Oilfield Communications Market Overview - Definition, scope, and significance

The Oilfield Communications Market encompasses the specialized communication systems and solutions designed to facilitate seamless data transmission, voice communication, and operational coordination across oil and gas exploration, production, and refining facilities. This market serves the critical need for reliable connectivity in remote and harsh environments where traditional communication infrastructure is often unavailable or unreliable. The scope includes both onshore and offshore operations, covering upstream exploration activities, midstream transportation networks, and downstream processing facilities. The significance of this market lies in its ability to enhance operational efficiency, ensure worker safety, enable real-time monitoring of critical infrastructure, and support the digital transformation of the oil and gas industry through advanced technologies such as IoT sensors, automation systems, and data analytics platforms.

Oilfield Communications Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Oilfield Communications Market is driven by several key factors including the increasing demand for real-time data analytics to optimize production, the growing adoption of digital oilfield technologies, and the need for enhanced safety measures in hazardous environments. The expansion of offshore drilling activities and the development of unconventional oil and gas resources further propel market growth. However, the market faces restraints such as high initial investment costs, the complexity of integrating legacy systems with modern communication technologies, and cybersecurity concerns in critical infrastructure. Challenges include the harsh environmental conditions that can damage equipment, the need for specialized technical expertise, and regulatory compliance requirements. Opportunities exist in the development of satellite-based communication solutions for ultra-remote locations, the integration of 5G technology for enhanced connectivity, and the growing demand for managed services that reduce operational burden on oil companies.

Oilfield Communications Market Growth Trends - Current and emerging trends shaping the market

The Oilfield Communications Market is experiencing several significant growth trends that are reshaping the industry landscape. One prominent trend is the increasing adoption of hybrid communication networks that combine multiple technologies such as satellite, microwave, and fiber-optic systems to ensure reliable connectivity. The market is also witnessing a shift towards cloud-based communication platforms that enable centralized data management and remote operations. Edge computing is gaining traction as companies seek to process data closer to the source for faster decision-making. The integration of artificial intelligence and machine learning for predictive maintenance and operational optimization represents another emerging trend. Additionally, there is a growing emphasis on cybersecurity solutions specifically designed for oilfield communications to protect against increasing cyber threats. The market is also seeing increased investment in 5G technology deployment to enhance bandwidth and reduce latency for critical applications.

COVID-19 Impact on the Oilfield Communications Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly impacted the Oilfield Communications Market, causing disruptions in supply chains, project delays, and reduced capital expenditure by oil and gas companies. The initial lockdowns and travel restrictions led to a temporary decline in demand for new communication infrastructure installations and maintenance services. However, the pandemic also accelerated certain trends, such as the adoption of remote monitoring and control systems, as companies sought to minimize on-site personnel and maintain operations with reduced workforce. The recovery trajectory has been gradual, with the market rebounding as oil prices stabilized and companies resumed their digital transformation initiatives. The pandemic highlighted the importance of robust communication infrastructure for maintaining business continuity in crisis situations, leading to increased investment in resilient and redundant communication systems. As the industry adapts to the post-pandemic environment, there is a renewed focus on technologies that enable remote operations and enhance operational efficiency.

Oilfield Communications Market Competitive Landscape - Major competitors and market consolidation

The Oilfield Communications Market features a competitive landscape characterized by a mix of established telecommunications giants, specialized oilfield technology providers, and emerging players focusing on innovative solutions. Major competitors include ABB Ltd, Huawei Technologies Co. Ltd., Nokia Corporation, Siemens AG, and Commscope Holding Company, which leverage their extensive telecommunications expertise and global presence. Specialized companies such as RigNet, Inc., Speedcast International Limited, and Commtel Networks Pvt. Ltd. offer tailored solutions specifically designed for the oil and gas industry. The market is witnessing increasing consolidation through mergers, acquisitions, and strategic partnerships as companies seek to expand their service portfolios and geographic reach. Competition is intensifying in areas such as managed services, where providers offer end-to-end communication solutions, and in the development of advanced technologies like 5G and satellite communications for oilfield applications. The competitive dynamics are further influenced by the need for compliance with industry-specific regulations and the ability to provide reliable connectivity in extreme environmental conditions.

