Smart Lighting Market Overview - Definition, scope, and significance

Smart lighting refers to advanced lighting systems that utilize intelligent controls, sensors, and connectivity technologies to optimize illumination while reducing energy consumption. These systems integrate hardware components like LED fixtures, sensors, and control modules with software platforms that enable remote management, automation, and data analytics. The scope of the smart lighting market encompasses residential, commercial, industrial, outdoor, government, and automotive applications, with connectivity options ranging from wired to wireless technologies. The significance of this market lies in its potential to address critical global challenges including energy efficiency, sustainability, and the growing demand for intelligent building management systems. As urbanization accelerates and smart city initiatives gain momentum worldwide, smart lighting serves as a foundational technology that enhances safety, reduces operational costs, and contributes to environmental conservation efforts.

Smart Lighting Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The smart lighting market is primarily driven by increasing energy costs, stringent government regulations on energy efficiency, and growing environmental awareness. The rapid adoption of LED technology, coupled with advancements in IoT and wireless communication protocols, has made smart lighting systems more accessible and cost-effective. Rising smart city projects and the integration of lighting systems with building management platforms further accelerate market growth. However, the market faces several restraints including high initial installation costs, concerns about data privacy and security, and the complexity of retrofitting existing infrastructure. Technical challenges such as interoperability issues between different manufacturers' systems and the need for continuous software updates present additional obstacles. Despite these challenges, significant opportunities exist in emerging markets, the development of human-centric lighting solutions, and the integration of artificial intelligence for predictive maintenance and optimization. The automotive sector presents a particularly promising opportunity as vehicle manufacturers increasingly incorporate smart lighting systems for enhanced safety and aesthetic appeal.

Smart Lighting Market Growth Trends - Current and emerging trends shaping the market

The smart lighting market is experiencing several transformative trends that are reshaping its trajectory. One prominent trend is the convergence of lighting systems with other building technologies, creating unified platforms for energy management, security, and environmental monitoring. The adoption of Li-Fi technology, which uses light waves for high-speed data transmission, represents an innovative application of smart lighting infrastructure. Another significant trend is the shift toward human-centric lighting that adjusts color temperature and intensity to support circadian rhythms and enhance occupant well-being. The market is also witnessing increased demand for tunable white lighting solutions that offer customizable color temperatures for different applications and times of day. Wireless mesh networking technologies are gaining traction due to their scalability and ease of installation, while the integration of voice assistants and smartphone apps for lighting control continues to expand user accessibility. Additionally, the emergence of as-a-service business models for lighting systems, where customers pay for illumination rather than hardware, is disrupting traditional sales approaches and lowering barriers to adoption.

COVID-19 Impact on the Smart Lighting Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a mixed impact on the smart lighting market, initially causing disruptions in supply chains, project delays, and reduced capital expenditure across commercial and industrial sectors. The global lockdowns and economic uncertainty led to temporary slowdowns in new installations and renovations, particularly in hospitality, retail, and office spaces. However, the pandemic also accelerated certain trends that benefited the smart lighting market. Increased focus on building health and safety drove demand for UV-C disinfection lighting systems and occupancy monitoring solutions. The shift toward remote work and hybrid office models created opportunities for smart lighting systems that optimize energy usage in partially occupied buildings. As economies recover, the market is witnessing a rebound driven by infrastructure stimulus packages, renewed emphasis on energy efficiency, and the acceleration of digital transformation initiatives. The recovery trajectory shows strong momentum, with many delayed projects resuming and new opportunities emerging in healthcare facilities, educational institutions, and residential developments that prioritize health, safety, and operational efficiency.

Smart Lighting Market Competitive Landscape - Major competitors and market consolidation

The smart lighting market features a diverse competitive landscape with established lighting manufacturers, technology companies, and emerging startups vying for market share. Major players like Signify (formerly Philips Lighting), Acuity Brands, and Zumtobel leverage their extensive lighting expertise and global distribution networks to maintain leadership positions. Technology giants such as Honeywell and Panasonic bring advanced connectivity and IoT capabilities to the market, while specialized companies like Lutron and Legrand focus on premium control systems and integration solutions. The competitive landscape is characterized by strategic partnerships, acquisitions, and collaborations aimed at expanding product portfolios and technological capabilities. Market consolidation is evident as larger companies acquire innovative startups to access new technologies and enter emerging application areas. Competition is intensifying in areas such as wireless protocols, with companies supporting multiple standards including Zigbee, Bluetooth Mesh, and proprietary solutions. The market also sees competition from regional players who offer localized solutions and pricing advantages in their respective markets, creating a dynamic environment where innovation, customer service, and ecosystem development are key differentiators.

