Europe Contract Logistics Market Overview - Definition, scope, and significance

Contract logistics refers to the outsourcing of logistics and supply chain management activities to third-party providers who specialize in handling specific logistics functions for businesses. In the European context, this market encompasses a wide range of services including transportation, warehousing, packaging, distribution, and aftermarket logistics across various industries. The significance of this market lies in its ability to help companies optimize their supply chains, reduce operational costs, and focus on core business activities while leveraging the expertise of specialized logistics providers. With Europe's complex cross-border trade environment and diverse industrial landscape, contract logistics has become increasingly vital for businesses seeking to navigate regulatory requirements, manage inventory efficiently, and ensure timely delivery across the continent's extensive network of markets.

Europe Contract Logistics Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Europe contract logistics market is driven by several key factors including the rapid growth of e-commerce, increasing globalization of supply chains, and the need for cost optimization among businesses. The rise of omnichannel retail and changing consumer expectations for faster delivery have compelled companies to seek specialized logistics partners. Additionally, technological advancements in areas such as warehouse automation, real-time tracking, and data analytics are creating new opportunities for contract logistics providers to offer value-added services. However, the market faces restraints such as labor shortages, rising fuel costs, and complex regulatory environments across different European countries. Challenges include managing sustainability requirements, adapting to Brexit-related trade complexities, and addressing cybersecurity concerns in increasingly digital supply chains. Opportunities exist in emerging sectors like pharmaceuticals and high-tech industries, as well as in developing green logistics solutions and expanding last-mile delivery capabilities to meet evolving market demands.

Europe Contract Logistics Market Growth Trends - Current and emerging trends shaping the market

The Europe contract logistics market is experiencing several notable growth trends that are reshaping the industry landscape. One prominent trend is the increasing adoption of automation and robotics in warehousing operations, with providers investing in automated storage and retrieval systems, autonomous mobile robots, and AI-powered inventory management solutions. Another significant trend is the growing emphasis on sustainability, with logistics providers implementing green initiatives such as electric vehicle fleets, optimized route planning to reduce carbon emissions, and sustainable packaging solutions. The market is also witnessing a shift toward integrated logistics solutions, where providers offer end-to-end supply chain management rather than individual services. Additionally, the rise of nearshoring and regionalization of supply chains is creating new opportunities for contract logistics providers to support more localized distribution networks. The integration of advanced analytics and Internet of Things (IoT) technologies is enabling real-time visibility and predictive maintenance, while the expansion of cold chain logistics is meeting the growing demand for temperature-sensitive goods transportation across Europe.

COVID-19 Impact on the Europe Contract Logistics Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the Europe contract logistics market, initially causing significant disruptions to supply chains and logistics operations. Lockdowns and border closures led to delays, capacity constraints, and increased costs as providers struggled to maintain operations while ensuring the safety of their workforce. However, the pandemic also accelerated certain trends, including the growth of e-commerce and the need for resilient supply chains. Contract logistics providers played a crucial role in supporting essential industries such as healthcare and food supply during the crisis. As the market recovers, there is a renewed focus on building more resilient and flexible supply chain models, with increased investment in digital technologies and contingency planning. The pandemic has also heightened awareness of the importance of contract logistics in ensuring business continuity, leading to stronger partnerships between companies and their logistics providers. Looking ahead, the market is expected to continue its recovery trajectory, with lessons learned from the pandemic driving innovation and adaptation in logistics strategies.

