Automotive Elastomers Market Overview - Definition, scope, and significance

Automotive elastomers are polymeric materials characterized by their viscoelasticity, offering both viscosity and elasticity. These materials are essential in the automotive industry due to their ability to withstand extreme temperatures, resist chemicals, and provide durability under various mechanical stresses. The scope of automotive elastomers encompasses a wide range of applications, including tires, interior components, exterior parts, and under-the-hood systems. Their significance lies in their contribution to vehicle performance, safety, and comfort, as well as their role in meeting increasingly stringent environmental regulations by enabling lightweight and fuel-efficient vehicle designs.

Automotive Elastomers Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The automotive elastomers market is driven by several factors, including the growing demand for lightweight vehicles to improve fuel efficiency and reduce emissions, the increasing production of electric vehicles, and the rising need for high-performance materials in automotive applications. Additionally, advancements in material science are leading to the development of new elastomer formulations with enhanced properties. However, the market faces restraints such as the volatility of raw material prices, particularly for petroleum-based elastomers, and the environmental concerns associated with the disposal of elastomeric materials. Challenges include the need for continuous innovation to meet evolving automotive standards and the competition from alternative materials. Opportunities exist in the development of sustainable and recyclable elastomers, as well as in the expansion of the market in emerging economies with growing automotive industries.

Automotive Elastomers Market Growth Trends - Current and emerging trends shaping the market

Current trends in the automotive elastomers market include the increasing use of thermoplastic elastomers (TPEs) due to their recyclability and ease of processing, the growing adoption of bio-based and sustainable elastomers, and the integration of smart materials with sensors for enhanced vehicle functionality. Emerging trends are focused on the development of elastomers with improved thermal and chemical resistance for electric vehicle battery systems, the use of 3D printing technology for customized elastomer components, and the application of nanotechnology to enhance material properties. Additionally, the market is witnessing a shift towards the use of elastomers in advanced driver-assistance systems (ADAS) and autonomous vehicles, where material performance is critical for safety and reliability.

COVID-19 Impact on the Automotive Elastomers Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the automotive elastomers market, primarily due to disruptions in global supply chains, temporary shutdowns of manufacturing facilities, and a decline in automotive production and sales. The pandemic led to a reduction in demand for automotive components, including elastomers, as consumer spending on vehicles decreased. However, the market has shown resilience, with a recovery trajectory supported by the gradual reopening of economies, the resumption of automotive production, and the increasing focus on electric vehicles and sustainable materials. The long-term impact of the pandemic has accelerated trends such as digitalization in manufacturing and the adoption of more flexible supply chain strategies, which are expected to shape the future of the automotive elastomers market.

Automotive Elastomers Market Competitive Landscape - Major competitors and market consolidation