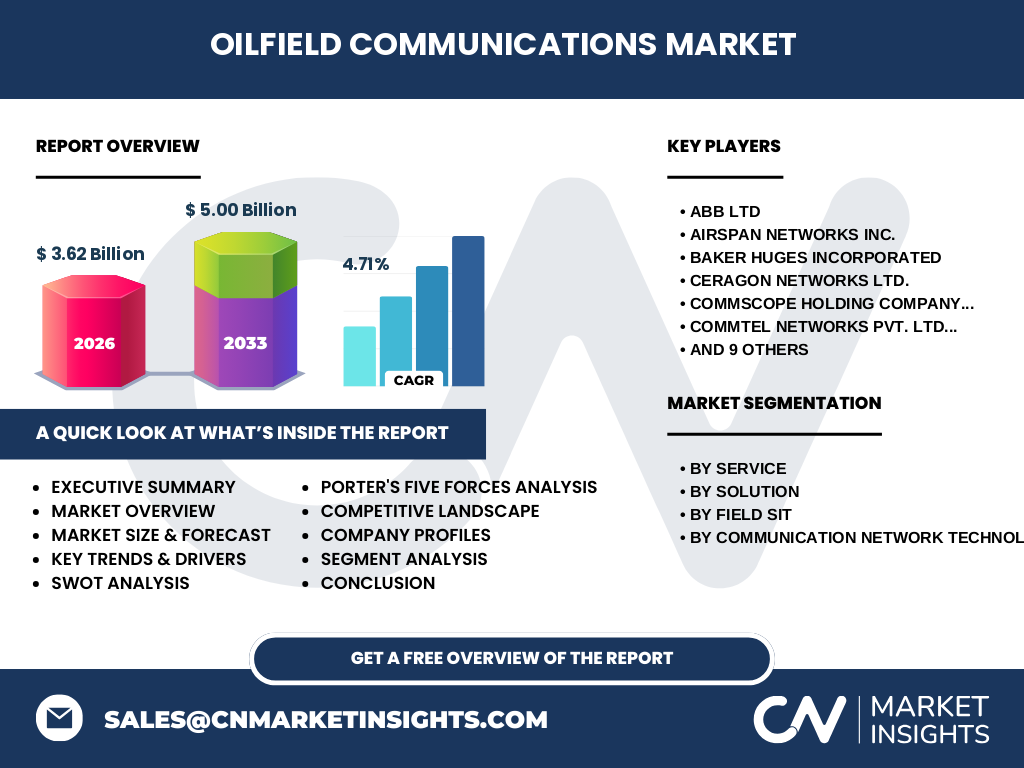

Executive Summary - High-level overview and key findings about Oilfield Communications Market

The Oilfield Communications Market is poised for steady growth, driven by the increasing digitalization of the oil and gas industry and the critical need for reliable communication infrastructure in remote and challenging environments. With a market size of 3.62 Billion in 2026 and projected to reach 5.00 Billion by 2033, the market demonstrates a healthy compound annual growth rate of 4.71%. Key findings indicate that the market is being shaped by the adoption of advanced communication technologies, the growing demand for managed services, and the increasing focus on operational efficiency and safety. The upstream segment continues to dominate due to extensive exploration and production activities, while onshore communications hold a larger share compared to offshore solutions. The market is characterized by technological advancements in communication networks, including the integration of 5G, satellite, and fiber-optic technologies. As the industry moves towards more connected and automated operations, the demand for robust, secure, and scalable communication solutions is expected to remain strong, presenting significant opportunities for market participants.

Oilfield Communications Market Forecast - Projections for 2025-2032 period

The Oilfield Communications Market is projected to experience steady growth throughout the 2025-2032 period, with the market expanding from its 2026 size of 3.62 Billion to reach 5.00 Billion by 2033. This growth trajectory represents a compound annual growth rate (CAGR) of 4.71%, indicating a stable and sustainable expansion of the market. The forecast period is expected to be characterized by continued investment in digital oilfield technologies, increasing offshore exploration activities, and the ongoing need for enhanced safety and operational efficiency measures. The adoption of advanced communication technologies, such as 5G networks and satellite communications, is anticipated to accelerate during this period, driven by the industry's push towards automation and real-time data analytics. The managed services segment is likely to see significant growth as oil and gas companies increasingly outsource their communication infrastructure management to specialized providers. Additionally, the market is expected to benefit from the recovery and stabilization of oil prices, which typically correlates with increased capital expenditure on communication and technology infrastructure.

