Aquafeed Market Overview - Definition, scope, and significance

Aquafeed represents the specialized food products formulated specifically for aquatic species raised in aquaculture operations. This comprehensive market encompasses manufactured feed for fish, crustaceans, and mollusks, designed to meet the nutritional requirements of various aquatic life stages. The scope extends across multiple species including salmon, shrimp, tilapia, carp, catfish, and other commercially farmed aquatic organisms. The significance of aquafeed lies in its critical role in supporting the global aquaculture industry, which provides over half of all seafood consumed worldwide. As wild fish stocks face increasing pressure from overfishing and environmental challenges, aquaculture has emerged as a vital solution for meeting growing global protein demand. Aquafeed serves as the foundation for sustainable aquaculture production, directly influencing growth rates, health outcomes, feed conversion efficiency, and ultimately the economic viability of aquaculture operations across both developed and developing markets.

Aquafeed Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The aquafeed market experiences robust growth driven by several key factors including rising global seafood consumption, increasing awareness of aquaculture's nutritional benefits, and technological advancements in feed formulation. Population growth and changing dietary preferences toward protein-rich foods continue to fuel demand for farmed seafood, consequently driving aquafeed consumption. However, the market faces significant restraints including volatile raw material prices, particularly for fishmeal and fish oil, which are essential but increasingly scarce ingredients. Environmental concerns regarding sustainable sourcing and the ecological impact of aquaculture operations present ongoing challenges. Additionally, disease outbreaks in aquaculture facilities can dramatically affect feed demand and production. Despite these challenges, substantial opportunities exist in developing alternative protein sources such as plant-based proteins, insect meal, and single-cell proteins. The growing demand for functional feeds with enhanced nutritional profiles, probiotics, and disease-prevention properties represents another significant opportunity. Expansion in emerging markets with untapped aquaculture potential and the development of species-specific formulations for niche aquaculture applications further contribute to market growth prospects.

Aquafeed Market Growth Trends - Current and emerging trends shaping the market

The aquafeed market demonstrates several notable growth trends that are reshaping the industry landscape. A prominent trend involves the increasing adoption of sustainable and alternative ingredients to reduce reliance on traditional fishmeal and fish oil, driven by both environmental concerns and supply constraints. Plant-based proteins, particularly from soy and corn, continue gaining market share, while novel ingredients like insect protein, algae, and single-cell proteins are experiencing rapid development. Another significant trend is the growing demand for functional feeds incorporating probiotics, prebiotics, and immune-enhancing additives that improve disease resistance and growth performance. The market is witnessing a shift toward species-specific formulations tailored to the unique nutritional requirements of different aquatic species and life stages. Technological advancements in feed manufacturing, including microencapsulation and controlled-release formulations, are enhancing feed efficiency and reducing environmental impact. Additionally, the integration of digital technologies and precision feeding systems is optimizing feed utilization and reducing waste. The trend toward organic and antibiotic-free aquaculture production is driving demand for specialized organic aquafeeds, while the expansion of inland aquaculture in regions with limited marine access is creating new market opportunities.

COVID-19 Impact on the Aquafeed Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly impacted the aquafeed market through multiple channels, creating both immediate disruptions and longer-term transformations. Initial pandemic effects included supply chain disruptions that affected the availability and pricing of key raw materials, particularly fishmeal and fish oil sourced internationally. Transportation restrictions and labor shortages temporarily constrained production capacity at feed manufacturing facilities. Demand volatility emerged as restaurant closures and changing consumer purchasing patterns affected seafood markets globally. However, the pandemic also accelerated certain market trends, including increased investment in domestic aquaculture to enhance food security and supply chain resilience. The recovery trajectory has been characterized by adaptive strategies such as diversification of raw material sourcing, increased automation in feed production, and enhanced digital integration for supply chain management. The pandemic highlighted the importance of aquaculture as a reliable protein source, potentially strengthening long-term market fundamentals. Recovery has been uneven across regions, with some markets rebounding more quickly than others based on local pandemic management, economic conditions, and aquaculture industry structure. The crisis has prompted renewed focus on sustainable and resilient aquafeed production systems.