Europe Contract Logistics Market Competitive Landscape - Major competitors and market consolidation

The Europe contract logistics market features a competitive landscape characterized by the presence of both global logistics giants and regional specialists. Major players such as Deutsche Post DHL, Kuehne + Nagel, and DB Schenker dominate the market with their extensive networks and comprehensive service offerings. These companies leverage their scale, technological capabilities, and industry expertise to maintain competitive advantages. The market is also witnessing consolidation through mergers and acquisitions, as larger providers seek to expand their geographic presence and service portfolios. Competition is intensifying in areas such as last-mile delivery, where innovative startups are challenging traditional providers with technology-driven solutions. Additionally, the market is seeing increased competition from asset-light providers who offer flexible, on-demand logistics services. To differentiate themselves, providers are focusing on value-added services, industry-specific expertise, and sustainability initiatives. The competitive landscape is further shaped by the need to adapt to evolving customer demands, regulatory requirements, and technological advancements, driving continuous innovation and strategic partnerships among market participants.

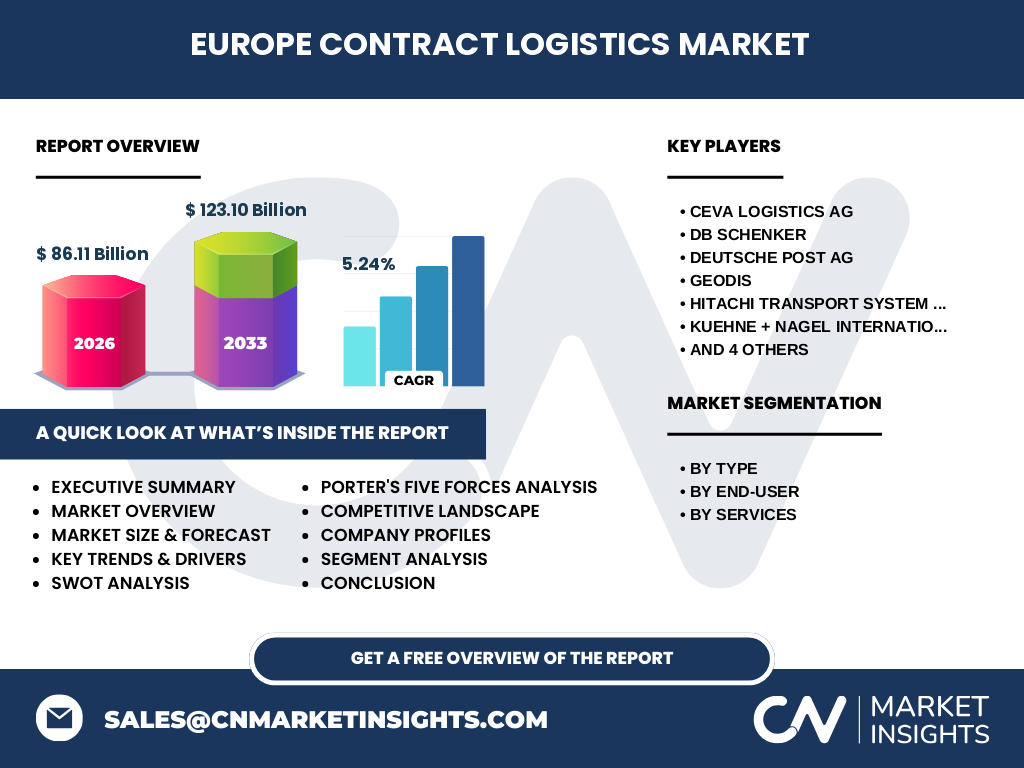

Executive Summary - High-level overview and key findings about Europe Contract Logistics Market

The Europe contract logistics market is positioned for steady growth, driven by the increasing complexity of supply chains, the expansion of e-commerce, and the need for specialized logistics expertise. With a projected CAGR of 5.24% from 2027 to 2033, the market is expected to grow from 86.11 billion in 2026 to 123.10 billion by 2033. This growth is underpinned by the market's ability to provide cost-effective, scalable, and technologically advanced logistics solutions to a diverse range of industries including automotive, pharmaceuticals, consumer goods, and high-tech sectors. Key findings indicate a strong trend toward automation and digitalization, with providers investing heavily in warehouse management systems, transportation management software, and data analytics capabilities. The market is also characterized by increasing demand for integrated logistics services, sustainability initiatives, and last-mile delivery solutions. Despite challenges such as labor shortages and regulatory complexities, the Europe contract logistics market presents significant opportunities for growth, particularly in emerging sectors and through the adoption of innovative technologies that enhance supply chain visibility and efficiency.

