1. Next Generation Data Storage Market Overview - Definition, scope, and significance

The Next Generation Data Storage Market encompasses advanced storage solutions designed to meet the escalating demands of modern data-driven enterprises. This market includes innovative technologies such as solid-state drives, network-attached storage systems, storage area networks, and cloud-based storage architectures that offer enhanced performance, scalability, and reliability compared to traditional storage methods. The significance of this market lies in its ability to support the exponential growth of data generated by businesses, governments, and individuals, enabling efficient data management, quick access, and secure storage across various sectors. As organizations increasingly adopt digital transformation strategies, the need for robust, high-capacity, and intelligent storage solutions has become critical for operational efficiency and competitive advantage.

2. Next Generation Data Storage Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Next Generation Data Storage Market is primarily driven by the rapid proliferation of data across industries, the increasing adoption of cloud computing, and the growing demand for real-time data analytics. The surge in IoT devices, artificial intelligence applications, and big data analytics has created an unprecedented need for high-performance storage solutions. However, the market faces restraints such as high initial investment costs, concerns over data security and privacy, and the complexity of integrating new storage systems with existing infrastructure. Challenges include managing energy consumption of data centers, ensuring data integrity, and addressing the skills gap in storage management. Opportunities abound in emerging technologies like NVMe, 5D optical storage, and DNA data storage, as well as in untapped markets in developing regions and vertical-specific solutions for industries like healthcare and financial services.

3. Next Generation Data Storage Market Growth Trends - Current and emerging trends shaping the market

The Next Generation Data Storage Market is witnessing several transformative trends that are reshaping the industry landscape. One of the most significant trends is the shift towards software-defined storage (SDS), which offers greater flexibility and scalability by separating storage software from hardware. Another emerging trend is the adoption of edge computing, necessitating distributed storage solutions that can process data closer to its source. The market is also seeing increased interest in AI-driven storage management, which optimizes data placement and enhances predictive maintenance. Additionally, there's a growing emphasis on sustainable storage solutions, with companies focusing on energy-efficient technologies and green data centers. The rise of hybrid cloud architectures is driving demand for solutions that seamlessly integrate on-premise and cloud storage, while advancements in storage-class memory (SCM) are blurring the lines between storage and memory, offering unprecedented performance improvements.

4. COVID-19 Impact on the Next Generation Data Storage Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has had a profound impact on the Next Generation Data Storage Market, initially causing supply chain disruptions and temporary manufacturing slowdowns. However, the crisis also accelerated digital transformation initiatives across industries, leading to increased demand for data storage solutions. The sudden shift to remote work and online services resulted in a surge in data generation, particularly in sectors such as e-commerce, telemedicine, and online education. This unexpected growth highlighted the importance of scalable and flexible storage solutions. As businesses adapted to the new normal, there was a notable increase in investments in cloud storage and edge computing to support distributed workforces. The recovery trajectory has been robust, with the market experiencing a V-shaped recovery as organizations continue to prioritize digital infrastructure. The pandemic has also underscored the critical nature of data backup and disaster recovery solutions, further driving market growth in these segments.

5. Next Generation Data Storage Market Competitive Landscape - Major competitors and market consolidation

The Next Generation Data Storage Market features a competitive landscape dominated by both established technology giants and innovative startups. Major players such as Dell Technologies, Hewlett Packard Enterprise, IBM, and NetApp continue to hold significant market share through their comprehensive product portfolios and strong brand recognition. These companies are increasingly focusing on integrated solutions that combine hardware, software, and services to provide end-to-end storage ecosystems. Meanwhile, specialized storage companies like Pure Storage and DataDirect Networks are gaining traction by offering high-performance, flash-based solutions tailored for specific use cases. The market is also witnessing strategic partnerships and acquisitions as companies seek to expand their capabilities and market reach. For instance, we're seeing collaborations between storage providers and cloud hyperscalers to deliver hybrid cloud solutions. Despite this consolidation, there remains ample opportunity for niche players to innovate and capture market share in specialized segments such as object storage or AI-optimized storage systems.

