Dairy Alternatives Market Overview - Definition, scope, and significance

The Dairy Alternatives Market encompasses plant-based products designed to replace traditional dairy items, offering consumers non-dairy options derived from sources such as soy, almond, coconut, and oats. This market includes various product types including milk, ice cream, yogurt, and cheese alternatives that cater to growing consumer demand for lactose-free, vegan, and health-conscious food options. The significance of this market lies in its response to changing dietary preferences, rising health awareness, and increasing prevalence of lactose intolerance and milk allergies. As consumers become more conscious about animal welfare, environmental sustainability, and personal health, dairy alternatives have emerged as a mainstream category rather than a niche market, fundamentally reshaping the global food and beverage landscape.

Dairy Alternatives Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the Dairy Alternatives Market include growing health consciousness among consumers, increasing prevalence of lactose intolerance and dairy allergies, and rising adoption of vegan and plant-based diets. Environmental concerns about dairy farming's carbon footprint and animal welfare issues have also accelerated market growth. However, the market faces restraints such as higher prices compared to conventional dairy products, taste and texture differences that may deter some consumers, and potential allergen concerns with certain plant-based ingredients. Key challenges include overcoming consumer skepticism about nutritional equivalence, addressing supply chain complexities for raw materials, and navigating regulatory frameworks across different regions. Significant opportunities exist in product innovation, expansion into emerging markets, development of new plant-based sources, and leveraging e-commerce channels for broader market reach.

Dairy Alternatives Market Growth Trends - Current and emerging trends shaping the market

The Dairy Alternatives Market is experiencing several transformative growth trends that are reshaping the industry landscape. There is a notable shift toward oat-based products, which have gained substantial market share due to their neutral taste profile and sustainable production characteristics. Innovation in product formulations is creating more authentic taste experiences that closely mimic traditional dairy products, reducing the gap between conventional and alternative options. The market is also witnessing increased fortification with vitamins, minerals, and proteins to address nutritional concerns. Emerging trends include the development of novel plant sources such as hemp, pea, and quinoa, as well as functional dairy alternatives enriched with probiotics, prebiotics, and other health-promoting ingredients. Additionally, the rise of direct-to-consumer channels and subscription-based models is changing how products reach consumers, while clean label and minimal processing claims are becoming increasingly important differentiators.

COVID-19 Impact on the Dairy Alternatives Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a mixed impact on the Dairy Alternatives Market, initially causing supply chain disruptions and temporary retail closures that affected distribution. However, the pandemic ultimately accelerated market growth as consumers became more health-conscious and focused on immunity-boosting foods. Lockdowns and restaurant closures shifted consumption patterns toward home-based eating, benefiting retail sales of packaged dairy alternatives. E-commerce channels experienced significant growth as consumers turned to online shopping for groceries. The pandemic also heightened awareness about food safety and ingredient transparency, driving demand for products with clean labels and minimal processing. As recovery progresses, the market is witnessing sustained growth driven by continued health awareness, with many of the behavioral changes adopted during the pandemic becoming permanent, including increased preference for plant-based options and online purchasing channels.

Dairy Alternatives Market Competitive Landscape - Major competitors and market consolidation

The Dairy Alternatives Market features a competitive landscape characterized by both established food and beverage giants and innovative plant-based specialists. Major competitors include multinational corporations such as Danone S.A., Nestle SA, and Blue Diamond Growers, which leverage their extensive distribution networks and R&D capabilities to maintain market presence. Specialized companies like Oatly Inc, Califia Farms, and Alpro have gained significant market share through focused innovation and strong brand positioning in the plant-based segment. The market is experiencing increasing consolidation through mergers, acquisitions, and strategic partnerships as larger companies seek to strengthen their plant-based portfolios. Competition is intensifying around product innovation, taste quality, nutritional profile, and sustainability credentials, with companies investing heavily in research and development to create products that closely match or exceed the sensory experience of traditional dairy while offering superior health and environmental benefits.