Europe Contract Logistics Market Forecast - Projections for 2025-2032 period

The Europe contract logistics market is projected to experience robust growth over the 2025-2032 period, with the market size expected to increase from 86.11 billion in 2026 to 123.10 billion by 2033. This represents a compound annual growth rate (CAGR) of 5.24%, indicating a healthy and sustainable expansion of the market. The forecast is based on several factors including the continued growth of e-commerce, increasing globalization of supply chains, and the rising demand for specialized logistics services across various industries. The transportation and warehousing segments are expected to remain the largest contributors to market growth, while services such as production logistics and aftermarket logistics are anticipated to see significant expansion due to the growing complexity of supply chains. Geographically, Western European countries are likely to maintain their dominant position in the market, although Central and Eastern European regions are expected to show higher growth rates due to increasing foreign investments and the development of logistics infrastructure. The forecast also takes into account the impact of technological advancements, with automation and digital solutions expected to drive efficiency and create new growth opportunities for contract logistics providers.

Europe Contract Logistics Market Size and Share by Segmentation - Breakdown by {segmentData}

The Europe contract logistics market is segmented by type, end-user, and services, each contributing differently to the overall market size and share. By type, the market is divided into outsourcing and insourcing, with outsourcing dominating due to the increasing trend of companies focusing on core competencies and delegating logistics operations to specialized providers. In terms of end-users, the market serves various industries including aerospace, automotive, consumer goods, high-tech, industrial, and pharma & healthcare sectors. The consumer goods segment currently holds the largest share, driven by the booming e-commerce sector and changing consumer preferences. The pharma & healthcare segment is expected to witness the highest growth rate due to increasing regulatory requirements and the need for specialized cold chain logistics. By services, the market is categorized into transportation, warehousing, packaging processes and solutions, distribution, production logistics, and aftermarket logistics. Transportation and warehousing services collectively account for the majority of the market share, as they form the backbone of most logistics operations. The distribution and packaging segments are also significant contributors, reflecting the growing complexity of supply chain requirements and the need for value-added services in the European market.

Global Europe Contract Logistics Market Size and Share by Region - Geographic distribution

The Europe contract logistics market exhibits distinct regional variations in terms of size and share, reflecting the diverse economic landscape and industrial distribution across the continent. Western European countries, including Germany, France, the United Kingdom, and the Netherlands, dominate the market due to their advanced logistics infrastructure, high concentration of manufacturing and distribution centers, and strong presence of major logistics providers. These countries benefit from well-developed transportation networks, including extensive road, rail, and port facilities, which facilitate efficient logistics operations. Central and Eastern European countries, such as Poland, Czech Republic, and Hungary, are emerging as significant players in the market, driven by lower operational costs, strategic location for distribution to Western Europe, and increasing foreign direct investments. Southern European countries, including Italy and Spain, contribute notably to the market, particularly in sectors such as fashion, food & beverage, and automotive logistics. The Nordic countries, while smaller in market size, are recognized for their innovation in green logistics and advanced supply chain technologies. Overall, the regional distribution of the Europe contract logistics market reflects a balance between established logistics hubs and emerging markets, with each region offering unique opportunities and challenges for service providers.