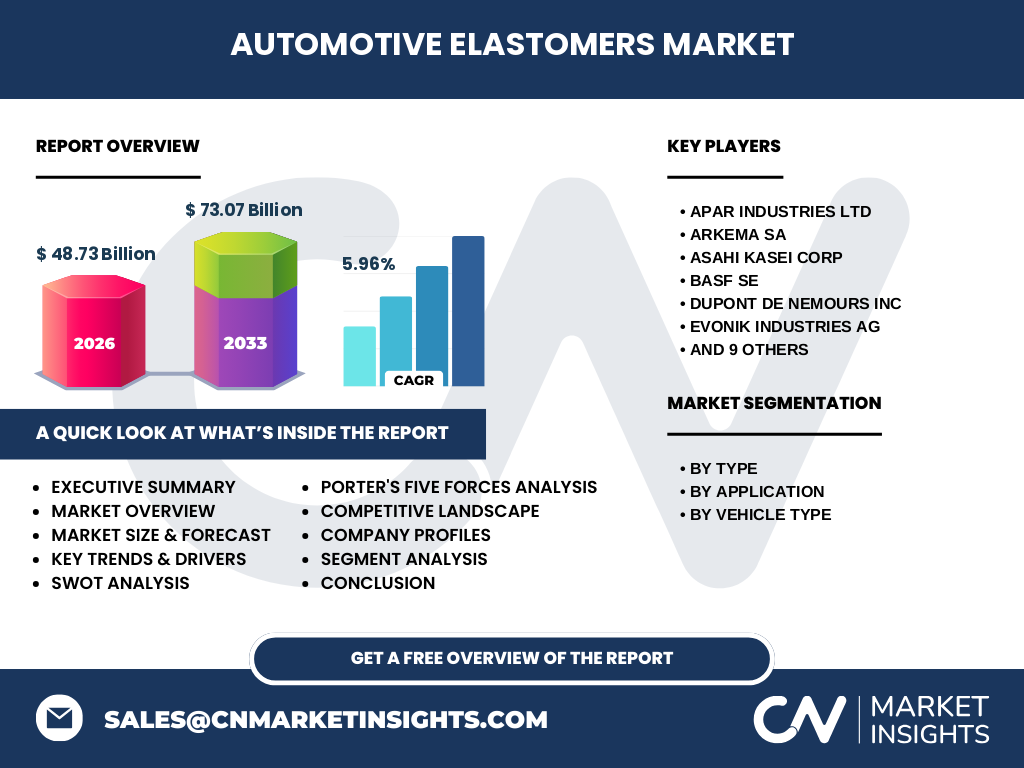

The automotive elastomers market is characterized by the presence of several key players, including APAR Industries Ltd, Arkema SA, Asahi Kasei Corp, BASF SE, and DuPont de Nemours Inc, among others. These companies are engaged in continuous research and development to innovate and improve their product offerings. The competitive landscape is marked by strategic collaborations, mergers and acquisitions, and investments in new technologies to gain a competitive edge. Market consolidation is observed as larger companies acquire smaller firms to expand their product portfolios and geographic presence. The competition is also driven by the need to comply with stringent environmental regulations and to meet the evolving demands of the automotive industry for high-performance and sustainable materials.

Executive Summary - High-level overview and key findings about Automotive Elastomers Market

The automotive elastomers market is poised for steady growth, with a projected CAGR of 5.96% from 2026 to 2033, reaching a market size of 73.07 billion by 2033. The market is segmented by type, application, and vehicle type, with thermoset and thermoplastic elastomers catering to diverse applications such as tires, interiors, exteriors, and under-the-hood systems. The passenger vehicle segment dominates the market, driven by the increasing production of electric vehicles and the demand for lightweight materials. Key findings indicate that the market is influenced by technological advancements, environmental regulations, and the shift towards sustainable materials. The competitive landscape is dynamic, with major players focusing on innovation and strategic partnerships to maintain their market position.

Automotive Elastomers Market Forecast - Projections for 2025-2032 period

The automotive elastomers market is forecasted to experience robust growth from 2025 to 2032, with a CAGR of 5.96%. The market size is expected to increase from 48.73 billion in 2026 to 73.07 billion by 2033. This growth is attributed to the rising demand for electric vehicles, the increasing adoption of lightweight materials to enhance fuel efficiency, and the development of advanced elastomer formulations with superior properties. The thermoplastic elastomers segment is anticipated to witness significant growth due to its recyclability and versatility. Geographically, the Asia-Pacific region is expected to lead the market, driven by the expansion of the automotive industry in countries like China and India. The forecast period also highlights the potential for innovation in sustainable and smart elastomers, which could further drive market growth.

Automotive Elastomers Market Size and Share by Segmentation - Breakdown by {segmentData}

The automotive elastomers market is segmented by type, application, and vehicle type. By type, the market is divided into thermoset elastomers and thermoplastic elastomers, with thermoplastic elastomers gaining traction due to their recyclability and ease of processing. In terms of application, the market is categorized into tire, interior, exterior, and under-the-hood systems, with the tire segment holding a significant share due to the high demand for durable and high-performance tires. By vehicle type, the market is segmented into passenger vehicles, light commercial vehicles, heavy commercial vehicles, and two-wheelers, with passenger vehicles accounting for the largest share, driven by the increasing production of electric and hybrid vehicles. This segmentation provides a comprehensive understanding of the market dynamics and the specific needs of different automotive applications.