Oilfield Communications Market Size and Share by Segmentation - Breakdown by {segmentData}

The Oilfield Communications Market is segmented by service, solution, field site, and communication network technology, each contributing to the overall market dynamics. In terms of services, the market is divided between Managed Services and Professional Services, with managed services gaining traction due to their ability to provide comprehensive, end-to-end solutions that reduce operational burden on oil companies. By solution, the market is categorized into Midstream, Downstream, and Upstream Communication Solutions, with the upstream segment typically holding the largest share due to extensive exploration and production activities requiring robust communication infrastructure. The field site segmentation reveals that Onshore Communications currently dominate the market, although Offshore Communications are growing as offshore exploration expands. Regarding communication network technology, the market is served by various solutions including Tetra Network, Fiber-Optic based Communication Network, Microwave Communication Network, Cellular Communication Network, and VSAT Communication Network, with VSAT and fiber-optic solutions being particularly crucial for remote and offshore locations. This segmentation highlights the diverse needs of the oil and gas industry and the importance of tailored communication solutions for different operational contexts.

Global Oilfield Communications Market Size and Share by Region - Geographic distribution

The global Oilfield Communications Market exhibits varied distribution across different regions, influenced by factors such as oil and gas reserves, exploration activities, technological adoption rates, and regulatory environments. North America, particularly the United States and Canada, represents a significant portion of the market due to extensive shale oil and gas operations, advanced technological infrastructure, and the presence of major oilfield communication providers. The Middle East and Africa region, with its vast oil reserves and ongoing exploration activities, constitutes another major market segment. Europe, while smaller in comparison, shows steady growth driven by offshore activities in the North Sea and increasing digitalization efforts. The Asia-Pacific region is emerging as a rapidly growing market, fueled by increasing energy demand, offshore exploration in countries like Australia and India, and investments in digital oilfield technologies. Latin America, with its significant offshore reserves, particularly in Brazil, presents growing opportunities for oilfield communication solutions. Each region presents unique challenges and opportunities, from harsh environmental conditions in Arctic regions to the need for advanced cybersecurity measures in areas with high geopolitical risks.

Regional Analysis of the Oilfield Communications Market - Detailed regional market performance

The regional performance of the Oilfield Communications Market varies significantly across different geographic areas, reflecting the unique characteristics and demands of each region's oil and gas industry. In North America, the market is driven by advanced shale operations, particularly in the Permian Basin, Eagle Ford, and Bakken formations, where operators require sophisticated communication networks to manage complex drilling and production activities. The region's focus on automation and digitalization further boosts demand for advanced communication solutions. The Middle East and Africa region, home to some of the world's largest oil producers, shows strong demand for both onshore and offshore communication systems, with a particular emphasis on reliable connectivity for remote desert and offshore installations. Europe's market is characterized by mature offshore operations in the North Sea, where aging infrastructure is being upgraded with modern communication technologies. The Asia-Pacific region presents a diverse landscape, with Australia's offshore LNG projects driving demand for satellite and microwave communications, while countries like China and India are investing in digital oilfield technologies to enhance their domestic production capabilities. Latin America, particularly Brazil with its pre-salt discoveries, represents a growing market for offshore communication solutions, while countries like Mexico are opening up to foreign investment, creating new opportunities for communication service providers.