Regional Analysis of the Europe Contract Logistics Market - Detailed regional market performance

The Europe contract logistics market demonstrates varied performance across different regions, influenced by local economic conditions, industrial strengths, and logistics infrastructure development. In Western Europe, countries like Germany and the Netherlands lead the market due to their strategic location, advanced logistics hubs, and strong manufacturing sectors. Germany, in particular, benefits from its automotive industry's complex supply chain requirements, while the Netherlands serves as a major gateway for European trade with its world-class port facilities. Southern European countries, such as Italy and Spain, show robust growth in contract logistics, driven by their fashion, food & beverage, and agricultural sectors, which require specialized logistics services. Central and Eastern European countries, including Poland and the Czech Republic, are experiencing rapid growth in contract logistics, fueled by foreign investments, lower labor costs, and their role as manufacturing bases for Western European companies. The Nordic region, while smaller in market size, is notable for its innovation in sustainable logistics solutions and high adoption of advanced technologies. Each region presents unique opportunities and challenges, with Western Europe focusing on high-value, technology-driven services, while Eastern Europe offers cost-effective solutions and growing market potential. The regional analysis highlights the diverse nature of the European contract logistics market and the need for providers to adapt their strategies to local conditions and industry requirements.

Leading Company Profiles in the Europe Contract Logistics Market - Industry players and strategies

The Europe contract logistics market is dominated by several key players who have established strong positions through their comprehensive service offerings, extensive networks, and strategic investments. Deutsche Post DHL, one of the largest logistics providers globally, leverages its integrated logistics solutions and advanced technology platforms to serve a wide range of industries across Europe. Kuehne + Nagel International AG is another major player, known for its expertise in seafreight, airfreight, and contract logistics, with a strong focus on digital solutions and sustainability initiatives. DB Schenker, a division of Deutsche Bahn, offers a full range of logistics services and has a significant presence in European industrial and automotive logistics. Geodis, part of the SNCF Group, specializes in supply chain optimization and has a strong foothold in the French and broader European markets. Other notable companies include CEVA Logistics, which focuses on tailored industry solutions, and XPO Logistics, known for its innovative approach to last-mile delivery and e-commerce logistics. These leading companies employ various strategies to maintain their competitive edge, including investments in automation and robotics, development of green logistics solutions, expansion of e-commerce capabilities, and strategic acquisitions to broaden their service portfolios and geographic reach. Their success is underpinned by their ability to adapt to changing market demands, invest in technology, and provide value-added services that address the complex logistics needs of their diverse client base.

Porter's Five Forces Analysis of the Europe Contract Logistics Market - Competitive forces assessment

The Europe contract logistics market is shaped by several competitive forces as analyzed through Porter's Five Forces framework. The threat of new entrants is moderate, as the market requires significant capital investment in infrastructure, technology, and expertise, creating barriers to entry. However, the rise of digital platforms and asset-light business models has lowered some barriers, allowing innovative startups to enter niche segments. The bargaining power of buyers is high, given the large number of logistics providers and the commoditization of certain services, which puts pressure on providers to offer competitive pricing and value-added services. Conversely, the bargaining power of suppliers is relatively low, as logistics providers have multiple options for carriers, warehouse operators, and technology vendors. The threat of substitutes is moderate, with in-house logistics operations and integrated supply chain solutions posing alternatives to contract logistics services. Competitive rivalry within the market is intense, characterized by price competition, service differentiation, and technological innovation. Major players compete on factors such as network coverage, industry expertise, and sustainability initiatives. The analysis reveals a market where established providers must continually innovate and adapt to maintain their positions, while new entrants can find opportunities in specialized or technology-driven niches.

SWOT Analysis of the Europe Contract Logistics Market - Strengths, weaknesses, opportunities, threats

