Cyber Insurance Market Overview - Definition, scope, and significance

Cyber insurance is a specialized form of insurance coverage designed to protect businesses and individuals from internet-based risks and information technology infrastructure, operations, and activities. This insurance typically covers expenses related to first-party losses such as data destruction, extortion, hacking, and data theft, as well as third-party liability for network security and privacy breaches. The market has grown significantly as organizations face increasing cyber threats, regulatory compliance requirements, and the potential for substantial financial losses from data breaches. With the digital transformation of businesses across all sectors, cyber insurance has become an essential component of risk management strategies for organizations of all sizes.

Cyber Insurance Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The cyber insurance market is driven by several key factors including the rising frequency and sophistication of cyber attacks, increasing regulatory requirements for data protection, growing awareness of cyber risks among businesses, and the expanding digital footprint of organizations. The COVID-19 pandemic has accelerated digital transformation, creating new vulnerabilities and driving demand for coverage. However, the market faces restraints such as the complexity of underwriting cyber risks, lack of historical data for pricing models, and the evolving nature of cyber threats. Challenges include accurately assessing risk exposure, managing catastrophic events, and addressing coverage gaps. Opportunities exist in emerging markets, innovative policy structures, and the integration of risk management services with insurance products.

Cyber Insurance Market Growth Trends - Current and emerging trends shaping the market

The cyber insurance market is experiencing several notable growth trends, including the shift from packaged to standalone policies, the expansion of coverage to address emerging risks such as ransomware and social engineering fraud, and the integration of cybersecurity services with insurance offerings. There is a growing trend toward customized policies that address specific industry risks, with particular attention to high-risk sectors such as healthcare and financial services. The market is also seeing increased adoption of parametric insurance products that provide rapid payouts based on predefined triggers. Additionally, insurers are leveraging advanced analytics, artificial intelligence, and machine learning to improve risk assessment and pricing models, while also developing partnerships with cybersecurity firms to offer comprehensive risk management solutions.

COVID-19 Impact on the Cyber Insurance Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has had a profound impact on the cyber insurance market, accelerating both the demand for coverage and the evolution of cyber risks. The rapid shift to remote work created new vulnerabilities, leading to an increase in cyber attacks and data breaches. This surge in claims has prompted insurers to reassess their underwriting practices, with many implementing stricter policy terms, higher premiums, and more comprehensive risk assessments. The pandemic has also highlighted the need for coverage related to business interruption caused by cyber events. As organizations continue to adapt to hybrid work models and increased digital reliance, the market is expected to maintain strong growth, with insurers developing more sophisticated products to address the evolving threat landscape.

Cyber Insurance Market Competitive Landscape - Major competitors and market consolidation