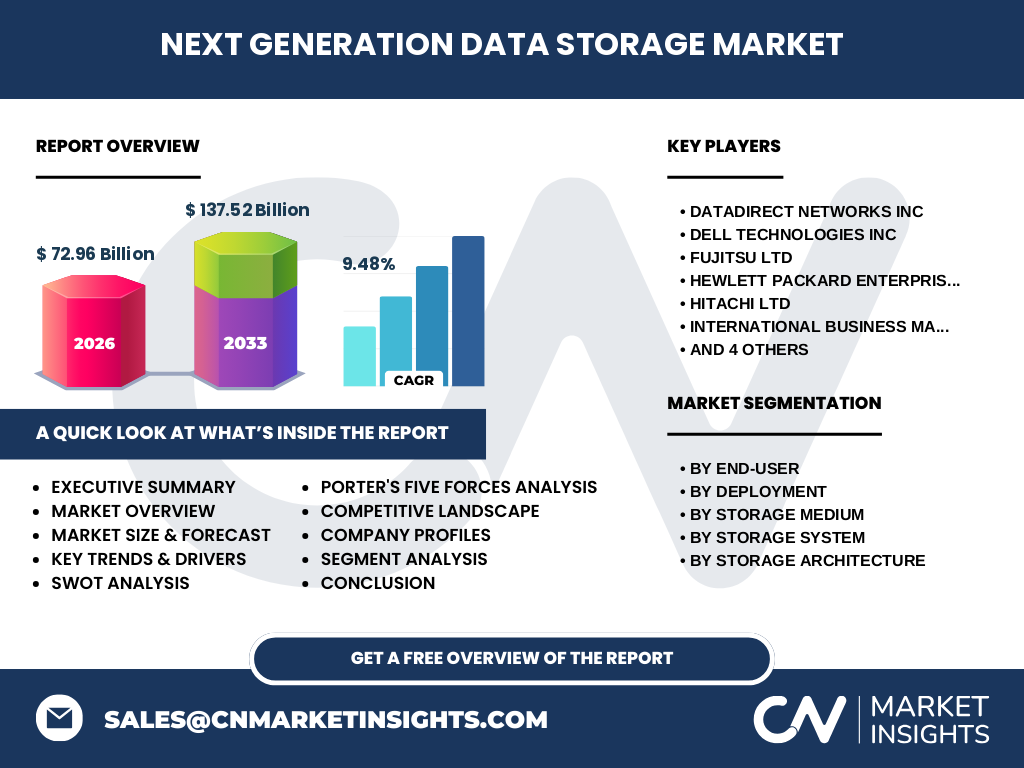

6. Executive Summary - High-level overview and key findings about Next Generation Data Storage Market

The Next Generation Data Storage Market is poised for substantial growth, driven by the exponential increase in data generation and the need for advanced storage solutions across industries. With a projected market size of 72.96 Billion by 2026 and a forecasted growth to 137.52 Billion by 2033, the market is expected to expand at a CAGR of 9.48% during the forecast period. This growth is fueled by the adoption of emerging technologies such as AI, IoT, and big data analytics, which require high-performance, scalable storage infrastructures. The market is characterized by a diverse range of storage mediums, including SSDs, HDDs, and tape storage, catering to various end-user needs across BFSI, retail, healthcare, and other sectors. Cloud-based and hybrid deployment models are gaining prominence, offering flexibility and cost-effectiveness. As organizations continue to prioritize digital transformation, the demand for intelligent, secure, and energy-efficient storage solutions is expected to remain strong, presenting significant opportunities for market players to innovate and expand their offerings.

7. Next Generation Data Storage Market Forecast - Projections for 2025-2032 period

The Next Generation Data Storage Market is projected to experience robust growth between 2025 and 2032, with the market size expected to reach 137.52 Billion by 2033, up from 72.96 Billion in 2026. This represents a compound annual growth rate (CAGR) of 9.48% over the forecast period. The growth trajectory is underpinned by several factors, including the continued expansion of cloud computing, the proliferation of IoT devices, and the increasing adoption of AI and machine learning technologies. As data generation continues to accelerate across all sectors, the demand for high-capacity, high-performance storage solutions is expected to remain strong. The forecast period is likely to see significant advancements in storage technologies, including the commercialization of new mediums such as DNA storage and further improvements in flash memory density and speed. Additionally, the growing emphasis on data security and compliance regulations is expected to drive investments in advanced storage solutions with built-in security features. The market is also likely to witness increased consolidation as larger players seek to acquire innovative startups to enhance their technology portfolios and expand their market presence.