The Europe contract logistics market exhibits several strengths, weaknesses, opportunities, and threats as identified in a comprehensive SWOT analysis. Among the strengths, the market benefits from a highly developed logistics infrastructure, advanced technological capabilities, and a diverse range of specialized service providers. The presence of major logistics hubs and intermodal transportation networks across Europe enhances the efficiency and reliability of contract logistics services. However, weaknesses include the high operational costs associated with labor, fuel, and compliance with diverse regulatory requirements across different countries. Additionally, the market faces challenges in managing seasonal fluctuations and capacity constraints during peak periods. Opportunities in the market are abundant, particularly in the areas of e-commerce logistics, sustainable supply chain solutions, and the integration of advanced technologies such as AI and IoT for improved visibility and efficiency. The growing trend of nearshoring and regionalization of supply chains also presents new opportunities for contract logistics providers to offer more localized services. Threats to the market include geopolitical uncertainties, such as Brexit and trade tensions, which can disrupt established supply chain patterns. The market also faces threats from economic downturns that can reduce demand for logistics services, as well as increasing competition from both traditional providers and new digital entrants offering innovative logistics solutions.

Europe Contract Logistics Market Value Chain Analysis - Industry structure and value flow

The Europe contract logistics market value chain encompasses a series of interconnected activities that create and deliver value to end customers. At the core of this value chain are the logistics service providers who coordinate and manage various functions including transportation, warehousing, inventory management, and distribution. These providers work closely with suppliers of logistics equipment, technology solutions, and transportation services to ensure smooth operations. The value chain begins with procurement and planning, where providers assess client needs and design customized logistics solutions. This is followed by implementation, which involves the physical movement of goods, storage, and order fulfillment. Value-added services such as packaging, labeling, and quality control are integrated into the process to enhance the overall offering. The use of advanced technologies, including warehouse management systems, transportation management software, and real-time tracking solutions, adds significant value by improving efficiency and visibility across the supply chain. At the end of the value chain, providers offer analytics and reporting services to clients, enabling data-driven decision-making and continuous improvement of logistics operations. The effectiveness of this value chain is crucial for contract logistics providers to differentiate themselves in a competitive market and deliver superior service to their clients.

Key Investment Insights in the Europe Contract Logistics Market - Strategic investment recommendations

The Europe contract logistics market presents several compelling investment opportunities for both existing players and new entrants. Strategic investments in automation and robotics are highly recommended, as these technologies can significantly improve operational efficiency, reduce labor costs, and enhance accuracy in warehousing and distribution operations. Investors should also consider opportunities in sustainable logistics solutions, including electric vehicle fleets, energy-efficient warehouses, and green packaging alternatives, as sustainability becomes increasingly important to clients and regulators. The growing e-commerce sector offers investment potential in last-mile delivery solutions, micro-fulfillment centers, and omnichannel distribution networks. Additionally, investments in digital platforms and data analytics capabilities can provide a competitive edge by enabling real-time visibility, predictive analytics, and optimized route planning. Emerging markets in Central and Eastern Europe represent attractive investment opportunities due to their growing manufacturing bases and improving logistics infrastructure. Investors should also consider strategic partnerships or acquisitions to gain access to specialized capabilities or expand geographic presence. The pharmaceutical and healthcare sectors offer niche investment opportunities, particularly in cold chain logistics and compliance with stringent regulatory requirements. Overall, successful investments in the Europe contract logistics market will require a focus on technology, sustainability, and the ability to provide integrated, value-added services that address the evolving needs of diverse industries.

Europe Contract Logistics Market Conclusion - Summary and key takeaways

The Europe contract logistics market is a dynamic and essential component of the region's economy, facilitating the efficient movement of goods across complex supply chains. With a projected growth from 86.11 billion in 2026 to 123.10 billion by 2033, representing a CAGR of 5.24%, the market demonstrates strong potential for expansion. Key takeaways from the analysis include the increasing importance of technology integration, with automation, AI, and IoT playing crucial roles in enhancing operational efficiency and providing value-added services. The market is characterized by its diversity, serving a wide range of industries from automotive to pharmaceuticals, each with unique logistics requirements. Sustainability has emerged as a critical focus area, driving investments in green logistics solutions and circular economy initiatives. The competitive landscape is dominated by global players but also includes niche specialists and innovative startups, creating a vibrant ecosystem of service providers. Regional variations across Europe offer both challenges and opportunities, with Western Europe leading in advanced logistics solutions while Central and Eastern Europe present growth potential. As the market continues to evolve, success will depend on providers' ability to adapt to changing customer needs, embrace technological advancements, and navigate complex regulatory environments while maintaining cost-effectiveness and service quality.

