Radiation Oncology Market Overview - Definition, scope, and significance

Radiation oncology is a specialized field of medicine that uses high-energy radiation to treat cancer and other diseases. It encompasses various treatment modalities including external beam radiation therapy (EBRT), internal beam radiation therapy, and systemic radiation therapy. The market includes equipment manufacturers, software providers, healthcare facilities, and pharmaceutical companies involved in radiation treatment delivery. This field plays a critical role in modern cancer care, serving as both a primary treatment modality and an essential component of multimodal cancer treatment strategies. The significance of radiation oncology continues to grow as technological advancements improve treatment precision, reduce side effects, and expand the range of treatable conditions.

Radiation Oncology Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The radiation oncology market is driven by several key factors including the rising global cancer incidence, technological advancements in treatment delivery systems, and increasing healthcare expenditure. Growing awareness about early cancer detection and the expanding applications of radiation therapy beyond traditional cancer treatment create substantial growth opportunities. However, the market faces restraints such as high treatment costs, limited access to advanced technologies in developing regions, and the shortage of skilled radiation oncologists. Challenges include managing complex treatment planning, ensuring quality assurance, and addressing patient concerns about radiation exposure. Opportunities exist in developing emerging markets, expanding telemedicine applications, and integrating artificial intelligence for treatment planning and delivery optimization.

Radiation Oncology Market Growth Trends - Current and emerging trends shaping the market

The radiation oncology market is experiencing several transformative trends. The adoption of advanced technologies such as intensity-modulated radiation therapy (IMRT), volumetric modulated arc therapy (VMAT), and stereotactic body radiation therapy (SBRT) is accelerating. There is increasing integration of artificial intelligence and machine learning for treatment planning, image guidance, and adaptive radiation therapy. The trend toward hypofractionated radiation therapy is gaining momentum, offering patients shorter treatment courses with comparable efficacy. Personalized medicine approaches are becoming more prevalent, with treatment plans tailored to individual patient characteristics. Additionally, the market is witnessing growing interest in proton therapy and other particle therapy modalities, though cost remains a significant barrier to widespread adoption.

COVID-19 Impact on the Radiation Oncology Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly impacted the radiation oncology market, causing treatment delays, reduced patient volumes, and operational disruptions in healthcare facilities. Many elective procedures were postponed, and cancer screening rates declined, potentially leading to more advanced disease presentations. However, the pandemic also accelerated certain positive developments, including the adoption of telemedicine for patient consultations, remote treatment planning capabilities, and enhanced infection control protocols. As healthcare systems recover, the market is experiencing a rebound with pent-up demand for cancer treatments. The pandemic has also highlighted the importance of resilient healthcare infrastructure and may lead to increased investment in radiation oncology capabilities to better handle future healthcare crises.

Radiation Oncology Market Competitive Landscape - Major competitors and market consolidation

The radiation oncology market features a competitive landscape with several major players including Elekta AB, Varian Medical Systems Inc, and IBA Worldwide (Ion Beam Applications SA) dominating the equipment manufacturing segment. These companies compete on technological innovation, product portfolio breadth, and service offerings. The market has seen some consolidation through mergers and acquisitions, particularly as companies seek to expand their technological capabilities and geographic presence. Competition extends beyond equipment manufacturers to include software providers, healthcare facilities, and pharmaceutical companies. Companies are increasingly focusing on integrated solutions that combine hardware, software, and services to provide comprehensive treatment systems. The competitive landscape is characterized by ongoing research and development investments, strategic partnerships, and efforts to improve treatment accessibility and affordability.