Aquafeed Market Competitive Landscape - Major competitors and market consolidation

The aquafeed market features a competitive landscape characterized by both global conglomerates and regional specialists competing across diverse geographic and species segments. Major multinational corporations including Cargill, Incorporated, Archer-Daniels-Midland Co, and BioMar Group AS leverage extensive distribution networks and research capabilities to maintain significant market positions. These companies benefit from integrated supply chains, substantial R&D investments, and broad product portfolios spanning multiple aquatic species. Regional players such as Avanti Feeds Limited in India, Growel Feeds Pvt Ltd in Southeast Asia, and Skretting across European markets maintain strong positions through local market knowledge and established customer relationships. Market consolidation trends are evident through strategic acquisitions, joint ventures, and partnerships aimed at expanding geographic presence and technological capabilities. Competitive dynamics are influenced by factors including product innovation, sustainability credentials, pricing strategies, and customer service quality. The market exhibits varying degrees of concentration across different regions and species segments, with some markets dominated by a few large players while others maintain more fragmented competitive structures. Differentiation strategies increasingly focus on specialized formulations, sustainability certifications, and value-added services beyond traditional feed supply.

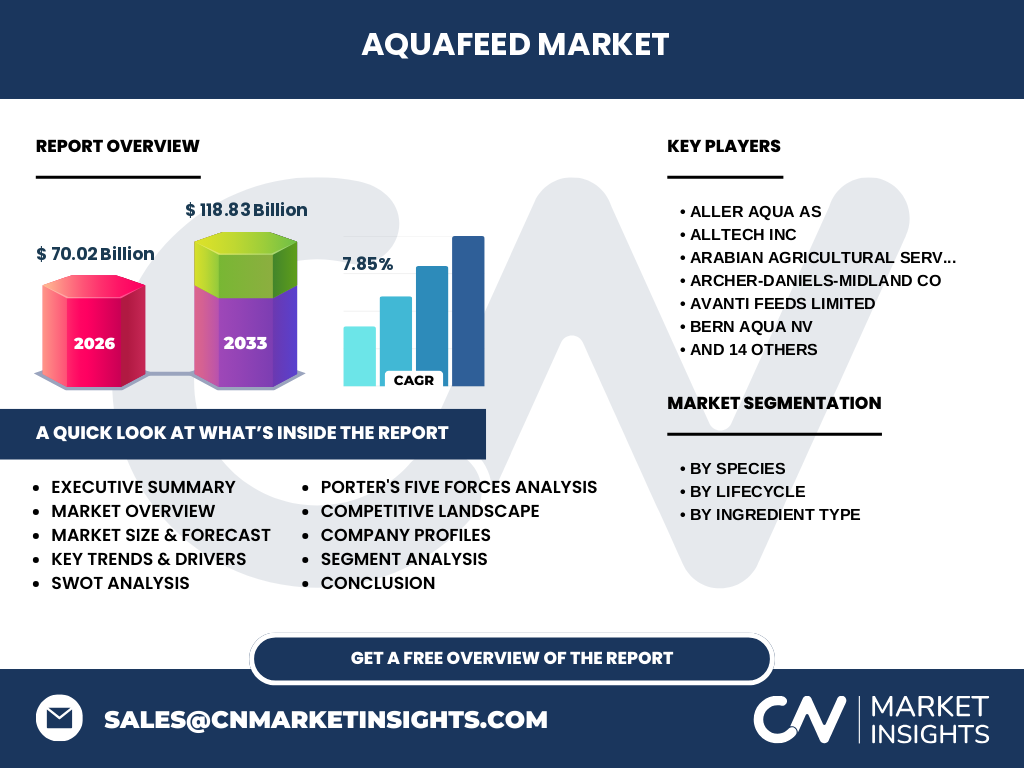

Executive Summary - High-level overview and key findings about Aquafeed Market

The global aquafeed market represents a dynamic and essential component of the expanding aquaculture industry, demonstrating robust growth driven by increasing seafood consumption and technological advancement. Market analysis indicates a trajectory from approximately 70.02 billion in 2026 to an estimated 118.83 billion by 2033, reflecting a compound annual growth rate of 7.85%. This growth is underpinned by rising global demand for protein, particularly in developing economies, and the aquaculture sector's critical role in meeting this demand as wild fisheries reach sustainable limits. Key market segments include fish, crustaceans, and mollusks, with feed formulations tailored to specific species and life stages ranging from starter to finisher feeds. Ingredient innovation represents a significant market driver, with traditional fishmeal and fish oil facing pressure from sustainable alternatives including plant proteins, insect meal, and novel ingredients. The competitive landscape features a mix of global conglomerates and regional specialists, with market dynamics varying significantly across geographic regions. Sustainability concerns, regulatory frameworks, and technological advancements in feed formulation and manufacturing continue to shape market evolution, creating both challenges and opportunities for industry participants.

Aquafeed Market Forecast - Projections for 2025-2032 period

Projections for the aquafeed market spanning 2025-2032 indicate substantial growth across all major segments and regions, building upon the established trajectory from 70.02 billion in 2026 toward 118.83 billion by 2033. This represents a compound annual growth rate of 7.85%, reflecting sustained demand across diverse aquaculture applications. Fish feed is expected to maintain the largest market share, driven by expanding production of species including salmon, tilapia, and carp, particularly in Asia-Pacific and Latin American markets. Crustacean feed, especially shrimp feed, demonstrates the highest growth rate among species segments, fueled by increasing