Cleanroom Technology Market Overview - Definition, scope, and significance

Cleanroom technology refers to the specialized engineering and operational practices designed to maintain controlled environments with extremely low levels of airborne particles, microbes, and chemical vapors. These controlled spaces are essential for industries where contamination could compromise product quality, research integrity, or patient safety. Cleanrooms achieve this through advanced air filtration systems, specialized construction materials, and strict protocols for personnel and equipment. The technology encompasses both the physical infrastructure (walls, ceilings, floors, air handling units) and the operational systems (HEPA/ULPA filtration, pressure differentials, temperature and humidity control) that create and maintain these controlled environments. The significance of cleanroom technology spans critical sectors including pharmaceuticals, biotechnology, semiconductor manufacturing, medical device production, and healthcare facilities, where even microscopic contamination can lead to product failures, regulatory violations, or compromised research outcomes.

Cleanroom Technology Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The cleanroom technology market is driven by several powerful forces including the expanding pharmaceutical and biotechnology sectors, increasing demand for sterile medical devices, and the growing complexity of semiconductor manufacturing processes. Stringent regulatory requirements from agencies like the FDA and EMA mandate controlled environments for many critical manufacturing processes, creating consistent demand. The rise of personalized medicine, cell and gene therapies, and advanced biologics requires increasingly sophisticated cleanroom facilities. However, the market faces restraints such as high initial capital investment costs, complex maintenance requirements, and the need for specialized technical expertise. Challenges include energy consumption concerns, the complexity of validating cleanroom performance, and adapting to evolving regulatory standards. Opportunities abound in emerging markets, the development of modular and portable cleanroom solutions, and innovations in energy-efficient designs. The integration of IoT and smart monitoring systems presents opportunities for enhanced contamination control and operational efficiency.

Cleanroom Technology Market Growth Trends - Current and emerging trends shaping the market

The cleanroom technology market is experiencing several transformative trends that are reshaping industry dynamics. Modular cleanroom construction is gaining popularity due to its flexibility, faster deployment, and cost-effectiveness compared to traditional built-in cleanrooms. The industry is witnessing a shift toward energy-efficient designs with advanced HVAC systems that reduce operational costs while maintaining stringent environmental controls. There's growing adoption of softwall cleanrooms in pharmaceutical and biotechnology applications due to their portability and scalability. The integration of automation and robotics is reducing human intervention in critical processes, thereby minimizing contamination risks. Another significant trend is the development of hybrid cleanroom systems that combine hardwall and softwall technologies to optimize performance and cost. The market is also seeing increased demand for pass-through cabinets and airlocks to maintain pressure differentials and prevent cross-contamination between different cleanroom classifications.

COVID-19 Impact on the Cleanroom Technology Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the cleanroom technology market, creating both immediate disruptions and long-term opportunities. Initial lockdowns and supply chain interruptions caused project delays and reduced new installations across many sectors. However, the pandemic simultaneously drove unprecedented demand for cleanroom technologies in vaccine development, pharmaceutical manufacturing, and medical device production. The accelerated development of COVID-19 vaccines and therapeutics required rapid expansion of cleanroom facilities worldwide. Hospitals and research laboratories invested heavily in enhanced contamination control systems. Looking at the recovery trajectory, the market is experiencing robust growth as postponed projects resume and new investments accelerate. The pandemic has heightened awareness about contamination control across industries, leading to sustained demand for cleanroom technologies beyond the immediate healthcare crisis. This increased focus on biosecurity and contamination prevention is expected to drive continued market expansion through 2025 and beyond.

Cleanroom Technology Market Competitive Landscape - Major competitors and market consolidation