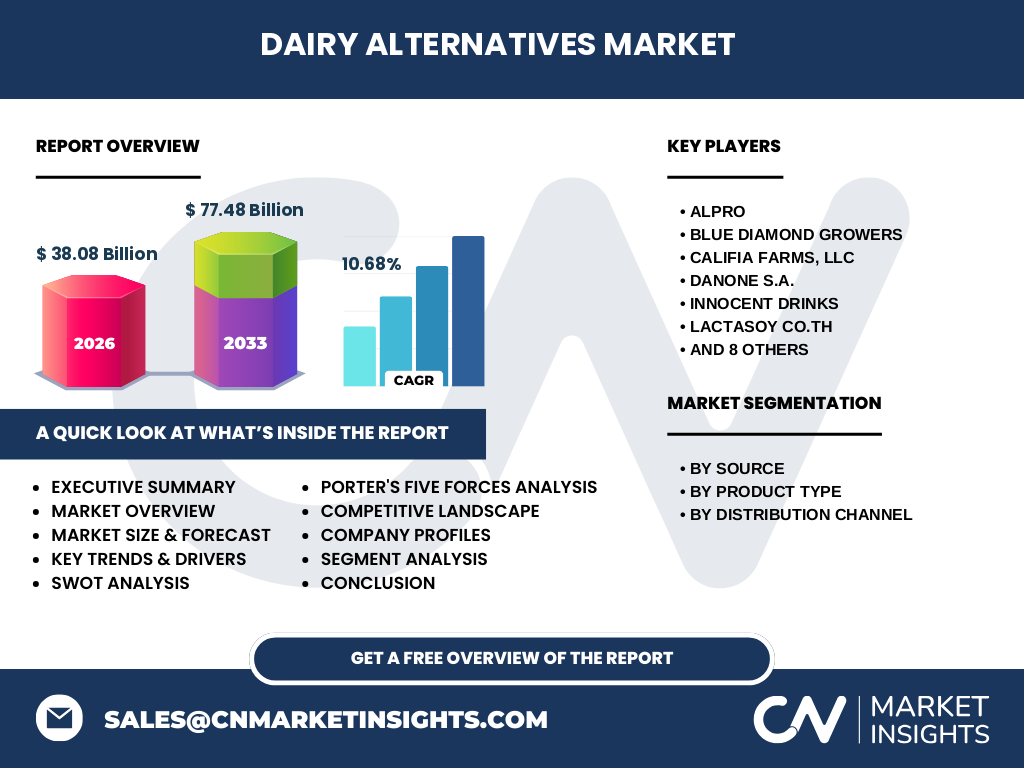

Executive Summary - High-level overview and key findings about Dairy Alternatives Market

The Dairy Alternatives Market represents a dynamic and rapidly evolving sector within the global food and beverage industry, driven by fundamental shifts in consumer preferences toward health, sustainability, and ethical consumption. With a market size of 38.08 Billion in 2026 and projected to reach 77.48 Billion by 2033, the market demonstrates robust growth at a CAGR of 10.68%. This expansion is fueled by increasing lactose intolerance, rising veganism, environmental concerns, and continuous product innovation that addresses taste and nutritional challenges. The market segmentation reveals diverse opportunities across different plant sources including soy, almond, coconut, and oats, with product categories spanning milk, ice cream, yogurt, and cheese alternatives. Distribution channels are evolving rapidly, with online retail gaining prominence alongside traditional supermarkets and convenience stores. The competitive landscape features a mix of established food corporations and specialized plant-based companies, creating a dynamic environment for innovation and market development.