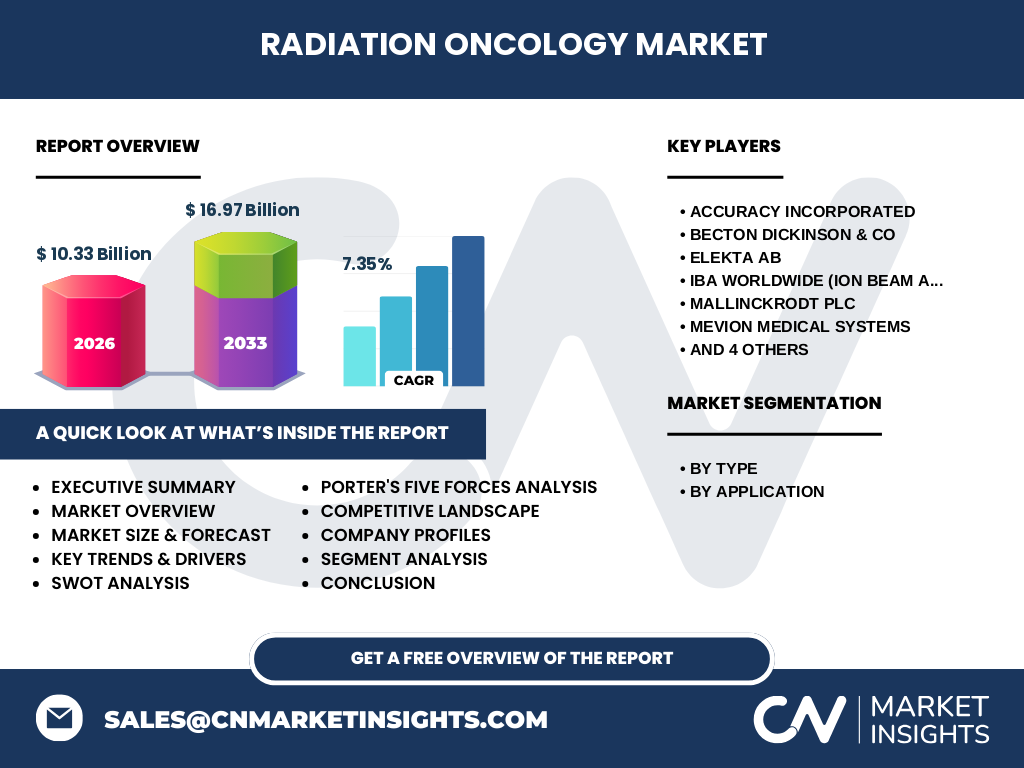

Executive Summary - High-level overview and key findings about Radiation Oncology Market

The radiation oncology market is positioned for substantial growth, driven by increasing cancer prevalence, technological advancements, and expanding treatment applications. The market is expected to grow from $10.33 billion in 2026 to $16.97 billion by 2033, representing a compound annual growth rate of 7.35%. Key growth segments include external beam radiation therapy and applications for breast, prostate, and lung cancers. The competitive landscape features established players investing heavily in innovation while facing challenges related to cost, access, and skilled workforce availability. The COVID-19 pandemic has reshaped market dynamics, accelerating digital transformation while highlighting healthcare system vulnerabilities. Overall, the market presents significant opportunities for stakeholders who can navigate technological complexity, address cost barriers, and expand access to radiation therapy services globally.

Radiation Oncology Market Forecast - Projections for 2025-2032 period

The radiation oncology market is projected to experience steady growth from 2025 to 2032, with the market size expected to reach $16.97 billion by 2033 from $10.33 billion in 2026. This represents a compound annual growth rate of 7.35% over the forecast period. The growth trajectory is supported by increasing cancer incidence globally, technological advancements in treatment delivery systems, and expanding applications of radiation therapy. External beam radiation therapy is expected to maintain its market dominance, while internal beam radiation therapy applications are anticipated to grow at a faster rate. By application, breast cancer and prostate cancer segments are projected to remain the largest contributors to market revenue, with lung cancer and head & neck cancer applications showing robust growth potential. Geographic expansion in emerging markets will be a key driver of overall market growth.

Radiation Oncology Market Size and Share by Segmentation - Breakdown by {segmentData}

The radiation oncology market segmentation reveals distinct patterns in technology adoption and application preferences. By type, external beam radiation therapy currently dominates the market due to its widespread availability and versatility in treating various cancer types. This segment benefits from continuous technological improvements in linear accelerators and treatment planning systems. Internal beam radiation therapy, while representing a smaller market share, is experiencing faster growth driven by advancements in brachytherapy techniques and applications. By application, breast cancer represents the largest segment due to high incidence rates and the effectiveness of radiation therapy in breast cancer treatment protocols. Prostate cancer follows as the second-largest application segment, with radiation therapy being a primary treatment option. Lung cancer, head & neck cancer, and cervical cancer represent significant but smaller market segments, each with specific technological and clinical considerations.

Global Radiation Oncology Market Size and Share by Region - Geographic distribution

The global radiation oncology market exhibits significant regional variations in market size, technology adoption, and growth rates. North America currently represents the largest regional market, driven by advanced healthcare infrastructure, high healthcare expenditure, and early technology adoption. Europe follows as the second-largest market, with strong government support for cancer care and established healthcare systems. The Asia-Pacific region is emerging as the fastest-growing market, fueled by rising cancer incidence, improving healthcare infrastructure, and increasing healthcare spending in countries like China and India. Latin America and the Middle East & Africa regions represent smaller but growing markets, facing challenges related to healthcare access and infrastructure development. Regional differences in reimbursement policies, regulatory frameworks, and economic conditions significantly influence market dynamics and growth patterns across different geographic areas.