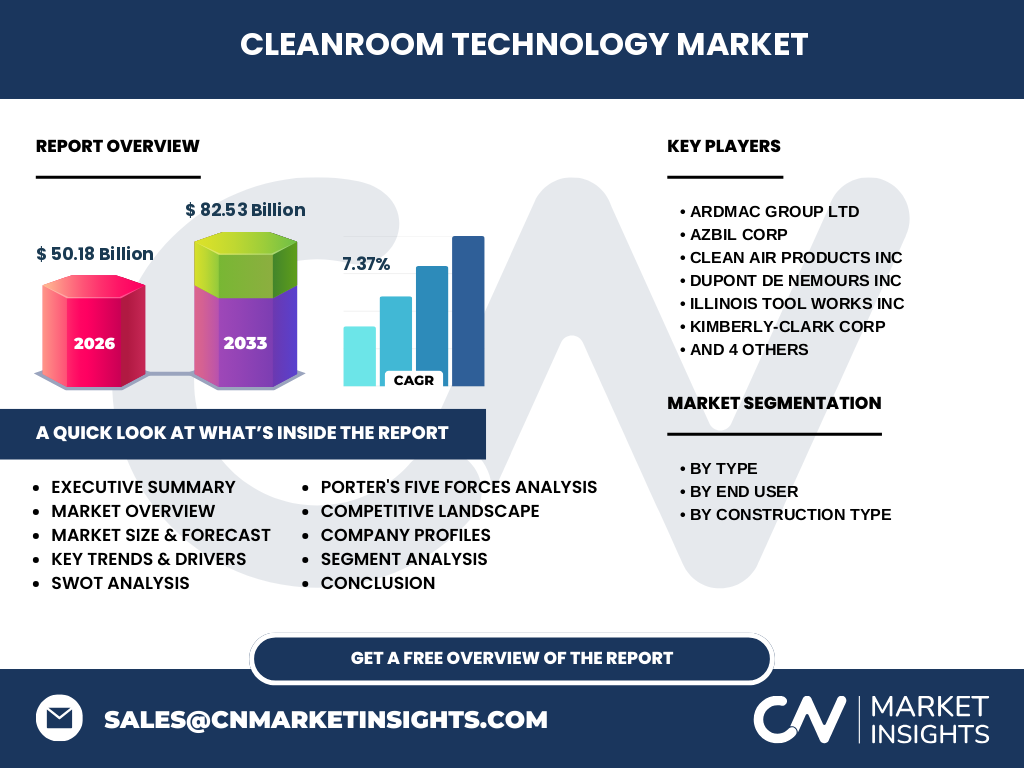

The cleanroom technology market features a moderately consolidated competitive landscape with several key players dominating the global market. Major competitors include Ardmac Group Ltd, Azbil Corp, Clean Air Products Inc, DuPont de Nemours Inc, Illinois Tool Works Inc, Kimberly-Clark Corp, Labconco Corp, M+W Group GmbH, Taikisha Ltd, and Terra Universal Inc. These companies compete across different segments of the value chain, from cleanroom construction and equipment to consumables and services. Market consolidation is occurring through strategic acquisitions, partnerships, and vertical integration strategies. Companies are expanding their product portfolios to offer comprehensive cleanroom solutions rather than individual components. Geographic expansion, particularly in emerging markets, is a key competitive strategy. The competitive intensity varies by segment, with equipment manufacturing being more consolidated than consumables, where numerous suppliers compete on price and quality. Innovation in energy efficiency, modular designs, and smart monitoring systems is becoming a key differentiator among competitors.

Executive Summary - High-level overview and key findings about Cleanroom Technology Market

The global cleanroom technology market represents a critical infrastructure sector supporting pharmaceutical, biotechnology, medical device, and electronics industries. With a market size of $50.18 billion in 2026 and projected to reach $82.53 billion by 2033, the market demonstrates robust growth at a CAGR of 7.37%. This growth is driven by increasing regulatory requirements, expanding pharmaceutical research and manufacturing, and technological advancements in contamination control. The market is segmented by type (equipment and consumables), end user (pharmaceutical, biotechnology, medical device manufacturers, hospitals, and microelectronics), and construction type (standard, hardwall, softwall cleanrooms, and pass-through cabinets). Key trends include the shift toward modular construction, energy-efficient designs, and the integration of smart monitoring systems. The competitive landscape features established players focusing on innovation and geographic expansion. Despite challenges related to high initial costs and complex maintenance, the market presents significant opportunities, particularly in emerging economies and for advanced applications in personalized medicine and semiconductor manufacturing.