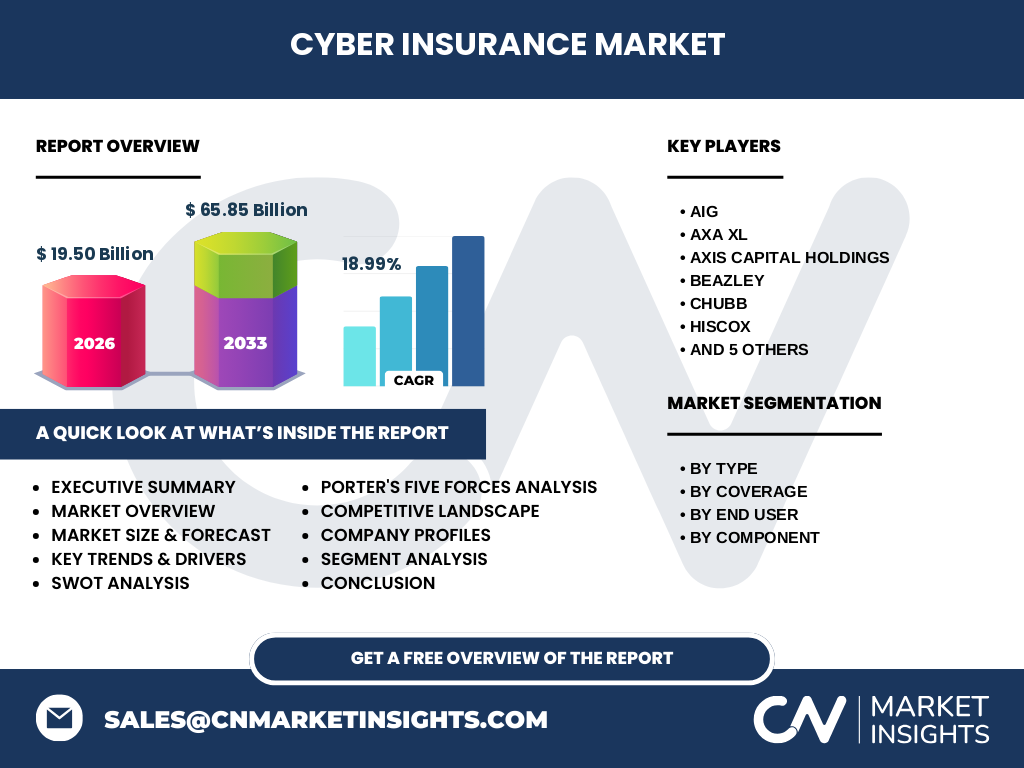

The cyber insurance market features a mix of traditional insurance carriers, specialty insurers, and reinsurers competing for market share. Major players include AIG, AXA XL, AXIS Capital Holdings, Beazley, Chubb, Hiscox, Munich Re, The Hartford, Travelers, and Zurich, among others. The competitive landscape is characterized by product innovation, strategic partnerships, and mergers and acquisitions. Companies are differentiating themselves through specialized expertise in specific industries, innovative coverage options, and value-added services such as risk assessment and cybersecurity consulting. The market has seen some consolidation as larger insurers acquire specialty cyber insurance providers to expand their capabilities and market presence. Competition is intensifying as new entrants, including technology companies and insurtech startups, seek to disrupt the traditional insurance model with digital-first approaches.

Executive Summary - High-level overview and key findings about Cyber Insurance Market

The cyber insurance market is experiencing robust growth, driven by increasing cyber threats, regulatory pressures, and growing awareness of digital risks. The market is projected to grow from $19.50 billion in 2026 to $65.85 billion by 2033, representing a compound annual growth rate of 18.99%. This growth is fueled by the expansion of coverage options, the emergence of standalone policies, and the increasing sophistication of cyber attacks. The market is characterized by strong demand across all end-user segments, with particular emphasis on healthcare, BFSI, and retail sectors. As organizations continue to digitize their operations and face mounting cyber risks, cyber insurance is becoming an essential component of comprehensive risk management strategies. The competitive landscape is dynamic, with established insurers and new entrants vying for market share through product innovation and strategic partnerships.

Cyber Insurance Market Forecast - Projections for 2025-2032 period

The cyber insurance market is projected to experience significant growth over the forecast period from 2025 to 2032, with the market size expected to increase from $19.50 billion to $65.85 billion by 2033. This represents a compound annual growth rate of 18.99%, indicating strong momentum in the sector. The forecast reflects increasing demand for cyber insurance across all market segments, driven by the rising frequency and cost of cyber attacks, growing regulatory requirements, and the expanding digital footprint of businesses. The growth trajectory suggests that organizations are becoming more proactive in managing their cyber risks, recognizing the potential financial impact of data breaches and other cyber incidents. The forecast also indicates opportunities for insurers to develop more sophisticated products and services to meet evolving customer needs.

Cyber Insurance Market Size and Share by Segmentation - Breakdown by {segmentData}

The cyber insurance market can be segmented by type, coverage, end user, and component. By type, the market includes standalone and packaged policies, with standalone policies gaining traction due to their comprehensive coverage options. Coverage segments include data breach and cyber liability, addressing different aspects of cyber risk. End-user segments encompass healthcare, retail, BFSI, IT & telecom, and manufacturing, with healthcare and BFSI representing significant portions of the market due to their high-value data assets and regulatory requirements. The component segment includes solutions and services, with services such as risk assessment and incident response becoming increasingly important differentiators. Each segment is experiencing growth, though at varying rates depending on the specific risks and regulatory environments faced by different industries.

Global Cyber Insurance Market Size and Share by Region - Geographic distribution

The global cyber insurance market exhibits varying levels of maturity and adoption across different regions, influenced by factors such as regulatory environments, technological infrastructure, and awareness of cyber risks. North America currently represents the largest market share, driven by stringent data protection regulations, high awareness of cyber risks, and the presence of major insurance providers. Europe follows as the second-largest market, with growth fueled by GDPR requirements and increasing cyber incidents. The Asia-Pacific region is experiencing the fastest growth rate, attributed to rapid digital transformation, increasing internet penetration, and growing awareness of cyber risks among businesses. Latin America and the Middle East & Africa regions are also showing potential for growth, though at a slower pace due to varying levels of digital maturity and economic development.

