In-Flight Wi-Fi Market Overview - Definition, scope, and significance

In-Flight Wi-Fi refers to wireless internet connectivity services provided to passengers during commercial and private flights. This technology enables travelers to access the internet, stream content, check emails, and stay connected with ground-based networks while airborne. The market encompasses both hardware infrastructure (antennas, modems, routers) and service delivery (subscription plans, bandwidth management, and content delivery). As air travel continues to recover and grow post-pandemic, in-flight connectivity has evolved from a luxury amenity to an essential service, particularly for business travelers and digitally connected passengers. The market's significance extends beyond passenger convenience, impacting airline competitiveness, operational efficiency, and the broader aviation technology ecosystem.

In-Flight Wi-Fi Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the In-Flight Wi-Fi market include increasing passenger demand for constant connectivity, airline differentiation strategies, and technological advancements in satellite and air-to-ground communications. Rising disposable incomes and the proliferation of connected devices further fuel market growth. However, the market faces significant restraints including high installation and maintenance costs, limited bandwidth availability, and regulatory challenges across different jurisdictions. Technical challenges such as signal interference, aircraft weight considerations, and the need for regular system upgrades present ongoing obstacles. Despite these challenges, substantial opportunities exist in emerging markets, next-generation satellite technologies, and the potential for new revenue streams through premium services and targeted advertising. The integration of 5G technology and the development of low-earth orbit satellite constellations present particularly promising opportunities for market expansion.

In-Flight Wi-Fi Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the In-Flight Wi-Fi market are characterized by the transition from basic connectivity to high-speed, low-latency services capable of supporting streaming and real-time applications. The adoption of hybrid connectivity solutions combining satellite and air-to-ground technologies is becoming increasingly prevalent. There is a notable trend toward the standardization of in-flight connectivity across airline fleets, with both legacy carriers and low-cost airlines investing in comprehensive Wi-Fi infrastructure. The market is also witnessing the emergence of software-defined networking solutions that allow for more flexible bandwidth allocation and improved service quality. Additionally, the integration of in-flight Wi-Fi with other aircraft systems for predictive maintenance and operational optimization represents a significant emerging trend. The development of more compact, lightweight hardware is also gaining traction as airlines seek to minimize fuel consumption and operational costs.

COVID-19 Impact on the In-Flight Wi-Fi Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially caused a severe contraction in the In-Flight Wi-Fi market as global air travel came to a near standstill in 2020. Airlines deferred non-essential investments, including connectivity upgrades, while manufacturers faced supply chain disruptions and reduced production. However, the pandemic also accelerated certain trends, including the recognition of in-flight connectivity as a critical tool for maintaining business continuity and passenger satisfaction during recovery. As travel restrictions eased, airlines began prioritizing Wi-Fi services as a key differentiator to attract passengers back to air travel. The recovery trajectory has been marked by a shift toward more flexible service models, including pay-per-use options and bundled packages. The pandemic also highlighted the importance of reliable connectivity for crew communications and operational efficiency, leading to increased investment in robust, multi-functional systems.

In-Flight Wi-Fi Market Competitive Landscape - Major competitors and market consolidation

The In-Flight Wi-Fi market features a mix of specialized connectivity providers, aerospace technology companies, and satellite operators competing for market share. The competitive landscape is characterized by strategic partnerships between airlines and technology providers, as well as vertical integration efforts by major players seeking to control both hardware and service delivery. Market consolidation has been evident through mergers, acquisitions, and long-term service agreements that create barriers to entry for new competitors. Key differentiators in the competitive landscape include technological capabilities, global coverage, service reliability, and pricing models. Companies are increasingly focusing on developing proprietary technologies and securing exclusive agreements with airlines to maintain competitive advantages. The market also sees competition from emerging players offering innovative solutions, particularly in the satellite technology segment.