Cleanroom Technology Market Forecast - Projections for 2025-2032 period

The cleanroom technology market is projected to experience substantial growth from 2025 through 2032, expanding from $50.18 billion in 2026 to $82.53 billion by 2033. This represents a compound annual growth rate of 7.37% over the forecast period. The growth trajectory is supported by several factors including continued expansion in pharmaceutical and biotechnology manufacturing, increasing semiconductor production capacity, and growing healthcare infrastructure investments globally. Equipment segments are expected to maintain strong growth as facilities upgrade to more energy-efficient and technologically advanced systems. The consumables segment will benefit from recurring demand for filters, garments, and cleaning supplies. Emerging markets in Asia-Pacific, Latin America, and the Middle East are projected to outpace developed markets in growth rate due to increasing industrialization and healthcare investments. The forecast also accounts for technological advancements in modular construction and smart monitoring systems that will drive replacement and upgrade cycles across existing facilities.

Cleanroom Technology Market Size and Share by Segmentation - Breakdown by {segmentData}

The cleanroom technology market is segmented by type, end user, and construction type, each contributing differently to the overall market size. By type, the market is divided into equipment and consumables segments. Equipment includes HVAC systems, HEPA filters, air diffusers, and monitoring systems, while consumables encompass garments, wipes, gloves, and cleaning agents. By end user, pharmaceutical companies represent the largest segment, followed by biotechnology firms, medical device manufacturers, hospitals, and microelectronics manufacturers. Each end user has distinct cleanroom requirements based on their contamination control needs and regulatory compliance. By construction type, the market includes standard cleanrooms, hardwall cleanrooms (permanent structures with rigid walls), softwall cleanrooms (flexible curtain systems), and pass-through cabinets (intermediary contamination control units). Hardwall cleanrooms currently dominate due to their durability and compliance with stringent regulations, while softwall cleanrooms are gaining traction for their flexibility and cost-effectiveness in less critical applications.

Global Cleanroom Technology Market Size and Share by Region - Geographic distribution

The global cleanroom technology market exhibits distinct regional characteristics and growth patterns across different geographic areas. North America currently holds the largest market share, driven by advanced pharmaceutical manufacturing, biotechnology research, and semiconductor production in the United States and Canada. Europe represents the second-largest market, with strong presence in countries like Germany, France, and the UK, supported by robust pharmaceutical industries and strict regulatory frameworks. The Asia-Pacific region is experiencing the fastest growth rate, fueled by expanding pharmaceutical manufacturing in China and India, growing semiconductor production in South Korea and Taiwan, and increasing healthcare infrastructure investments. Latin America and the Middle East & Africa represent emerging markets with significant growth potential, though from a smaller base. Regional variations in regulatory requirements, economic development, and industrial base create diverse market dynamics, with developed regions focusing on technological upgrades while emerging markets prioritize establishing basic cleanroom infrastructure.

Regional Analysis of the Cleanroom Technology Market - Detailed regional market performance

Regional market performance in the cleanroom technology sector varies significantly based on industrial development, regulatory environments, and economic factors. North America demonstrates mature market characteristics with steady growth driven by technological upgrades, replacement cycles, and expansion in biopharmaceutical manufacturing. The region benefits from advanced research infrastructure and stringent regulatory compliance requirements. Europe shows similar maturity with strong emphasis on energy efficiency and sustainability in cleanroom design. The region's pharmaceutical industry and medical device manufacturing drive consistent demand. Asia-Pacific exhibits dynamic growth patterns, with China and India emerging as manufacturing hubs for pharmaceuticals and electronics. South Korea and Taiwan lead in semiconductor-related cleanroom applications. The region benefits from lower production costs and government initiatives supporting industrial development. Latin America presents growth opportunities in pharmaceutical manufacturing and healthcare infrastructure, though economic volatility affects investment patterns. The Middle East & Africa region shows potential in healthcare and research applications, with Gulf Cooperation Council countries investing in advanced medical facilities and research centers.

Leading Company Profiles in the Cleanroom Technology Market - Industry players and strategies

The cleanroom technology market features several prominent companies with distinct strategic approaches and market positions. Ardmac Group Ltd specializes in cleanroom construction and engineering solutions, focusing on pharmaceutical and biotechnology facilities across Europe. Azbil Corp provides advanced control systems and automation solutions for cleanroom environments, leveraging its expertise in industrial automation. Clean Air Products Inc offers comprehensive cleanroom equipment including air showers, pass-throughs, and filtration systems, with strong presence in North America. DuPont de Nemours Inc brings material science expertise to cleanroom applications, particularly in protective apparel and surface materials. Illinois Tool Works Inc operates across multiple industrial segments, providing contamination control solutions through its various divisions. Kimberly-Clark Corp dominates the consumables segment with its protective apparel and cleaning products. Labconco Corp specializes in laboratory equipment including biological safety cabinets and fume hoods. M+W Group GmbH (now part of Exyte) focuses on high-tech facility construction including semiconductor and pharmaceutical cleanrooms. Taikisha Ltd provides comprehensive cleanroom solutions including design, construction, and maintenance services. Terra Universal Inc offers modular cleanroom systems and laboratory equipment with emphasis on customization and rapid deployment.