Global Automotive Elastomers Market Size and Share by Region - Geographic distribution

The global automotive elastomers market is distributed across various regions, with the Asia-Pacific region holding the largest share due to the presence of major automotive manufacturing hubs in countries like China, Japan, and India. North America and Europe are also significant markets, driven by the demand for advanced automotive technologies and stringent environmental regulations. The Middle East and Africa, as well as Latin America, are emerging markets with growing automotive industries. The regional distribution of the market is influenced by factors such as economic growth, industrialization, and the adoption of electric vehicles. The Asia-Pacific region is expected to maintain its dominance during the forecast period, supported by the increasing production of vehicles and the expansion of the automotive supply chain.

Regional Analysis of the Automotive Elastomers Market - Detailed regional market performance

The regional analysis of the automotive elastomers market reveals distinct performance patterns across different geographies. In the Asia-Pacific region, the market is driven by the rapid growth of the automotive industry, particularly in China and India, where there is a high demand for both passenger and commercial vehicles. North America is characterized by the adoption of advanced automotive technologies and a strong focus on sustainability, leading to the increased use of thermoplastic elastomers. Europe, with its stringent environmental regulations, is witnessing a shift towards eco-friendly elastomers and the development of electric vehicles. The Middle East and Africa, as well as Latin America, are experiencing growth due to the expansion of the automotive sector and the increasing investment in infrastructure. Each region presents unique opportunities and challenges, influenced by local economic conditions, regulatory frameworks, and consumer preferences.

Leading Company Profiles in the Automotive Elastomers Market - Industry players and strategies

The automotive elastomers market is dominated by several leading companies, each with its own strategic focus and market approach. APAR Industries Ltd is known for its innovative solutions in the electrical and automotive sectors, while Arkema SA specializes in high-performance materials and sustainable solutions. Asahi Kasei Corp and BASF SE are global leaders in chemical and material sciences, offering a wide range of elastomer products. DuPont de Nemours Inc is recognized for its advanced materials and technologies, particularly in the automotive industry. Evonik Industries AG focuses on specialty chemicals and performance materials, while Huntsman International LLC provides a diverse portfolio of elastomer products. KRAIBURG TPE and Kraton Corp are key players in the thermoplastic elastomer segment, and LG Chem Ltd is a major supplier of advanced materials for automotive applications. These companies are engaged in strategic initiatives such as mergers, acquisitions, and partnerships to strengthen their market position and drive innovation.

Porter's Five Forces Analysis of the Automotive Elastomers Market - Competitive forces assessment

Porter's Five Forces analysis of the automotive elastomers market reveals the competitive dynamics that shape the industry. The threat of new entrants is moderate due to the high capital requirements and the need for technological expertise. The bargaining power of suppliers is significant, as raw material prices are subject to fluctuations and suppliers may have limited alternatives. The bargaining power of buyers is high, given the presence of large automotive manufacturers who can influence pricing and demand. The threat of substitutes is moderate, with alternative materials such as metals and composites posing a potential challenge. The intensity of competitive rivalry is high, with numerous players competing on the basis of product quality, innovation, and price. Overall, the market is characterized by a balance of power among these forces, with companies needing to navigate these dynamics to maintain their competitive position.

SWOT Analysis of the Automotive Elastomers Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the automotive elastomers market highlights its internal and external factors. Strengths include the versatility and durability of elastomers, their ability to meet diverse automotive applications, and the continuous innovation in material science. Weaknesses involve the dependency on petroleum-based raw materials, environmental concerns related to disposal, and the high cost of advanced elastomer formulations. Opportunities exist in the development of sustainable and bio-based elastomers, the expansion of the electric vehicle market, and the increasing demand for lightweight materials. Threats include the volatility of raw material prices, the potential for regulatory changes affecting material usage, and the competition from alternative materials. By leveraging strengths and addressing weaknesses, companies can capitalize on opportunities and mitigate threats in the market.

Automotive Elastomers Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the automotive elastomers market provides insights into the industry structure and the flow of value from raw materials to end-users. The value chain begins with the procurement of raw materials, such as natural rubber, synthetic rubber, and additives, which are then processed into elastomers through various manufacturing techniques. The elastomers are supplied to automotive manufacturers or component suppliers, who integrate them into various parts of the vehicle. The final products are then distributed to end-users through dealerships and aftermarket channels. Key activities in the value chain include research and development, manufacturing, quality control, and distribution. The value chain is characterized by a high degree of integration, with companies often involved in multiple stages to ensure quality and efficiency. The analysis highlights the importance of each stage in delivering high-quality elastomer products to the automotive industry.