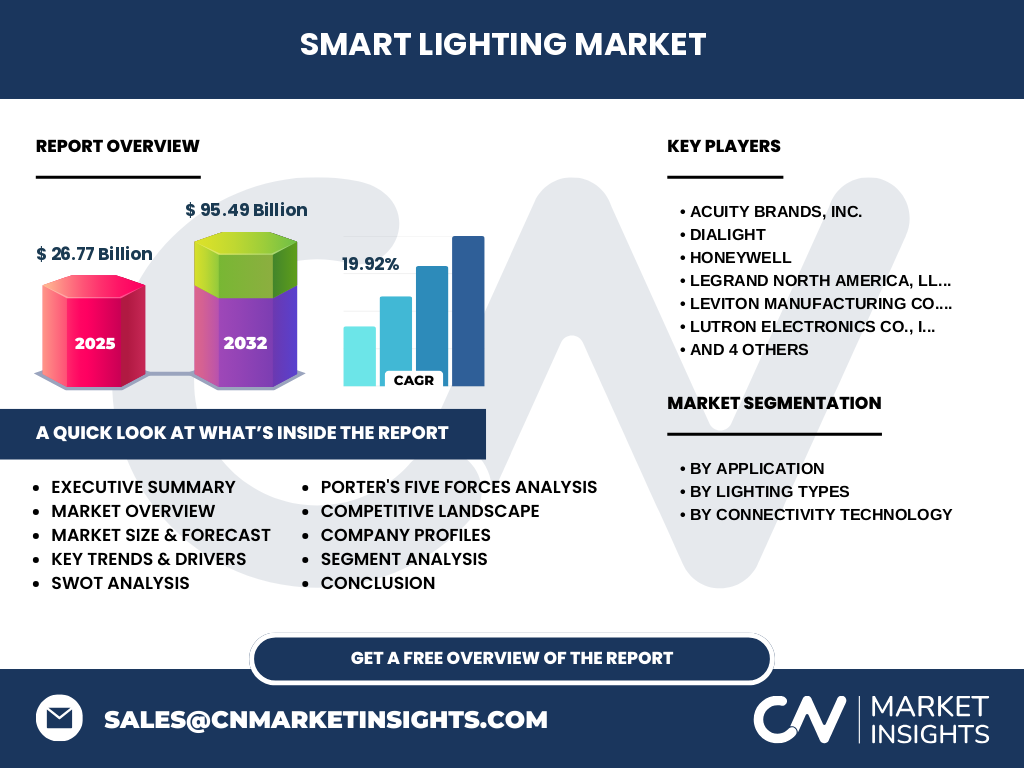

Executive Summary - High-level overview and key findings about Smart Lighting Market

The smart lighting market represents a dynamic and rapidly evolving sector within the broader lighting and building automation industries. With a market size of $26.77 billion in 2025 and projected to reach $95.49 billion by 2032, growing at a CAGR of 19.92%, the market demonstrates exceptional growth potential driven by technological advancements and increasing demand for energy-efficient solutions. The market's expansion is fueled by the convergence of LED technology, IoT connectivity, and intelligent control systems across diverse applications including residential, commercial, industrial, outdoor, government, and automotive sectors. Key findings indicate that wireless connectivity solutions are gaining preference due to installation flexibility, while LED-based systems dominate the lighting types segment. The competitive landscape is characterized by both established lighting manufacturers and technology companies entering the space, creating a rich ecosystem of solutions. Despite challenges related to initial costs and interoperability, the market's trajectory remains positive, supported by smart city initiatives, sustainability mandates, and the growing recognition of lighting's role in occupant well-being and operational efficiency. The market's future appears promising, with emerging technologies like Li-Fi and human-centric lighting opening new avenues for growth and differentiation.

The smart lighting market is segmented across multiple dimensions, with each segment exhibiting distinct growth patterns and market dynamics. By application, the commercial lighting segment currently dominates the market, driven by the need for energy efficiency and intelligent building management in office spaces, retail environments, and hospitality venues. The residential segment is experiencing rapid growth as smart home adoption increases and consumers seek convenience and energy savings. Industrial lighting applications are expanding due to the integration of lighting systems with manufacturing automation and safety protocols. Government applications benefit from smart city initiatives and public infrastructure modernization programs, while outdoor lighting is growing with the adoption of adaptive street lighting and connected urban infrastructure. The automotive lighting segment represents an emerging opportunity as vehicles incorporate advanced lighting systems for safety and aesthetics. By lighting types, LED lamps dominate due to their energy efficiency, long lifespan, and compatibility with smart controls. The market also segments by connectivity technology, with wireless solutions gaining traction for their ease of installation and scalability, though wired systems remain important in applications requiring maximum reliability and security.