Dairy Alternatives Market Forecast - Projections for 2025-2032 period

The Dairy Alternatives Market is positioned for substantial growth over the 2025-2032 period, with projections indicating significant market expansion driven by multiple converging factors. The market is expected to grow from 38.08 Billion in 2026 to 77.48 Billion by 2033, representing a compound annual growth rate of 10.68%. This robust growth trajectory reflects sustained consumer demand for plant-based alternatives, continued product innovation, and expanding distribution channels. Key growth drivers include increasing health consciousness, environmental sustainability concerns, and the rising prevalence of lactose intolerance and dairy allergies. The forecast period will likely see accelerated adoption in emerging markets, expansion of product portfolios to include new plant sources and functional ingredients, and increased investment in sustainable packaging solutions. Geographic expansion, particularly in Asia-Pacific and Latin American markets, is expected to contribute significantly to overall market growth, while developed markets will continue to see innovation-driven expansion.

Dairy Alternatives Market Size and Share by Segmentation - Breakdown by {segmentData}

The Dairy Alternatives Market segmentation reveals distinct patterns in consumer preferences and market dynamics across different categories. By source, the market is divided among soy, almond, coconut, and oats, with each source offering unique nutritional profiles, taste characteristics, and environmental impacts that appeal to different consumer segments. Product type segmentation shows milk alternatives currently dominating the market, followed by growing segments in ice cream, yogurt, and cheese alternatives as product formulations continue to improve. The distribution channel analysis indicates that supermarkets and hypermarkets remain the primary sales channels, though online retail is experiencing the fastest growth rate as e-commerce becomes increasingly integrated into grocery shopping habits. Each segment presents unique growth opportunities and challenges, with factors such as taste acceptance, price sensitivity, and nutritional perception varying significantly across different product categories and consumer demographics.

Global Dairy Alternatives Market Size and Share by Region - Geographic distribution

The global Dairy Alternatives Market exhibits distinct regional patterns in adoption, growth rates, and market maturity. North America and Europe currently represent the largest markets, driven by high health consciousness, established distribution networks, and strong consumer acceptance of plant-based diets. These regions benefit from higher disposable incomes and sophisticated retail infrastructure that supports premium product offerings. Asia-Pacific represents the fastest-growing region, fueled by large populations, rising health awareness, and increasing lactose intolerance prevalence in countries like China and Japan. Latin America and Middle East & Africa are emerging markets showing promising growth potential as Western dietary trends influence local consumption patterns and disposable incomes rise. Regional differences in taste preferences, cultural dietary norms, and regulatory environments create both opportunities and challenges for market expansion, with companies needing to adapt their strategies to local market conditions and consumer preferences.

Regional Analysis of the Dairy Alternatives Market - Detailed regional market performance

Regional analysis of the Dairy Alternatives Market reveals significant variations in market maturity, growth drivers, and consumer preferences across different geographic areas. In North America, particularly the United States and Canada, the market benefits from high health consciousness, strong vegan and vegetarian populations, and sophisticated retail infrastructure supporting premium product offerings. Europe demonstrates similar characteristics with additional emphasis on sustainability and organic certification, particularly in countries like Germany, the UK, and the Nordic nations. The Asia-Pacific region presents unique opportunities driven by large populations, rising middle-class incomes, and increasing awareness of lactose intolerance, though cultural preferences for traditional dairy products create both challenges and opportunities for market penetration. Latin America shows growing adoption influenced by health trends and environmental awareness, while the Middle East & Africa region represents an emerging market with potential for growth as Western dietary influences spread and local production capabilities develop.

Leading Company Profiles in the Dairy Alternatives Market - Industry players and strategies

The Dairy Alternatives Market features a diverse array of companies ranging from multinational food corporations to specialized plant-based innovators, each employing distinct strategies to capture market share. Danone S.A. has positioned itself as a leader through strategic acquisitions and extensive R&D investment in plant-based products. Nestle SA leverages its global distribution network and brand recognition to expand its dairy alternatives portfolio across multiple product categories. Specialized companies like Oatly Inc have achieved rapid growth through focused innovation, strong brand identity, and effective marketing that resonates with millennial and Gen Z consumers. Blue Diamond Growers capitalizes on its almond expertise to maintain leadership in almond-based products, while Califia Farms differentiates through premium positioning and innovative packaging. These companies employ various strategies including product innovation, sustainable sourcing, strategic partnerships, and geographic expansion to strengthen their market positions and meet evolving consumer demands for taste, nutrition, and environmental responsibility.