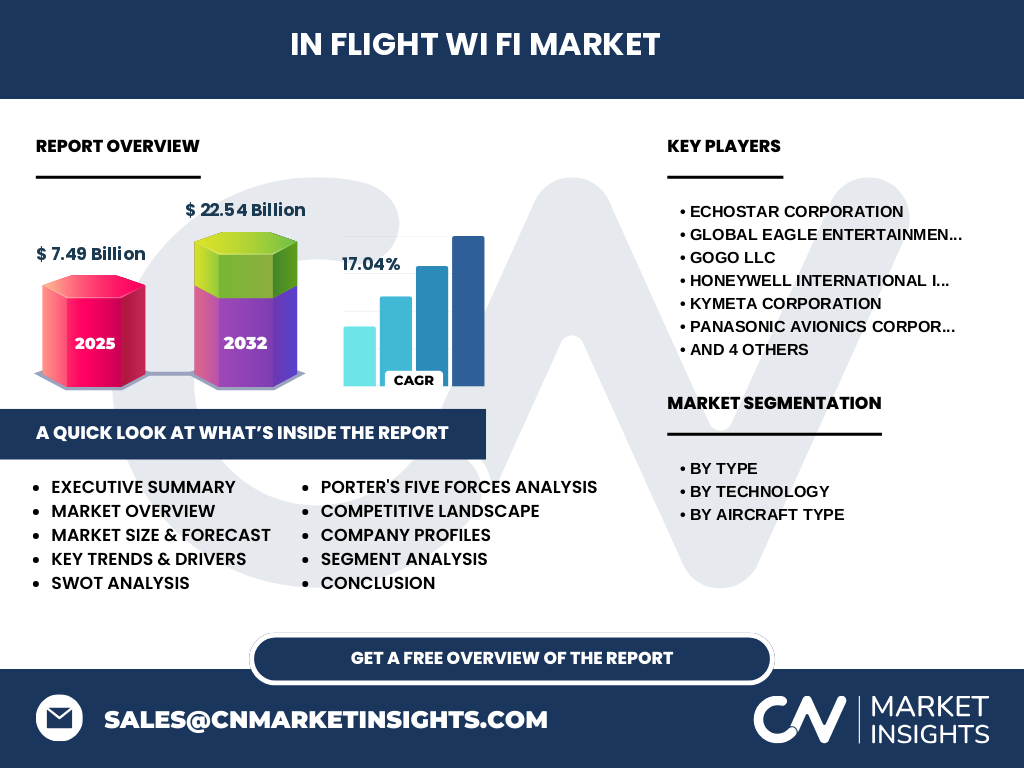

Executive Summary - High-level overview and key findings about In-Flight Wi-Fi Market

The In-Flight Wi-Fi market is experiencing robust growth, driven by increasing passenger expectations for connectivity and airlines' need to differentiate their services. With a projected CAGR of 17.04% from 2025 to 2032, the market is expected to grow from USD 7.49 billion to USD 22.54 billion, reflecting strong demand across all aircraft segments. The market is characterized by rapid technological advancements, particularly in satellite communications and hybrid connectivity solutions. While challenges remain in terms of cost and technical limitations, the overall trajectory points toward continued expansion and innovation. Key findings indicate that the satellite technology segment is gaining prominence over air-to-ground solutions, and narrow-body aircraft represent a significant growth opportunity as low-cost carriers expand their connectivity offerings. The market's future success will depend on addressing bandwidth constraints, reducing hardware costs, and developing more flexible service models to meet diverse passenger needs.

In-Flight Wi-Fi Market Forecast - Projections for 2025-2032 period

The In-Flight Wi-Fi market is projected to experience substantial growth over the 2025-2032 period, with the market size expected to increase from USD 7.49 billion in 2025 to USD 22.54 billion by 2032, representing a compound annual growth rate of 17.04%. This growth is driven by the increasing number of connected aircraft, technological advancements in satellite communications, and the rising demand for in-flight connectivity services. The forecast period will likely see accelerated adoption of high-speed connectivity solutions, particularly on narrow-body aircraft as low-cost carriers expand their offerings. The satellite technology segment is expected to show particularly strong growth as new constellations become operational, providing global coverage and higher bandwidth capabilities. The market is also likely to benefit from the recovery and expansion of global air travel, with airlines increasingly viewing in-flight Wi-Fi as a standard rather than optional service.