Porter's Five Forces Analysis of the Cleanroom Technology Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the cleanroom technology market. The threat of new entrants is moderate due to high capital requirements for manufacturing facilities and the need for specialized technical expertise. However, modular construction innovations have lowered barriers somewhat for new construction-focused companies. Bargaining power of buyers is moderate to high, particularly for large pharmaceutical companies that can negotiate volume discounts and influence product specifications. The bargaining power of suppliers varies by segment; for specialized equipment components, supplier power is moderate, while for commodity materials it remains low. The threat of substitutes is relatively low as cleanroom technology has unique requirements that cannot be easily replaced by alternative solutions. Competitive rivalry is intense among established players, characterized by price competition, technological innovation, and service differentiation. Companies compete on reliability, energy efficiency, compliance with regulations, and after-sales support. Geographic expansion and vertical integration strategies are common responses to competitive pressures.

SWOT Analysis of the Cleanroom Technology Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the cleanroom technology market reveals key strategic factors. Strengths include the essential nature of cleanroom technology for critical industries, established regulatory frameworks driving consistent demand, and continuous technological advancements improving efficiency and effectiveness. The market benefits from diverse applications across multiple industries, reducing dependence on any single sector. Weaknesses include high initial investment costs that can deter smaller companies, complex maintenance requirements demanding specialized expertise, and vulnerability to economic downturns affecting capital expenditure. Opportunities abound in emerging markets where industrialization and healthcare infrastructure development are accelerating, the growing biopharmaceutical sector requiring advanced contamination control, and technological innovations in modular and energy-efficient designs. Threats include economic uncertainty affecting capital investment decisions, potential regulatory changes creating compliance challenges, and competitive pressure from both established players and new entrants offering innovative solutions. The market also faces threats from supply chain disruptions and raw material price volatility.

Cleanroom Technology Market Value Chain Analysis - Industry structure and value flow

The cleanroom technology market value chain encompasses multiple interconnected stages from raw material suppliers to end users. At the foundation, raw material suppliers provide specialized materials including high-grade stainless steel, polymers, HEPA/ULPA filter media, and cleanroom-compatible chemicals. Component manufacturers produce specialized parts such as air handling units, filtration systems, monitoring instruments, and control panels. System integrators combine these components into complete cleanroom solutions, handling design, engineering, and installation. Construction companies build the physical infrastructure, while equipment manufacturers produce specialized cleanroom machinery and tools. Service providers offer maintenance, validation, and certification services essential for regulatory compliance. Distributors and wholesalers facilitate product delivery to end users. The end-user segment includes pharmaceutical companies, biotechnology firms, medical device manufacturers, semiconductor producers, and research institutions. Value is added at each stage through technological innovation, quality improvements, and service enhancements. The value chain is characterized by both vertical integration among large players and specialized niche providers focusing on specific segments or technologies.

Key Investment Insights in the Cleanroom Technology Market - Strategic investment recommendations

Investment insights for the cleanroom technology market highlight several strategic opportunities for stakeholders. The market's projected growth to $82.53 billion by 2033 at a 7.37% CAGR indicates strong long-term investment potential. Key investment areas include modular cleanroom systems that offer flexibility and faster deployment, energy-efficient technologies addressing rising operational costs and sustainability concerns, and smart monitoring systems leveraging IoT and AI for enhanced contamination control. Investors should consider the growing biopharmaceutical sector, particularly cell and gene therapy manufacturing, which requires highly specialized cleanroom environments. Geographic expansion in emerging markets presents opportunities as healthcare infrastructure and pharmaceutical manufacturing capacity increase in Asia-Pacific, Latin America, and the Middle East. Companies investing in R&D for advanced filtration technologies, automated contamination control, and sustainable materials are likely to gain competitive advantages. Strategic partnerships and acquisitions can provide market entry or expansion opportunities, particularly for companies seeking to expand their geographic presence or technological capabilities.