Global Smart Lighting Market Size and Share by Region - Geographic distribution

The global smart lighting market exhibits significant regional variations in adoption rates, market maturity, and growth trajectories. North America leads in market share, driven by early technology adoption, strong presence of key manufacturers, and extensive smart city initiatives. The region's mature infrastructure and high disposable income levels support premium smart lighting solutions in both residential and commercial applications. Europe follows closely, with stringent energy efficiency regulations and ambitious sustainability targets driving market growth. Countries like Germany, the UK, and the Nordic nations are particularly advanced in smart lighting adoption, supported by government incentives and environmental awareness. The Asia-Pacific region represents the fastest-growing market, fueled by rapid urbanization, infrastructure development, and increasing investments in smart city projects across China, India, Japan, and Southeast Asian countries. The region's large population and growing middle class create substantial opportunities for residential smart lighting solutions. Latin America and the Middle East & Africa regions, while currently smaller markets, are showing promising growth as economic development accelerates and awareness of smart technologies increases. Regional differences in energy costs, regulatory frameworks, and technological infrastructure significantly influence market dynamics and adoption patterns across geographies.

Regional Analysis of the Smart Lighting Market - Detailed regional market performance

Regional analysis reveals distinct market characteristics and growth drivers across different geographies. In North America, the market benefits from advanced technological infrastructure, high consumer awareness, and supportive government policies promoting energy efficiency. The region's focus on smart buildings and connected cities drives demand for integrated lighting solutions that offer both energy savings and enhanced user experiences. Europe's market is characterized by strong regulatory frameworks such as the EU's Energy Efficiency Directive, which mandates significant reductions in energy consumption. The region's commitment to sustainability and carbon neutrality creates a favorable environment for smart lighting adoption, particularly in commercial and public sector applications. The Asia-Pacific region presents a unique combination of mature markets like Japan and South Korea, alongside rapidly developing economies such as China and India. This diversity creates opportunities across the value chain, from high-end smart lighting solutions in developed markets to cost-effective systems in emerging economies. Government initiatives like China's smart city program and India's Smart Cities Mission are major catalysts for market growth. The Middle East region, particularly the Gulf Cooperation Council countries, is investing heavily in smart city infrastructure, creating significant opportunities for advanced lighting systems. Latin America's market is growing steadily, supported by urbanization trends and increasing awareness of energy efficiency benefits, though economic volatility in some countries presents challenges.

Leading Company Profiles in the Smart Lighting Market - Industry players and strategies

The smart lighting market features several prominent companies with distinct strategic approaches and market positions. Signify (formerly Philips Lighting) stands as a global leader, leveraging its extensive lighting heritage and comprehensive product portfolio spanning professional, consumer, and connected lighting solutions. The company's strategy focuses on innovation in connected lighting and IoT integration, with strong emphasis on sustainability and circular economy principles. Acuity Brands has established itself as a dominant player in North America through its vertically integrated business model, combining lighting fixtures, controls, and IoT platforms under one roof. The company's strategy emphasizes data-driven solutions and building management integration. Lutron Electronics specializes in lighting control systems and has built a strong reputation for quality and innovation in both residential and commercial markets. Their strategy centers on premium positioning and ecosystem development through strategic partnerships. Honeywell approaches the market from a building automation perspective, integrating lighting with broader facility management solutions. Their strategy focuses on enterprise customers and comprehensive building management platforms. Legrand North America has carved a niche in electrical and digital building infrastructures, with smart lighting as a key component of their connected building solutions. The company's strategy emphasizes architectural integration and user experience. Other notable players like Zumtobel, Dialight, and Leviton bring specialized expertise in commercial, industrial, and residential applications respectively, each pursuing strategies that leverage their core competencies while expanding into connected lighting solutions.