In-Flight Wi-Fi Market Size and Share by Segmentation - Breakdown by {segmentData}

The In-Flight Wi-Fi market segmentation reveals distinct growth patterns across different categories. By type, the market is divided into hardware and services, with services currently dominating due to recurring revenue models and the need for continuous bandwidth provision. However, the hardware segment is expected to see significant growth as airlines undertake fleet-wide connectivity upgrades. In terms of technology, the market is segmented into air-to-ground technology and satellite technology, with satellite technology gaining increasing market share due to its global coverage capabilities and improving bandwidth. By aircraft type, narrow-body aircraft represent the largest and fastest-growing segment, driven by the expansion of low-cost carriers and their need to offer competitive services. Wide-body aircraft continue to be a strong market for premium connectivity services, while very large aircraft and business jets represent a niche but high-value segment with specific requirements for high-bandwidth, low-latency connections.

Global In-Flight Wi-Fi Market Size and Share by Region - Geographic distribution

While specific regional market share data is not provided, the global distribution of the In-Flight Wi-Fi market typically shows North America as the largest market, driven by the high concentration of major airlines and early technology adoption. Europe represents the second-largest market, with strong demand from both legacy carriers and low-cost airlines. The Asia-Pacific region is expected to show the highest growth rate during the forecast period, fueled by increasing air travel demand, rising disposable incomes, and significant investments in aviation infrastructure. The Middle East, with its major international hubs, represents a strong market for premium in-flight connectivity services. Latin America and Africa, while currently smaller markets, are expected to see increased adoption as air travel expands and technology costs decrease. Regional variations in regulatory frameworks, satellite coverage, and airline business models create distinct market dynamics in each geographic area.

Regional Analysis of the In-Flight Wi-Fi Market - Detailed regional market performance

Regional market performance in the In-Flight Wi-Fi sector varies significantly based on factors such as air traffic volume, regulatory environment, and technological infrastructure. North America leads in market maturity, with extensive adoption across major carriers and a well-established ecosystem of service providers. The region benefits from advanced satellite coverage and supportive regulatory frameworks. Europe shows strong market performance with a mix of high-speed rail competition driving airlines to offer superior connectivity, and strict data protection regulations influencing service delivery models. The Asia-Pacific region demonstrates the most dynamic growth, with countries like China, Japan, and Australia investing heavily in both satellite infrastructure and airline connectivity. However, the region faces challenges related to diverse regulatory requirements and varying levels of technological development across countries. The Middle East, led by carriers such as Emirates and Qatar Airways, represents a premium market segment with high expectations for service quality and global coverage. Emerging markets in Latin America and Africa are gradually adopting in-flight connectivity, primarily driven by international route expansion and partnerships with global service providers.

Leading Company Profiles in the In-Flight Wi-Fi Market - Industry players and strategies

The In-Flight Wi-Fi market features several key players with distinct strategic approaches. ECHOSTAR CORPORATION leverages its satellite technology expertise to provide comprehensive connectivity solutions, focusing on global coverage and high-bandwidth services. GLOBAL EAGLE ENTERTAINMENT INC specializes in integrated entertainment and connectivity platforms, targeting both commercial airlines and business aviation. GOGO LLC has established itself as a pioneer in air-to-ground technology while expanding into satellite solutions to offer hybrid connectivity options. HONEYWELL INTERNATIONAL INC brings its extensive aerospace experience to develop integrated hardware and software solutions for in-flight connectivity. KYMETA CORPORATION focuses on innovative flat-panel satellite antennas that promise to revolutionize aircraft connectivity with their lightweight and aerodynamic designs. PANASONIC AVIONICS CORPORATION offers end-to-end solutions from hardware to content delivery, emphasizing premium service quality. SITAONAIR specializes in aircraft communication services with a strong focus on operational efficiency and crew connectivity. THALES GROUP leverages its aerospace and defense expertise to provide secure, reliable connectivity solutions. THINKOM SOLUTIONS INC focuses on advanced antenna technologies, while VIASAT INC has made significant investments in satellite constellations to provide high-speed global coverage. These companies employ various strategies including technological innovation, strategic partnerships, and vertical integration to maintain competitive advantages in the market.

