Building Automation System Market Overview - Definition, scope, and significance

A Building Automation System (BAS) is an intelligent, integrated network of hardware and software that monitors and controls a building's mechanical, electrical, and plumbing systems. These systems manage HVAC (heating, ventilation, and air conditioning), lighting, security, fire safety, and other critical building functions through centralized control. The scope of BAS encompasses commercial buildings, industrial facilities, and residential properties, creating smart environments that optimize energy consumption, enhance occupant comfort, and improve operational efficiency. The significance of BAS lies in its ability to reduce energy costs by up to 30%, extend equipment lifespan, provide real-time monitoring and diagnostics, and create sustainable buildings that meet modern environmental standards and occupant expectations.

Building Automation System Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Building Automation System market is primarily driven by increasing energy costs, stringent government regulations on energy efficiency, and growing demand for smart building technologies. The push for sustainable construction and green building certifications has accelerated BAS adoption across commercial and industrial sectors. However, the market faces restraints including high initial installation costs, complex integration with legacy systems, and cybersecurity concerns regarding connected building systems. Major challenges include skilled workforce shortages for system installation and maintenance, interoperability issues between different vendors' systems, and the need for continuous software updates and security patches. Opportunities abound in emerging markets, retrofitting existing buildings with modern BAS, integration with IoT and AI technologies, and the growing trend of net-zero energy buildings that require sophisticated automation systems.

Building Automation System Market Growth Trends - Current and emerging trends shaping the market

The Building Automation System market is experiencing several transformative trends that are reshaping the industry landscape. Cloud-based BAS platforms are gaining traction, offering remote monitoring, predictive maintenance, and enhanced data analytics capabilities. The integration of artificial intelligence and machine learning enables systems to learn occupant behavior patterns and optimize building operations automatically. Wireless sensor networks are replacing traditional wired systems, reducing installation costs and complexity. Mobile applications for building management are becoming standard, allowing facility managers to control systems from anywhere. Edge computing is emerging as a key trend, processing data locally to reduce latency and enhance security. Additionally, the convergence of IT and OT (operational technology) is creating more sophisticated, interconnected building ecosystems that can communicate with smart grid systems and participate in demand response programs.

COVID-19 Impact on the Building Automation System Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the Building Automation System market through supply chain interruptions, project delays, and reduced capital expenditures as building owners focused on immediate health and safety concerns. However, the pandemic also accelerated certain market trends, particularly the demand for advanced ventilation systems, touchless controls, and air quality monitoring capabilities. The shift toward remote work created new opportunities for home automation systems and highlighted the importance of flexible building management solutions. As buildings reopened, there was increased investment in systems that could monitor occupancy levels, ensure proper ventilation, and maintain healthy indoor environments. The market is now on a recovery trajectory, with pent-up demand for new construction projects and retrofitting existing buildings with modern BAS to meet post-pandemic health and safety standards.

Building Automation System Market Competitive Landscape - Major competitors and market consolidation

The Building Automation System market features a mix of established industrial giants and specialized technology companies competing for market share. The competitive landscape is characterized by strategic partnerships, mergers and acquisitions, and continuous innovation in product offerings. Major players are expanding their portfolios through vertical integration, offering complete building management solutions rather than individual components. Competition is intensifying in emerging markets where local players are challenging established multinational corporations. The market is witnessing consolidation as larger companies acquire smaller, innovative firms to enhance their technological capabilities and expand their geographic presence. Competition is also driven by the need for open protocols and interoperability standards, with companies developing solutions that can integrate with multiple building systems and third-party applications.