consumer demand and production intensification in Southeast Asia and Latin America. Mollusk feed, while representing a smaller segment, shows steady growth aligned with expanding oyster, mussel, and clam aquaculture. Lifecycle-specific feed formulations continue gaining market share as producers recognize the performance benefits of tailored nutrition across growth stages. Regional growth patterns indicate Asia-Pacific maintaining dominance while Latin America and Africa present the highest growth opportunities. Ingredient trends favor continued expansion of plant-based proteins alongside emerging alternative ingredients, with sustainable formulations commanding premium pricing in developed markets.

Aquafeed Market Size and Share by Segmentation - Breakdown by {segmentData}

Market segmentation analysis reveals distinct patterns across species, lifecycle stages, and ingredient types that collectively shape the aquafeed market structure. By species segmentation, fish feed dominates the market, accounting for approximately 50-60% of total volume, driven by the extensive production of species including salmon, tilapia, and various carp species. Crustacean feed represents the second-largest segment at approximately 25-30% market share, with shrimp feed being the primary driver within this category due to the species' global popularity and production volume. Mollusk feed constitutes approximately 10-15% of the market, serving growing oyster, mussel, and clam aquaculture operations. Lifecycle segmentation demonstrates that grower feed represents the largest share at approximately 35-40%, followed by finisher feed at 25-30%, reflecting the extended duration of these production stages. Starter feed accounts for 15-20% of the market, while specialized feeds including brooder and broodstock formulations represent 10-15%. Ingredient type segmentation reveals plant-based proteins, particularly soy and corn, comprising approximately 60-65% of feed formulations, while fishmeal and fish oil maintain approximately 15-20% share despite declining relative importance. Alternative ingredients including insect meal, algae, and single-cell proteins collectively represent approximately 5-10% and show the highest growth trajectory.

Global Aquafeed Market Size and Share by Region - Geographic distribution

Regional analysis of the global aquafeed market reveals significant geographic variations in market size, growth rates, and competitive dynamics. Asia-Pacific dominates the global market, accounting for approximately 60-65% of total volume, driven by extensive aquaculture production in China, India, Vietnam, and Indonesia. China alone represents nearly 30% of global aquafeed consumption, with the country's massive carp and tilapia production forming the backbone of regional demand. Latin America emerges as the second-largest regional market at approximately 15-20% share, with Ecuador, Chile, and Brazil leading production, particularly in salmon and shrimp aquaculture. Europe accounts for approximately 10-12% of global market volume, characterized by advanced production technologies and strong sustainability standards, with Norway, the UK, and Spain as key contributors. North America represents approximately 7-9% of the market, dominated by the United States with its catfish and salmon production, alongside significant shrimp farming in Mexico. Africa and the Middle East collectively account for approximately 5-7% of global volume, with Egypt leading African production and Saudi Arabia representing the primary Middle Eastern market. Regional growth rates vary considerably, with Latin America and Africa demonstrating the highest expansion trajectories while mature markets in Europe and North America show more moderate growth.