Research Methodology - How this research was conducted

The research for this Europe contract logistics market report was conducted using a comprehensive and rigorous methodology to ensure accuracy and reliability of the findings. The process began with extensive secondary research, involving the analysis of industry reports, market databases, company annual reports, and relevant publications from trusted sources. This was complemented by primary research, which included interviews with industry experts, logistics providers, and key stakeholders to gather firsthand insights and validate market trends. Data triangulation was employed to cross-verify information from multiple sources, enhancing the credibility of the research findings. The market size and forecast were derived using both top-down and bottom-up approaches, considering various factors such as industry growth rates, technological advancements, and economic indicators. Segmentation analysis was performed to understand the contribution of different service types, end-user industries, and geographic regions to the overall market. The research also incorporated a detailed competitive landscape analysis, examining the strategies and market positions of key players. Throughout the process, attention was paid to emerging trends, regulatory changes, and macroeconomic factors that could impact the market. The methodology ensured a holistic view of the Europe contract logistics market, providing stakeholders with actionable insights and strategic recommendations.

Research Scope - Coverage and limitations

The research scope for this Europe contract logistics market report encompasses a comprehensive analysis of the market across various dimensions including service types, end-user industries, and geographic regions within Europe. The report covers key services such as transportation, warehousing, packaging, distribution, production logistics, and aftermarket logistics, providing insights into their individual market dynamics and growth prospects. It also examines the demand for contract logistics services across major industries including aerospace, automotive, consumer goods, high-tech, industrial, and pharma & healthcare sectors. The geographic scope includes all major European countries, with a focus on key markets such as Germany, France, the United Kingdom, and emerging markets in Central and Eastern Europe. The research timeframe extends from historical data to future projections up to 2033, offering a long-term view of market trends and opportunities. However, it's important to note some limitations of the research. The report may not capture the impact of unforeseen global events or rapid technological disruptions that could significantly alter market dynamics. Additionally, while efforts were made to include all relevant market players, some smaller or highly specialized providers may not be extensively covered. The research also acknowledges that market conditions can vary significantly at a local level, which may not be fully reflected in the broader regional analysis. Despite these limitations, the report aims to provide a comprehensive and insightful overview of the Europe contract logistics market, serving as a valuable resource for industry stakeholders and decision-makers.

Key Companies and Recent Developments in the Europe Contract Logistics Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Europe contract logistics market is characterized by the presence of several key companies that have established themselves as industry leaders through continuous innovation and strategic developments. Deutsche Post DHL Group, one of the largest logistics providers globally, has recently announced significant investments in electric vehicle fleets and sustainable warehousing solutions across Europe, aligning with its commitment to reduce carbon emissions. Kuehne + Nagel International AG has launched advanced digital platforms for real-time supply chain visibility and has formed strategic partnerships with technology companies to enhance its service offerings. DB Schenker has expanded its e-commerce logistics capabilities, introducing new last-mile delivery solutions and automated warehousing systems to meet the growing demand for online retail logistics. Geodis has strengthened its position in the pharmaceutical logistics sector through the development of specialized cold chain solutions and has announced collaborations with biotech companies to support vaccine distribution. CEVA Logistics has focused on industry-specific solutions, launching tailored logistics services for the automotive and consumer goods sectors, while also investing in AI-driven warehouse automation. XPO Logistics has made headlines with its innovative approach to last-mile delivery, introducing robotic delivery systems and drone technology trials in select European markets. These companies, along with others in the market, continue to drive innovation through product launches, strategic partnerships, and investments in emerging technologies, shaping the future of contract logistics in Europe.