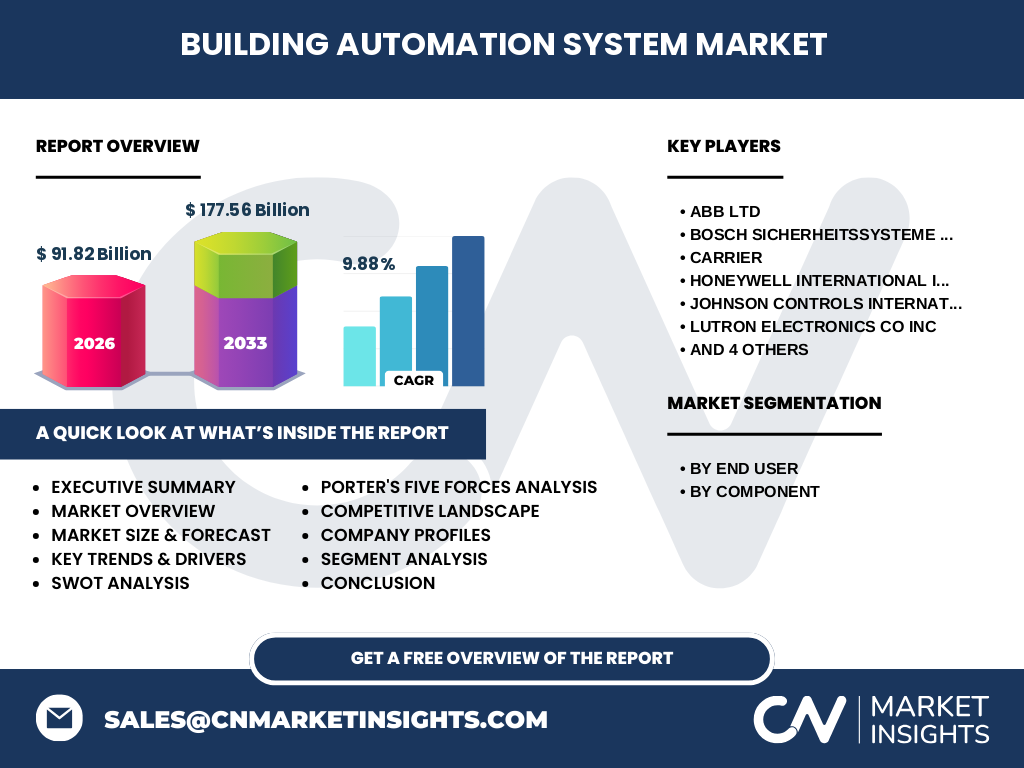

Executive Summary - High-level overview and key findings about Building Automation System Market

The Building Automation System market represents a dynamic and rapidly evolving industry with substantial growth potential. The market is experiencing robust expansion driven by increasing urbanization, rising energy costs, and the global push toward sustainable building practices. Key findings indicate that commercial buildings dominate the market, followed by industrial and residential segments, with hardware components currently representing the largest share of the market. The market is characterized by technological advancements in IoT, AI, and cloud computing, which are transforming traditional building management into intelligent, data-driven operations. North America and Europe lead in market adoption due to strict energy regulations and high awareness, while Asia-Pacific is emerging as the fastest-growing region due to rapid urbanization and infrastructure development. The market's compound annual growth rate of 9.88% reflects strong momentum and promising future prospects.

Building Automation System Market Forecast - Projections for 2025-2032 period

The Building Automation System market is projected to experience substantial growth from 2025 through 2032, with the market size expected to reach 177.56 Billion by 2033, up from 91.82 Billion in 2026. This represents a compound annual growth rate of 9.88% over the forecast period. The growth trajectory is supported by increasing global construction activities, particularly in emerging economies, and the ongoing modernization of existing building infrastructure. The forecast period will likely see accelerated adoption of advanced technologies such as AI-driven predictive maintenance, 5G-enabled smart buildings, and blockchain-based energy management systems. Market expansion will be driven by the increasing focus on energy efficiency, government initiatives promoting green buildings, and the rising demand for integrated security and building management solutions. The residential segment is expected to witness the highest growth rate as smart home technologies become more affordable and mainstream.

Building Automation System Market Size and Share by Segmentation - Breakdown by {segmentData}

The Building Automation System market is segmented by end user and component categories, each showing distinct growth patterns and market dynamics. By end user, the commercial segment currently dominates the market, accounting for the largest share due to extensive adoption in office buildings, retail spaces, hospitals, and educational institutions. This segment benefits from high energy consumption and the need for sophisticated building management systems to ensure occupant comfort and operational efficiency. The industrial segment represents the second-largest share, driven by manufacturing facilities, data centers, and warehouses that require precise environmental control and energy management. The residential segment, while currently smaller, is experiencing the fastest growth rate as smart home technologies become more accessible and affordable to consumers. By component, hardware currently holds the largest market share, encompassing controllers, sensors, actuators, and other physical devices essential for building automation. However, the software and services segment is expected to witness the highest growth rate as buildings become more connected and require sophisticated management platforms and ongoing support services.

Global Building Automation System Market Size and Share by Region - Geographic distribution

The global Building Automation System market exhibits varying adoption rates and growth patterns across different geographic regions. North America currently holds the largest market share, driven by stringent energy efficiency regulations, high awareness of sustainable building practices, and the presence of major technology providers. The region's mature construction industry and focus on smart city initiatives continue to drive BAS adoption. Europe represents the second-largest market, characterized by strict environmental regulations, high energy costs, and strong government support for green building initiatives. The Asia-Pacific region is emerging as the fastest-growing market, fueled by rapid urbanization, increasing construction activities, and growing awareness of energy conservation in countries like China, India, and Southeast Asian nations. The Middle East and Africa region is experiencing steady growth, particularly in the Gulf Cooperation Council countries where there is significant investment in smart city projects and sustainable infrastructure. Latin America is showing promising growth potential, driven by economic development and increasing adoption of modern building technologies in commercial and residential sectors.