Porter's Five Forces Analysis of the In-Flight Wi-Fi Market - Competitive forces assessment

The Porter's Five Forces analysis of the In-Flight Wi-Fi market reveals a complex competitive landscape. The threat of new entrants is moderate to high due to the significant capital requirements for technology development and the need for regulatory approvals, but relatively low barriers exist for service-based innovations. Bargaining power of buyers (airlines) is significant as they can negotiate based on fleet size and route networks, but is somewhat mitigated by the specialized nature of the technology and the importance of reliability. The bargaining power of suppliers is high, particularly for satellite capacity and specialized hardware components, creating potential cost pressures. The threat of substitute services is low in the traditional sense, but competition from alternative passenger engagement methods and ground-based connectivity solutions exists. Competitive rivalry is intense, characterized by technological differentiation, pricing pressures, and the race for global coverage. The market also faces potential disruption from emerging technologies and changing passenger expectations, requiring continuous innovation and adaptation from existing players.

SWOT Analysis of the In-Flight Wi-Fi Market - Strengths, weaknesses, opportunities, threats

The SWOT analysis of the In-Flight Wi-Fi market reveals several key factors. Strengths include the growing demand for connectivity, technological advancements in satellite communications, and the increasing importance of in-flight services as a competitive differentiator for airlines. The market also benefits from the potential for new revenue streams through premium services and data monetization. However, weaknesses exist in the form of high implementation costs, bandwidth limitations, and the complexity of integrating systems across diverse aircraft types. Opportunities are abundant in emerging markets, next-generation satellite technologies, and the potential for expanding services beyond passenger connectivity to include operational and maintenance applications. The market also has opportunities in developing more cost-effective solutions for narrow-body aircraft and low-cost carriers. Threats include regulatory challenges across different jurisdictions, potential cybersecurity risks, and the rapid pace of technological change that could render existing solutions obsolete. Economic downturns affecting air travel demand and the potential for market saturation in mature regions also pose significant threats to market growth.

In-Flight Wi-Fi Market Value Chain Analysis - Industry structure and value flow

The In-Flight Wi-Fi market value chain encompasses several interconnected stages, from technology development to end-user service delivery. At the upstream level, the value chain includes satellite operators, antenna manufacturers, and component suppliers who provide the essential infrastructure for connectivity. Midstream activities involve system integrators, service providers, and airlines who combine these components into functional solutions and manage service delivery. Downstream, the value chain extends to content providers, application developers, and end-users who consume the connectivity services. Key value-adding activities include technology innovation, service quality management, and the development of user-friendly interfaces and applications. The value chain is characterized by strategic partnerships and vertical integration efforts, with companies seeking to control multiple stages to improve efficiency and capture more value. Challenges in the value chain include coordinating across multiple stakeholders, managing complex installations, and ensuring consistent service quality across diverse operational environments.

Key Investment Insights in the In-Flight Wi-Fi Market - Strategic investment recommendations

Investment opportunities in the In-Flight Wi-Fi market are primarily driven by technological innovation and market expansion potential. Strategic investments should focus on next-generation satellite technologies, particularly low-earth orbit constellations that promise to deliver higher bandwidth and lower latency services. The development of more efficient antenna technologies and integrated hardware solutions represents another attractive investment area, especially solutions that reduce aircraft weight and improve fuel efficiency. Investments in software-defined networking and artificial intelligence for bandwidth management and predictive maintenance offer significant growth potential. The market also presents opportunities for investments in emerging regions, particularly in Asia-Pacific and Latin America, where air travel demand is growing rapidly. Additionally, investments in hybrid connectivity solutions that combine multiple technologies to ensure seamless global coverage are likely to yield strong returns. Strategic partnerships between technology providers, satellite operators, and airlines are increasingly important for market success and represent attractive investment opportunities.