Porter's Five Forces Analysis of the Smart Lighting Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the smart lighting market. The threat of new entrants remains moderate due to the capital requirements for R&D, manufacturing capabilities, and established distribution networks needed to compete effectively. However, the market is seeing increased startup activity in software and connectivity solutions, which face lower barriers to entry. The bargaining power of suppliers is relatively low for lighting components like LEDs, which are commodity products with multiple suppliers, but higher for specialized components such as advanced sensors and communication modules. The bargaining power of buyers varies significantly by segment; large commercial and industrial customers have substantial negotiating power due to bulk purchasing, while residential consumers have limited influence. The threat of substitute products is moderate, with traditional lighting systems still prevalent in many applications, though the superior energy efficiency and functionality of smart lighting systems are gradually reducing this threat. Competitive rivalry is intense, with numerous players competing on technology, price, and integration capabilities. The market is witnessing consolidation as larger companies acquire innovative startups, while established players differentiate through ecosystem development, service offerings, and vertical integration. Overall, the market presents opportunities for differentiation through innovation, customer service, and comprehensive solution offerings.

SWOT Analysis of the Smart Lighting Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the smart lighting market reveals several key factors influencing its development. Strengths include the proven energy efficiency benefits of LED technology, the growing maturity of IoT and wireless communication protocols, and the increasing consumer awareness of smart home technologies. The market also benefits from strong support from government initiatives promoting energy efficiency and smart city development. Weaknesses include the high initial costs of installation and the complexity of integrating smart lighting systems with existing infrastructure. Technical challenges such as interoperability between different systems and concerns about cybersecurity and data privacy also present significant weaknesses. Opportunities abound in emerging markets where urbanization is driving infrastructure development, in new application areas such as horticulture and healthcare, and in the development of advanced features like Li-Fi and human-centric lighting. The market also has opportunities to expand through as-a-service business models that lower adoption barriers. Threats include intense competition leading to price pressures, rapid technological changes that can quickly render products obsolete, and economic uncertainties that may delay infrastructure investments. Additionally, the market faces threats from regulatory changes, supply chain disruptions, and the potential for market saturation in mature regions. Despite these challenges, the market's fundamental strengths and the growing demand for energy-efficient, intelligent lighting solutions position it for continued growth.

Smart Lighting Market Value Chain Analysis - Industry structure and value flow

The smart lighting market value chain encompasses multiple stages, from raw material suppliers to end-users, with value added at each step. The chain begins with component suppliers providing essential elements such as LEDs, sensors, microcontrollers, and communication modules. These components are assembled by lighting fixture manufacturers who integrate them with control systems and software platforms. System integrators and distributors then play crucial roles in bringing these solutions to market, often providing installation, commissioning, and ongoing support services. At the value creation stage, significant innovation occurs in areas such as wireless connectivity protocols, energy management algorithms, and user interface design. Lighting manufacturers differentiate through product design, performance specifications, and compatibility with various control systems. System integrators add value through their expertise in designing and implementing comprehensive lighting solutions tailored to specific customer needs. The distribution channel has evolved to include traditional electrical distributors, specialized lighting showrooms, and increasingly, direct-to-consumer e-commerce platforms. Value is also created through after-sales services including maintenance, upgrades, and data analytics that optimize system performance over time. The emergence of lighting as a service (LaaS) models is further transforming the value chain by shifting the focus from product sales to outcome-based solutions, where customers pay for illumination rather than hardware, creating new revenue streams and business opportunities across the value chain.

Key Investment Insights in the Smart Lighting Market - Strategic investment recommendations

The smart lighting market presents compelling investment opportunities driven by its strong growth trajectory and technological innovation. Strategic investments should focus on companies that demonstrate leadership in key growth areas such as wireless connectivity solutions, human-centric lighting, and integrated building management systems. Companies with strong intellectual property portfolios in areas like advanced control algorithms, energy optimization, and data analytics are particularly attractive investment targets. The market also offers opportunities in emerging applications such as Li-Fi technology, horticultural lighting, and UV-C disinfection systems, which represent high-growth niches with significant differentiation potential. Investors should consider companies that have established strong partnerships and ecosystems, as the market increasingly moves toward integrated solutions rather than standalone products. Geographic diversification is another important consideration, with strong growth prospects in the Asia-Pacific region balanced against the stability and maturity of North American and European markets. Companies that offer lighting as a service models present interesting investment opportunities, as these models can provide recurring revenue streams and lower adoption barriers for customers. Additionally, investments in companies that prioritize sustainability and circular economy principles align with growing environmental regulations and consumer preferences. The market's consolidation trend also creates opportunities for strategic acquisitions and roll-up strategies, particularly for private equity investors looking to build comprehensive lighting solution providers.