Regional Analysis of the Aquafeed Market - Detailed regional market performance

Regional market performance analysis reveals distinct characteristics and growth patterns across global aquafeed markets. Asia-Pacific demonstrates robust growth driven by expanding aquaculture production, particularly in China, India, Vietnam, and Indonesia, where freshwater fish farming dominates. The region benefits from abundant raw materials, established supply chains, and growing domestic consumption, though it faces challenges including disease management and environmental regulations. Latin America shows exceptional growth momentum, particularly in Ecuador and Chile, where shrimp and salmon aquaculture respectively drive feed demand. The region benefits from favorable climate conditions, extensive coastlines, and increasing investment in production infrastructure. Europe presents a mature but technologically advanced market characterized by high feed quality standards, strong sustainability requirements, and significant R&D investment. Norway leads European production with its salmon industry, while Mediterranean countries maintain substantial sea bass and sea bream farming. North America exhibits steady growth with the United States focusing on catfish and salmon production, while Mexico's shrimp industry expands rapidly. Africa demonstrates emerging market potential, particularly in Egypt's tilapia industry and Nigeria's catfish farming, though infrastructure limitations constrain broader development. The Middle East shows concentrated growth in Saudi Arabia's aquaculture expansion, supported by significant government investment in food security initiatives.

Leading Company Profiles in the Aquafeed Market - Industry players and strategies

Leading company profiles in the aquafeed market reveal diverse strategies and competitive positioning among major industry players. Cargill, Incorporated leverages its global agricultural supply chain and extensive R&D capabilities to offer comprehensive aquafeed solutions across multiple species and regions. The company's strategy emphasizes sustainability through alternative ingredient development and integrated supply chain management. BioMar Group AS focuses on premium feed formulations with strong emphasis on sustainability certifications and technological innovation, particularly in salmon and marine species feed. Skretting, a subsidiary of Nutreco, maintains global leadership through specialized R&D centers and a broad product portfolio spanning all major aquaculture species. Aller Aqua AS concentrates on European and African markets with high-quality feed formulations and strong customer relationships. Avanti Feeds Limited dominates the Indian shrimp feed market through vertical integration and extensive distribution networks in South Asia. Growel Feeds Pvt Ltd pursues aggressive expansion in Southeast Asian markets with cost-competitive products and strong local partnerships. Kemin Industries Inc differentiates through functional feed additives and health-focused formulations incorporating probiotics and immune enhancers. These companies employ varied strategies including vertical integration, sustainability positioning, technological innovation, and geographic expansion to maintain competitive advantages in their respective market segments.

Porter's Five Forces Analysis of the Aquafeed Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics shaping the aquafeed market structure. The threat of new entrants remains moderate due to substantial capital requirements for feed manufacturing facilities, established distribution networks, and the need for technical expertise in feed formulation. However, opportunities exist in emerging markets and specialized segments where established players have limited presence. Bargaining power of suppliers presents a significant force, particularly regarding key raw materials like fishmeal, fish oil, and specialty ingredients, where price volatility and supply constraints can impact profitability. The bargaining power of buyers varies by region and species, with large aquaculture operations in mature markets exerting considerable influence on pricing and service requirements, while fragmented small-scale farmers in developing regions have limited negotiating power. The threat of substitute products remains relatively low for core aquafeed applications, though alternative protein sources and on-farm feed production present potential substitution risks in certain markets. Competitive rivalry among existing players is intense, characterized by price competition, product differentiation efforts, and geographic expansion strategies. Industry consolidation through mergers and acquisitions continues, potentially reducing rivalry while increasing barriers to entry. Overall, the market structure favors established players with integrated supply chains and strong R&D capabilities.