Leading Company Profiles in the Oilfield Communications Market - Industry players and strategies

The Oilfield Communications Market is served by a diverse array of companies, each bringing unique strengths and strategies to the competitive landscape. ABB Ltd leverages its extensive experience in industrial automation and control systems to provide integrated communication solutions for oil and gas operations. Airspan Networks Inc. focuses on advanced wireless technologies, including 5G solutions tailored for oilfield applications. Baker Hughes Incorporated, a major oilfield services company, offers comprehensive communication solutions as part of its broader digital oilfield portfolio. Ceragon Networks Ltd. specializes in high-capacity wireless backhaul solutions crucial for remote oilfield sites. Commscope Holding Company, Inc. provides a wide range of networking and connectivity solutions adapted for harsh oilfield environments. Commtel Networks Pvt. Ltd. offers specialized communication systems designed specifically for the oil and gas industry's unique requirements. Huawei Technologies Co. Ltd. brings its global telecommunications expertise to the oilfield sector, offering advanced network solutions and 5G technology. Hughes Network Systems LLC is a leader in satellite communications, providing critical connectivity for ultra-remote locations. Inmarsat plc offers global satellite communication services essential for offshore operations. Nokia Corporation (Alcatel-Lucent) provides robust networking solutions and is actively involved in developing 5G applications for the oil and gas industry. Rad Data Communications specializes in network access solutions for critical infrastructure. RigNet, Inc. focuses exclusively on oilfield communication services, offering a range of solutions from basic connectivity to advanced digital oilfield applications. Siemens AG brings its industrial communication expertise to provide integrated solutions for oil and gas operations. Speedcast International Limited offers a broad portfolio of communication and IT services for remote and harsh environments. Tait Communications provides specialized radio communication systems designed for the demanding conditions of oil and gas operations. These companies employ various strategies, including technological innovation, strategic partnerships, geographic expansion, and service diversification, to maintain their competitive edge in the market.

Porter's Five Forces Analysis of the Oilfield Communications Market - Competitive forces assessment

The Oilfield Communications Market is characterized by a complex interplay of competitive forces as analyzed through Porter's Five Forces framework. The threat of new entrants is moderate due to the high capital requirements, need for specialized technical expertise, and strong relationships with oil and gas companies that existing players have established. However, the growing demand for advanced communication solutions and the industry's digital transformation present opportunities for new, innovative entrants. The bargaining power of buyers, primarily oil and gas companies, is significant as they often have multiple options for communication services and can negotiate based on the critical nature of these services to their operations. The bargaining power of suppliers is relatively low for standardized communication equipment but can be higher for specialized components or services. The threat of substitutes is low as the unique requirements of oilfield communications, particularly in remote and harsh environments, limit alternative solutions. Competitive rivalry is intense among existing players, driven by the need to offer differentiated services, maintain reliability in challenging conditions, and provide comprehensive solutions that integrate with digital oilfield technologies. This rivalry is further intensified by the trend towards managed services and the increasing importance of cybersecurity in communication solutions.

SWOT Analysis of the Oilfield Communications Market - Strengths, weaknesses, opportunities, threats

The Oilfield Communications Market presents a complex landscape of strengths, weaknesses, opportunities, and threats that shape its current state and future trajectory. Strengths of the market include the critical nature of communication services to oil and gas operations, ensuring consistent demand; the ability to provide solutions for harsh and remote environments where few alternatives exist; and the growing trend towards digitalization in the oil and gas industry, which increases the need for advanced communication infrastructure. Weaknesses include the high capital expenditure required for infrastructure development, the vulnerability of communication systems to extreme weather and environmental conditions, and the potential for cybersecurity breaches in critical infrastructure. Opportunities abound in the development of 5G and satellite communication technologies, the expansion of offshore exploration activities, and the increasing adoption of managed services that offer recurring revenue streams. The market also benefits from the growing emphasis on operational efficiency and safety in the oil and gas industry. Threats to the market include the volatility of oil prices affecting investment in communication infrastructure, increasing regulatory scrutiny on data security and environmental impact, and the potential for rapid technological obsolescence as new communication standards emerge. Additionally, the market faces challenges from the global push towards renewable energy, which could potentially reduce long-term demand for oil and gas communication solutions.