8. Next Generation Data Storage Market Size and Share by Segmentation - Breakdown by {segmentData}

The Next Generation Data Storage Market can be segmented by various criteria, each offering unique insights into market dynamics and growth opportunities. By end-user, the market is divided into BFSI, retail, IT and telecom, healthcare, and media and entertainment sectors. The BFSI sector is expected to hold a significant share due to the critical need for secure and high-performance storage solutions to manage vast amounts of financial data and comply with regulatory requirements. In terms of deployment, cloud-based solutions are gaining traction, driven by their scalability and cost-effectiveness, while on-premise and hybrid deployments continue to serve organizations with specific security or latency requirements. Storage medium segmentation reveals a diverse landscape, with SSDs leading in performance-critical applications, HDDs maintaining relevance in cost-sensitive scenarios, and tape storage offering long-term archival solutions. Storage system segmentation includes Direct Attached Storage (DAS), Network Attached Storage (NAS), and Storage Area Networks (SAN), each catering to different use cases and performance requirements. Finally, the market is divided between file-object based storage and block storage architectures, with the former gaining popularity for its scalability and the latter remaining essential for high-performance applications.

9. Global Next Generation Data Storage Market Size and Share by Region - Geographic distribution

The global Next Generation Data Storage Market exhibits varying growth patterns and market shares across different regions, reflecting the diverse technological adoption rates and economic conditions worldwide. North America currently dominates the market, driven by the presence of major technology companies, early adoption of advanced storage solutions, and significant investments in data centers and cloud infrastructure. The region's strong focus on innovation and digital transformation across industries contributes to its leading position. Europe follows closely, with countries like Germany, the UK, and France showing robust growth in storage adoption, particularly in sectors such as automotive, manufacturing, and finance. The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, fueled by rapid digitalization in countries like China, India, and Japan, coupled with the expansion of cloud services and increasing data center construction. Latin America and the Middle East & Africa regions, while currently smaller markets, are showing promising growth potential as they continue to invest in digital infrastructure and adopt advanced storage technologies to support their growing economies.

10. Regional Analysis of the Next Generation Data Storage Market - Detailed regional market performance

Regional analysis of the Next Generation Data Storage Market reveals distinct characteristics and growth drivers across different geographical areas. In North America, the market is characterized by high technology adoption rates and significant investments in research and development. The region's strong presence of cloud service providers and data center operators drives demand for advanced storage solutions. Europe's market is influenced by strict data protection regulations such as GDPR, which impacts storage architecture and data management practices. The region is also seeing increased adoption of edge computing, particularly in manufacturing and automotive sectors. Asia-Pacific presents a dynamic market with rapid growth, led by countries like China, which is investing heavily in domestic technology infrastructure. The region's large population and growing digital economy create substantial demand for scalable storage solutions. Japan and South Korea are at the forefront of storage technology innovation, particularly in high-density and energy-efficient solutions. Emerging markets in Latin America and the Middle East & Africa are gradually adopting advanced storage technologies, driven by digital transformation initiatives and the need to manage growing data volumes in sectors such as oil and gas, telecommunications, and government services.

11. Leading Company Profiles in the Next Generation Data Storage Market - Industry players and strategies

The Next Generation Data Storage Market is populated by a mix of established technology giants and innovative specialists, each employing distinct strategies to capture market share. Dell Technologies leverages its comprehensive portfolio, offering solutions ranging from consumer-grade storage to enterprise-class data center infrastructure. The company's strategy focuses on integrated solutions that combine hardware, software, and services. Hewlett Packard Enterprise (HPE) emphasizes its strengths in hybrid cloud and edge computing, positioning its storage solutions as part of a broader IT ecosystem. IBM continues to innovate in areas such as AI-driven storage management and quantum computing, targeting enterprise customers with complex data needs. NetApp has carved out a niche in cloud-connected storage, offering solutions that seamlessly integrate on-premise and cloud environments. Pure Storage differentiates itself through its all-flash storage arrays, targeting performance-critical applications. Emerging players like DataDirect Networks focus on high-performance computing and AI workloads, while Huawei Technologies is expanding its presence in the Asia-Pacific region with a full range of storage products. These companies are increasingly forming strategic partnerships and pursuing mergers and acquisitions to enhance their technology portfolios and expand into new markets.