SWOT Analysis of the Aquafeed Market - Strengths, weaknesses, opportunities, threats

SWOT analysis of the aquafeed market reveals critical internal and external factors influencing industry dynamics. Strengths include the essential nature of aquafeed to aquaculture production, established global supply chains, and continuous technological advancement in feed formulation and manufacturing. The industry benefits from strong demand fundamentals driven by growing global seafood consumption and aquaculture's role in food security. Weaknesses encompass dependence on volatile raw material prices, particularly fishmeal and fish oil, environmental concerns regarding feed sustainability, and vulnerability to disease outbreaks in aquaculture operations. The industry also faces challenges related to feed conversion efficiency and environmental impact of nutrient discharge. Opportunities abound in developing alternative protein sources, expanding into emerging markets with untapped aquaculture potential, and creating value-added functional feeds with health and growth benefits. Technological advancements in precision feeding and digital integration present additional growth avenues. Threats include increasing regulatory scrutiny regarding environmental impact and ingredient sourcing, competition from alternative protein sources, and potential disruptions from climate change affecting both raw material availability and aquaculture production. Disease outbreaks, whether in aquaculture facilities or feed production, represent significant operational risks that can rapidly impact market dynamics.

Aquafeed Market Value Chain Analysis - Industry structure and value flow

Value chain analysis of the aquafeed market reveals a complex network of interconnected activities and stakeholders contributing to final product delivery. The chain begins with raw material sourcing, where suppliers provide essential ingredients including fishmeal, fish oil, plant proteins, and emerging alternatives like insect meal and algae. Primary processors transform these raw materials into usable feed components through various processing methods. Feed manufacturers then formulate and produce finished feeds, incorporating additives, vitamins, and minerals tailored to specific species and production objectives. Distribution networks transport products to aquaculture operations, which may involve direct delivery to large farms or retail through agricultural supply channels for smaller producers. End customers, the aquaculture producers, utilize feeds to grow aquatic species for eventual harvest and processing. Supporting activities include research and development for new formulations, quality control testing, technical support services, and sustainability certification programs. Value is added at multiple stages through product differentiation, technical expertise, and service provision beyond basic feed supply. The chain exhibits varying degrees of vertical integration, with some companies controlling multiple stages while others focus on specific segments. Emerging trends include increased integration of digital technologies for supply chain optimization and growing emphasis on sustainability throughout the value chain.

Key Investment Insights in the Aquafeed Market - Strategic investment recommendations

Investment insights for the aquafeed market reveal several strategic opportunities aligned with industry growth trajectories and emerging trends. Alternative ingredient development represents a particularly attractive investment area, with plant-based proteins, insect meal, algae, and single-cell proteins showing strong growth potential as sustainable alternatives to traditional fishmeal and fish oil. Companies investing in R&D for these novel ingredients and their scalable production technologies are positioned for significant returns as regulatory pressures and supply constraints drive demand for alternatives. Geographic expansion into high-growth emerging markets, particularly in Africa and Latin America, offers substantial opportunities as aquaculture production intensifies in these regions. Investment in vertical integration strategies, combining feed production with raw material sourcing or distribution, can enhance competitive positioning and margin stability. Functional feed additives incorporating probiotics, immune enhancers, and disease prevention compounds represent another promising investment area as producers seek to improve production efficiency and reduce antibiotic use. Digital integration investments, including precision feeding technologies and supply chain optimization systems, align with industry trends toward increased efficiency and sustainability. Sustainability-focused investments, including carbon footprint reduction and circular economy initiatives, address growing regulatory and consumer demands while potentially creating competitive advantages in premium market segments.