Oilfield Communications Market Value Chain Analysis - Industry structure and value flow

The Oilfield Communications Market value chain encompasses a series of interconnected activities that create and deliver value to end-users in the oil and gas industry. At the foundation of the value chain are raw material and component suppliers, providing essential elements such as semiconductors, networking hardware, and satellite components. These inputs flow to manufacturers of communication equipment, who produce specialized devices designed to withstand harsh oilfield environments. The next stage involves system integrators and solution providers who combine various technologies to create comprehensive communication packages tailored to specific oilfield needs. Service providers then offer these solutions to oil and gas companies, often through a combination of direct sales and partnerships with major oilfield service firms. Value is added at each stage through technological innovation, customization for specific operational requirements, and the integration of advanced features such as cybersecurity and data analytics capabilities. The distribution channel includes both direct sales to major oil companies and indirect sales through distributors and system integrators. After-sales services, including maintenance, upgrades, and technical support, represent a significant portion of the value chain, ensuring the reliability and longevity of communication systems in challenging environments. The value chain is characterized by strong interdependencies between stages, with innovation and quality improvements at one level often driving advancements throughout the chain. This interconnected structure emphasizes the importance of collaboration and strategic partnerships in delivering comprehensive, reliable communication solutions to the oil and gas industry.

Key Investment Insights in the Oilfield Communications Market - Strategic investment recommendations

The Oilfield Communications Market presents several compelling investment opportunities driven by the industry's ongoing digital transformation and the critical need for reliable communication infrastructure. Strategic investments should focus on companies developing advanced communication technologies specifically tailored for oilfield applications, particularly those working on 5G integration, satellite communications for ultra-remote locations, and hybrid network solutions that combine multiple technologies for enhanced reliability. There is significant potential in investing in managed services providers, as oil and gas companies increasingly seek to outsource their communication infrastructure management to reduce operational complexity and costs. Investments in cybersecurity solutions for oilfield communications are particularly attractive given the growing threat of cyber attacks on critical infrastructure. The market for satellite communications is expected to see substantial growth, driven by the expansion of offshore exploration and the need for connectivity in remote onshore locations, making this a key area for investment consideration. Additionally, companies focusing on the integration of artificial intelligence and machine learning for predictive maintenance and operational optimization in communication systems represent promising investment targets. Investors should also consider opportunities in firms developing communication solutions for emerging areas such as subsea operations and Arctic exploration, where traditional connectivity options are limited. As the industry moves towards more connected and automated operations, investments in companies that can provide end-to-end communication solutions, including hardware, software, and services, are likely to yield strong returns. However, potential investors should be mindful of the cyclical nature of the oil and gas industry and the impact of oil price volatility on capital expenditure for communication infrastructure.

Oilfield Communications Market Conclusion - Summary and key takeaways

The Oilfield Communications Market stands at a critical juncture, driven by the oil and gas industry's digital transformation and the increasing demand for reliable, advanced communication infrastructure in challenging environments. With a projected market size of 5.00 Billion by 2033, growing at a CAGR of 4.71% from 3.62 Billion in 2026, the market demonstrates steady and sustainable growth potential. Key takeaways from the market analysis include the critical role of communication technologies in enabling operational efficiency, safety, and the adoption of digital oilfield solutions. The market is characterized by technological advancements in areas such as 5G, satellite communications, and hybrid network solutions, addressing the unique challenges of oil and gas operations. The increasing trend towards managed services and the growing importance of cybersecurity in communication systems are reshaping the competitive landscape. While the market faces challenges such as high initial investment costs and the need for specialized expertise, the opportunities presented by offshore expansion, the integration of AI and IoT, and the development of solutions for emerging exploration areas provide a positive outlook. As the industry continues to evolve, companies that can offer comprehensive, reliable, and innovative communication solutions tailored to the specific needs of oil and gas operations are well-positioned for success in this dynamic market.