Regional Analysis of the Building Automation System Market - Detailed regional market performance

Regional market performance in the Building Automation System industry varies significantly based on economic development, regulatory frameworks, and technological adoption rates. In North America, the market is characterized by early adoption of advanced technologies, strong emphasis on energy efficiency, and integration with smart grid systems. The region benefits from well-established building codes and incentives for green building certifications. Europe's market is driven by ambitious carbon reduction targets, with countries like Germany, UK, and Nordic nations leading in sustainable building practices. The region's focus on building renovation and retrofitting older structures presents significant opportunities for BAS providers. Asia-Pacific's market is expanding rapidly due to massive infrastructure development, particularly in China and India, where smart city initiatives are creating substantial demand for integrated building management systems. The region's diverse economic landscape creates opportunities across different market segments, from luxury commercial buildings to affordable residential solutions. Middle East markets are characterized by high-end commercial and hospitality projects, while Latin American markets are growing through increased awareness and gradual adoption of modern building technologies.

Leading Company Profiles in the Building Automation System Market - Industry players and strategies

The Building Automation System market is dominated by several key players who have established strong market positions through technological innovation, comprehensive product portfolios, and global presence. ABB Ltd has positioned itself as a leader in industrial automation and smart building solutions, focusing on energy management and IoT integration. Bosch Sicherheitssysteme GmbH leverages its expertise in security systems to offer comprehensive building management solutions that integrate safety and automation. Carrier, known for its HVAC systems, has expanded into complete building automation, emphasizing energy efficiency and occupant comfort. Honeywell International Inc stands out for its broad portfolio spanning commercial and residential solutions, with strong emphasis on cloud-based platforms and analytics. Johnson Controls International has built its reputation on integrated building management systems and smart building technologies. Lutron Electronics Co Inc specializes in lighting control systems and has expanded into comprehensive building automation. Mitsubishi Electric Corporation brings strong engineering capabilities and innovative solutions for commercial and industrial applications. Schneider Electric has established itself as a leader in energy management and automation, offering end-to-end building solutions. Siemens AG provides comprehensive building technologies with strong focus on digitalization and smart infrastructure. Trane Technologies, while traditionally focused on HVAC, has expanded into complete building automation solutions with emphasis on sustainability and energy efficiency.

Porter's Five Forces Analysis of the Building Automation System Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the Building Automation System market. The threat of new entrants is moderate due to high initial capital requirements, the need for technical expertise, and established relationships between major players and building developers. However, the market is witnessing increased competition from startups offering innovative, cloud-based solutions that challenge traditional players. The bargaining power of buyers is increasing as building owners and facility managers become more knowledgeable about BAS technologies and demand integrated, cost-effective solutions. Supplier power varies across the value chain, with component manufacturers having moderate bargaining power, while software providers and system integrators maintain stronger positions. The threat of substitutes is relatively low as BAS provides unique value in energy management and operational efficiency that standalone systems cannot match. Competitive rivalry is intense among established players, characterized by price competition, technological innovation, and strategic partnerships to expand market reach and capabilities.

SWOT Analysis of the Building Automation System Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Building Automation System market reveals key internal and external factors influencing market dynamics. Strengths include the proven ability to reduce energy costs by up to 30%, enhance building occupant comfort, and provide valuable data insights for facility management. The technology's maturity and reliability, combined with growing standardization in protocols and interfaces, represent significant advantages. Weaknesses include high initial installation costs, complexity in integrating with legacy systems, and ongoing cybersecurity vulnerabilities in connected systems. The need for specialized training and maintenance also presents challenges for widespread adoption. Opportunities abound in emerging markets, retrofitting existing buildings, and the integration of advanced technologies like AI, IoT, and 5G. The growing focus on sustainability and green building certifications creates additional demand for sophisticated BAS solutions. Threats include economic downturns affecting construction spending, rapid technological changes that could render existing systems obsolete, and increasing cybersecurity risks as buildings become more connected. Regulatory changes and potential supply chain disruptions also pose ongoing challenges to market growth.

Building Automation System Market Value Chain Analysis - Industry structure and value flow

The Building Automation System market value chain encompasses multiple stages from component manufacturing to end-user implementation and support. The chain begins with component manufacturers who produce sensors, controllers, actuators, and other hardware elements essential for BAS functionality. These components are integrated by system integrators who design and configure complete building automation solutions tailored to specific building requirements. Software developers create the management platforms, analytics tools, and user interfaces that enable building operators to monitor and control systems effectively. Distributors and wholesalers play a crucial role in supplying products to contractors and installers who implement the systems in buildings. Value-added resellers often provide additional services such as system customization and specialized support. The chain extends to maintenance and support services, which are critical for ensuring system performance and longevity. Each stage of the value chain contributes to the overall value proposition, with successful companies often operating across multiple stages to capture more value and provide comprehensive solutions to customers.