Regional Analysis of the Radiation Oncology Market - Detailed regional market performance

Regional analysis reveals distinct market characteristics and growth patterns across different geographic areas. In North America, the market benefits from advanced technological infrastructure, favorable reimbursement policies, and high awareness about cancer treatment options. The region leads in adopting cutting-edge technologies such as proton therapy and advanced IMRT techniques. Europe demonstrates strong market performance with comprehensive cancer care networks and government initiatives supporting radiation oncology development. The Asia-Pacific region presents significant growth opportunities despite infrastructure challenges, with countries like Japan and South Korea being technology leaders while China and India offer substantial market expansion potential. Latin America faces healthcare access challenges but shows improving market conditions with increasing investment in cancer care infrastructure. The Middle East & Africa region has the smallest market share but presents opportunities for growth through international collaborations and targeted healthcare investments.

Leading Company Profiles in the Radiation Oncology Market - Industry players and strategies

The radiation oncology market features several leading companies with distinct strategic approaches and market positions. Elekta AB specializes in advanced radiation therapy solutions, focusing on innovative treatment systems and software for precision radiation delivery. Varian Medical Systems Inc offers comprehensive radiation oncology solutions including linear accelerators, treatment planning software, and services, with a strong emphasis on integration and user experience. IBA Worldwide (Ion Beam Applications SA) is a key player in particle therapy, particularly proton therapy systems, positioning itself in the high-end treatment segment. Other notable companies include Accuracy Incorporated, Becton Dickinson & Co, Mallinckrodt Plc, Mevion Medical Systems, NTP Radioisotopes, Nordion, Perspective Therapeutics Inc, and various regional players. These companies compete through technological innovation, strategic partnerships, geographic expansion, and service offerings, with strategies varying based on their core competencies and target market segments.

Porter's Five Forces Analysis of the Radiation Oncology Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the radiation oncology market. The threat of new entrants is moderate due to high capital requirements, regulatory barriers, and the need for specialized technical expertise. Bargaining power of suppliers is relatively low as equipment manufacturers have multiple component suppliers and can often vertically integrate. The bargaining power of buyers, primarily hospitals and cancer treatment centers, is moderate as they have multiple vendor options but face switching costs and training requirements. The threat of substitutes is low since radiation therapy remains a primary treatment modality for many cancers with limited alternatives for certain applications. Competitive rivalry is intense among major players, characterized by technological innovation, pricing pressures, and service differentiation efforts. Overall, the market structure supports ongoing innovation but creates challenges for new entrants and price-sensitive customers.

SWOT Analysis of the Radiation Oncology Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the radiation oncology market reveals key strategic factors. Strengths include advanced technological capabilities, proven clinical efficacy, and established treatment protocols that support market growth. The market benefits from strong scientific foundations and continuous innovation in treatment delivery systems. Weaknesses encompass high treatment costs, limited access in developing regions, and the shortage of specialized personnel. Opportunities exist in expanding applications of radiation therapy, emerging market growth, and technological advancements such as artificial intelligence integration. Threats include potential reimbursement cuts, competition from alternative treatment modalities, and regulatory challenges. The market also faces threats from economic downturns affecting healthcare spending and potential shifts in cancer treatment paradigms. Understanding these factors is crucial for stakeholders to develop effective strategies and capitalize on market opportunities.

Radiation Oncology Market Value Chain Analysis - Industry structure and value flow

The radiation oncology market value chain encompasses multiple stages from research and development through treatment delivery. The chain begins with component suppliers providing essential parts for radiation therapy equipment, followed by original equipment manufacturers who design and assemble treatment systems. Software developers create treatment planning and delivery optimization solutions that integrate with hardware systems. Distributors and service providers ensure equipment availability and maintenance support. Healthcare facilities, including hospitals and specialized cancer centers, represent the primary customers who purchase and operate radiation therapy equipment. Finally, patients receive treatment from radiation oncologists and medical physicists who utilize these systems. Value is created through technological innovation, improved treatment outcomes, and operational efficiency at each stage. The value chain is characterized by high capital requirements, specialized knowledge needs, and strong quality assurance requirements throughout the process.