12. Porter's Five Forces Analysis of the Next Generation Data Storage Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the Next Generation Data Storage Market. The threat of new entrants is moderate, as the market requires significant capital investment and technical expertise, creating barriers to entry. However, the rapid pace of technological change and the emergence of innovative startups keep this threat alive. The bargaining power of buyers is high, given the commoditization of certain storage products and the availability of multiple suppliers. Large enterprise customers can negotiate favorable terms and demand customized solutions. Suppliers' bargaining power varies; while component suppliers for common technologies have limited power, specialized component providers for cutting-edge storage technologies can exert significant influence. The threat of substitutes is moderate, with emerging technologies like cloud storage and software-defined storage offering alternatives to traditional storage solutions. However, the unique performance characteristics of certain storage systems limit direct substitution. Competitive rivalry in the market is intense, driven by rapid technological advancements, price pressures, and the need for continuous innovation. Companies compete on performance, reliability, scalability, and total cost of ownership, leading to ongoing product development and strategic partnerships.

13. SWOT Analysis of the Next Generation Data Storage Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Next Generation Data Storage Market reveals key internal and external factors influencing its trajectory. Strengths of the market include the continuous technological innovation driving performance improvements, the growing demand for data storage across all industries, and the presence of established players with strong R&D capabilities. The market also benefits from the increasing adoption of cloud computing and the proliferation of data-generating devices. However, weaknesses exist in the form of high capital requirements for advanced storage technologies and the complexity of integrating new solutions with legacy systems. There's also a growing skills gap in managing advanced storage architectures. Opportunities abound in emerging technologies such as AI-driven storage management, quantum storage, and DNA data storage, as well as in untapped markets in developing regions. The market can also capitalize on the increasing focus on data security and compliance regulations. Threats include intense price competition, which can erode profit margins, and the rapid pace of technological change, which can quickly render existing solutions obsolete. Additionally, concerns over data privacy and the potential for disruptive technologies from unexpected sources pose ongoing challenges to market players.

14. Next Generation Data Storage Market Value Chain Analysis - Industry structure and value flow

The value chain of the Next Generation Data Storage Market encompasses a complex network of activities and stakeholders, each contributing to the final delivery of storage solutions to end-users. At the foundation of the value chain are raw material suppliers and component manufacturers, providing essential elements such as semiconductors, magnetic materials, and specialized hardware components. These feed into the production of storage devices by original equipment manufacturers (OEMs), who design and assemble storage systems ranging from individual drives to large-scale data center solutions. The next layer includes system integrators and solution providers who combine storage hardware with software, offering customized solutions to meet specific customer needs. Value-added resellers (VARs) and distributors play a crucial role in bridging the gap between manufacturers and end-users, providing local support and expertise. At the top of the value chain are the end-users, spanning various sectors including enterprise, government, and individual consumers. Supporting these primary activities are research and development efforts, marketing and sales initiatives, and after-sales services, all of which contribute to the overall value proposition of storage solutions. The value chain is characterized by increasing collaboration and integration, with companies seeking to offer end-to-end solutions that encompass storage, networking, and computing capabilities.

15. Key Investment Insights in the Next Generation Data Storage Market - Strategic investment recommendations

Investment insights in the Next Generation Data Storage Market point to several strategic areas for potential growth and returns. Investors should consider focusing on companies that are at the forefront of emerging storage technologies such as NVMe over Fabrics (NVMe-oF), storage-class memory (SCM), and computational storage, as these are likely to drive the next wave of performance improvements. There's also significant potential in firms developing AI-driven storage management solutions, which promise to optimize data placement and enhance predictive maintenance capabilities. The shift towards edge computing presents investment opportunities in distributed storage architectures and micro data centers. Additionally, companies focusing on energy-efficient and sustainable storage solutions are likely to gain traction as environmental concerns become more prominent. Investors should also consider the growing importance of data security and compliance, making storage solutions with built-in encryption and advanced access controls attractive prospects. The market for storage solutions tailored to specific industries, such as healthcare or financial services, offers niche investment opportunities with potentially high returns. Lastly, keeping an eye on strategic partnerships and mergers in the storage ecosystem can provide insights into companies positioning themselves for long-term growth in this rapidly evolving market.