Key Investment Insights in the Building Automation System Market - Strategic investment recommendations

Strategic investment in the Building Automation System market should focus on several key areas to maximize returns and capture emerging opportunities. Investors should prioritize companies developing cloud-based and IoT-enabled BAS platforms that offer scalability and remote management capabilities. There is significant potential in solutions that integrate energy management with renewable energy systems and smart grid technologies. Investment in cybersecurity solutions specifically designed for building automation systems is becoming increasingly critical as connected buildings face growing security threats. The residential smart home segment represents an attractive investment opportunity, particularly companies offering affordable, user-friendly solutions that appeal to mass-market consumers. Retrofitting existing buildings with modern BAS presents substantial investment potential, especially in regions with aging building infrastructure. Companies focusing on AI and machine learning applications for predictive maintenance and energy optimization are well-positioned for future growth. Additionally, investments in companies developing open protocols and interoperable solutions will benefit from the industry's shift toward integrated building ecosystems.

Building Automation System Market Conclusion - Summary and key takeaways

The Building Automation System market stands at a pivotal juncture, characterized by robust growth, technological innovation, and increasing global adoption. The market's impressive compound annual growth rate of 9.88%, with projections reaching 177.56 Billion by 2033, underscores the strong momentum and promising future prospects. Key takeaways include the market's resilience demonstrated through pandemic recovery, the accelerating trend toward smart, connected buildings, and the critical role of energy efficiency in driving adoption. The competitive landscape features established players continuously innovating while facing challenges from agile startups offering cloud-based solutions. Regional variations highlight opportunities in emerging markets while mature markets focus on advanced technologies and system integration. The convergence of IoT, AI, and cloud computing is transforming building management from basic automation to intelligent, data-driven operations. As sustainability becomes increasingly important and energy costs continue to rise, the Building Automation System market is well-positioned for sustained growth, offering significant opportunities for technology providers, building owners, and investors alike.

Research Methodology - How this research was conducted

This comprehensive Building Automation System market research was conducted using a rigorous methodology combining primary and secondary research approaches. Primary research involved interviews with industry experts, including system integrators, building owners, technology providers, and market analysts to gather firsthand insights into market trends, challenges, and opportunities. Secondary research encompassed extensive review of company annual reports, industry publications, government databases, and market research reports to validate findings and establish market size and growth projections. Data triangulation was employed to cross-verify information from multiple sources, ensuring accuracy and reliability. The research methodology included both top-down and bottom-up approaches to estimate market size, with detailed segmentation analysis to understand specific market dynamics across different end-user categories and geographic regions. Market forecasting was based on historical growth patterns, current market conditions, and future growth drivers, with careful consideration of potential market restraints and challenges.

Research Scope - Coverage and limitations

This research report covers the Building Automation System market comprehensively, focusing on key segments including commercial, industrial, and residential end users, as well as hardware and software/service components. The geographic scope encompasses major global regions including North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America, providing a balanced view of regional market dynamics and growth opportunities. The research timeline covers historical data, current market conditions, and future projections through 2033, offering a complete perspective on market evolution. Limitations of this research include the availability of consistent data across all regions, particularly in emerging markets where formal reporting structures may be less developed. Additionally, rapid technological changes in the industry may affect the accuracy of long-term projections. The research focuses primarily on established BAS technologies and may not fully capture emerging innovations that could significantly impact the market in the future. Currency fluctuations and regional economic variations also present challenges in creating truly comparable regional analyses.

Key Companies and Recent Developments in the Building Automation System Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Building Automation System market features several leading companies that continue to shape industry trends through innovative product launches, strategic partnerships, and technological advancements. ABB Ltd has recently announced expanded cloud-based building management platforms with enhanced AI capabilities for predictive maintenance and energy optimization. Bosch Sicherheitssysteme GmbH launched new integrated security and building automation solutions that combine video surveillance with environmental control systems. Carrier introduced advanced HVAC systems with built-in automation features and improved connectivity for smart building integration. Honeywell International Inc unveiled next-generation building management platforms with enhanced mobile applications and cloud-based analytics capabilities. Johnson Controls International announced strategic partnerships with major technology companies to enhance their IoT and AI offerings in building automation. Lutron Electronics Co Inc launched new wireless lighting control systems with improved energy monitoring and integration capabilities. Mitsubishi Electric Corporation introduced innovative building management solutions with advanced energy storage integration for commercial applications. Schneider Electric expanded its EcoStruxure Building platform with new features for sustainability reporting and energy optimization. Siemens AG announced the development of digital twin technology for building management, enabling virtual building modeling and optimization. Trane Technologies launched new connected HVAC systems with advanced automation features and improved energy efficiency ratings. These developments reflect the industry's focus on digitalization, energy efficiency, and integrated building management solutions.