Regional Analysis of the Cyber Insurance Market - Detailed regional market performance

Regional analysis of the cyber insurance market reveals distinct patterns of adoption and growth across different geographies. In North America, the market is characterized by high penetration rates, sophisticated policy offerings, and strong regulatory frameworks driving demand. The United States, in particular, leads in terms of market size and innovation in cyber insurance products. Europe's market is shaped by strict data protection regulations such as GDPR, with countries like the UK, Germany, and France showing significant adoption rates. The Asia-Pacific region presents a diverse landscape, with developed markets like Japan and Australia showing mature adoption while emerging economies in Southeast Asia are experiencing rapid growth in demand. Latin America's market is developing, with countries like Brazil and Mexico leading in adoption. The Middle East & Africa region shows potential for growth, particularly in Gulf Cooperation Council countries, though adoption remains relatively low in many areas due to varying levels of digital infrastructure and economic development.

Leading Company Profiles in the Cyber Insurance Market - Industry players and strategies

Leading companies in the cyber insurance market include AIG, AXA XL, AXIS Capital Holdings, Beazley, Chubb, Hiscox, Munich Re, The Hartford, Travelers, and Zurich. These companies have established strong market positions through comprehensive product offerings, specialized expertise, and extensive distribution networks. AIG has focused on developing industry-specific solutions and leveraging its global presence to serve multinational clients. AXA XL has emphasized innovation in policy structures and partnerships with cybersecurity firms. Beazley has built a reputation for expertise in complex cyber risks and incident response services. Chubb has leveraged its broad insurance portfolio to offer integrated risk management solutions. Hiscox has focused on the small and medium enterprise segment with tailored products. Munich Re provides reinsurance support and risk modeling expertise to primary insurers. The Hartford has emphasized customer service and claims handling. Travelers has developed strong capabilities in risk assessment and prevention services. Zurich has focused on digital distribution channels and data analytics to improve underwriting and pricing.

Porter's Five Forces Analysis of the Cyber Insurance Market - Competitive forces assessment

Porter's Five Forces analysis of the cyber insurance market reveals the following competitive dynamics: The threat of new entrants is moderate, as the market requires significant expertise in risk assessment and substantial capital investment, though insurtech startups are challenging traditional models. The bargaining power of buyers is increasing as organizations become more sophisticated in understanding their cyber risks and negotiating coverage terms. The threat of substitutes is low, as cyber insurance remains a unique solution for managing cyber risks, though internal risk management and cybersecurity measures can serve as alternatives. The competitive rivalry among existing insurers is high, characterized by product innovation, pricing pressure, and the race to develop comprehensive risk management solutions. The bargaining power of suppliers, primarily reinsurance providers and cybersecurity service partners, is moderate, as insurers rely on their expertise and capacity to underwrite complex cyber risks.

SWOT Analysis of the Cyber Insurance Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the cyber insurance market reveals several key factors. Strengths include growing market demand, increasing awareness of cyber risks, and the ability to offer value-added services beyond traditional insurance. Weaknesses encompass the complexity of underwriting cyber risks, lack of historical data for pricing models, and potential coverage gaps. Opportunities exist in emerging markets, innovative policy structures, integration of risk management services, and the development of parametric insurance products. Threats include the evolving nature of cyber threats, potential for catastrophic events that could overwhelm the market, regulatory changes that could impact coverage requirements, and competition from new business models such as self-insurance and captives. The market's ability to address these factors will determine its long-term success and sustainability.

Cyber Insurance Market Value Chain Analysis - Industry structure and value flow

The cyber insurance value chain consists of several key components that work together to deliver comprehensive coverage to customers. At the foundation are risk assessment and underwriting activities, where insurers evaluate potential exposures and determine appropriate coverage terms. This is supported by data analytics and risk modeling capabilities that help quantify cyber risks. The distribution channel includes brokers, agents, and direct sales teams that connect insurers with potential customers. Policy administration and claims management systems handle the operational aspects of insurance delivery. Value-added services such as risk assessment, employee training, and incident response support represent an increasingly important part of the value chain, differentiating insurers and providing additional revenue streams. Reinsurance partners provide capacity and risk sharing for large or complex risks. The value chain is evolving as insurers integrate cybersecurity services and leverage technology to improve efficiency and customer experience.