16. Next Generation Data Storage Market Conclusion - Summary and key takeaways

The Next Generation Data Storage Market stands at the forefront of technological innovation, driven by the exponential growth of data and the increasing demand for high-performance, scalable storage solutions. With a projected market size of 72.96 Billion by 2026 and a forecasted growth to 137.52 Billion by 2033, representing a CAGR of 9.48%, the market demonstrates robust potential for expansion. Key trends shaping the industry include the adoption of cloud-based and hybrid storage architectures, the emergence of edge computing, and the integration of AI-driven storage management. The market is characterized by a diverse range of storage mediums and architectures, catering to various end-user needs across sectors such as BFSI, healthcare, and media and entertainment. While the competitive landscape is intense, with established players and innovative startups vying for market share, there remains ample opportunity for growth and differentiation. As organizations continue to prioritize digital transformation and data-driven decision-making, the demand for advanced storage solutions is expected to remain strong, presenting significant opportunities for market players to innovate and expand their offerings in this dynamic and evolving market.

17. Research Methodology - How this research was conducted

The research methodology employed for this Next Generation Data Storage Market analysis combines both primary and secondary research approaches to ensure comprehensive and accurate insights. Primary research involved conducting interviews with industry experts, including CTOs, storage architects, and market analysts, to gather firsthand information on market trends, technological developments, and competitive dynamics. These interviews provided valuable qualitative insights and helped validate quantitative findings. Secondary research encompassed a thorough review of industry reports, company annual reports, financial statements, and relevant publications from reputable sources such as technology journals, market research firms, and industry associations. Data on market size, growth rates, and segmentation was compiled from multiple sources to ensure reliability and cross-verification. The research also utilized data triangulation techniques to validate findings across different data points and methodologies. Market forecasting was performed using a combination of top-down and bottom-up approaches, considering factors such as technological trends, economic indicators, and industry-specific growth drivers. The final analysis was subjected to rigorous quality checks and expert review to ensure accuracy and relevance of the findings presented in this report.

18. Research Scope - Coverage and limitations

The research scope for this Next Generation Data Storage Market analysis encompasses a comprehensive examination of the global market, focusing on key segments including storage mediums (HDD, SSD, Tape), storage systems (DAS, NAS, SAN), deployment models (on-premise, cloud-based, hybrid), and end-user industries (BFSI, retail, IT and telecom, healthcare, media and entertainment). The study covers major geographic regions, including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, providing insights into regional market dynamics and growth opportunities. The research timeframe extends from historical data (2020-2021) to the forecast period (2022-2033), allowing for a thorough analysis of market trends and future projections. However, it's important to note certain limitations in the research scope. Due to the rapidly evolving nature of the storage technology landscape, some emerging technologies may not be fully represented in the current analysis. Additionally, the impact of unforeseen global events or regulatory changes beyond the forecast period cannot be entirely accounted for in the projections. The research also focuses primarily on commercial aspects of the market, with limited coverage of academic or experimental storage technologies that may have future commercial potential.

19. Key Companies and Recent Developments in the Next Generation Data Storage Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Next Generation Data Storage Market features several key players who are continuously innovating and expanding their product portfolios to maintain competitive advantage. Dell Technologies has recently announced advancements in its PowerStore platform, introducing AI-driven storage optimization features and enhanced data protection capabilities. Hewlett Packard Enterprise (HPE) unveiled its next-generation Alletra storage portfolio, focusing on as-a-service delivery models and simplified management interfaces. IBM continues to push the boundaries with its FlashSystem storage solutions, incorporating machine learning for predictive analytics and automated tiering. NetApp has strengthened its position in the hybrid cloud space with the launch of its unified data storage operating system, enhancing data mobility across on-premise and cloud environments. Pure Storage introduced its Evergreen//One service, offering a subscription-based model for its all-flash storage arrays, aligning with the industry's shift towards consumption-based pricing. DataDirect Networks (DDN) announced a strategic partnership with NVIDIA to deliver high-performance storage solutions optimized for AI and deep learning workloads. Huawei Technologies expanded its OceanStor portfolio with new all-flash storage systems designed for big data analytics and cloud applications. These developments reflect the industry's focus on intelligent storage management, cloud integration, and performance optimization to meet the evolving needs of data-intensive applications.