Aquafeed Market Conclusion - Summary and key takeaways

The aquafeed market presents a compelling growth narrative characterized by robust expansion from 70.02 billion in 2026 toward 118.83 billion by 2033, reflecting a compound annual growth rate of 7.85%. This growth is fundamentally driven by the aquaculture industry's critical role in meeting global seafood demand as wild fisheries reach sustainable limits. Key market dynamics include the shift toward sustainable ingredients, with plant-based proteins maintaining dominance while novel alternatives gain traction. Regional variations reveal Asia-Pacific's continued market leadership alongside exceptional growth opportunities in Latin America and Africa. The competitive landscape features both global conglomerates and regional specialists employing diverse strategies from vertical integration to sustainability positioning. Market segmentation analysis highlights the dominance of fish feed alongside the rapid expansion of crustacean feed, particularly shrimp. Lifecycle-specific formulations and functional feeds represent growing market segments as producers seek performance optimization. Investment opportunities align with sustainability trends, technological advancement, and geographic expansion. Despite challenges including raw material volatility and environmental concerns, the market's essential role in global food security and positive growth fundamentals position it for continued expansion throughout the forecast period.

Research Methodology - How this research was conducted

The research methodology employed for this aquafeed market analysis combines comprehensive primary and secondary research approaches to ensure accuracy and reliability. Primary research involved interviews with key industry stakeholders including feed manufacturers, aquaculture producers, raw material suppliers, and industry experts across major geographic regions. These interviews provided insights into market dynamics, growth trends, competitive strategies, and emerging opportunities. Secondary research encompassed extensive review of industry reports, company financial statements, trade publications, government statistics, and academic research related to aquaculture and feed production. Market size and forecast projections were developed using bottom-up analysis based on species-specific feed consumption data, regional production volumes, and price trends. Segmentation analysis incorporated both quantitative data and qualitative insights regarding market structure and competitive dynamics. Regional analysis utilized country-level production data, trade statistics, and economic indicators to assess geographic variations in market performance. Competitive landscape assessment combined company profiling with market share analysis based on production capacity, geographic presence, and product portfolio. The research methodology prioritized data triangulation across multiple sources to validate findings and ensure comprehensive market coverage.

Research Scope - Coverage and limitations

The research scope encompasses a comprehensive analysis of the global aquafeed market, covering major species segments including fish, crustaceans, and mollusks across all major geographic regions. The study examines market dynamics through 2033, incorporating historical data where available and forward-looking projections based on industry trends and growth drivers. Coverage includes detailed segmentation by species, lifecycle stage, and ingredient type, providing granular insights into market structure and growth patterns. Regional analysis addresses major aquaculture producing countries and emerging markets, with particular attention to Asia-Pacific, Latin America, Europe, and North America. The competitive landscape assessment profiles leading companies and analyzes market consolidation trends, though specific market share data for individual players remains limited due to confidentiality considerations. Research limitations include the inherent challenges in obtaining accurate production data from fragmented small-scale aquaculture operations, particularly in developing regions. Currency fluctuations and regional economic variations may impact financial projections. The rapidly evolving nature of alternative ingredient development means that some emerging trends may develop differently than projected. Additionally, the analysis focuses on commercial aquafeed production, with limited coverage of on-farm feed production or non-commercial aquaculture operations that may represent significant market segments in certain regions.

Key Companies and Recent Developments in the Aquafeed Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Key companies in the aquafeed market have demonstrated significant strategic developments and innovations shaping industry evolution. Cargill, Incorporated announced expanded production capacity in Vietnam and Ecuador to support growing shrimp and marine fish aquaculture in Southeast Asia and Latin America. The company launched new functional feed lines incorporating probiotics and immune-enhancing compounds designed to improve disease resistance in farmed species. BioMar Group AS unveiled its "BioMar Future" initiative focusing on carbon-neutral feed production by 2030, including partnerships with alternative ingredient suppliers for novel protein sources. Skretting introduced species-specific formulations for emerging aquaculture species including yellowtail and kingfish, targeting premium market segments in Japan and Australia. Aller Aqua AS expanded its African operations with new production facilities in Egypt, addressing growing tilapia farming demand in the region. Avanti Feeds Limited announced vertical integration initiatives combining feed production with hatchery and farming operations to enhance supply chain control. Growel Feeds Pvt Ltd launched cost-optimized feed formulations for small-scale farmers in India, incorporating locally sourced ingredients to improve affordability. Kemin Industries Inc formed strategic partnerships with aquaculture technology companies to develop integrated feeding and monitoring systems. These developments reflect industry trends toward sustainability, technological innovation, and geographic expansion as companies position for continued market growth.