In-Flight Wi-Fi Market Conclusion - Summary and key takeaways

The In-Flight Wi-Fi market is positioned for significant growth over the forecast period, driven by increasing passenger demand for connectivity, technological advancements, and the strategic importance of in-flight services for airlines. The market's projected CAGR of 17.04% reflects strong underlying demand across all aircraft segments, with particular growth opportunities in narrow-body aircraft and emerging markets. While challenges exist in terms of cost, technical limitations, and regulatory complexities, the overall market trajectory remains positive. Key takeaways include the increasing dominance of satellite technology over air-to-ground solutions, the importance of hybrid connectivity approaches, and the growing role of software-defined solutions in improving service quality and operational efficiency. The market's future success will depend on addressing bandwidth constraints, reducing hardware costs, and developing more flexible service models to meet diverse passenger needs while ensuring reliable, high-quality connectivity across global routes.

Research Methodology - How this research was conducted

The research methodology for this In-Flight Wi-Fi market analysis combines multiple approaches to ensure comprehensive and accurate insights. Primary research involved interviews with industry experts, technology providers, airline representatives, and regulatory authorities to gather firsthand information about market dynamics, technological developments, and strategic initiatives. Secondary research included extensive review of company annual reports, industry publications, regulatory filings, and market databases to validate findings and establish historical trends. Data triangulation methods were employed to cross-verify information from multiple sources, ensuring reliability and accuracy. The analysis incorporated both top-down and bottom-up approaches to estimate market size and forecast future growth, considering factors such as aircraft fleet sizes, technology adoption rates, and regional air travel trends. Market segmentation was conducted based on technology type, aircraft category, and geographic regions, with careful consideration of the interdependencies between these factors. The research also included competitive analysis through company profiling, patent analysis, and assessment of strategic developments in the industry.

Research Scope - Coverage and limitations

The research scope for this In-Flight Wi-Fi market analysis encompasses the global market with detailed segmentation by technology type (air-to-ground and satellite), aircraft type (narrow-body, wide-body, very large aircraft, and business jets), and service type (hardware and services). The analysis covers the period from 2025 to 2032, with historical context provided for key trends and developments. Geographic coverage includes major markets across North America, Europe, Asia-Pacific, Middle East, Latin America, and Africa, with regional variations in technology adoption and market maturity considered. The scope includes both commercial aviation and business aviation segments, recognizing their distinct requirements and growth patterns. Limitations of the research include the availability of detailed regional market data, the rapidly evolving nature of technology that may impact long-term forecasts, and the potential for unforeseen regulatory changes that could affect market dynamics. The analysis also acknowledges the challenge of accurately forecasting technology adoption rates and the impact of potential economic disruptions on air travel demand.

Key Companies and Recent Developments in the In-Flight Wi-Fi Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The In-Flight Wi-Fi market features several key companies driving innovation and market growth through strategic developments. ECHOSTAR CORPORATION recently announced expanded satellite capacity to support growing demand for high-speed connectivity, particularly on long-haul routes. GLOBAL EAGLE ENTERTAINMENT INC has formed strategic partnerships with major airlines to provide integrated entertainment and connectivity solutions, with recent announcements focusing on enhanced content delivery capabilities. GOGO LLC launched its next-generation 5G network infrastructure, targeting improved coverage and bandwidth for both commercial and business aviation segments. HONEYWELL INTERNATIONAL INC introduced new lightweight antenna systems designed to reduce aircraft weight while improving signal quality and reliability. KYMETA CORPORATION unveiled its latest flat-panel satellite antenna technology, promising significant improvements in aerodynamic efficiency and installation flexibility. PANASONIC AVIONICS CORPORATION announced expanded service agreements with several major carriers, focusing on premium connectivity solutions for international routes. SITAONAIR has been developing advanced data analytics capabilities to optimize bandwidth allocation and improve passenger experience. THALES GROUP recently secured a major contract for integrated connectivity systems across a large aircraft fleet, emphasizing cybersecurity features. THINKOM SOLUTIONS INC launched new phased array antenna technology designed for high-throughput satellite communications. VIASAT INC announced significant investments in its satellite constellation expansion, aiming to provide global high-speed coverage and compete directly with emerging low-earth orbit providers. These companies continue to drive market evolution through technological innovation, strategic partnerships, and expanded service offerings.