Porter's Five Forces Analysis of the Dairy Alternatives Market - Competitive forces assessment

Porter's Five Forces analysis of the Dairy Alternatives Market reveals a dynamic competitive environment shaped by several key factors. The threat of new entrants remains moderate to high due to relatively low barriers to entry in terms of production technology, though established brands benefit from strong consumer loyalty and distribution advantages. Bargaining power of suppliers varies by ingredient type, with some plant sources having concentrated supply chains while others offer more supplier diversity. The bargaining power of buyers is increasing as consumers become more informed and have access to multiple product options through expanding retail channels. Threat of substitutes exists from both traditional dairy products and other plant-based alternatives, creating ongoing competitive pressure. Competitive rivalry is intense among both established food companies and specialized plant-based brands, driving continuous innovation in product development, marketing, and sustainability initiatives. Overall, the market structure encourages ongoing innovation and strategic positioning as companies compete for growing but increasingly discerning consumer segments.

SWOT Analysis of the Dairy Alternatives Market - Strengths, weaknesses, opportunities, threats

A comprehensive SWOT analysis of the Dairy Alternatives Market reveals significant strategic insights for industry participants. Strengths include strong consumer demand driven by health and sustainability trends, continuous product innovation improving taste and texture, and expanding distribution channels reaching broader consumer segments. Weaknesses encompass higher price points compared to conventional dairy, occasional nutritional concerns regarding protein content and fortification, and challenges in achieving authentic dairy-like sensory experiences. Opportunities are abundant in emerging markets with growing middle classes, development of novel plant sources and functional ingredients, and expansion into new product categories beyond traditional alternatives. Threats include potential regulatory changes affecting labeling and health claims, supply chain vulnerabilities for key plant ingredients, and competitive pressure from both traditional dairy companies launching their own alternatives and other plant-based beverage categories. The analysis suggests that companies focusing on innovation, quality, and strategic market expansion are best positioned to capitalize on the market's growth potential while mitigating inherent risks.

Dairy Alternatives Market Value Chain Analysis - Industry structure and value flow

The Dairy Alternatives Market value chain encompasses multiple stages from raw material sourcing through final consumption, each contributing distinct value and facing unique challenges. The chain begins with agricultural production of plant sources including soy, almonds, oats, and coconuts, where factors such as crop yields, water usage, and geographic concentration affect supply stability and pricing. Processing and manufacturing stages involve converting raw materials into finished products through techniques that preserve nutritional content while achieving desired taste and texture profiles. Distribution channels have evolved to include traditional retail, specialty health food stores, and rapidly growing e-commerce platforms, each requiring different logistics and marketing approaches. Marketing and branding play crucial roles in educating consumers and building brand loyalty in a category where taste and nutritional perception remain key purchase drivers. The value chain is characterized by ongoing innovation at multiple stages, with companies investing in sustainable sourcing, clean label formulations, and efficient production methods to enhance competitiveness and meet evolving consumer expectations.

Key Investment Insights in the Dairy Alternatives Market - Strategic investment recommendations

Strategic investment insights for the Dairy Alternatives Market highlight several compelling opportunities for stakeholders seeking to capitalize on this growing sector. Investment in R&D for product innovation represents a critical area, particularly in developing improved taste profiles, enhanced nutritional fortification, and novel plant sources that address current market limitations. Expansion into emerging markets offers significant growth potential, especially in Asia-Pacific and Latin American regions where rising incomes and health consciousness are driving demand. Investment in sustainable production and packaging technologies aligns with growing consumer environmental concerns and can provide competitive differentiation. The e-commerce channel presents attractive investment opportunities as online grocery shopping continues to gain market share, requiring investments in digital marketing, direct-to-consumer platforms, and efficient fulfillment systems. Strategic acquisitions of innovative smaller brands can provide quick access to new technologies, consumer segments, and geographic markets. Overall, successful investment strategies will focus on innovation, sustainability, and market expansion while addressing the evolving needs of health-conscious and environmentally aware consumers.