Research Methodology - How this research was conducted

The research for this Oilfield Communications Market report was conducted using a comprehensive methodology that combines primary and secondary research techniques to ensure accuracy and reliability of the findings. Primary research involved interviews with key industry stakeholders, including executives from leading oilfield communication companies, oil and gas operators, and technology experts. These interviews provided valuable insights into market trends, technological developments, and future outlook. Secondary research encompassed a thorough review of industry reports, company annual reports, press releases, and relevant publications from industry associations and regulatory bodies. Market size and forecast calculations were derived using a combination of top-down and bottom-up approaches, considering factors such as oil production volumes, exploration activities, and technological adoption rates across different regions. Data triangulation was employed to validate findings across multiple sources, ensuring the robustness of the market analysis. The research also incorporated an analysis of macroeconomic factors, oil price trends, and geopolitical developments that could impact the market. All data and projections were subjected to rigorous quality checks and reviewed by industry experts to ensure the highest level of accuracy and relevance for stakeholders in the Oilfield Communications Market.

Research Scope - Coverage and limitations

The research scope for this Oilfield Communications Market report encompasses a comprehensive analysis of the global market, covering key segments including services (Managed Services and Professional Services), solutions (Midstream, Downstream, and Upstream Communication Solutions), field sites (Onshore and Offshore Communications), and communication network technologies (Tetra Network, Fiber-Optic based Communication Network, Microwave Communication Network, Cellular Communication Network, and VSAT Communication Network). The report provides detailed coverage of major geographic regions, including North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America, with a focus on key countries driving market growth in each region. The scope includes an analysis of market drivers, restraints, opportunities, and challenges, as well as a competitive landscape featuring major industry players. The research covers the period from 2025 to 2032, with 2026 as the base year for market size calculations. While the report aims to provide a comprehensive view of the market, it is important to note certain limitations. The research is primarily focused on commercial communication solutions and does not extensively cover military or government-specific communication systems used in oil and gas operations. Additionally, the rapidly evolving nature of technology and potential geopolitical shifts may impact future market dynamics in ways that are difficult to predict with complete accuracy. The report also does not delve into the specific technical specifications of communication equipment, focusing instead on market-level analysis and trends.

Key Companies and Recent Developments in the Oilfield Communications Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Oilfield Communications Market is characterized by the presence of several key players who are driving innovation and shaping the industry's future through strategic initiatives and technological advancements. ABB Ltd has been focusing on expanding its digital solutions portfolio, with recent announcements emphasizing the integration of artificial intelligence in oilfield communication systems for enhanced predictive maintenance. Airspan Networks Inc. has made significant strides in 5G technology deployment for oil and gas applications, with recent product launches targeting improved connectivity in remote oilfield locations. Baker Hughes Incorporated has announced partnerships with major telecommunications companies to enhance its digital oilfield offerings, including advanced communication solutions for real-time data analytics. Ceragon Networks Ltd. has introduced new high-capacity wireless backhaul solutions designed specifically for the harsh environments of oil and gas operations. Commscope Holding Company, Inc. has recently expanded its product line with ruggedized networking equipment tailored for extreme oilfield conditions. Commtel Networks Pvt. Ltd. has announced the development of integrated communication and surveillance systems for offshore platforms, enhancing both connectivity and security. Huawei Technologies Co. Ltd. continues to invest in 5G applications for the oil and gas industry, with recent demonstrations of ultra-reliable low-latency communication (URLLC) for critical oilfield operations. Hughes Network Systems LLC has launched new satellite communication terminals with improved bandwidth and reliability for ultra-remote oilfield sites. Inmarsat plc has announced partnerships with oilfield service companies to provide global connectivity solutions for offshore exploration vessels. Nokia Corporation (Alcatel-Lucent) has introduced private wireless networks for oil and gas facilities, emphasizing enhanced security and reliability. Rad Data Communications has recently unveiled new network access solutions designed to improve the resilience of oilfield communication infrastructure. RigNet, Inc. has announced the acquisition of a cybersecurity firm to enhance its managed services portfolio with advanced threat protection. Siemens AG has launched integrated communication and automation solutions that combine operational technology with information technology for improved oilfield efficiency. Speedcast International Limited has announced the expansion of its satellite network capacity to support growing demand for high-bandwidth applications in offshore oil and gas operations. Tait Communications has introduced new digital radio systems with enhanced noise cancellation and extended range for use in challenging oilfield environments. These recent developments underscore the industry's focus on technological innovation, strategic partnerships, and the development of comprehensive solutions to meet the evolving needs of the oil and gas sector.