Key Investment Insights in the Radiation Oncology Market - Strategic investment recommendations

Investment insights for the radiation oncology market highlight several strategic considerations for stakeholders. Technology development investments should focus on artificial intelligence integration, treatment automation, and precision medicine applications to address growing demand for personalized cancer care. Geographic expansion investments in emerging markets offer substantial growth potential, particularly in regions with improving healthcare infrastructure and rising cancer incidence. Companies should consider investments in training and education programs to address the shortage of skilled radiation oncology professionals. Strategic partnerships between equipment manufacturers, software developers, and healthcare providers can create integrated solutions that enhance market competitiveness. Investment in research and development remains crucial for maintaining technological leadership and addressing unmet clinical needs. Additionally, investments in cost-reduction technologies and treatment accessibility initiatives can help expand market reach and improve patient access to radiation therapy services.

Radiation Oncology Market Conclusion - Summary and key takeaways

The radiation oncology market presents a compelling growth opportunity with a projected market size increase from $10.33 billion in 2026 to $16.97 billion by 2033, representing a 7.35% CAGR. The market is driven by rising cancer incidence, technological advancements, and expanding treatment applications, while facing challenges related to cost, access, and skilled workforce availability. External beam radiation therapy dominates the market by type, with breast cancer and prostate cancer leading application segments. The competitive landscape features established players investing in innovation and strategic partnerships to maintain market positions. Regional variations in market development create diverse opportunities, with North America and Europe leading in technology adoption while Asia-Pacific offers the highest growth potential. Success in this market requires navigating technological complexity, addressing cost barriers, and expanding access to radiation therapy services globally. Stakeholders who can effectively address these challenges while capitalizing on emerging opportunities will be well-positioned for growth in this dynamic market.

Research Methodology - How this research was conducted

This research was conducted using a comprehensive methodology combining multiple data collection and analysis approaches. Primary research involved interviews with industry experts, healthcare providers, and market stakeholders to gather firsthand insights about market trends, challenges, and opportunities. Secondary research included analysis of industry reports, scientific publications, company financial statements, and regulatory documents to validate findings and provide market context. Market sizing was performed using both top-down and bottom-up approaches, starting with global cancer incidence data and treatment patterns to estimate radiation oncology market demand. Segmentation analysis considered technology types, applications, and geographic regions to provide detailed market insights. Data triangulation was employed to ensure accuracy and reliability of findings. The research also incorporated trend analysis and competitive assessment to provide a comprehensive market overview. All data points and projections were carefully validated against multiple sources to ensure research integrity.

Research Scope - Coverage and limitations

This research covers the global radiation oncology market from 2025 to 2032, focusing on key market segments, competitive landscape, and growth trends. The scope includes analysis of external beam and internal beam radiation therapy technologies, applications across major cancer types, and regional market performance. The research examines market drivers, restraints, and opportunities while providing detailed company profiles of major industry players. Geographic coverage includes North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa regions. However, the research has certain limitations, including the exclusion of detailed pricing analysis for individual products and services, limited coverage of emerging technologies still in early development stages, and the exclusion of certain niche applications due to data availability constraints. The research also focuses primarily on commercial market aspects and does not extensively cover academic or research institution perspectives. Despite these limitations, the research provides comprehensive coverage of the mainstream radiation oncology market and its key growth drivers.

Key Companies and Recent Developments in the Radiation Oncology Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The radiation oncology market features several key companies driving innovation and market growth. Elekta AB has announced advancements in adaptive radiation therapy and artificial intelligence integration for treatment planning. Varian Medical Systems Inc, recently acquired by Siemens Healthineers, continues to launch new linear accelerator models with enhanced imaging capabilities and treatment precision. IBA Worldwide (Ion Beam Applications SA) has expanded its proton therapy installations globally, with recent announcements about next-generation proton therapy systems. Accuracy Incorporated has introduced new software solutions for treatment planning optimization. Becton Dickinson & Co has expanded its portfolio through strategic acquisitions in radiation oncology technology. Mallinckrodt Plc has announced developments in radiopharmaceuticals for targeted radiation therapy. Mevion Medical Systems has launched compact proton therapy systems designed for easier installation and operation. NTP Radioisotopes continues to be a key supplier of medical isotopes for radiation therapy. Nordion has expanded its radiopharmaceutical manufacturing capabilities. Perspective Therapeutics Inc has announced new treatment delivery systems with enhanced automation features. These companies are actively engaged in product launches, strategic partnerships, and technological developments to strengthen their market positions and address evolving clinical needs.