Dairy Alternatives Market Conclusion - Summary and key takeaways

The Dairy Alternatives Market represents a compelling growth opportunity within the global food and beverage industry, characterized by strong consumer demand, continuous innovation, and expanding market reach. With a projected market size of 77.48 Billion by 2033 and a robust CAGR of 10.68%, the sector demonstrates significant potential for continued expansion across multiple product categories and geographic regions. Key success factors include product quality improvements that address taste and texture concerns, effective marketing that communicates health and environmental benefits, and strategic expansion into emerging markets with rising health consciousness. The competitive landscape features both established food giants and specialized plant-based companies, creating a dynamic environment for innovation and market development. As consumers increasingly prioritize health, sustainability, and ethical consumption, dairy alternatives are well-positioned to capture growing market share, though companies must navigate challenges related to pricing, nutrition, and supply chain complexity to fully realize the market's potential.

Research Methodology - How this research was conducted

The research methodology for this Dairy Alternatives Market analysis employed a comprehensive approach combining multiple data collection and analysis techniques to ensure accuracy and reliability. Primary research involved interviews with industry experts, company executives, and market participants to gather firsthand insights into market trends, challenges, and opportunities. Secondary research utilized extensive review of company annual reports, industry publications, market databases, and government statistics to establish baseline market data and identify historical trends. Data triangulation techniques were applied to validate findings across multiple sources, while market size calculations incorporated both top-down and bottom-up approaches for enhanced accuracy. The analysis considered various market dynamics including economic indicators, consumer behavior trends, regulatory environments, and competitive landscape factors. Forecasting methodologies incorporated compound annual growth rate calculations, scenario analysis, and consideration of macroeconomic factors to project market development through 2033. This rigorous methodology ensures that the findings provide a reliable foundation for strategic decision-making in the dairy alternatives sector.

Research Scope - Coverage and limitations

The research scope for this Dairy Alternatives Market analysis encompasses a comprehensive examination of the global market from 2026 through 2033, focusing on key product categories, distribution channels, and geographic regions. The study covers major plant sources including soy, almond, coconut, and oats, along with product types such as milk, ice cream, yogurt, and cheese alternatives. Geographic coverage includes North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa regions, though the depth of analysis may vary by region based on data availability and market significance. The research focuses on commercial market dynamics and excludes certain niche or artisanal segments that may exist outside mainstream commercial channels. Limitations include potential variations in data quality across different regions and product categories, the challenge of tracking informal or unbranded market segments, and the inherent uncertainty in long-term market forecasting. Additionally, rapid technological and consumer preference changes may affect the accuracy of projections beyond the immediate forecast period. Despite these limitations, the research provides a robust framework for understanding market dynamics and identifying strategic opportunities in the dairy alternatives sector.

Key Companies and Recent Developments in the Dairy Alternatives Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Dairy Alternatives Market features several key companies driving innovation and market expansion through strategic initiatives and product development. Danone S.A. has strengthened its position through acquisitions of plant-based brands and investment in sustainable packaging solutions, while launching new product lines targeting specific consumer segments. Nestle SA has expanded its dairy alternatives portfolio with innovative formulations and entered partnerships to enhance its plant-based offerings across multiple geographic markets. Oatly Inc has achieved significant market penetration through successful IPOs, expansion into new product categories, and strategic retail partnerships that have increased its global presence. Califia Farms continues to differentiate through premium positioning, innovative packaging, and expansion into functional beverages enriched with probiotics and adaptogens. Blue Diamond Growers maintains leadership in almond-based products while investing in sustainable almond farming practices and developing new flavor profiles. These companies, along with others such as Alpro, Rude Health, and Valio Ltd., are shaping the market through continuous innovation, strategic partnerships, and expansion into emerging markets, creating a dynamic competitive landscape that benefits consumers through improved product quality and variety.