Smart Lighting Market Conclusion - Summary and key takeaways

The smart lighting market stands at the intersection of several powerful trends including energy efficiency, IoT connectivity, and intelligent building management, positioning it for sustained growth over the coming years. With a projected CAGR of 19.92% from 2025 to 2032, the market demonstrates exceptional potential, driven by technological advancements and increasing awareness of the benefits of intelligent lighting systems. The market's expansion is supported by diverse applications across residential, commercial, industrial, outdoor, government, and automotive sectors, each contributing to overall growth while presenting unique opportunities and challenges. Key takeaways include the dominance of LED technology, the growing preference for wireless connectivity solutions, and the increasing integration of lighting systems with broader building management platforms. While challenges such as high initial costs and interoperability issues persist, the market's fundamental drivers remain strong, supported by smart city initiatives, sustainability mandates, and the growing recognition of lighting's role in occupant well-being and operational efficiency. The competitive landscape is dynamic, with both established players and innovative startups contributing to rapid technological advancement. As the market matures, success will increasingly depend on companies' ability to offer comprehensive, integrated solutions that address specific customer needs while navigating the complexities of a rapidly evolving technological landscape.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology combining primary and secondary research approaches to ensure accuracy and reliability. Primary research involved interviews with industry experts, including executives from leading smart lighting companies, system integrators, and technology providers. These interviews provided valuable insights into market trends, competitive dynamics, and future growth opportunities. Secondary research encompassed extensive review of company annual reports, industry publications, technical journals, and market databases to gather quantitative and qualitative data. The research methodology included detailed analysis of market segmentation, regional variations, and competitive landscapes through both bottom-up and top-down approaches. Data triangulation techniques were employed to validate findings across multiple sources, ensuring consistency and reliability. The market size and forecast figures were derived using historical data analysis, consideration of market drivers and restraints, and expert opinions on future market developments. The research also incorporated analysis of patent filings, product launches, and strategic developments to understand technological trends and competitive positioning. Special attention was given to emerging technologies and their potential impact on market dynamics. The methodology ensured comprehensive coverage of all market segments while maintaining focus on key growth drivers and potential challenges that could influence future market performance.

Research Scope - Coverage and limitations

This research report covers the global smart lighting market with a focus on key applications, technologies, and geographic regions that drive market dynamics. The scope encompasses six major application segments: industrial lighting, residential lighting, commercial lighting, government applications, outdoor lighting, and automotive lighting. The research also examines two primary lighting types: Light Emitting Diode (LED) lamps and traditional lighting technologies including fluorescent, compact fluorescent, and high-intensity discharge lamps. Connectivity technology analysis includes both wired and wireless solutions, with particular attention to emerging wireless protocols and their adoption patterns. Geographic coverage spans North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa regions, providing a comprehensive global perspective. The research timeframe extends from 2025 to 2032, with 2025 as the base year for market size calculations and historical data used to establish growth trends. Limitations of the research include the availability of detailed regional market data for certain emerging economies, potential variations in technology adoption rates across different market segments, and the challenge of accurately forecasting the impact of emerging technologies that may disrupt current market dynamics. The research also acknowledges the difficulty in quantifying certain market factors such as the impact of regulatory changes and the pace of smart city development across different regions.

Key Companies and Recent Developments in the Smart Lighting Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The smart lighting market features several key companies that are driving innovation and shaping industry trends through strategic developments and product launches. Signify (formerly Philips Lighting) continues to lead with its Philips Hue consumer lighting system and professional Interact platform, recently announcing expanded capabilities in human-centric lighting and enhanced connectivity with third-party smart home ecosystems. The company has also made significant strides in sustainability, committing to carbon-neutral operations and circular lighting solutions. Acuity Brands has strengthened its position through the acquisition of innovative startups and the launch of new IoT platforms that integrate lighting with building management systems. Their recent developments include advanced sensory networks embedded in lighting fixtures for occupancy detection and air quality monitoring. Lutron Electronics has expanded its residential offerings with new wireless protocols and enhanced integration with popular voice assistants, while maintaining its premium positioning in commercial lighting controls. Honeywell has leveraged its building automation expertise to develop comprehensive smart lighting solutions that integrate with broader facility management platforms, with recent announcements focusing on AI-driven energy optimization. Legrand North America has expanded its connected building portfolio through strategic acquisitions and the development of new wireless lighting control solutions. Zumtobel has focused on architectural lighting solutions with advanced connectivity features, recently launching new tunable white lighting systems for commercial applications. These companies, along with other key players like Dialight, Leviton, and Savant Technologies, continue to drive market evolution through ongoing innovation, strategic partnerships, and expansion into emerging application areas.