Cleanroom Technology Market Conclusion - Summary and key takeaways

The cleanroom technology market represents a vital and growing sector supporting critical industries worldwide. With a projected market size of $82.53 billion by 2033 and a robust CAGR of 7.37%, the industry demonstrates strong fundamentals driven by pharmaceutical expansion, biotechnology advancements, and stringent regulatory requirements. The market's diverse segmentation across equipment, consumables, end users, and construction types provides multiple growth avenues and risk diversification. Regional dynamics show developed markets focusing on technological upgrades while emerging markets drive volume growth through new facility construction. Key trends including modular construction, energy efficiency, and smart monitoring systems are reshaping industry practices. Despite challenges related to high costs and complex maintenance, the market offers substantial opportunities in emerging economies, biopharmaceutical manufacturing, and advanced semiconductor production. Companies that innovate in energy efficiency, modular design, and integrated solutions while expanding in high-growth regions are best positioned to capture market share in this essential technology sector.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology combining primary and secondary research approaches. Secondary research involved extensive analysis of industry reports, company annual reports, regulatory filings, trade publications, and academic journals to establish baseline market data and trends. Primary research included interviews with industry experts, cleanroom technology manufacturers, end users in pharmaceutical and biotechnology sectors, and regulatory specialists to validate findings and gain insights into market dynamics. The research employed both top-down and bottom-up approaches to estimate market size, starting with macroeconomic indicators and industry-specific factors. Data triangulation was used to cross-verify information from multiple sources, ensuring accuracy and reliability. The forecast period analysis considered historical growth patterns, technological trends, regulatory developments, and economic indicators. Market segmentation was based on industry-standard classifications and validated through expert consultations. The research methodology ensured comprehensive coverage of the cleanroom technology market while maintaining analytical rigor and objectivity.

Research Scope - Coverage and limitations

This research report covers the global cleanroom technology market with a focus on key segments, regional dynamics, competitive landscape, and growth projections through 2033. The scope includes analysis of equipment and consumables, various end-user industries, and different construction types. Geographic coverage encompasses major markets in North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The research examines market drivers, restraints, opportunities, and challenges while providing detailed company profiles of leading industry players. Limitations of the research include the availability of detailed market data for certain emerging regions, the rapid pace of technological change that may affect long-term projections, and the proprietary nature of some competitive information that limits comprehensive competitive analysis. The research focuses on commercial cleanroom applications and does not extensively cover military, space, or highly specialized research applications. Currency fluctuations and regional economic variations may also impact the accuracy of long-term financial projections.

Key Companies and Recent Developments in the Cleanroom Technology Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The cleanroom technology market features several leading companies that have recently announced significant developments. Ardmac Group Ltd has expanded its European operations, securing contracts for advanced pharmaceutical cleanroom facilities in Ireland and the UK. The company has introduced new modular cleanroom solutions designed for rapid deployment in biotechnology applications. Azbil Corp has launched next-generation cleanroom control systems with enhanced IoT integration, allowing for real-time monitoring and predictive maintenance capabilities. The company has formed strategic partnerships with pharmaceutical companies to provide integrated contamination control solutions. Clean Air Products Inc has introduced energy-efficient air handling units with improved HEPA filtration efficiency, targeting the semiconductor and pharmaceutical markets. DuPont de Nemours Inc has expanded its protective apparel line with new fabric technologies offering enhanced comfort and contamination protection for cleanroom personnel. Illinois Tool Works Inc has acquired a specialized cleanroom equipment manufacturer to strengthen its contamination control portfolio. Kimberly-Clark Corp has launched biodegradable cleanroom wipes, addressing sustainability concerns in the industry. Labconco Corp has introduced advanced biological safety cabinets with improved energy efficiency and user interface. M+W Group GmbH has secured major contracts for semiconductor fabrication facility construction in Asia. Terra Universal Inc has expanded its modular cleanroom offerings with new softwall configurations designed for pharmaceutical applications. These developments reflect the industry's focus on energy efficiency, modular construction, and integrated smart technologies.