. Distribution channels, including direct sales to manufacturers and aftermarket suppliers, facilitate the delivery of semiconductors to end users. Value is created through technological innovation, quality improvements, and the development of specialized solutions for specific automotive applications. Key value chain activities include research and development, design and engineering, manufacturing and testing, quality assurance, and technical support services. The analysis highlights opportunities for value enhancement through vertical integration, strategic partnerships, and the development of specialized capabilities that address specific automotive market needs.

Key Investment Insights in the North America Automotive Semiconductor Market - Strategic investment recommendations

Key investment insights for the North America Automotive Semiconductor Market indicate several strategic areas for potential investment and development. The transition to electric vehicles presents significant opportunities for investment in power semiconductors, battery management systems, and charging infrastructure components. Autonomous driving technology development requires substantial investment in high-performance processors, sensors, and AI accelerators capable of real-time data processing and decision-making. Connected vehicle technologies offer investment opportunities in V2X communication semiconductors and secure connectivity solutions. The growing emphasis on vehicle safety and emissions reduction creates demand for specialized semiconductors that enable advanced safety features and efficient powertrain management. Strategic investment recommendations include focusing on vertical integration to enhance supply chain control, developing partnerships with automotive OEMs for co-development of next-generation solutions, and investing in advanced manufacturing capabilities to address the increasing complexity of automotive semiconductor requirements.

North America Automotive Semiconductor Market Conclusion - Summary and key takeaways

The North America Automotive Semiconductor Market represents a dynamic and rapidly evolving sector that is fundamental to the future of automotive technology and transportation. With a projected market size of 18.07 billion by 2033 and a steady CAGR of 6.41%, the market demonstrates strong growth potential driven by the convergence of electric vehicle adoption, autonomous driving development, and connected car technologies. The market's segmentation across components, applications, and vehicle types reveals diverse opportunities for innovation and growth, while the competitive landscape shows both established semiconductor leaders and new technology entrants driving market evolution. Key takeaways include the critical importance of automotive semiconductors in enabling vehicle electrification and automation, the need for continued investment in manufacturing capacity and technological development, and the strategic significance of partnerships between semiconductor manufacturers and automotive OEMs. The market's future success will depend on addressing supply chain challenges, meeting evolving automotive requirements, and capitalizing on emerging opportunities in electric and autonomous vehicles.

Research Methodology - How this research was conducted

The research methodology employed for this North America Automotive Semiconductor Market analysis combines comprehensive primary and secondary research approaches to ensure accurate and reliable market insights. Primary research involved interviews with industry experts, semiconductor manufacturers, automotive OEMs, and technology analysts to gather firsthand information about market trends, challenges, and opportunities. Secondary research encompassed the analysis of industry reports, company financial statements, technical publications, and government databases to validate market data and identify emerging trends. The research methodology also included competitive analysis of key market players, supply chain assessment, and evaluation of technological developments in automotive semiconductor applications. Data triangulation techniques were applied to cross-verify information from multiple sources, while market size calculations were based on both top-down and bottom-up approaches to ensure accuracy. The methodology accounts for regional variations, technological advancements, and market dynamics to provide a comprehensive understanding of the North America Automotive Semiconductor Market landscape.

Research Scope - Coverage and limitations

The research scope for this North America Automotive Semiconductor Market analysis encompasses the comprehensive examination of market dynamics, trends, competitive landscape, and future projections across the United States, Canada, and Mexico. The scope includes detailed analysis of market segmentation by component type, application area, and vehicle category, along with regional performance assessment and competitive positioning of key market players. The research covers both current market conditions and future projections through 2033, incorporating the impact of technological developments, regulatory changes, and market disruptions such as the COVID-19 pandemic. Limitations of the research include the availability of certain proprietary data from private companies, the rapidly evolving nature of semiconductor technology that may affect long-term projections, and the potential for unforeseen market disruptions that could impact growth trajectories. The scope also acknowledges the complexity of automotive semiconductor supply chains and the challenges in obtaining comprehensive data on all market participants and their respective market shares.

Key Companies and Recent Developments in the North America Automotive Semiconductor Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The North America Automotive Semiconductor Market features several key companies that have demonstrated significant recent developments and strategic initiatives. Infineon Technologies has announced advancements in silicon carbide power semiconductors for electric vehicle applications, while NXP Semiconductors has launched new automotive radar processors for advanced driver assistance systems. Texas Instruments has expanded its automotive microcontroller portfolio with solutions optimized for electric vehicle powertrain management. ON Semiconductor has introduced innovative image sensing technologies for automotive safety applications. Intel Corporation has announced partnerships with major automotive manufacturers to develop AI-powered autonomous driving platforms, and NVIDIA Corporation has launched its DRIVE platform for autonomous vehicle computing. These companies, along with others such as Renesas Electronics, STMicroelectronics, and Bosch, continue to invest in research and development, form strategic partnerships, and introduce new products to address the evolving needs of the automotive industry. Recent developments also include increased manufacturing capacity investments, supply chain optimization initiatives, and collaborative efforts to address semiconductor shortages and enhance supply chain resilience.