Key Investment Insights in the Cyber Insurance Market - Strategic investment recommendations

Key investment insights for the cyber insurance market highlight several strategic opportunities for growth and differentiation. Investors should consider the potential of emerging technologies such as artificial intelligence and machine learning to improve risk assessment and underwriting accuracy. There is significant opportunity in developing specialized products for high-growth sectors such as healthcare, manufacturing, and retail, where cyber risks are particularly acute. Investments in data analytics capabilities and partnerships with cybersecurity firms can enhance risk management services and create competitive advantages. The market for small and medium-sized enterprises represents an underserved segment with substantial growth potential. Geographic expansion into emerging markets, particularly in Asia-Pacific and Latin America, offers opportunities for first-mover advantages. Additionally, investments in digital distribution channels and customer experience improvements can drive market share growth and operational efficiency.

Cyber Insurance Market Conclusion - Summary and key takeaways

The cyber insurance market is positioned for substantial growth over the coming years, driven by increasing cyber threats, regulatory pressures, and growing awareness of digital risks. The market's projected expansion from $19.50 billion to $65.85 billion by 2033, at a CAGR of 18.99%, reflects the critical role that cyber insurance is playing in organizational risk management strategies. Key trends include the shift toward standalone policies, the integration of risk management services, and the development of innovative coverage options for emerging risks. The competitive landscape is dynamic, with established insurers and new entrants vying for market share through product innovation and strategic partnerships. As organizations continue to digitize their operations and face mounting cyber risks, the demand for comprehensive cyber insurance solutions is expected to remain strong, creating opportunities for insurers who can effectively address evolving customer needs.

Research Methodology - How this research was conducted

The research methodology for this cyber insurance market analysis involved a comprehensive approach combining primary and secondary research methods. Secondary research included analysis of industry reports, market data, regulatory filings, and company publications to establish market size, growth trends, and competitive landscape. Primary research involved interviews with industry experts, insurance professionals, and technology specialists to validate findings and gain insights into market dynamics. The research utilized both top-down and bottom-up approaches to estimate market size and validate segmentations. Data triangulation techniques were employed to ensure accuracy and reliability of the findings. The analysis considered various factors including technological advancements, regulatory changes, economic conditions, and competitive developments to provide a holistic view of the market. Limitations of the research include the rapidly evolving nature of the cyber insurance market and the potential for emerging risks to impact future projections.

Research Scope - Coverage and limitations

The research scope for this cyber insurance market analysis encompasses a comprehensive examination of the global market, including market size and forecast, segmentation by type, coverage, end user, and component, regional analysis, competitive landscape, and key trends. The analysis covers the period from 2025 to 2033, with historical data used to establish growth trajectories and future projections. The scope includes major market players, their strategies, and recent developments. However, the research has certain limitations, including the rapidly evolving nature of cyber risks and the potential for new threat vectors to emerge. The analysis is based on available data and may not capture all niche segments or emerging regional markets. Additionally, the research scope does not extend to detailed financial performance of individual companies beyond what is publicly available, and it may not fully account for the impact of potential disruptive technologies or regulatory changes that could significantly alter market dynamics.

Key Companies and Recent Developments in the Cyber Insurance Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Key companies in the cyber insurance market have been actively pursuing strategies to strengthen their market positions and address evolving customer needs. AIG has expanded its cyber insurance offerings with enhanced coverage for ransomware and business interruption, while also launching industry-specific solutions for sectors such as healthcare and manufacturing. AXA XL has announced partnerships with leading cybersecurity firms to integrate risk assessment services with insurance products, enhancing its value proposition to customers. AXIS Capital Holdings has developed innovative parametric cyber insurance products that provide rapid payouts based on predefined triggers, addressing the need for quick recovery from cyber incidents. Beazley has introduced new coverage options for emerging risks such as cryptocurrency theft and social engineering fraud, while also expanding its incident response services. Chubb has launched a suite of cyber insurance products specifically designed for small and medium-sized enterprises, addressing an underserved market segment. Hiscox has announced strategic partnerships with technology companies to improve its digital distribution capabilities and enhance customer experience. Munich Re has developed advanced risk modeling tools using artificial intelligence to improve underwriting accuracy and pricing models. The Hartford has expanded its cyber insurance offerings to include coverage for Internet of Things (IoT) risks and cloud service provider failures. Travelers has announced the acquisition of a specialized cyber risk management firm to enhance its service offerings and strengthen its market position. Zurich has launched a digital platform that integrates cyber insurance with risk management tools, providing customers with a comprehensive solution for managing their cyber exposures.