Key Investment Insights in the Automotive Elastomers Market - Strategic investment recommendations

Investment insights in the automotive elastomers market suggest several strategic recommendations for stakeholders. Investors should focus on companies that are leading in the development of sustainable and high-performance elastomers, as these are expected to drive future growth. There is also potential in investing in firms that are expanding their presence in emerging markets, particularly in the Asia-Pacific region, where the automotive industry is growing rapidly. Additionally, investments in companies that are adopting advanced manufacturing technologies, such as 3D printing and automation, could yield significant returns. Strategic partnerships and collaborations with automotive manufacturers to develop customized elastomer solutions are also recommended. Overall, investments should be directed towards innovation, sustainability, and geographic expansion to capitalize on the evolving dynamics of the automotive elastomers market.

Automotive Elastomers Market Conclusion - Summary and key takeaways

In conclusion, the automotive elastomers market is on a growth trajectory, driven by the increasing demand for lightweight, high-performance materials in the automotive industry. The market is expected to grow at a CAGR of 5.96%, reaching a size of 73.07 billion by 2033. Key trends include the adoption of thermoplastic elastomers, the development of sustainable materials, and the integration of smart technologies. The competitive landscape is dynamic, with major players focusing on innovation and strategic initiatives to maintain their market position. Regional analysis indicates that the Asia-Pacific region will continue to dominate the market, supported by the growth of the automotive sector. Overall, the market presents significant opportunities for stakeholders who can navigate the challenges and capitalize on the emerging trends.

Research Methodology - How this research was conducted

The research methodology for this automotive elastomers market report involved a comprehensive approach to data collection and analysis. Primary research was conducted through interviews with industry experts, including manufacturers, suppliers, and automotive companies, to gather insights into market trends, challenges, and opportunities. Secondary research involved the analysis of industry reports, company publications, and government data to validate and supplement the primary findings. The market size and forecasts were derived using a combination of top-down and bottom-up approaches, considering factors such as historical data, current market conditions, and future projections. The segmentation of the market was based on type, application, and vehicle type, with regional analysis providing a detailed understanding of geographic distribution. The methodology ensured a robust and reliable assessment of the automotive elastomers market.

Research Scope - Coverage and limitations

The research scope of this automotive elastomers market report encompasses a detailed analysis of the market by type, application, and vehicle type, as well as a regional breakdown. The report covers the period from 2025 to 2033, with a focus on key trends, drivers, and challenges influencing the market. The scope includes an assessment of the competitive landscape, featuring leading companies and their strategic initiatives. However, the research has certain limitations, such as the availability of data for certain regions and the potential for rapid technological changes that could impact market dynamics. Despite these limitations, the report provides a comprehensive overview of the automotive elastomers market, offering valuable insights for stakeholders and decision-makers.

Key Companies and Recent Developments in the Automotive Elastomers Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The automotive elastomers market is characterized by the presence of several key companies that are driving innovation and growth. APAR Industries Ltd has been focusing on expanding its product portfolio and enhancing its manufacturing capabilities. Arkema SA recently announced the development of new bio-based elastomer solutions, aligning with the industry's shift towards sustainability. Asahi Kasei Corp has been investing in advanced material technologies to improve the performance of its elastomer products. BASF SE has launched several new elastomer formulations designed for electric vehicle applications, addressing the growing demand for lightweight and durable materials. DuPont de Nemours Inc has introduced innovative elastomer solutions for under-the-hood applications, enhancing vehicle performance and efficiency. Evonik Industries AG has been collaborating with automotive manufacturers to develop customized elastomer solutions. Huntsman International LLC has expanded its production capacity to meet the increasing demand for thermoplastic elastomers. KRAIBURG TPE and Kraton Corp have been at the forefront of developing recyclable and sustainable elastomer products. LG Chem Ltd has been focusing on the development of high-performance elastomers for electric vehicle battery systems. These companies are actively engaged in strategic developments, including mergers, acquisitions, and partnerships, to strengthen their market position and drive innovation in the automotive elastomers market.